DEEP RESEARCH · HFR

HFR: An 88% Loss Reduction Inside a Revenue Decline

2025 earnings and 2026-2028 leverage in front of O-RAN, private 5G and AT&T CAPEX

0. Bottom line first

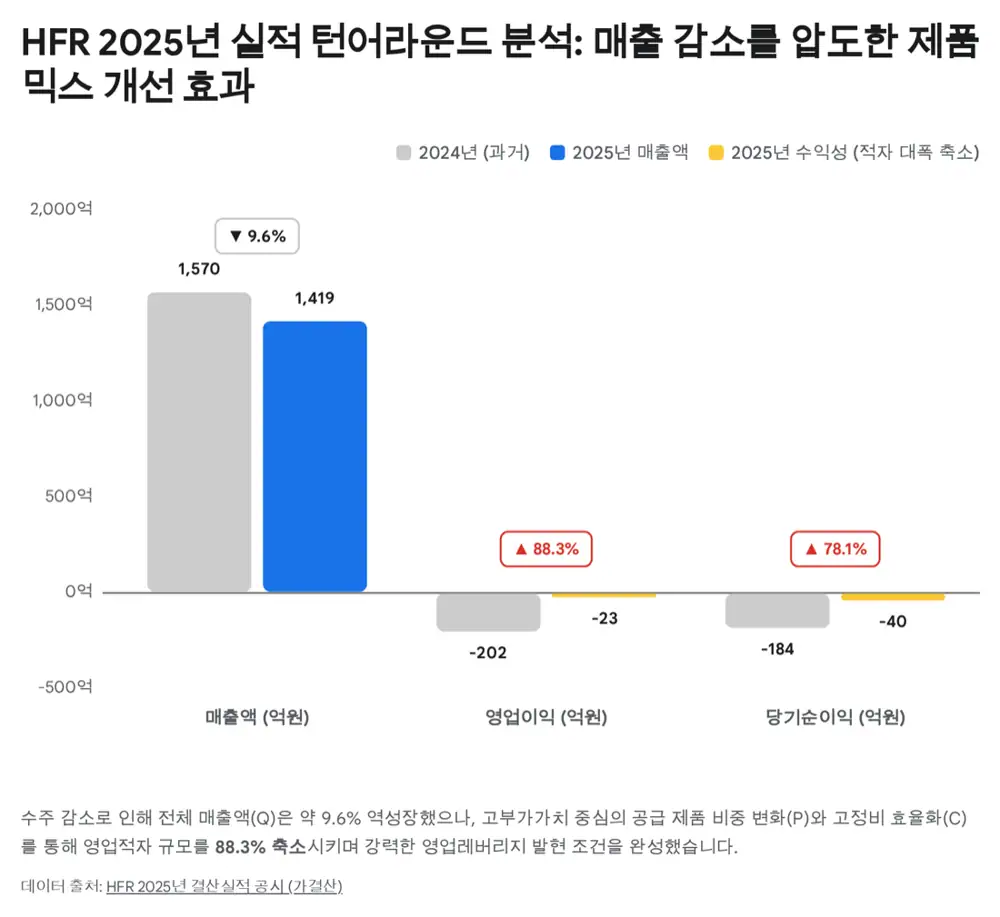

HFR’s 2025 numbers look weak at the revenue line, but the income statement suggests a major mix and cost reset. Revenue fell 9.6%, yet operating loss narrowed 88.3%.

Official fact: 2025 consolidated revenue was KRW 141.98 billion, down 9.6% from KRW 157.09 billion. Operating profit improved from -KRW 20.23 billion to -KRW 2.36 billion, and net income from -KRW 18.48 billion to -KRW 4.05 billion.

Interpretation: Q was weak due to lower orders, but higher-value product mix and cost control brought the company closer to break-even. The source’s thesis is that recovering Q in 2026-2027 could unlock large operating leverage.

