DEEP RESEARCH · AT&T

AT&T 4Q25 and Investor Update: Infrastructure Power in the Physical AI Era

How 5G SA, edge computing, fiber, spectrum, and security investment can reshape a telecom moat

0. Bottom line first

AT&T's USD 250B infrastructure plan through 2030 is not routine network maintenance. I read it as a strategy to pre-empt the ultra-low-latency data infrastructure needed for physical AI. The source's core argument is that AT&T is combining 5G SA, edge computing, fiber, spectrum, satellite, and quantum-safe security into a physical nervous system that competitors will struggle to replicate.

USD 250B

A five-year infrastructure master plan through 2030.

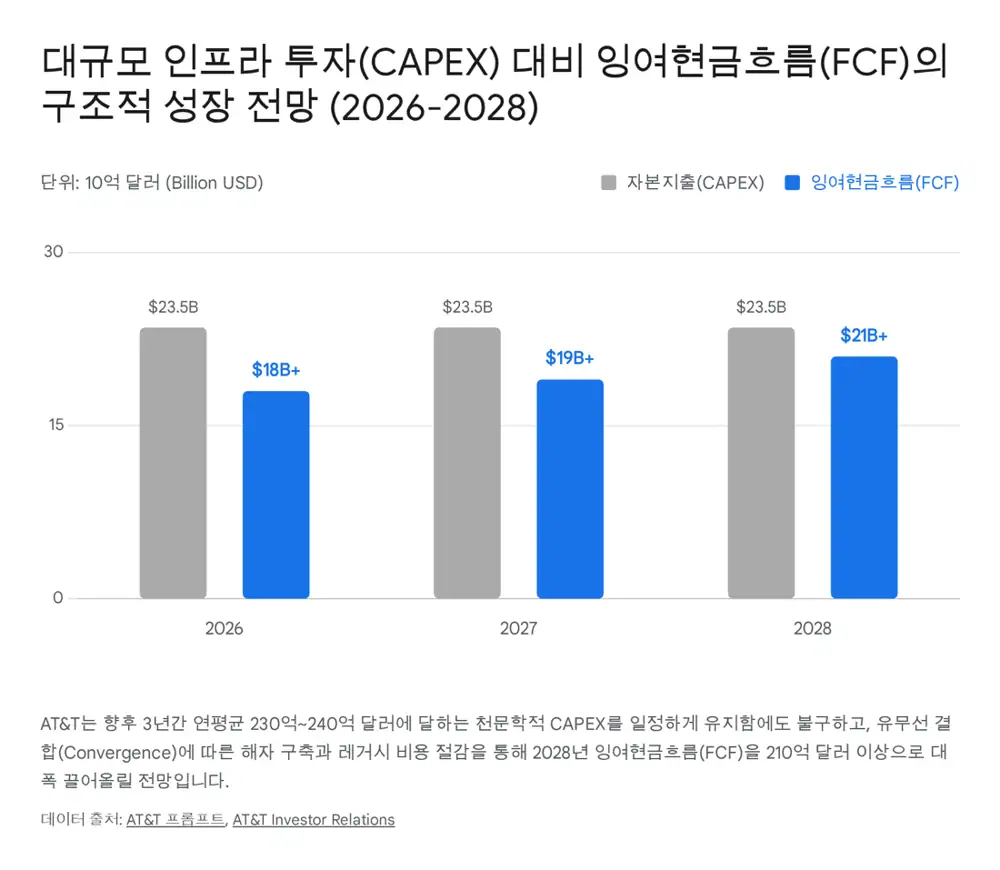

USD 23B-24B

Annual CAPEX guidance, driven by physical-AI traffic and edge-infrastructure rebuild.

USD 21B+ FCF

The source expects 2028 FCF to exceed 2024's USD 15.3B and 2025's USD 16.6B despite heavy CAPEX.

Official fact: The source says AT&T presented a total CAPEX plan of USD 250 billion through 2030, with annual CAPEX of USD 23-24 billion, after solid 4Q25 results. It also says AT&T plans more than USD 45 billion of combined dividends and buybacks for 2026-2028, including about USD 8 billion of buybacks in 2026.

Interpretation: Near term, the CAPEX load can create FCF concerns. But the payback case exists if the 42% fiber-wireless convergence ratio, legacy copper shutdown, OBBBA tax benefits, and B2B/B2G ultra-low-latency revenue model work together.

