DEEP RESEARCH · KAON GROUP

KAON Group: Q4 Turnaround Driven by Wi-Fi 7 and XGS-PON

A turnaround report covering BEAD, North America/Japan orders and the robotics subsidiary option

0. Bottom line first

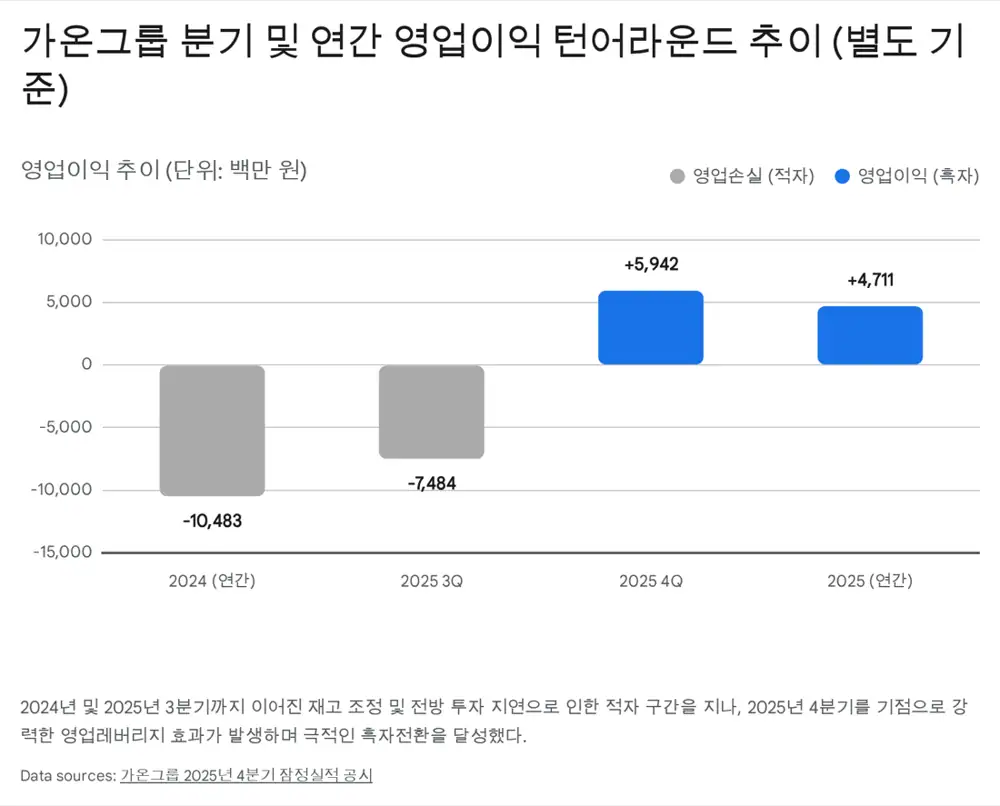

KAON’s Q4 2025 looks less like a simple base effect and more like the result of product mix and inventory cleanup. The key number is the swing from a KRW 7.484 billion operating loss in Q3 to KRW 5.942 billion profit in Q4.

Official fact: On a separate basis, Q4 2025 revenue was KRW 94.605 billion, up 24.6% QoQ and 20.6% YoY. Operating profit was KRW 5.942 billion, up 101.5% YoY and a turnaround from -KRW 7.484 billion in Q3.

Interpretation: The source attributes the leverage to Wi-Fi 7, XGS-PON, higher North America/Japan high-end customer mix and reduced bad-inventory burden.

