DEEP RESEARCH · INNOWIRELESS

Innowireless: Testing the 2026~2028 Telecom Equipment Supercycle Setup

A 4Q results report separating the annual loss from 4Q profit, T&M, small cells, and Open RAN measurement demand

0. Bottom line first

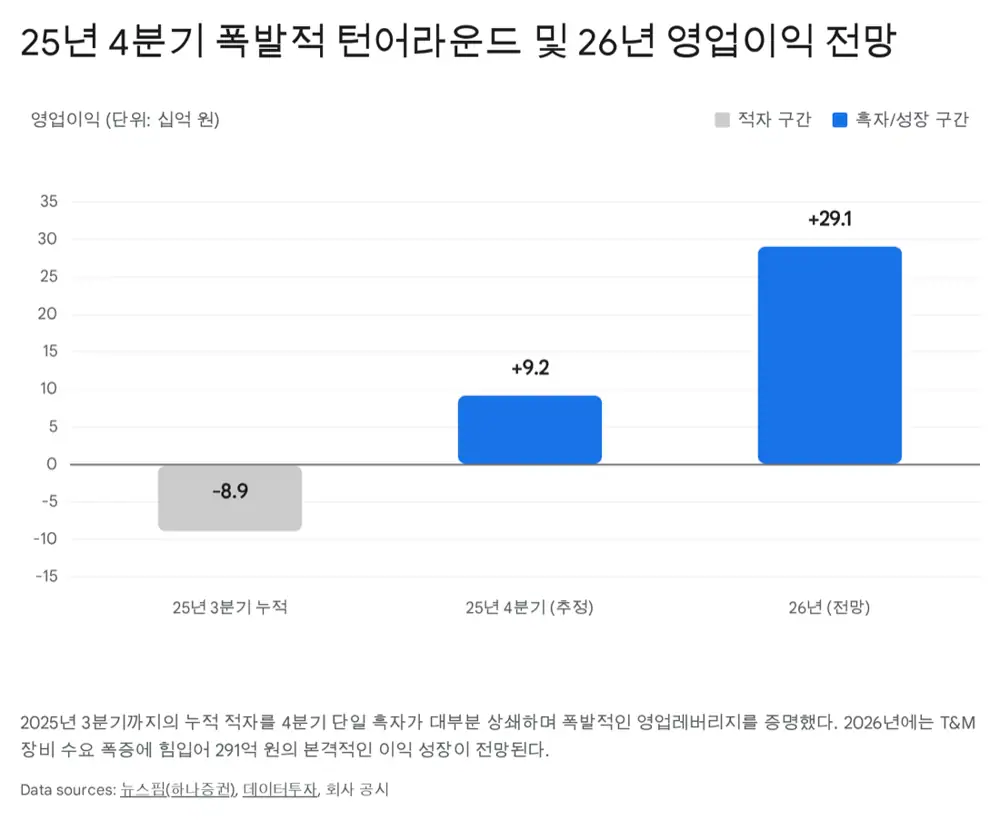

Innowireless reported 2025 revenue of KRW 186.1B, operating loss of KRW 1.12B, and net loss of KRW 1.14B. But the source argues that moving from a cumulative 3Q operating loss of KRW 8.9B to a full-year loss of KRW 1.12B implies roughly KRW 7.8B of 4Q operating profit, or about KRW 9.2B in broker estimates.

