DEEP RESEARCH · RF Materials (327260)

RF Materials Q4 2025 Earnings — Dawn of the AI Optical Supercycle

Compound-semiconductor packaging — operating leverage proven where AT&T's $250B CAPEX meets 800G/1.6T optical transceivers

0. Bottom line first

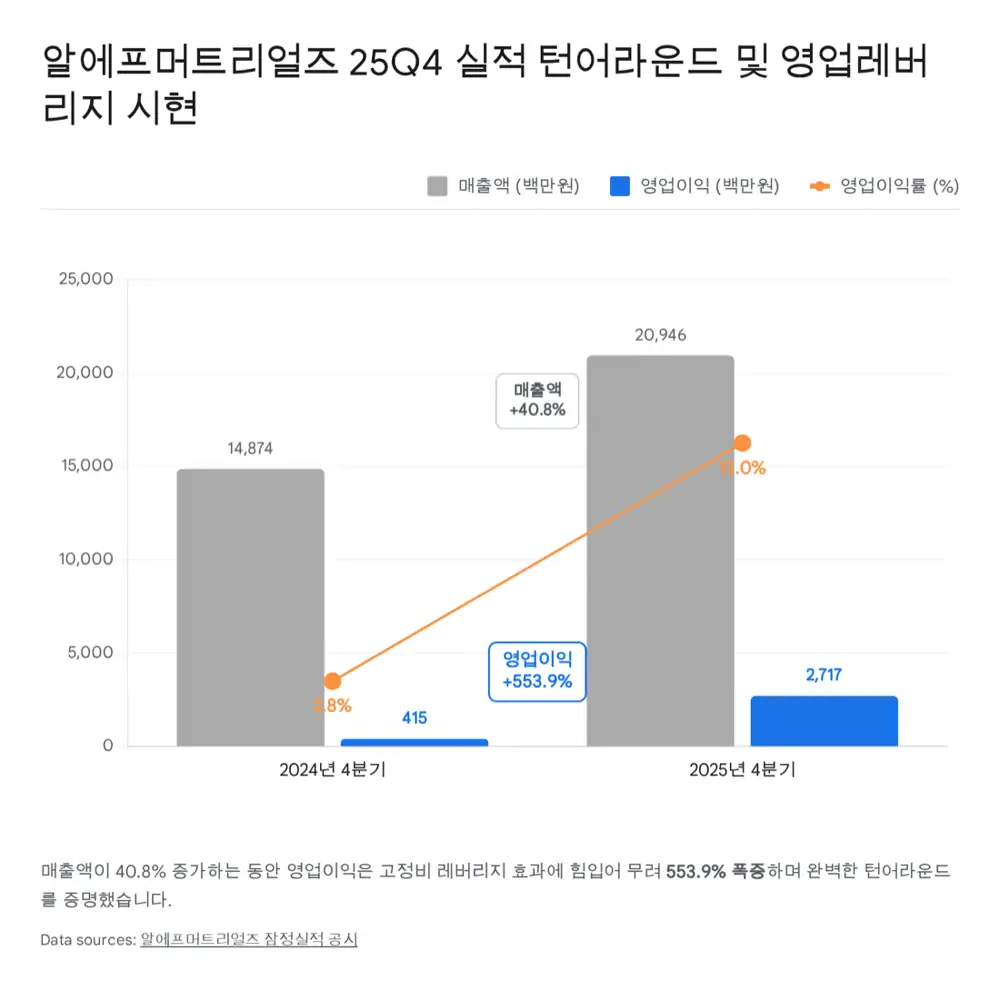

RF Materials posted a compressed-spring turnaround in Q4 2025: revenue ₩20.946B / operating profit ₩2.717B (YoY +553.93%). The drivers are ① a vertical jump in 800G/1.6T optical HTCC package volumes to Lumentum and MACOM, ② structural reflex benefits from the Clean Network de-China geopolitics, and ③ structural GaN-package demand born of AT&T's five-year $250B (~₩370T) CAPEX plus its $14B Open RAN contract with Ericsson. The company redeemed a ₩10B convertible bond early with internal cash and locked in growth-CAPEX funding via a treasury-share disposal (₩4.534B) explicitly tagged for "AI data-center facility and operating capital" — no mezzanine dilution.