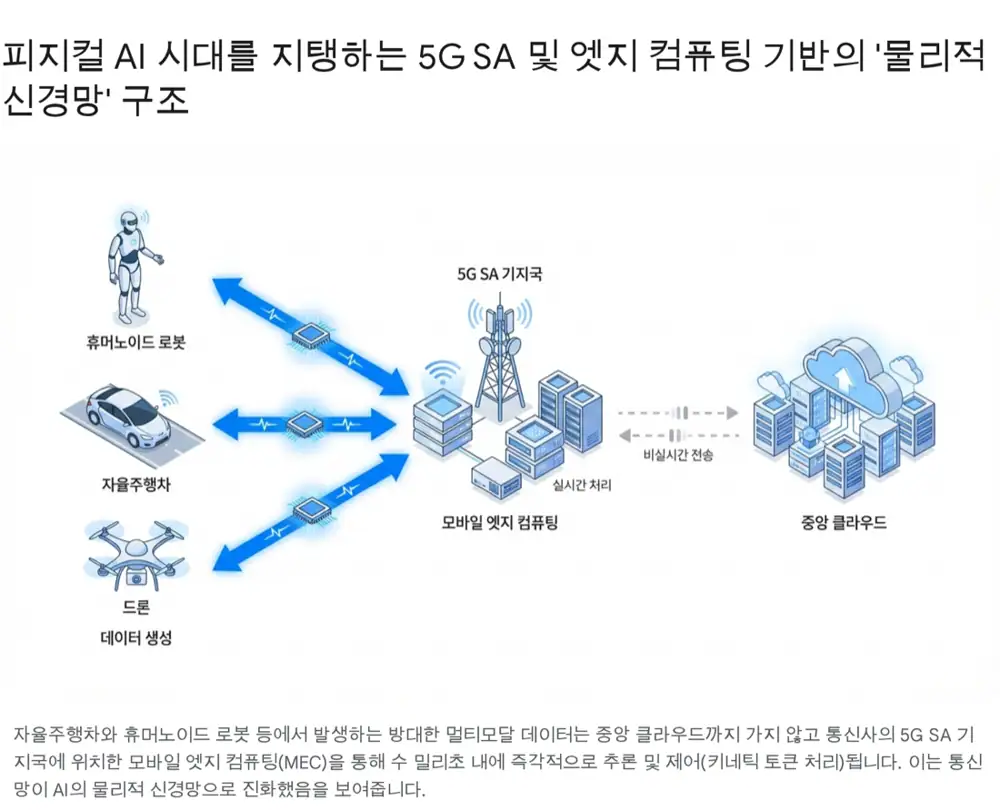

1. Physical AI and the changing telecom role

The source argues that AI is moving from data-center LLMs toward physical AI combined with robots, autonomous vehicles, UAM, and real-time interaction in the physical world. In that environment, sensors, cameras, and robotic joints generate terabytes of multimodal data per second, and telecom operators shift from dumb pipes to intelligent infrastructure platforms responsible for the physical nervous system.

- Latency: Unlike informational tokens used for summarization and text generation, physical AI kinetic tokens require millisecond-level response.

- 5G SA: Unlike NSA 5G, standalone 5G uses an independent cloud-native core, reduces latency, and can provide dedicated QoS to surgical robots or autonomous vehicles through network slicing.

- Edge computing: Telecom base stations, central offices, and switching offices already have power, cooling, and real estate that can be converted into MEC nodes.

- Revenue model: Beyond B2C smartphone-rate competition, new revenue sources include B2B/B2G AI-compute infrastructure leasing, dynamic network-API charging, and SLA-based premium private networks.

2. CAPEX structure: wireless, wireline, satellite, security

AT&T's investment expansion is meant to create the uplink capacity, reliability, ultra-low latency, and edge infrastructure physical AI requires. The source interprets 5G SA conversion of hundreds of thousands of U.S. base stations, conversion of switching offices into MEC nodes, and fronthaul/backhaul fiber investment as turning the whole telecom network into a distributed AI computing resource.

| Asset | Target and size | Strategic value |

|---|---|---|

| Wireless spectrum | EchoStar, about USD 23B | Secures 600MHz low-band and 3.45GHz mid-band spectrum, strengthening both wide-area coverage and traffic capacity. |

| Fiber | Lumen mass-market assets, about USD 5.75B | Adds 1 million subscribers and 4 million fiber-passed locations, densifying the backhaul path from edge to cloud. |

| Satellite / NTN | AST SpaceMobile strategic partnership | Uses LEO satellite communication to extend Always-On coverage to mountains, deserts, seas, and other coverage gaps. |

| Quantum-safe security | Dynamic Defense, QKD, PQC | Rebuilds network core, routers, and optical transport around security against Q-Day and harvest-now-decrypt-later attacks. |

Interpretation: If the EchoStar and Lumen transactions close in 1H26 as described, AT&T would control a three-part wireless, fiber, and satellite structure. That is not just coverage expansion; it is internalizing the paths that future physical-AI traffic will use.