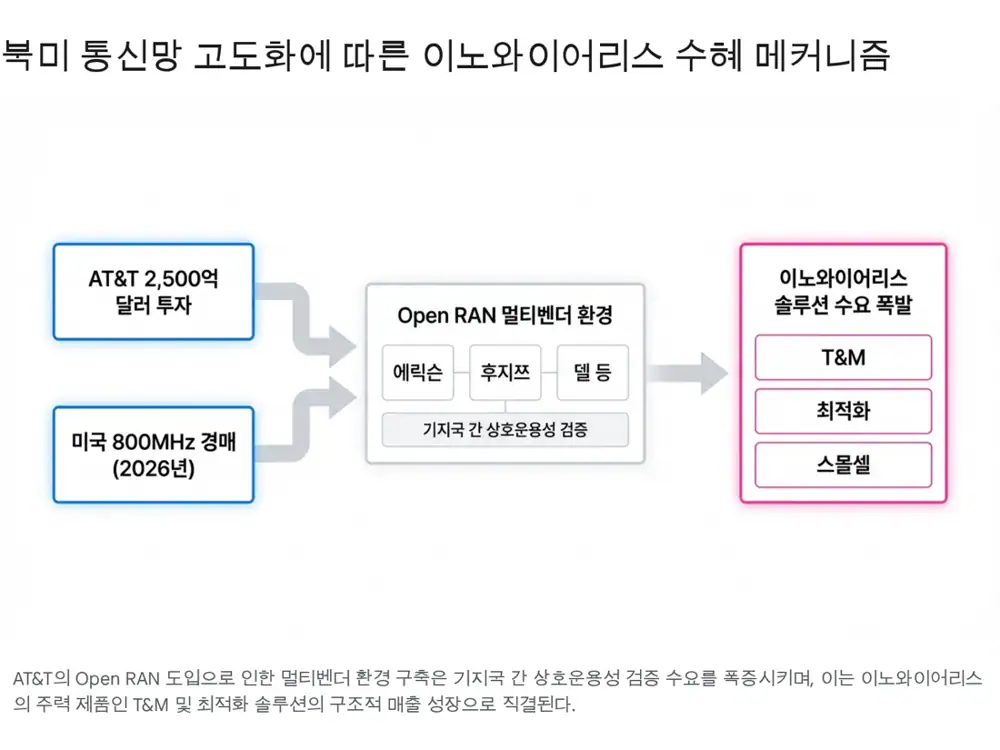

Official fact: The source presents AT&T's 2026~2030 infrastructure investment of USD 250B, about KRW 330T, a 70% Open RAN traffic target, and an approximately USD 14B Ericsson contract as key macro signals.

Interpretation: While the market focuses on the 2025 annual loss, the more important points are the 4Q profit swing and measurement/optimization demand forced by Open RAN.

1. Macro: Return of the Telecom Equipment Cycle

- The source interprets U.S. and European exclusion of Huawei and ZTE as a structural tailwind for Korean telecom equipment vendors. Germany is described as banning high-risk equipment and core parts in two phases, 2026 and 2029.

- AT&T plans to invest USD 250B, more than KRW 330T, from 2026 through 2030 and aims to process 70% of wireless traffic on Open RAN platforms by the end of 2026.

- Physical AI, robotics, autonomous driving, and smart factories require ultra-low latency and network slicing, supporting the shift to 5G SA and AI-RAN.

2. Portfolio and Moat

| Segment | Product group | Function |

|---|---|---|

| Mobile communications | Network optimization | Finds poor radio areas, analyzes performance bottlenecks, and measures quality in real time |

| Mobile communications | Big Data products | XDB and XDV monitor, collect, statistically process, and diagnose traffic data |

| Mobile communications | T&M | Portable base-station O&M measurement and automated lab testing in virtual network environments |

| Mobile communications | SmallCell | Secures coverage and offloads traffic where macro base stations are difficult or indoor signals are weak |

| Mobile communications | Defense | Collects, analyzes, and identifies electromagnetic signals; supports satellite-payload control and ground testing |

| Automotive | Automotive chips and V2X | Supplies MCUs and memory, and verifies CAV high-volume data and ultra-low-latency communications |

Official fact: The source says the wholly owned Accuver organization handles global sales, with service networks in seven major locations: Hong Kong, the U.S., Japan, the U.K., Poland, China, and India.

Interpretation: Innowireless products are closer to inspection infrastructure than commodity hardware. In 5G SA and AI-RAN, small delays and packet losses can be critical, so T&M and optimization solutions become necessities.

3. Small Cells and Subsidiary Restructuring

Small cells become more important because high-frequency 5G signals have weaker diffraction, making urban dense areas and indoor coverage harder to solve with macro base stations alone. The source says the small-cell business is normalizing after past hacking and supply-chain issues.

- On March 24, 2025, wholly owned Qcell Networks was merged into Innowireless.

- The source also presents 57.5%-owned V2X company Wayties and 100%-owned automotive semiconductor distributor Myeongsung Lifix as growth assets.

- The source views the merger positively because small-cell profits can belong 100% to controlling shareholders without minority-interest leakage.

4. 2025 Results and the 4Q Reversal

| Item | 2024 | 2025 | Change |

|---|---|---|---|

| Revenue | KRW 189.7B | KRW 186.1B | -KRW 3.6B, -1.9% |

| Operating profit | KRW 2.4B | -KRW 1.12B | -KRW 3.52B, swung to loss |

| Pre-tax profit | KRW 5.8B | -KRW 1.4B | -KRW 7.2B, swung to loss |

| Net income | KRW 2.9B | -KRW 1.14B | -KRW 4.04B, swung to loss |

Official fact: Cumulative 3Q operating loss is presented as KRW 8.9B. If full-year operating loss was KRW 1.12B, the source calculates that 4Q required roughly KRW 7.8B of operating profit, with broker estimates near KRW 9.2B.

- Based on a Hana Securities report cited in the source, expected 4Q revenue was KRW 71.9B, up 23% YoY and 73% QoQ.

- The source attributes the reversal to renewed high-margin T&M supply, new high-margin defense revenue, and recovering small-cell exports.