₩20.946B

QoQ +43.58% · YoY +40.82%

₩2.717B

YoY +553.93% · operating leverage confirmed

₩7.318B

Prior FY -₩1.453B → swing to profit

~48.6%

Short-term financial assets ₩41.464B · zero liquidity stress

1. Company snapshot — the physical shield and thermal artery of compound semiconductors

1.1. Core business and positioning

RF Materials is a deep-tech designer/manufacturer of compound-semiconductor packages used in wireless infrastructure (base stations, small cells), optical communications (data centers, transport equipment), industrial/medical laser modules, and defense IR sensors and radars.

Unlike silicon (Si), compound semiconductors based on Group III–V combinations — gallium nitride (GaN), gallium arsenide (GaAs), indium phosphide (InP) — operate at ultra-high frequency, ultra-high speed, and high power, and inevitably generate enormous heat. RF Materials' packages dissipate that heat externally and provide complete hermetic sealing to shield the die from moisture, oxygen, and mechanical shock.

Official fact: The firm has internalized multilayer-ceramic HTCC (High Temperature Co-fired Ceramic) and high-thermal cladding tech. It was the first in Korea to develop MoCu/WCu heat-sink materials via Mo/W infiltration, and holds multiple patents on CPC/CMC/Super-CMC composites joined by hot-press.

Interpretation: Japan's Kyocera/NTK and France's Egide once dominated this market — RF Materials achieved full domestic substitution. Its tri-axial portfolio (telecom + laser + defense) cushioned the cycle through the long telecom-capex "valley of death," and it emerges with strong pricing power as a survivor.

