DEEP RESEARCH · AVATEC (149950)

AVATEC 4Q25 Results and the MLCC/OLED Structural Shift

A combined review of the 4Q25 profit turn, KRW 90bn MLCC CAPEX delay, and controlling-shareholder earnings quality

0. Bottom line first

The core of my AVATEC view is earnings growth despite lower revenue. 2025 revenue fell 4.26% year over year to KRW 80.944bn, but operating profit rose 6.05% to KRW 6.148bn. In the source, my conclusion was Strong Buy; in this report, I break that view into the numbers, CAPEX, customer cycles, and risks.

Official fact: The source notice says the writer is a beginner investor without extensive investment experience, that the post is a personal study record, and that it was written using Gemini.

KRW 21.733bn

Fourth-quarter revenue rose 39.52% year over year, with operating profit of KRW 2.701bn and net income of KRW 2.457bn, turning profitable.

KRW 8.574bn

MLCC revenue jumped from KRW 307mn in 2024 to KRW 8.574bn in 2025, or about 28 times.

7.41% debt ratio

At end-2025, cash and equivalents were KRW 50.75bn and total liabilities were KRW 11.27bn, close to a net-cash, nearly debt-free structure.

June 30, 2027

The KRW 90bn MLCC expansion end date was pushed from October 31, 2025 to June 30, 2027. I read this less as a simple delay and more as timing adjustment to demand recovery.

Official fact: The source states that AVATEC's standalone revenue for the first nine months of 2025 fell 14.1% year over year, while operating profit and net income both fell more than 60%. But 4Q25 revenue was KRW 21.733bn, operating profit was KRW 2.701bn, and net income was KRW 2.457bn.

Interpretation: On the surface, revenue contracted. Underneath, the mix improved: lower-margin LCD exposure shrank, while hybrid OLED slimming and solar-inverter MLCC expanded, lifting operating margin from 6.8% to 7.6%.

1. The 4Q25 Earnings Surprise: Mix Changed More Than Sales

AVATEC's 2025 results were an optical-misread period where headline numbers and earnings quality moved in different directions. Through 3Q, display-cycle volatility and customer utilization adjustments weighed heavily on revenue, operating profit, and net income. In 4Q, the situation reversed, and the full-year result became operating-profit growth despite lower revenue.

| Item | 2024 | 2025 | Driver |

|---|---|---|---|

| Total revenue | KRW 84.54bn | KRW 80.94bn | Overall scale declined slightly due to weaker LCD end demand. |

| Display revenue | KRW 84.23bn | KRW 72.37bn | LCD utilization fell from 38% to 35%, while OLED stayed solid. |

| MLCC revenue | KRW 0.30bn | KRW 8.57bn | SolarEdge-bound export volume increased, about 28x growth. |

| Operating profit | KRW 5.79bn | KRW 6.14bn | Higher share of high-margin hybrid OLED and MLCC. |

| Operating margin | 6.8% | 7.6% | Lower low-margin products, higher value-added products. |

1.1 MLCC revenue quantum jump

The MLCC business used to be a small part of the portfolio, but its meaning changed in 2025. MLCC revenue surged from KRW 307mn in 2024 to KRW 8.574bn in 2025, while MLCC exports rose from roughly KRW 7mn in 2024 to KRW 5.746bn in 2025. The source interprets this as evidence that high-reliability MLCC supply for SolarEdge Technologies' solar inverters entered full-scale mass-production mode in 2H25.

1.2 Quality growth in OLED slimming

AVATEC's traditional LCD Glass Slimming utilization fell from 38% in 2024 to 35% in 2025. By contrast, OLED Glass Slimming utilization moved from 15% in 2023 to 66% in 2024 and 65% in 2025, staying high. The source's central interpretation is that Apple's adoption of glass-substrate hybrid OLED in the iPad Pro increased demand for AVATEC's panel-thinning etching process.

Interpretation: Hybrid OLED slimming carries higher unit pricing and higher process difficulty than commodity LCD slimming. That is why it can defend company-wide profitability even when total panel-related revenue declines.

2. Earnings Quality: Controlling-Shareholder Income and Per-Share Value

AVATEC's 2025 net income of KRW 6.91bn maps directly to parent-shareholder earnings without subsidiary losses or non-controlling-interest leakage. The source sees AVATEC's end-2025 single-entity structure, with no consolidated subsidiaries, as a key earnings-quality point.

KRW 6.91bn

2025 net income can be interpreted directly as controlling-shareholder net income.

1,939,797 shares

On September 25, 2025, AVATEC retired all treasury shares with an acquisition cost of about KRW 16.82bn through retained-earnings cancellation.

About 12.4%

The retired shares were about 12.4% of the 15,607,500 shares outstanding.

DB to DC

During 2025, the retirement pension plan for all employees was converted from defined-benefit to defined-contribution.

Official fact: The source says roughly KRW 13.89bn of external pension assets were replaced by the DC plan during the conversion, with settlement gains or losses recognized.

Interpretation: Defined-benefit plans create actuarial gains and losses as wage-growth rates and discount rates change. Moving to DC reduces future retirement-benefit liability risk and comprehensive-income volatility. Combined with the 12.4% treasury retirement, future earnings growth can flow more sensitively into EPS and ROE.

3. KRW 90bn MLCC CAPEX: Delay or Strategic Realignment?

In April 2023, AVATEC disclosed a KRW 90bn investment for new MLCC production buildings and equipment expansion. The strategy was to address automotive and industrial MLCC demand beyond legacy IT MLCC for smartphones and similar devices. The investment end date, however, was delayed by about one year and eight months, from October 31, 2025 to June 30, 2027.