1. Business structure and moat

HFR is positioned across mobile networks, fixed broadband and private 5G. In mobile access, key products include flexiHaul, 5G-PON, packet fronthaul, in-building DAS, TRIO and 5G Active Relay; in broadband, OLT, ONU, ONT and TSS matter.

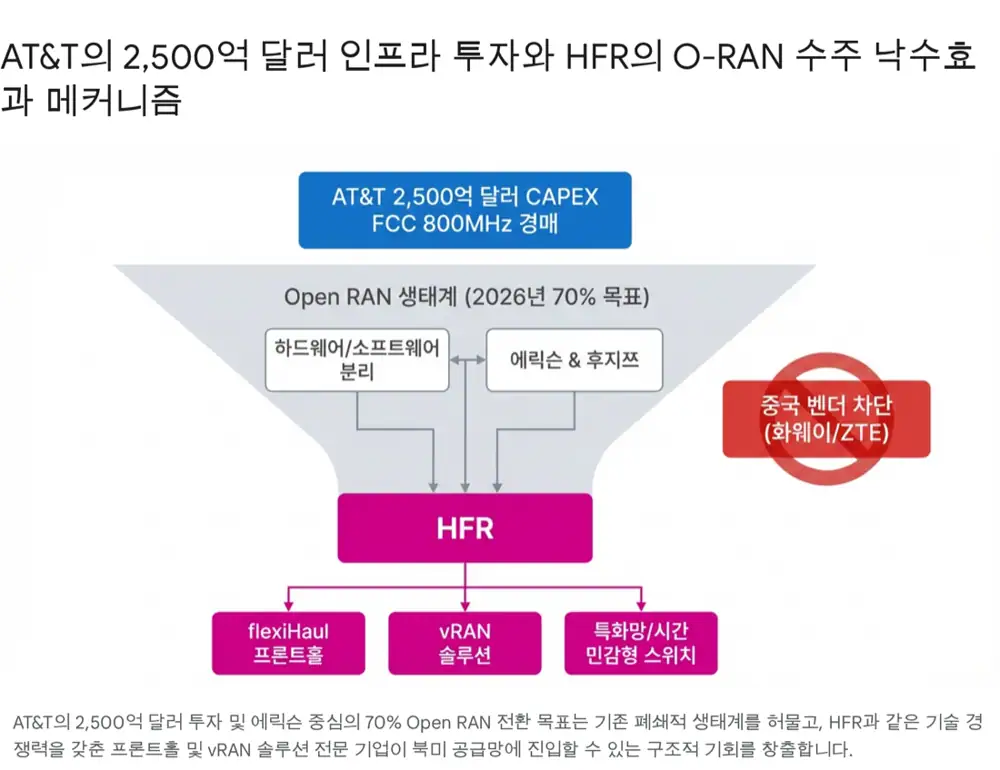

2. Demand catalyst: AT&T and O-RAN

The source treats AT&T’s plan to invest USD 250 billion through 2030 as the largest macro catalyst. Its intent to open the network to new equipment suppliers is tied to the O-RAN transition.

Official fact: The source cites AT&T’s timeline to process 70% of wireless network traffic on open-capable platforms by end-2026 and a five-year, roughly USD 14 billion Ericsson contract.

Interpretation: When RU and DU come from different vendors in O-RAN, fronthaul becomes critical. HFR’s flexiHaul and O-RAN-optimized products are candidates for this spillover.

3. 2025 results: weak Q, better P and C

| Item | 2024 | 2025 preliminary | Change | Rate |

|---|---|---|---|---|

| Revenue | KRW 157.09bn | KRW 141.98bn | -KRW 15.11bn | -9.6% |

| Operating profit | -KRW 20.23bn | -KRW 2.36bn | +KRW 17.87bn | 88.3% better |

| Pre-tax profit | -KRW 15.09bn | -KRW 2.13bn | +KRW 12.96bn | 85.8% better |

| Net income | -KRW 18.48bn | -KRW 4.05bn | +KRW 14.43bn | 78.1% better |

Order decline

The official reason for revenue decline was lower orders.