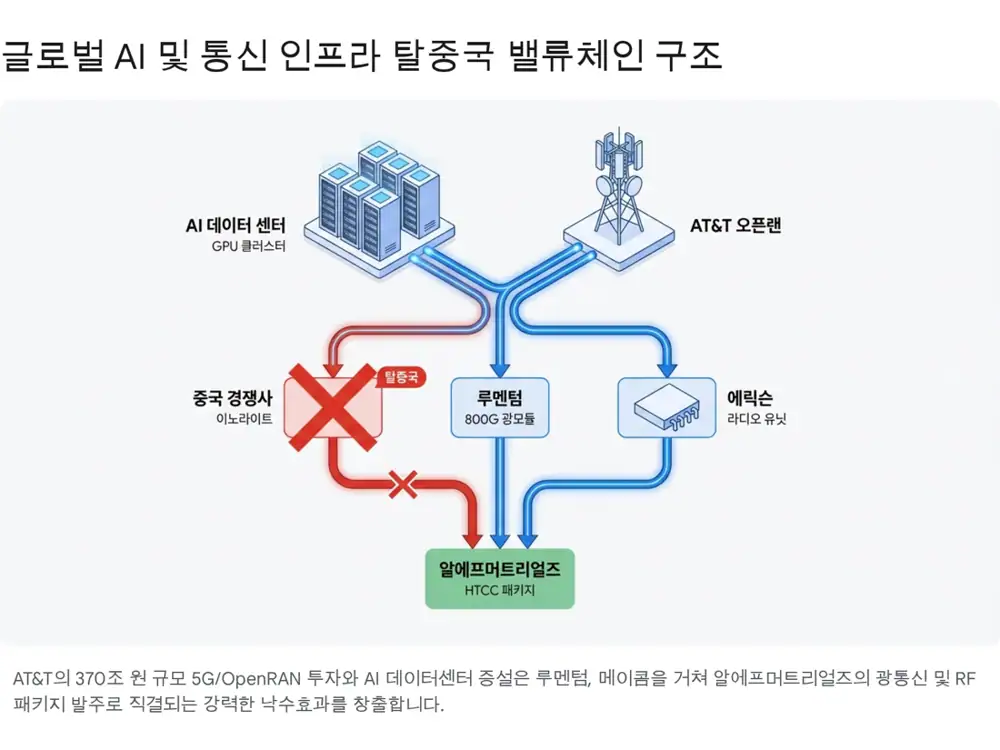

Interpretation: Even with the EU's cybersecurity law against Chinese components, this de-China shift is irreversible. RF Materials, the exclusive supplier of pump-laser telecom packages to Lumentum, captures the supplier-side "vacant-house" effect in full.

1.2. Entry into global vendor ecosystems and de-China geopolitical reflex benefit

RF Materials' true value lies less in its patents than in its place inside Top-tier global vendor networks. In wireless RF it is connected via parent RFHIC to Samsung, Ericsson, and Nokia and supplies GaN transistor packages. Today's explosive growth, however, comes from optics: North America's largest optical-module and telecom-semi houses — Lumentum and MACOM — are core customers. U.S. semiconductor and telecom-equipment sanctions on China are a once-in-a-generation structural opportunity: the seats once held by China's Innolight and Eoptolink in the 400G/800G market are being absorbed by Clean-Network vendors in Korea and the U.S.

Official fact: CHIPS-Act-funded MACOM is expanding GaN/GaAs fabs in Massachusetts and North Carolina at scale. Lumentum is dramatically expanding its ultra-high-power (UHP) laser fab in San Jose.

2. Front-end momentum — AT&T CAPEX & AI-RAN

2.1. AT&T's infrastructure overhaul and the Open RAN paradigm

U.S. telecom giant AT&T unveiled a plan to spend more than $250B (~₩370T) on combined CAPEX/OPEX over the next five years — covering fiber broadband, nationwide 5G enhancement, satellite links, and AI-driven network automation (AI CERTs News, AT&T IR Analyst Day).

Official fact: Versus the prior five-year ~$145B execution, this implies roughly 70%+ budget expansion. Skeptics highlight OPEX commingling (Light Reading critique), but the absolute scale is overwhelming.

The watershed moment is AT&T's $14B commercial Open RAN deal with Ericsson (Ericsson PR, AT&T release). AT&T targets routing 70% of total wireless traffic by end-2026 through open-capable platforms.

AT&T and Ericsson have already demonstrated "AI-native Link Adaptation" on commercial Cloud RAN running Intel Xeon 6 SoCs — delivering up to 20% higher network throughput over rule-based algorithms (AT&T 2026 release, Ericsson case study).

Interpretation: Building this intelligent network physically requires massive MIMO antennas and high-power, low-latency base stations en masse. PA materials are rapidly shifting from Si LDMOS to GaN. The AI-RAN equipment of Ericsson, Fujitsu and others mandates high-thermal GaN transistor packages — and RF Materials sits at the bottom of that BOM, generating structural demand.

2.2. Explosion of 800G optical-transceiver demand from AI data centers

Beyond wireless, the steeper momentum comes from hyperscale data centers around NVIDIA GPUs. As LLM parameter counts swell into the trillions, clusters of tens of thousands of GPUs become standard, and East-West server-to-server and switch-to-switch traffic grows exponentially.

Official fact: Lumentum leads UHP lasers and 200G EML (Electro-absorption Modulated Laser) chipsets for 800G/1.6T transceivers (800G 2×DR4 OSFP, Datacom Transceivers, Data Center Products). Cloud and AI infra revenue already exceeds 60%, with next-quarter guidance of YoY +120%. With Marvell and Coherent, Lumentum has also demonstrated 800G ZR/ZR+ pluggables for 500km DCI.

