DEEP RESEARCH · Yellow Balloon

Yellow Balloon (A104620): 2025 Results and 2026 Sustainability Check

Breaking down the 4Q25 operating-profit rebound through P/Q/C, TMON-Wemakeprice allowance reversal, FX risk, and mezzanine overhang

0. Bottom line first

My conclusion on Yellow Balloon is Medium / Accumulate on pullbacks. The 4Q25 rebound appears to be a mix of genuine operating repair from mobile, direct procurement, and premium products, plus a possible partial reversal of the roughly KRW 3.8 billion allowance booked conservatively during the 2024 TMON-Wemakeprice settlement crisis. That is why annualizing 4Q25 operating profit into 2026 normalized operating profit would be dangerous.

Medium / Accumulate

The KRW 4,100~4,500 zone is close to three- and five-year lows, giving some downside rigidity, but a sharp near-term rally still looks capped.

Mobile 42.8%

The mobile booking share for the recent one-year period in 2025 rose to 42.8%, more than 20 percentage points above 2019.

About KRW 7.4bn

Roughly KRW 4.4bn of CBs and KRW 3.0bn of BWs remain, with the floor-refixed conversion/exercise price of KRW 5,745 acting as a share-price ceiling.

Official fact: The source summarizes Yellow Balloon's confirmed 3Q25 revenue at KRW 25.01 billion, down 30.9% year over year, with an operating loss of KRW 2.18 billion. It also states that Korean residents' overseas card spending in 3Q25 reached USD 5.93 billion, up 7.3% quarter over quarter and a record high, while HanaTour and ModeTour outbound travelers fell 2.2% and 31.2% year over year, respectively.

Interpretation: Travel spending itself did not disappear; the portion captured by package agencies was shaken by FIT migration and high FX. Yellow Balloon is trying to fill that gap with premium long-haul products, active seniors, direct mobile acquisition, and direct procurement, but FX and mezzanine supply still press down on the 2026 valuation ceiling.

