DEEP RESEARCH · SOLID

SOLiD: Telecom Equipment Supercycle and 4Q Turnaround

A 2025 4Q results report linking DAS, Open RAN, North American capex, financial strength, and treasury-share cancellation

0. Bottom line first

The question for SOLiD is whether leverage turns back on after surviving a long capex drought. The source treats the February 2026 North American DAS contract worth USD 11,854,114, about KRW 17.17B, and 2026E operating profit of KRW 35.9B as evidence of a turnaround.

Official fact: SOLiD was founded in November 1998 and listed on KOSDAQ in July 2005. Its core businesses are DAS repeaters, fronthaul optical transmission equipment, Open RAN O-RU, and defense communication systems.

Interpretation: Results slowed through 3Q25 because of weak telecom capex, but the source argues that North American shipment recovery and deferred demand started converting into earnings in 4Q25.

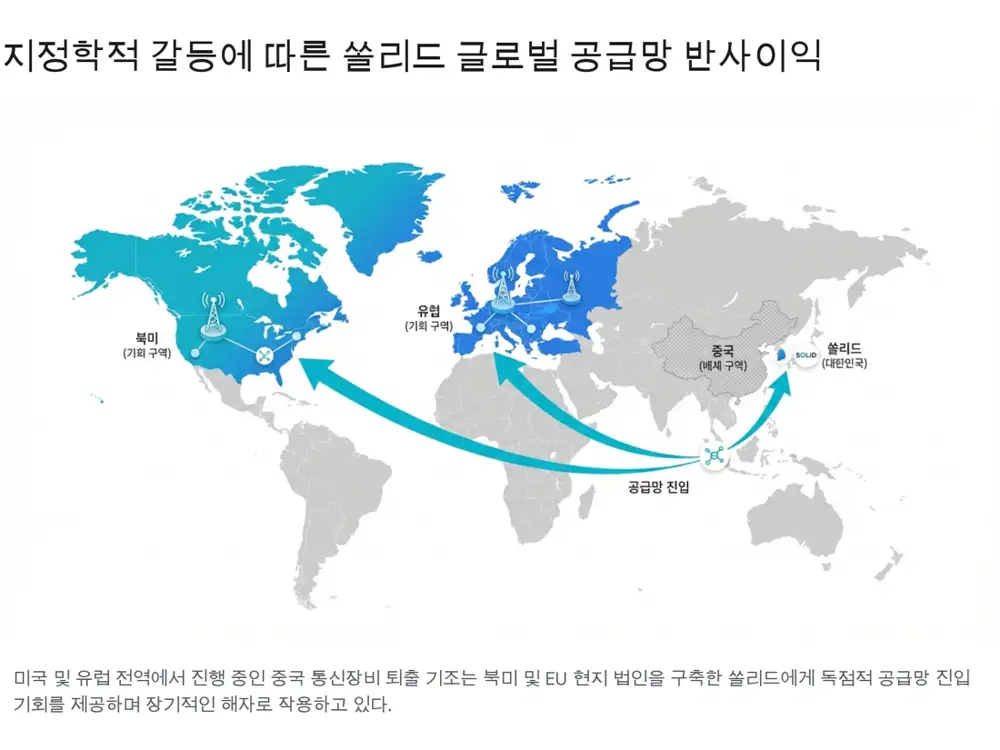

1. Business Model and Macro Inflection

The source presents four telecom-infrastructure inflection points: AT&T's roughly KRW 370T five-year capex plan, 5G SA and AI-RAN for Physical AI, U.S. spectrum auctions including the 800 MHz band in 2026, and the removal of Chinese telecom equipment and optical components such as Huawei and ZTE.

In-building coverage

Because the source assumes more than 70% of wireless data traffic occurs indoors, indoor shadow-area coverage is essential for 5G and 6G.

First K-OTIC certification

The source says SOLiD received Korea's first international certification for its O-RU in April 2024.

North America, Europe, Japan

Local entities and the Tessco partnership form the sales channel in key developed markets.

SOLiD Wintech

The subsidiary covers TICN, TMMR, tactical mobile-network repeaters, and next-generation military satellite communication equipment.

2. Diversification and Technology Moat

- SOLiD targets both large public venues and middleprise commercial buildings through SOLiD ALLIANCE, SOLiD GENESIS, and SOLiD BARS.

- In December 2024, subsidiary SOLID GEAR won the U.S. federal NOFO2 award, adding a public-infrastructure reference.

- In April 2025, SOLiD was selected as the lead organization for a low-earth-orbit communication satellite project by Korea's Ministry of Science and ICT.

- On January 31, 2026, it acquired 50.001% of Darwin Friction for KRW 10B, equal to 3.1% of equity, adding a bridge between railway and aviation brake controls and ultra-low-latency wireless control.

- The source presents SOLiD as the No. 3 global in-building DAS supplier with a 15.1% share.

Interpretation: I would not read it as a simple repeater maker. It is a communications-infrastructure portfolio spanning in-building DAS, O-RU, optical transmission, defense, satellite communication, and smart-mobility control.

3. Turnaround and Operating Leverage

| Item | 2024 1Q-3Q | 2025 1Q-3Q | 2026E |

|---|---|---|---|

| Revenue | KRW 240.9B | KRW 181.9B | KRW 308.8B |

| Operating profit | KRW 23.1B | KRW 7.1B | KRW 35.9B |

| OP margin | 9.5% | 3.9% | 11.6% |

Official fact: The source gives cumulative 3Q25 consolidated net income of KRW 9.2591B and profit attributable to controlling shareholders of KRW 9.3264B.