Interpretation: This is not a short spike but a structural transformation from copper scale-up to optical scale-out. Optical transceivers' laser diodes need precise wavelength control and hermetic sealing — RF Materials' pump-laser packages powered the 2025 earnings rebound (Convequity analysis).

2.3. Long-term risks

- Telco CAPEX execution delays: Past 5G cycles saw share-price surges on order expectations followed by long corrections as actual investment lagged. AT&T's Lightspeed fiber build-out is reportedly pressured by higher-than-expected costs to replace copper (Light Reading).

- Pricing competition from incumbents: Japan's Kyocera and other ceramic oligopolists.

- Low-loss polymer dielectrics: For mmWave low-loss signaling, commercialization of LCP/PTFE-based low-loss polymer dielectrics — projected at $224.66M by 2034 — could nibble at HTCC long-term.

Interpretation: But for the relentless heat of telecom-PA and AI data-center laser environments, the thermodynamic credibility of ceramic–metal (CMC, MoCu) hybrid packages with atomic-level bonding is hard for organic polymers to displace short-term, per industry consensus.

3. Q4 2025 turnaround and 2026–2027 operating leverage

3.1. Anatomy of the surprise — Q, P, C analysis

The preliminary consolidated results disclosed on 26 January 2026 are a financial milestone confirming a fundamental level-up.

| (₩M) | Q4 2024 | Q3 2025 | Q4 2025 | YoY | QoQ | FY2024 | FY2025 | YoY (FY) |

|---|---|---|---|---|---|---|---|---|

| Revenue | 14,874 | 14,589 | 20,946 | +40.82% | +43.58% | 44,497 | 63,904 | +43.61% |

| Op. profit | 415 | 1,891 | 2,717 | +553.93% | +43.66% | -1,453 | 7,318 | Swing to profit |

| Pre-tax profit | -6,178 | 2,353 | 2,970 | Swing | +26.24% | -7,498 | 8,240 | Swing |

| NI attributable to owners | -4,793 | 1,738 | 4,035 | Swing | +132.09% | -2,917 | 7,017 | Swing |

Beneath this turnaround is margin-spread improvement across volume (Q), price (P), and cost (C):

- Q (Volume — core product expansion): Optical comms is the primary driver. North-America Lumentum pump-laser and data-center optical-transceiver package revenue is estimated to have jumped 2–3× in Q4 alone from a roughly ₩2.6B prior baseline. Defense subsidiary RF Systems also recorded ₩13.5B in Q4 on strong antenna-component orders via LIG Nex1.

- P (Price — high-mix improvement): Mix shift from low-margin wireless-repeater "can" packages toward 400G/800G TOSA DML, LiDAR, K/Ka aerospace-grade packages. Multi-pin feedthrough and precision brazing lift ASP structurally.

- C (Cost & operating leverage — strong fixed-cost gearing): Ceramic forming, kilns, brazing, plating — a textbook fixed-cost equipment industry. Once Q breaks above BEP, marginal profit explodes. Revenue +40%, op. profit +554% — perfect empirical proof of operating leverage.

3.2. Owner-attributable profit and underlying earnings power

More important than headline operating profit is the bottom-line attributable to the parent. Q4 2025 NI attributable to owners was ₩4.035B — swinging from a ₩2.917B loss in the prior-year quarter and rising +132.09% from the prior quarter (₩1.738B).

On an FY basis, NI attributable to owners reached ₩7.017B, reversing a ₩4.793B accumulated loss in 2024. Even after stripping minority-interest distortions tied to RF Systems, the parent's optical/laser ceramic packaging core is generating real free cash flow. The quality of earnings — anchored in AI data-center infrastructure orders rather than one-off cost cuts — suggests the high-margin regime can hold through the 2026–2027 supercycle.