- Q is U.S. spectrum auctions and resumed Japanese small-cell supply, P is XDB/XDV plus defense and aerospace digital signal-processing equipment, and C is a fixed-cost structure centered on R&D personnel and software amortization.

5. R&D, Balance Sheet, and Returns

| Item | Source figure | Interpretation |

|---|---|---|

| Cumulative 3Q25 R&D | KRW 17.8B | 14.4% of revenue |

| Technology certification | XDB and XDV GS grade 1, KS Q 9100 | Preparation for telecom, defense, and aerospace work |

| Equity / liabilities | KRW 167.2B / KRW 61.9B | Survived the trough without dilutive outside capital |

| Credit rating | BBB to A- | Investment-grade ratings from eCredible, NICE Information Service, and Korea Ratings Data |

| Dividend | KRW 100 per share, 0.4% yield, KRW 760M total | Dividend maintained despite KRW 1.14B annual net loss |

Interpretation: The source reads maintaining the dividend during a loss year as management's confidence in 4Q cash generation and the 2026 order cycle.

6. Valuation, Catalysts, and Risks

- The source says the stock is around the lower end of its historical band, near PBR 1x.

- It cites analyst Kim Hong-sik of Hana Securities raising the target price from KRW 40,000 to KRW 60,000, up 50%, by applying target PBR of 3x.

- The stock rebounded from a 52-week low of KRW 16,610 and traded with volatility in the KRW 33,000~48,800 band; the source says a move beyond the 2021 high of KRW 55,000 remains open.

- Catalysts are formalization of the U.S. 800 MHz auction schedule, large North American and global MNO orders, and 1Q26 results proving the 4Q profit trend is not one-off.

- Risks are carrier capex delays, slower rate cuts, a short-term RSI above 70 after a rapid rally, and volatility until net profit turns visibly positive.

- The source presents the 20-day moving average around KRW 31,000~34,000 and the 60-day moving average around KRW 25,000~28,000 as key support zones.

7. My Conclusion

Innowireless is a company where the surface annual loss conflicts with the 4Q inflection. The key is whether AT&T Open RAN, Chinese-equipment exclusion, and the 5G SA transition for Physical AI convert into actual orders.

Interpretation: As the source argues, Open RAN creates more complex multi-vendor networks, which should increase the need for measurement and optimization tools. Whether Innowireless can turn that need into orders and recurring revenue is the 2026~2028 watchpoint.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224217157647

- Source 2: https://www.kita.net/board/overseasMarketNews/overseasMarketNewsDetail.do?postIndex=1846851&boardType=0

- Source 3: https://biz.chosun.com/it-science/ict/2026/02/25/63MNHBWNMVAV3EYU3HZXC7Z4IU/

- Source 4: https://www.youtube.com/watch?v=A2rBdEr5vhI

- Source 5: https://file.alphasquare.co.kr/media/pdfs/market-report/%ED%86%B5%EC%8B%A0%EC%96%91%EC%9E%90%EC%97%9020260304%ED%95%98%EB%82%98%EC%A6%9D%EA%B6%8C

- Source 6: https://www.telecompetitor.com/att-is-gung-ho-on-open-ran-upgrading-70-of-mobile-network-by-2026/

- Source 7: https://www.telecomstechnews.com/news/att-plans-most-wireless-traffic-flow-across-open-ran-by-2026/

- Source 8: https://www.ericsson.com/en/news/2023/12/ericsson-and-att-in-major-future-network-of-the-future-deal

- Source 9: https://about.att.com/story/2023/commercial-scale-open-radio-access-network.html

- Source 10: https://www.ericsson.com/en/press-releases/2023/12/att-to-accelerate-open-and-interoperable-radio-access-networks-ran-in-the-united-states-through-new-collaboration-with-ericsson

- Source 11: https://www.mobileworldlive.com/att/att-ericsson-make-live-open-ran-call/

- Source 12: https://www.hankyung.com/article/202603114324i

- Source 13: https://m.newspim.com/news/view/20260304000129

- Source 14: https://www.newspim.com/news/view/20251126000145

- Source 15: https://www.thepowernews.co.kr/view.php?ud=202511211033518775de3f0aa1be_7

- Source 16: https://www.judal.co.kr/?view=stockAI&shareToken=fOieaq8S1a2g1f0q

- Source 17: https://www.judal.co.kr/?view=stockAI&shareToken=4Cgzr525OjJADhZj

- Source 18: https://www.datatooza.com/article/20251126095322975252ef3b9bae_80

- Source 19: https://www.iprovest.com/weblogic/RSNewsServlet?scr_id=17&mode=detail&listnum=239&dgubun=4&ymd=20260204&seqno=15474611

- Source 20: https://www.judal.co.kr/?view=stockAI&shareToken=OmmzJRkYpzOwkTGd