The February 24, 2026 North American DAS supply contract is worth USD 11,854,114, about KRW 17.17B. It equals 5.19% of 2024 revenue of KRW 331.0B, and runs from February 23, 2026 to February 27, 2027. The source also mentions North American backlog of USD 22.77M, about KRW 30B, at the end of 3Q25.

Interpretation: Q is North American DAS and O-RU shipments, P is mix-up toward AI-RAN, 5G mmWave, and 6G NTN, and C is fixed-cost discipline proven by profitability through 2022~2024.

4. R&D, Financial Strength, and Shareholder Returns

| Item | Source figure | Meaning |

|---|---|---|

| Cumulative 3Q25 R&D | KRW 31.95024B | 17.6% of revenue, up 6.5 percentage points from 11.1% a year earlier |

| Cash and cash equivalents | KRW 88.95532B | More than KRW 117.8B of liquidity including short-term financial instruments |

| Total borrowings | KRW 93.233B | Net debt of only KRW 4.27767B |

| Capital procurement ratio | 1.31% | The source reads this as nearly debt-free |

| Return action | Timing | Size | Source read |

|---|---|---|---|

| 1st treasury cancellation | August 2024 | 126,409 common shares | First step to lift per-share value |

| 2nd treasury cancellation | September 2025 | 338,697 common shares, about KRW 2.2B | Continuity of shareholder returns |

| New trust contract | March 13, 2026 | KRW 1.764B, about 142,258 shares estimated | All acquired shares intended for cancellation |

5. Valuation and Catalysts

The source cites estimated PER of 17.19x and PBR of about 1.43x on 2026E operating profit of KRW 35.9B. It also includes a view that a 12-month target price of KRW 20,000, roughly PBR 3x, is conservative for a No. 3 global in-building DAS company, and that fair market cap should be at least KRW 1T, implying more than 78% upside from the then-current price.

- Sequential U.S. and European orders: the February 2026 North American KRW 17.2B contract is framed as the first signal.

- Open RAN deployment after K-OTIC certification: real network deployment of O-RU could re-rate SOLiD as an AI-RAN player.

- Treasury purchases and cancellation: the KRW 1.76B trust contract and further return policy are treated as supply-demand catalysts.

- Risks to monitor: delayed global carrier capex, intensifying Open RAN competition, and price pressure from low-cost hardware entrants.

6. My Conclusion

The source strongly frames SOLiD as an early-cycle telecom equipment candidate. I read the core evidence as a combination of North American DAS orders, K-OTIC O-RU certification, a lower fixed-cost base, net debt of only about KRW 4.3B, and ongoing treasury-share cancellation.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224217161023

- Source 2: https://www.newsworks.co.kr/news/articleView.html?idxno=822521

- Source 3: https://www.datatooza.com/article/20251114131109979edd30f73a8_80

- Source 4: https://www.etoday.co.kr/news/view/1721991

- Source 5: https://www.ksdaily.co.kr/news/articleView.html?idxno=104328

- Source 6: https://comp.wisereport.co.kr/company/c1010001.aspx?cmp_cd=050890

- Source 7: https://m.etnews.com/20260225000045?obj=Tzo4OiJzdGRDbGFzcyI6Mjp7czo3OiJyZWZlcmVyIjtOO3M6NzoiZm9yd2FyZCI7czoxMzoid2ViIHRvIG1vYmlsZSI7fQ%3D%3D

- Source 8: https://jasoseol.com/companies/2352/insights

- Source 9: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20251113001109&docno=&viewerhost=&

- Source 10: https://magazine.hankyung.com/business/article/202603114900b

- Source 11: https://www.etnews.com/20260205000023

- Source 12: http://www.dailystock.co.kr/news/articleView.html?idxno=33044

- Source 13: https://www.digitaltoday.co.kr/aigongsi/4488/solid-darwinfriction-stake-acquisition

- Source 14: https://www.junggi.co.kr/news/articleView.html?idxno=35725

- Source 15: https://www.newspim.com/news/view/20251021000097

- Source 16: https://m.irgo.co.kr/IR%EC%9E%90%EB%A3%8C/68842/TB/%EC%8F%A0%EB%A6%AC%EB%93%9C-%EB%8B%A8%EC%9D%BC%ED%8C%90%EB%A7%A4%EA%B3%B5%EA%B8%89%EA%B3%84%EC%95%BD-%EC%B2%B4%EA%B2%B0-%EB%B6%81%EB%AF%B8-1437%EB%A7%8C-%EA%B7%9C%EB%AA%A8-%EC%88%98%EC%A3%BC

- Source 17: https://www.hankyung.com/article/202602242205L

- Source 18: https://www.digitaltoday.co.kr/news/articleView.html?idxno=633895

- Source 19: https://www.etoday.co.kr/news/view/2234898

- Source 20: https://kr.tradingview.com/symbols/KRX-050890/

- Source 21: https://invest.deepsearch.com/stock/050890/

- Source 22: https://www.mt.co.kr/stock/2026/03/12/2026031208333063980

- Source 23: http://www.s-econ.kr/news/articleView.html?idxno=3101480

- Source 24: https://www.newstomato.com/ReadNews.aspx?no=1276297

- Source 25: https://marketin.edaily.co.kr/News/ReadE?newsId=04159046642301432

- Source 26: https://www.digitaltoday.co.kr/news/articleView.html?idxno=592942

- Source 27: https://www.datatooza.com/article/20260313161400734452ef37ae24_80

- Source 28: https://biz.heraldcorp.com/article/10693954