High-value mix

The source points to AI-RAN, private 5G, TSS and O-RAN fronthaul as higher-quality mix.

Cost control

Large loss reduction despite lower revenue signals lower COGS and fixed-cost discipline.

4. Balance sheet, capacity and overhang

| Item | End-2024 | End-2025 preliminary | Change |

|---|---|---|---|

| Assets | KRW 271,084,802,354 | KRW 276,381,683,881 | Slight increase |

| Liabilities | KRW 112,271,469,571 | KRW 125,146,598,609 | Increase |

| Equity | KRW 158,813,332,783 | KRW 151,235,085,272 | Down on net loss |

| Capital stock | KRW 6,744,513,000 | KRW 6,744,513,000 | No change |

The preliminary debt-to-equity ratio was about 82%. At end-Q3 2025, short-term borrowings were about KRW 43.1 billion and long-term borrowings about KRW 33.1 billion.

HFR issued USD 10 million of convertible preferred shares at its U.S. subsidiary in December 2021, but bought back about 54,672,897 of the 93,457,944 issued shares in Q3 2025. The source also highlights a KRW 220 per-share dividend in March 2024, cancellation of 180,026 common shares in July 2024, and a roughly KRW 2.0 billion treasury-share purchase of 100,251 shares in Q3 2025.

5. Catalysts and risks

- Official inclusion in AT&T/Ericsson O-RAN or a major North America fronthaul order would be the first catalyst.

- Japanese private-5G enterprise orders through NEC/NESIC could re-rate the full-stack solution value.

- A confirmed quarterly profit turnaround in H1 2026 could break the market’s skepticism.

- Risks include telecom CAPEX delays, more O-RAN competition, bundled offerings from large vendors and low-cost entrants from India or Taiwan.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224217158620

- 산업일보: https://kidd.co.kr/news/229620

- 뉴스토마토: https://www.newstomato.com/ReadNews.aspx?no=1152710

- Fierce Network: https://www.fierce-network.com/wireless/despite-2025-turbulence-open-ran-poised-2026-surge

- Mobile World Live AT&T/Ericsson: https://www.mobileworldlive.com/att/att-ericsson-make-live-open-ran-call/

- Ericsson Open RAN: https://www.ericsson.com/en/press-releases/2023/12/att-to-accelerate-open-and-interoperable-radio-access-networks-ran-in-the-united-states-through-new-collaboration-with-ericsson

- AT&T Open RAN: https://about.att.com/story/2023/commercial-scale-open-radio-access-network.html

- beBeez AT&T Cloud RAN: https://bebeez.eu/2026/03/04/att-continues-open-ran-overhaul-builds-on-ericsson-partnership-with-cloud-ran-tests/

- AT&T Open RAN readiness: https://about.att.com/blogs/2026/att-advances-open-ran-readiness.html

- One Touch Intelligence FCC: https://onetouchintelligence.com/2025/07/22/fcc-auction-authority-restored-ntia-to-consider-more-5g-spectrum/

- Mobile World Live FCC: https://www.mobileworldlive.com/fcc/us-fcc-regains-spectrum-auction-authority/

- Light Reading spectrum: https://www.lightreading.com/regulatory-politics/looking-ahead-spectrum-sales-and-squabbles-in-2026

- 전자신문 HFR 자사주: https://www.etnews.com/20240517000181

- HFR hedge fund article: https://www.hfr.com/media/market-commentary/global-hedge-fund-industry-capital-surges-past-historic-5-trillion-milestone/

- RCR Wireless AT&T/Fujitsu: https://www.rcrwireless.com/20250319/open_ran/att-fujitsu-mwc25

- AT&T collaborations: https://about.att.com/blogs/2024/open-ran-new-collaborations.html

- FCC: https://www.fcc.gov/restoring-americas-leadership-wireless