3. Payback logic: convergence, copper shutdown, 2028 guidance

The Wall Street concern is that annual CAPEX above USD 23B can pressure near-term FCF. The source answers with three payback mechanisms.

42% fiber-wireless

Among AT&T Fiber households, 42% also use AT&T wireless. Converged customers have lower churn and higher LTV.

Copper shutdown by 2029

Legacy copper networks are planned to be powered down by the end of 2029, reducing power, maintenance, and truck-roll costs.

5%+ adjusted EBITDA growth

After 3-4% growth in 2026, guidance points to 5% or better by 2028 from copper shutdown and Advanced Connectivity growth.

| Item | Source number | Meaning |

|---|---|---|

| Legacy revenue | Down more than 20% in 2026, immaterial by end-2029 | Customers are migrated to Advanced Connectivity such as AIA and fiber. |

| Legacy EBITDA | Short-term negative EBITDA accepted through 2027 | Losses are accepted until direct costs of copper operations are removed. |

| FCF | USD 15.3B in 2024, USD 16.6B in 2025, USD 21B+ in 2028 | The scenario assumes structurally improved operating cash generation despite large CAPEX. |

| Shareholder returns | USD 45B+ in 2026-2028, USD 8B buyback in 2026 | A signal that management expects to fund both CAPEX and capital returns. |

4. OBBBA and spectrum policy

The source treats the One Big Beautiful Bill Act, signed by President Donald Trump on July 4, 2025, as a telecom investment catalyst. Key items are permanent 100% bonus depreciation for qualified assets acquired after January 19, 2025, restored immediate R&E expensing, restored FCC auction authority, and a new 800MHz commercial spectrum pipeline.

| OBBBA item | Impact on AT&T |

|---|---|

| Permanent 100% bonus depreciation | Allows full immediate expensing of qualifying CAPEX installed after January 19, 2025, creating more than USD 1B of annual tax savings. |

| Immediate R&E expensing | Improves liquidity for next-generation R&D such as quantum cryptography and AI network architecture. |

| FCC auction authority restored | Restores FCC spectrum auction authority through September 2034, reducing uncertainty around spectrum access. |

| 800MHz spectrum pipeline | Requires at least 800MHz of federal spectrum, including 3.98-4.2GHz upper C-band, to be identified and auctioned for commercial use within two years. |

The source says AT&T management expects OBBBA tax provisions to save USD 1.0-1.5 billion in annual cash taxes, funding more than 1 million additional fiber homes per year and working-capital expansion.

5. Geopolitics: China equipment exclusion and national-security premium

U.S. and EU exclusion of Chinese telecom equipment is reshaping the telecom-equipment supply chain. The source says the U.S. Congress added USD 3 billion to the Rip and Replace program through the late-2024 NDAA, and that the EU is moving toward forcing phase-out of high-risk supplier equipment within three years.

- Western vendors benefit: With Huawei and ZTE excluded, North American and European carriers must rely more heavily on Ericsson and Nokia.

- Korean component spillover: The source flags RFHIC, which supplies GaN transistors to Ericsson, and KMW, which makes high-performance antennas and next-generation RF filters, as potential geopolitical beneficiaries.

- FirstNet: AT&T is described as the design and operating partner for America's national public-safety network FirstNet, responsible for more than 6 million connections.

- Dynamic Defense: Detecting and blocking DDoS and hacking at the network-core layer can create an intangible advantage in Department of Defense, federal infrastructure, and critical-facility contracts.

6. Risks and my view

The source frames AT&T as an Overweight and long-term holding. I see three prerequisites for that conclusion. First, the USD 250B CAPEX must truly translate into integrated 5G SA, edge, fiber, satellite, and security assets. Second, short-term negative EBITDA and legacy revenue decline from the copper shutdown must be absorbed by Advanced Connectivity and B2B/B2G revenue. Third, OBBBA tax benefits and spectrum supply must proceed as planned.