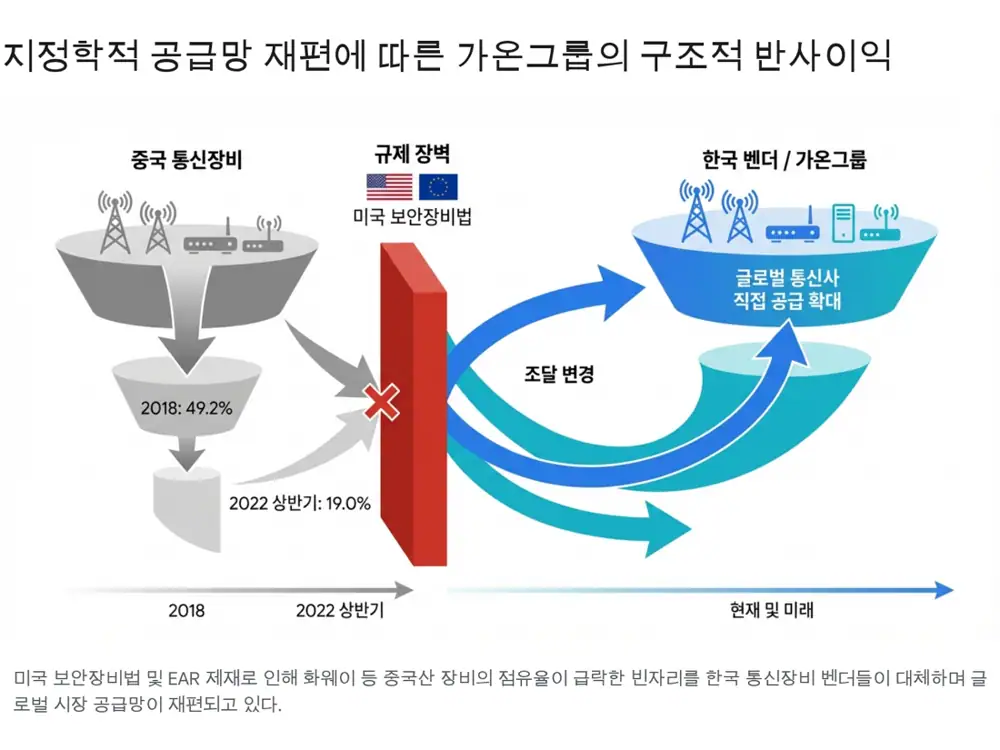

1. Business structure and geopolitical moat

KAON Group is an AI total-solution and telecom-device company with networks across more than 90 countries and over 240 broadcasting and telecom operators. In 9M 2025, OTT/AI solutions represented 52.2% of consolidated revenue, while network solutions represented 47.8%.

| Segment | Entity | Core products | 9M 2025 revenue | Share |

|---|---|---|---|---|

| OTT | KAON Group | AI devices, smart OTT set-top boxes | KRW 196,382mn | 52.2% |

| Network | KAON Broadband | Broadband CPE, AP, PON, DOCSIS, Wi-Fi repeaters, KRMS | KRW 179,967mn | 47.8% |

| New business | KAON Robotics, etc. | Service robots, XR, autonomous-driving modules | Included in OTT | - |

The source treats the U.S. exclusion of Chinese telecom equipment as KAON’s geopolitical moat. It also cites a decline in Chinese telecom-equipment share in the U.S. market from 49.2% in 2018 to 19.0% in H1 2022.

2. BEAD and next-generation standards

Official fact: The source frames the U.S. BEAD budget at USD 42.45 billion, about KRW 55 trillion, and says AT&T announced KRW 370 trillion of network modernization CAPEX over five years, about KRW 75 trillion annually.

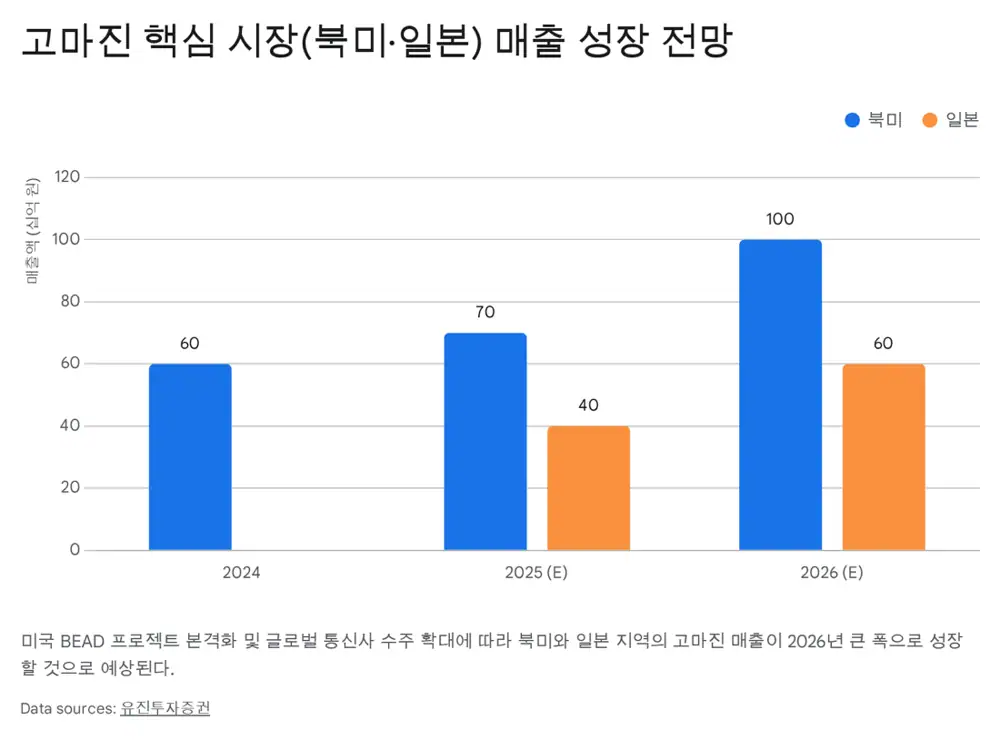

Based on the Eugene Investment report, the source expects North America revenue to rise from about KRW 60 billion in 2024 to KRW 70 billion in 2025 and the KRW 100 billion range in 2026. Japan revenue is expected to rise from about KRW 40 billion in 2025 to KRW 60 billion in 2026.