4. CAPEX capacity and financial health

4.1. Balance-sheet resilience after a brutal restructuring

| (₩M) | 2024-12-31 (prior YE) | 2025-09-30 (Q3-end) |

|---|---|---|

| Current assets | 81,813 | 75,354 |

| - Cash & equivalents | 38,949 | 5,487 |

| - Short-term financial assets | 18,611 | 41,464 |

| - Trade & other receivables | 10,746 | 10,663 |

| - Inventory | 11,946 | 16,098 |

| Non-current assets | 31,718 | 39,234 |

| - PP&E | 26,474 | 25,881 |

| Total assets | 113,531 | 114,589 |

| Total liabilities | 43,684 | 37,513 |

| Total equity | 69,846 | 77,075 |

Official fact: As of Q3 2025, consolidated assets ₩114.589B, short-term financial assets ₩41.464B inside current assets of ₩75.354B. Total liabilities ₩37.513B vs. equity ₩77.075B — D/E ~48.6%.

Interpretation: Inventory rose from ₩11.9B at YE2024 to ₩16.1B at Q3-end 2025. In manufacturing, active build-up of raw materials (e.g. PGC) and WIP is a strong leading indicator of confirmed backlog deliverable within the next 1–2 quarters.

4.2. Pre-emptive CAPEX and shareholder-friendly financing

While many marginal peers diluted shareholders during the winter via CB/BW/private placements, RF Materials' Q3 2025 cash-flow statement shows the firm redeeming a ₩10B private CB ahead of schedule with internal cash — eliminating the overhang risk at the root.

The symbolic event: a 21 October 2025 treasury-share disposal filing — 247,357 treasury shares (~2.93% stake, ₩4.534B) to be sold via block trades by January 2026 (MarketIn coverage).

The key is the use of proceeds explicitly tagged as "facility and operating capital for AI data-center-bound package revenue growth." This signals confirmed visibility on 800G/1.6T optical-transceiver package orders from Lumentum and others — funding brazing furnaces, large kilns, vacuum leak detectors, and other bottleneck capacity pre-emptively. Using previously low-cost treasury shares instead of mezzanine bombing is exemplary capital allocation.

4.3. R&D loading the future portfolio

RF Materials kept R&D spending steady through the demand cliff — 5.47% of revenue (₩2.35B) on a cumulative Q3 2025 basis.

| Key R&D project | Description and application | Commercialization stage |

|---|---|---|

| 400/800G TOSA package | Optimized package for data-center AI-cluster high-speed TOSA (Transmitter Optical Sub Assembly) transceivers. High-power + metal–ceramic pattern combination. | Mass production |

| High-thermal HTCC RF package | Fully hermetic ceramic packages for 5G/6G base-station HEMT devices and LEO satellite communications. | Mass production |

| Satellite K/Ka power package | Space-grade high-reliability power and RF packages. Full domestic substitution of fully imported space-grade parts. | Development / mass production |

| Autonomous-driving LiDAR package | Specialty package for laser-signal sensors that precisely measure vehicle surroundings. | Mass production |

Selected as the prime institution for a Ministry-of-Science-and-ICT and Ministry-of-Trade-led national R&D project on "Localizing data-transmission components for LEO satellites (₩4.5B total)," and participating in "Global Top LEO satellite space-package materials development (₩3B)" — extending the technological moat into aerospace and defense.