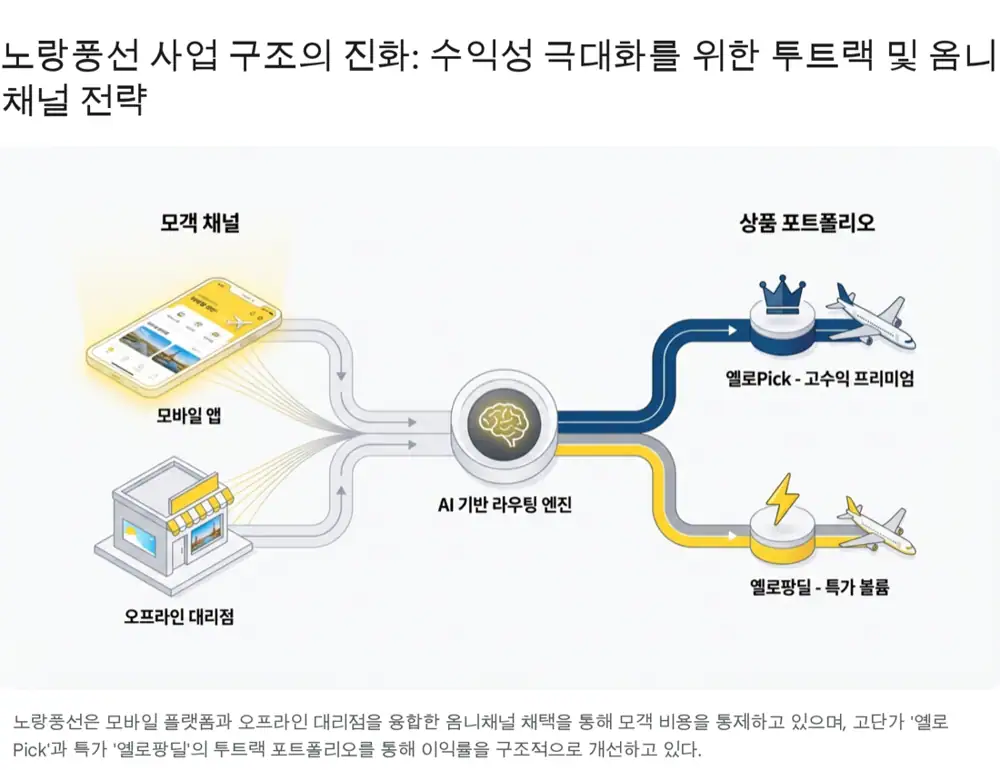

1. Business Structure: From Direct B2C to a Platform-Style Travel Agency

Korea's outbound travel industry traditionally relied on a B2B2C indirect sales structure: wholesale travel companies built products, while offline retail agencies recruited customers. Yellow Balloon grew from the beginning as a direct-to-consumer B2C agency, reducing unnecessary distribution commissions. As the post-pandemic market shifted from group packages to FIT and small customized theme trips, the company's change can be summarized in two pillars: a bifurcated product portfolio and omnichannel digital transformation.

Two-track product portfolio

| Axis | Source evidence | What it means to me |

|---|---|---|

| Yellow Pang Deal | Ultra-low-price short-haul promotions such as a 3-day Dalian package around KRW 360,000 and a 3-day Yantai package around KRW 160,000. | Margins are low, but the products function as loss leaders that drive platform traffic and new customer data. |

| Yellow Pick | Spain/Portugal 9~11 day packages priced at KRW 2.19mn~4.78mn, and Eastern/Northern Europe products at KRW 3.25mn~3.89mn. | Direct Korean Air/Asiana flights, 4~5-star hotels, Santiago pilgrimage themes, and no-option/no-shopping structures raise ASP and become a core profit source. |

Official fact: The source states that the mobile booking share reached 42.8% for the recent one-year period in 2025 and rose by more than 20 percentage points from 2019. It also says the company revamped its main homepage UI/UX in 2H24 and introduced AI-based personalized product recommendations.

Interpretation: Mobile migration is a cost-structure change that lowers external OTA/portal commissions and CAC. At the same time, expanding company-branded offline agencies from roughly 80 to 200 by 2026 looks contradictory only on the surface; it is an O2O strategy to retain senior and VIP customers who want face-to-face counseling before buying packages worth several million won.

2. Why 4Q25 Rebounded: A P/Q/C Breakdown

Through 3Q25, high KRW/USD rates and weak domestic consumption pressured package agencies. In 4Q, however, bridge-holiday seasonality, premium products, and cost controls worked together and created the opening for a turnaround. I break that down into price (P), quantity (Q), and cost (C).

ASP step-up

High-ticket long-haul packages such as Spain/Portugal at KRW 2.19mn~4.78mn, plus no-option/no-shopping premium mix, lifted unit price.

Seniors and destinations

Customers aged 70+ rose about 77% year over year; Beijing and Shanghai searches rose 5x and 4x, while North America and other new interest regions rose more than 80%.

Platform and direct procurement

Direct mobile acquisition reduces commissions and CAC, while direct procurement can improve margin by up to about 3% of package sales.

P: Expanding the premium mix

The old package market depended on low-price volume competition on identical routes. In 2025, Yellow Balloon avoided pure volume competition and chose a route that raised ASP. Passing through global inflation and higher jet-fuel costs required an upgrade in product quality, so the company emphasized national-carrier flights, premium city-center hotels, special meals, and no-option/no-shopping structures to reduce resistance to higher prices. The source frames this as similar to ModeTour's premium brand strategy with ModeTour Signature.

Q: Active seniors and destination reallocation

FX pressure and FIT adoption threatened the outbound traveler volume captured by traditional travel agencies. Yellow Balloon found a defense line in active seniors in their 60s and 70s. In its 1H25 internal log and payment data, customers aged 70+ rose about 77% year over year. This group prefers safe, comfortable, curated premium packages over difficult FIT trips where they must handle booking and itinerary control themselves.

- Destination diversification: Demand shifted away from excessive Japan/Southeast Asia concentration toward China, Greater China, and North America. Beijing and Shanghai package searches rose 5x and 4x year over year, while demand for North America and other new interest regions rose more than 80%.

- Companion-pattern change: Large family packages declined, while trips by friends and couples in their 20s to 40s, women-only or men-only groups, and groups of 16+ alumni or clubs increased.

- Semi-packages: Combining only airfare and hotels, or packaging only part of the itinerary, keeps FIT-leaning customers inside the company's ecosystem.