| Region | 2024 | 2025E | 2026E | Driver |

|---|---|---|---|---|

| North America | About KRW 60bn | About KRW 70bn | About KRW 100bn | BEAD and Tier-1 direct sourcing |

| Japan | No data | About KRW 40bn | About KRW 60bn | Expansion at two major telecom customers |

3. Quality of Q4 turnaround

| Separate basis | Q4 2024 | Q3 2025 | Q4 2025 | QoQ | YoY |

|---|---|---|---|---|---|

| Revenue | KRW 78,420mn | KRW 75,930mn | KRW 94,605mn | +24.6% | +20.6% |

| Operating profit | KRW 2,949mn | -KRW 7,484mn | KRW 5,942mn | Turned profitable | +101.5% |

| Annual revenue | KRW 289,042mn | - | KRW 305,965mn | - | +5.9% |

| Annual operating profit | -KRW 10,483mn | - | KRW 4,711mn | - | Turned profitable |

Developed-market orders

North America and Japan telecom demand drive volume.

Wi-Fi 7 and XGS-PON

Higher-value CPE raises ASP and margin.

Inventory cleanup

The source sees the Q4 profit swing as reflecting cleanup of legacy inventory burdens.

4. R&D, robotics option and balance sheet

KAON has a Brazil production subsidiary, but the source cites Q3 2025 average utilization of 5% for network and 17% for OTT. It interprets this as spare internal capacity plus an asset-light EMS outsourcing strategy.

9M 2025 R&D spending was KRW 16.645 billion, equal to 4.42% of revenue. The source connects on-device AI set-top boxes, KAON GPT Cloud, AR navigation, 5G-based XR devices and Matter/Thread network solutions to a smart-home and physical-AI hub strategy.

KAON Robotics is the service-robot, XR and autonomous-module option. The source says a large-volume contract tied to collaborations such as Hyundai MobED could re-rate the company beyond a telecom-equipment multiple.

Official fact: At Q3 2025, consolidated assets were KRW 372.9 billion, liabilities KRW 263.6 billion, equity KRW 109.2 billion and cash/equivalents KRW 35.5 billion. CB balance was around KRW 7.0 billion. The source also cites a stock dividend of 0.02 common shares per share and a cash dividend of KRW 70 per common share.

5. Valuation and catalysts

The source cites 2026 expected controlling-shareholder net income of about KRW 13.0 billion, forward PER of 10.5x, 2025E PER of 19.7x, market cap around KRW 140 billion, a share price around KRW 7,600 and PBR around 1.0x.

- Major North America/Europe Wi-Fi 7 and optical-terminal orders are the first catalyst.

- A large service-robot drive-module contract through KAON Robotics could expand the valuation multiple.

- Watch whether the KRW 5.9 billion Q4 2025 profit repeats through 2026 quarterly results.

- Risks include CAPEX delays, low-cost competition and certification/delivery risk for new products.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224217160336

- 조선비즈: https://biz.chosun.com/industry/company/2022/10/13/POOMTB5E6FDTVEQ2ADHIACIN7Q/

- 아시아경제: https://cm.asiae.co.kr/ampview.htm?no=2025111908154684158

- 뉴스핌: https://www.newspim.com/news/view/20260108000165

- 뉴스토마토: https://www.newstomato.com/ReadNews.aspx?no=1152710

- 산업일보: https://kidd.co.kr/news/229620

- 유진투자증권 리포트: https://file.alphasquare.co.kr/media/pdfs/market-report/%EA%B0%80%EC%98%A8%EA%B7%B8%EB%A3%B9%ED%86%B5%EC%8B%A0%EA%B3%BC20260304%EC%9C%A0%EC%A7%84%ED%88%AC%EC%9E%90%EC%A6%9D%EA%B6%8C

- 머니투데이 더벨: https://www.mt.co.kr/stock/2025/12/16/2025121613269661091

- 키움증권: https://bbn.kiwoom.com/rfCR11797

- 디지털투데이 배당: https://www.digitaltoday.co.kr/news/articleView.html?idxno=629369

- Investing.com: https://kr.investing.com/equities/kaon-media-co-ltd