5. Valuation and powerful share-price catalysts

5.1. The market's misunderstanding and a deep-value entry

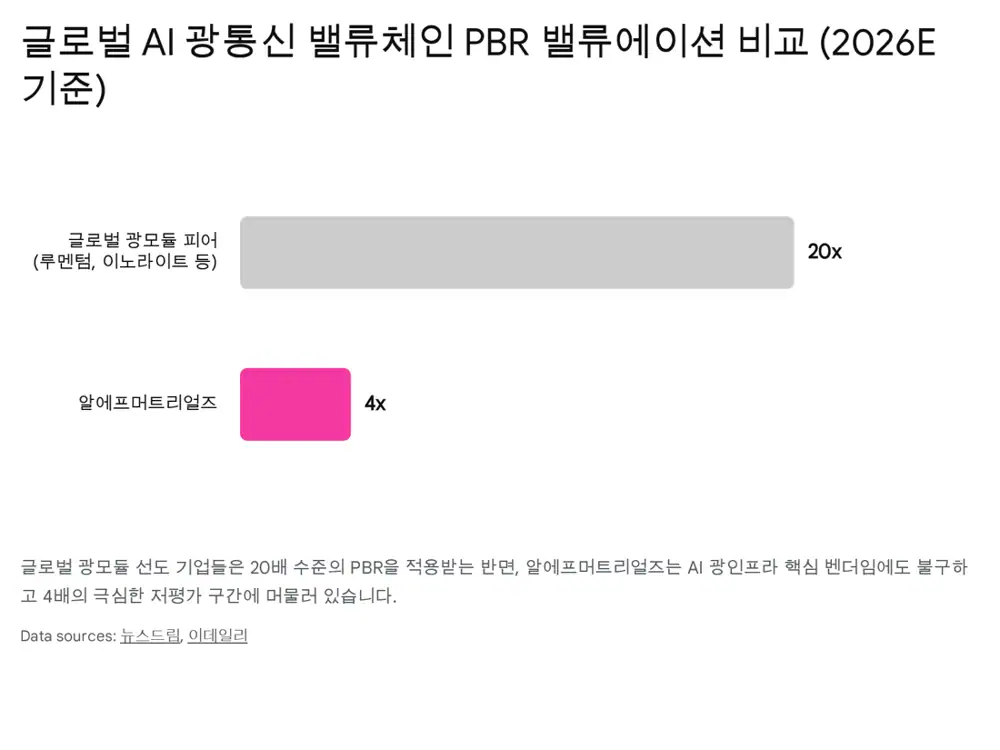

Official fact: Korean broker estimates put 2026 revenue at ₩92.7B and op. profit at ₩14.5B (YoY +45% and +98%). Optical packages including Lumentum pump-lasers alone are forecast at ~₩55B, more than 60% of total revenue (Hana Securities report via Newsdream, MarketIn, Daum news).

PBR >20x

2025–2026 forward multiples for optical-module beneficiaries

PBR ~4x

2026 forward — below the PBR 5.2x acknowledged at the RF Systems acquisition (Investing.com)

Interpretation: The market still tags RF Materials as a "legacy wireless-component name" scarred by past 5G disappointments. The company's identity has, however, completed the transition into "a monopoly-grade materials supplier to AI data-center optical infrastructure."

5.2. Three core catalysts

- Large-scale AI optical-transceiver production and order disclosures: Once Lumentum and other North American key customers visibly ramp 800G/1.6T HTCC package orders, a multiple re-rating becomes the immediate trigger.

- U.S./EU formal removal of Chinese telecom gear: EU cybersecurity law activation + additional CHIPS-Act-driven U.S. sanctions → physical exit of Chinese module vendors such as Innolight from global data-center switch and telecom infra (RF Semiconductor Market analysis).

- AT&T- and Ericsson-led Open RAN order restart: Aligned with North America's 2026 additional spectrum auctions, once AT&T's ₩370T CAPEX flips into real RU hardware budgets, GaN RF package orders via Ericsson and Samsung will explode.

5.3. Final investment conclusion and trade strategy

"If you wait until orders are filed and earnings are in the books, you're already late. The eve of the earnings storm is the last entry window."

RF Materials walked alone through telecom's long deficit tunnel, built technical independence from Japanese material monopolies, and earned the right to a profitable survival. It now stands at the intersection of two mega-trends: AT&T's ₩370T network modernization and NVIDIA-GPU-cluster-led data-center optical transition.

The Q4 2025 +553% operating-profit jump is not a one-off rebound but the opening salvo of a structural operating-leverage regime that will unfold over the next three years. For bottom-up investors hunting for the genuine turnaround ten-bagger riding North America's AI build-out, the current share price sits in a historic Strong-Buy zone created by the gap between fundamentals and momentum.