C: Deep cost-structure innovation

Typical small and mid-sized travel agencies depend on portals such as Naver/Kakao or OTAs such as Yanolja/Agoda and pay large traffic commissions. Yellow Balloon improved booking convenience on its own app and website, added easy payment, and revamped UI, helping lock in seniors in their 50s and 60s digitally. As a result, mobile bookings rose to 42.8% of total acquisition in 2025, lowering CAC and SG&A burden.

Official fact: Citing Korea IR Council's corporate research center, the source says direct procurement of core local infrastructure such as hotels, vehicles, and restaurants is estimated to have improved the margin in travel-arrangement revenue by up to about 3% of package sales.

Interpretation: Since travel agencies usually operate with single-digit operating margins, a 3 percentage point cost-ratio improvement is meaningful. It is the main reason I accept that there was real operating-strength improvement behind the 4Q rebound.

3. The Optical Boost in 4Q25 Operating Profit: TMON-Wemakeprice Allowance Reversal

Viewing the 4Q25 profit surge as pure fundamental improvement is risky. The source highlights a possible large allowance reversal related to the TMON-Wemakeprice settlement delay as a key variable.

During the July-August 2024 settlement crisis at TMON and Wemakeprice, Yellow Balloon decided to operate July departures regardless of whether PG companies or TMON-Wemakeprice paid the company, and it waived cancellation penalties for customers scheduled to depart from August onward who wanted to cancel. This protected brand trust, but the company pre-booked roughly KRW 3.8 billion of bad-debt expense for unsettled receivables and customer support costs. The source presents this as the direct factor that pushed 1H24 results into a KRW 2.5 billion loss.

Interpretation: If legal relief, financial-authority support, guarantee insurance, or PG responsibility settlements later make partial cash recovery possible, accounting can produce a bad-debt allowance reversal. The source argues that as legal arrangements progressed in 2H25, a meaningful portion of the KRW 3.8 billion allowance may have reversed into 4Q25. For 2026 normalized operating profit, this non-recurring item must be adjusted out.

4. 2026 Sustainability: Partially Sustainable

I classify 2026 earnings sustainability as Medium Sustainability. Mobile platform migration, senior demand, and direct procurement are structural. TMON-Wemakeprice reversals and pent-up travel demand are unlikely to repeat.

| Type | Factor | Meaning for 2026 |

|---|---|---|

| Structural positive | Senior mobile lock-in | Customers in their 60s and 70s feel high switching costs once a brand and platform are proven. The source treats their mobile booking share exceeding 45% as a generational lifestyle shift. |

| Structural positive | AI/IT efficiency | The 2H25 UI/UX overhaul and AI personalization raise conversion and reduce SG&A such as performance marketing and call-center labor. |

| Structural positive | Direct infrastructure procurement | Direct control and bulk purchasing of air blocks, global-chain hotels, and local transport can defend a structurally 2~3 percentage point higher margin than competitors. |

| Fading factor | Allowance reversal | The TMON-Wemakeprice-related reversal that inflated 4Q25 should not recur after year-end closing. 2026 year-over-year headline profit growth may look optically slower. |

| Fading factor | Pent-up demand normalization | Abnormal growth such as the 80% surge in China/US searches in 2025 is likely to mean-revert toward low-single-digit growth in 2026. |

5. Key Risks: FX and Overhang

KRW/USD around 1,400

Dollar-based fuel surcharges, hotels, and meals pressure won-based cost of sales and margins.

FIT counterattack

Millennial and Gen Z travelers may use Skyscanner, Agoda, Klook, and other tools to save even KRW 10,000~20,000 in agency fees.

KRW 5,745 ceiling

The floor-refixed CB/BW price of KRW 5,745, roughly KRW 7.4bn balance, and 8.1% of listed shares can become selling supply when the stock rises.

5.1 High FX and FIT conversion

Overseas card spending hit a record in 3Q25, yet package outbound travelers were weak. The source interprets this not as the death of travel spending, but as consumers moving from agency packages to direct booking. If KRW/USD threatens and stays near the 1,400 level, fuel surcharges and local expenses rise, while price-sensitive consumers may choose complete FIT to save even KRW 10,000~20,000 of agency commission.