Interpretation: The upside is clear. If AT&T builds the physical nervous system while competitors delay CAPEX, the entry barrier rises. The main risk is equally clear: if monetization of new traffic is late, the investment scale can pressure FCF and shareholder-return expectations at the same time.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224217055663

- SiTime: Edge Computing, Edge AI & Physical AI: https://www.sitime.com/company/newsroom/blog/what-edge-computing-edge-ai-and-physical-ai

- Medium: Telco AI and 6G nervous system: https://medium.com/@mountdavistechnologies/physical-ai-the-6g-nervous-system-or-another-costly-telco-mirage-dae5eb85634f

- Deloitte: TMT Predictions 2026: https://www.deloitte.com/us/en/insights/industry/technology/technology-media-and-telecom-predictions.html

- Fierce Network: kinetic tokens and 6G: https://www.fierce-network.com/wireless/exclusive-t-mobiles-john-saw-explains-kinetic-tokens-and-why-they-matter-6g

- Ericsson: intelligent fabric: https://www.ericsson.com/en/blog/2026/1/ai-future-will-be-defined-by-the-intelligent-digital-fabric

- Ericsson: SoftBank and Ericsson AI-RAN demo: https://www.ericsson.com/en/press-releases/2026/2/softbank-corp-and-ericsson-demonstrate-network-enabled-physical-ai-with-ai-ran

- NVIDIA Blog: 2025 AI predictions: https://blogs.nvidia.com/blog/industry-ai-predictions-2025/

- The Mobile Network: Ericsson AI into RAN, edge and AWS: https://the-mobile-network.com/2026/02/ericsson-driving-ai-into-the-ran-edge-and-aws/

- Juniper Research: Post-quantum cryptography market: https://www.juniperresearch.com/press/post-quantum-cryptography-market-to-exceed-13-billion-by-2035-as-q-day-awareness-accelerates/

- Quantum Xchange: Post-Quantum Cryptography in 2026: https://quantumxc.com/blogs-podcasts/quantum-predictions-it-network-infrastructure/

- SandboxAQ: PQC, QKD and crypto-agility: https://www.sandboxaq.com/post/pqc-qkd-and-crypto-agility-for-quantum-threats

- World Economic Forum: quantum-safe migration: https://www.weforum.org/stories/2026/01/quantum-safe-migration-cryptography-cybersecurity/

- Peterson Foundation: OBBBA federal spending: https://www.pgpf.org/article/how-did-the-one-big-beautiful-bill-act-affect-federal-spending/

- RSM US: OBBBA telecom tax implications: https://rsmus.com/insights/services/business-tax/obbba-tax-telecom.html

- Texas Capital: OBBBA tax guide: https://texascapitalbank.com/insights/ultimate-guide-how-one-big-beautiful-bill-act-impacts-your-taxes

- Wikipedia: One Big Beautiful Bill Act: https://en.wikipedia.org/wiki/One_Big_Beautiful_Bill_Act

- AT&T: Fiber expansion following OBBBA: https://about.att.com/story/2025/accelerating-fiber-network-expansion-one-big-beautiful-bill-act.html

- Bloomberg Government: OBBBA guide: https://about.bgov.com/insights/federal-policy/guide-to-the-one-big-beautiful-bill/

- SiliconANGLE: $3B rip and replace funding: https://siliconangle.com/2024/12/25/us-allocates-3b-rip-replace-chinese-technology-smaller-telcos/

- Broadband Breakfast: EU high-risk supplier phase-out: https://broadbandbreakfast.com/eu-plans-to-phase-out-high-risk-telecom-suppliers-targeting-china/

- Telecoms Tech News: China telecom reviews impact on Nokia and Ericsson: https://www.telecomstechnews.com/news/china-telecom-reviews-deal-a-blow-to-nokia-and-ericsson/

- Light Reading: Huawei/ZTE rip and replace: https://www.lightreading.com/mobile-core/fcc-moves-toward-ripping-huawei-zte-equipment-out-of-us-networks

- AT&T IR: Q2 2024 earnings call transcript: https://investors.att.com/~/media/Files/A/ATT-IR-V2/financial-reports/quarterly-earnings/2024/2Q24/t-usq-transcript-2024-07-24.pdf