Sources

- AT&T's Record AI Infrastructure Spend Commitment — AI CERTs News: https://www.aicerts.ai/news/atts-record-ai-infrastructure-spend-commitment/

- AT&T to Accelerate Open RAN with Ericsson — Ericsson PR: https://www.ericsson.com/en/press-releases/2023/12/att-to-accelerate-open-and-interoperable-radio-access-networks-ran-in-the-united-states-through-new-collaboration-with-ericsson

- AT&T Collaborates with Ericsson on Open RAN: https://about.att.com/story/2023/commercial-scale-open-radio-access-network.html

- Lumentum 800G 2×DR4 OSFP Transceiver: https://www.lumentum.com/en/products/800g-2dr4-osfp-transceiver-module

- Lumentum Datacom Transceivers: https://www.lumentum.com/en/products/data-center/datacom-transceivers

- Lumentum Holdings: Optical Engine Behind AI Data-Center — Convequity: https://www.convequity.com/lumentum-holdings-the-optical-engine-behind-the-ai-data-center-revolution/

- Hana Sec on RF Materials' China-reflex benefit — Newsdream: http://www.newsdream.kr/news/articleView.html?idxno=106153

- RF Materials AI demand + China sanctions reflex — MarketIn: https://marketin.edaily.co.kr/News/ReadE?newsId=02453446645322312

- RF Materials China sanctions reflex feature — Daum: https://v.daum.net/v/20260128094742950

- NIST preliminary terms with MACOM — Light Reading: https://www.lightreading.com/regulatory-politics/nist-announces-preliminary-terms-with-macom-to-strengthen-supply-chain-resilience-for-u-s-defense-and-telecommunications-industries

- Lumentum Expands U.S. Manufacturing for AI CPO — Business Wire: https://www.businesswire.com/news/home/20250807428905/en/Lumentum-Expands-U.S.-Manufacturing-for-AI-Driven-Co-Packaged-Optics

- AT&T Analyst Day Presentation — IR: https://investors.att.com/~/media/Files/A/ATT-IR-V2/reports-and-presentations/2024-analyst-day-with-notes.pdf

- AT&T and Ericsson Enhance Cloud RAN Performance: https://about.att.com/story/2026/att-ericsson-enhance-cloud-ran.html

- AT&T and Ericsson Case Study: https://www.ericsson.com/en/cases/2025/att-and-ericsson

- RF Semiconductor Market — P&S Intelligence: https://www.psmarketresearch.com/market-analysis/rf-semiconductor-market-report

- Lumentum Data Center Products: https://www.lumentum.com/en/products/data-center

- Marvell/Lumentum/Coherent 800G ZR/ZR+ Demo: https://investor.marvell.com/news-events/press-releases/detail/128/marvell-lumentum-and-coherent-demonstrate-industrys-first-800g-zrzr-pluggable-modules-for-500km-data-center-interconnects

- Analyst: AT&T Capex Spend Slowing — Light Reading: https://www.lightreading.com/fttx/analyst-at-t-capex-spend-slowing

- Ceramic materials for 5G wireless: https://ceramics.org/wp-content/uploads/2019/07/August-2019_Feature.pdf

- RF Materials Co Ltd (KOSDAQ:A327260) P/E — Investing.com: https://ng.investing.com/pro/KOSDAQ:A327260/explorer/pe_ltm

- 5G RF Circuits: Low-Loss Polymer Dielectrics — PatSnap: https://eureka.patsnap.com/article/5g-rf-circuits-low-loss-polymer-dielectrics-for-millimeter-wave-applications

- Low-Loss Materials for 5G Market Size — Precedence Research: https://www.precedenceresearch.com/low-loss-materials-for-5g-market

- RF Materials' ₩4.5B treasury-share disposal — MarketIn: https://marketin.edaily.co.kr/News/ReadE?newsId=04457526642335216

- Naver blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224217159062