5.2 CB/BW overhang

In March 2021, Yellow Balloon raised mezzanine funding with KRW 10 billion of convertible bonds and KRW 10 billion of bonds with warrants, for KRW 20 billion in total. By end-2025, much had been repaid or converted, but around KRW 4.4 billion of CBs and KRW 3.0 billion of BWs, or about KRW 7.4 billion of potential selling supply, remained.

- Conversion/exercise price: Refixed down to the legal floor of KRW 5,745.

- Trading range: In early 2026, the stock moved in a KRW 4,150~5,110 box.

- Dilution pressure: If the stock approaches KRW 5,745, bondholders have greater incentive to exercise and sell. The source sizes the potential supply at 8.1% of listed shares.

- Practical meaning: This is the 2026 glass ceiling that lowers expectations for a break above KRW 6,000.

6. Final Judgment: A Small but Solid Turnaround

My final view is Medium / Hold and accumulate gradually on pullbacks. I cannot call it a strong buy because of KRW/USD pressure around 1,400 and roughly KRW 7.4 billion of mezzanine overhang. I also cannot call it a sell because the KRW 4,100~4,500 stock range already reflects much of the three- and five-year low, close to the COVID-crisis level.

| Upside case | Counterargument |

|---|---|

| The company has moved from an old B2B travel agency model to a platform-style agency with 40%+ mobile direct acquisition, direct local procurement, and AI personalization. | A strong dollar and the FIT megatrend can structurally cap long-term package-agency revenue growth. |

| Customers in their 60s and 70s are locked in, while KRW 3mn+ Yellow Pick long-haul premium products help defend margins. | Younger consumers may view the 10~20% margin taken by package agencies as an unnecessary intermediary cost. |

| The stock has fallen more than 70~80% from its historical high of KRW 21,450, and losses plus the KRW 3.8bn TMON-Wemakeprice bad-debt issue appear substantially priced in. | Until the KRW 5,745 conversion/exercise price and roughly KRW 7.4bn, 8.1%-of-shares overhang are absorbed, rerating remains limited. |

Interpretation: Yellow Balloon is a turnaround company that has partly removed financial damage and has shifted toward digital innovation and profitability-first operations since 4Q25. In 2026, the key is not blind revenue growth but efficiency from AI and direct procurement. I would continue tracking mezzanine absorption and approach the KRW 4,100~4,500 bottom band through staggered buying rather than chasing rallies.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224221615064

- Yellow Balloon 2025 Business Report DART PDF: 노랑풍선_2025사업보고서_DART.pdf

- Daum Zoom-in stock article: https://v.daum.net/v/6JkWaMRu3F?f=p

- Discovery News: https://www.discoverynews.kr/news/articleView.html?idxno=1054385

- Econovill: https://www.econovill.com/news/articleView.html?idxno=675348

- MoneyToday: https://www.mt.co.kr/stock/2024/07/25/2024072515353540435

- Hitchhickr: https://www.hitchhickr.com/outbound_travel_industry_2025_3q/

- Judal 2026.01.08: https://www.judal.co.kr/?view=stockAI&shareToken=ExYIpmwpaaR77s16

- Toss Securities disclosure: https://www.tossinvest.com/stocks/A104620/news?menu=disclosure&symbol-or-stock-code=A104620&contentType=disclosure&contentParams=%7B%22id%22%3A%22DART%3AA%3A104620-20251114002196%22%2C%22companyCode%22%3A%22104620%22%2C%22reportItem%22%3A%224.2.0%22%7D

- YouthDaily: https://www.youthdaily.co.kr/news/article.html?no=196219

- ONews: https://www.onews.tv/news/articleView.html?idxno=226943

- LawIssue: https://www.lawissue.co.kr/view.php?ud=20240725214541179204ead0791_12

- Shinailbo: https://www.shinailbo.co.kr/news/articleView.html?idxno=1908481

- Judal 2026.03.16: https://www.judal.co.kr/?view=stockAI&shareToken=r6zYSL2FbvgGKEid

- Judal 2026.03.07: https://www.judal.co.kr/?view=stockAI&shareToken=s8UERdQY42MsmIdH

- Judal 2025.12.15: https://www.judal.co.kr/?view=stockAI&shareToken=5zA5Q692tYEGsMb3