The source argues that the market often misreads large-investment delays as weak demand or funding trouble. SolarEdge, however, went through inventory destocking across 2024 and 1H25 because of prolonged high rates and excess European solar-inverter inventory. If AVATEC had force-started a KRW 90bn new line at end-2025 without enough volume, heavy depreciation would likely have hit cost of sales before revenue caught up.

Official fact: The source states that SolarEdge's 4Q25 revenue was USD 335.4mn, up 71% from USD 196.2mn a year earlier, and that the company delivered four consecutive quarters of year-over-year revenue growth. It also cites CEO Shuki Nir's 2026 comments around the Nexis platform, global share expansion, AI data-center power, adjacent growth areas, and profitable growth.

Interpretation: Pushing the KRW 90bn CAPEX completion into mid-2027 can be read as aligning capacity with SolarEdge's rebound, North American and European solar infrastructure investment, and the AI data-center power demand cycle across 2026~2027.

3.1 Financial strength: enough balance sheet to absorb CAPEX

| Item | End-2025 figure | Meaning |

|---|---|---|

| Current assets | About KRW 72.26bn | Short-term liquidity base |

| Cash and equivalents | KRW 50.75bn | Core resource to absorb a large investment schedule |

| FVTPL financial assets and other short-term financial assets | About KRW 5.07bn | Liquid financial assets |

| Avaco stake | 4.97%, about KRW 9.97bn | Investment asset, fair-value basis |

| Current / non-current liabilities | KRW 10.78bn / KRW 0.48bn | Total liabilities of about KRW 11.27bn |

| Total equity | KRW 152.0bn | Debt ratio of 7.41% |

If the KRW 90bn investment is completed and the new MLCC factory comes online across 2H26~2027, the source expects existing annual capacity of about 1.44bn units to expand sharply. 2025 MLCC utilization was still around 36%. If SolarEdge demand recovery lifts that figure toward 70~80% in 2026, operating leverage can become the central earnings driver.

4. 2026~2027 Sustainability: End Markets Through Q, P, and C

If AVATEC's 2025 result is not a short-term peak, quantity, price, and cost must all improve through 2026~2027. The source argues that technology-standard shifts in display and electronic components support that possibility.

IT OLED and MLCC volume

OLED adoption in tablets, notebooks, and automotive displays plus EV, autonomous-driving, and AI-power demand create volume growth.

High-end ASP

Hybrid OLED slimming and 50V~100V-class high-reliability MLCC have better pricing power than commodity LCD or small IT MLCC.

Depreciation control

The burden from the 2018 KRW 45bn first MLCC investment has largely passed, and the company turned profitable even at low utilization.

4.1 Q: hybrid OLED and AI/automotive MLCC

In display, the central demand driver is IT-device OLED transition. OLED is expanding from smartphones into tablets, notebooks, and in-vehicle infotainment displays. Apple first adopted OLED in the iPad Pro in 2024, and the source includes the view that adoption will broaden to MacBooks and other formats from 2026.

LG Display, AVATEC's major customer and second-largest shareholder, is borrowing KRW 1tn from LG Electronics to invest in eighth-generation IT OLED and automotive OLED lines. For AVATEC, a post-processing company that slims OLED panels and coats surfaces, that implies long-term volume spillover.

In MLCC, electrification and autonomous driving lift demand. The source says an internal-combustion vehicle typically uses thousands of MLCCs, while an EV or autonomous vehicle equipped with ADAS and dozens of ECUs needs at least 15,000 and sometimes more than 20,000 MLCCs per vehicle. AVATEC has passed AEC-Q200 testing, obtained IATF-16949 certification, and built an automotive high-reliability MLCC lineup at 100V class and above.

Another demand source is SolarEdge's AI data-center power solution. AI servers consume heavy power and generate heat, requiring high-capacity, high-reliability industrial MLCC. On that combined demand, the source presents a 2026 standalone revenue forecast of KRW 103.5bn and operating profit of KRW 10.5bn, up about 29.7% and 125.1% year over year.

4.2 P: high-end mix changes ASP

Traditional LCD slimming was exposed to Chinese panel supply expansion and price-reduction pressure. In contrast, Apple's IT hybrid OLED slimming is a high-difficulty process: the thick glass substrate must be etched extremely thin while preserving panel rigidity and flatness. The source says AVATEC stabilized yield by combining proprietary screen-printing methods with precision chemical etching.

The same logic applies to MLCC. Commodity small IT MLCC has become a red ocean under Chinese low-price pressure, while high-voltage solar micro-inverter MLCC and automotive 50V~100V-class MLCC require strict quality validation and are supplier-favorable, premium-priced markets.

4.3 C: low utilization becomes the source of leverage

In 2021~2022, AVATEC absorbed profitability damage from depreciation on the KRW 45bn first MLCC investment made in 2018 and from early yield-stabilization costs. By 2025, the source judges that much of this burden had passed and manufacturing yield had stabilized beyond breakeven.

In 2025, LCD slimming utilization was 35% and MLCC plant utilization was 36%. In manufacturing, utilization in the 30% range usually struggles to cover fixed costs. Yet AVATEC turned profitable in 4Q25 and generated KRW 6.1bn of annual operating profit. If utilization rises to 50% or 70%, incremental volume can flow quickly into operating profit.

Interpretation: The source views 2026~2027 as the early stage of a profit rally in which operating margin could move from 7.6% toward the high teens and possibly 20%. That view only works if utilization recovery actually appears.

5. Competitive Advantages: In-Line Process, LG Display, and MLCC Micro Technology

A manufacturer needs an economic moat to sustain high returns on capital. The source divides AVATEC's moat into integrated display post-processing, the captive relationship with LG Display, and MLCC micro-technology.

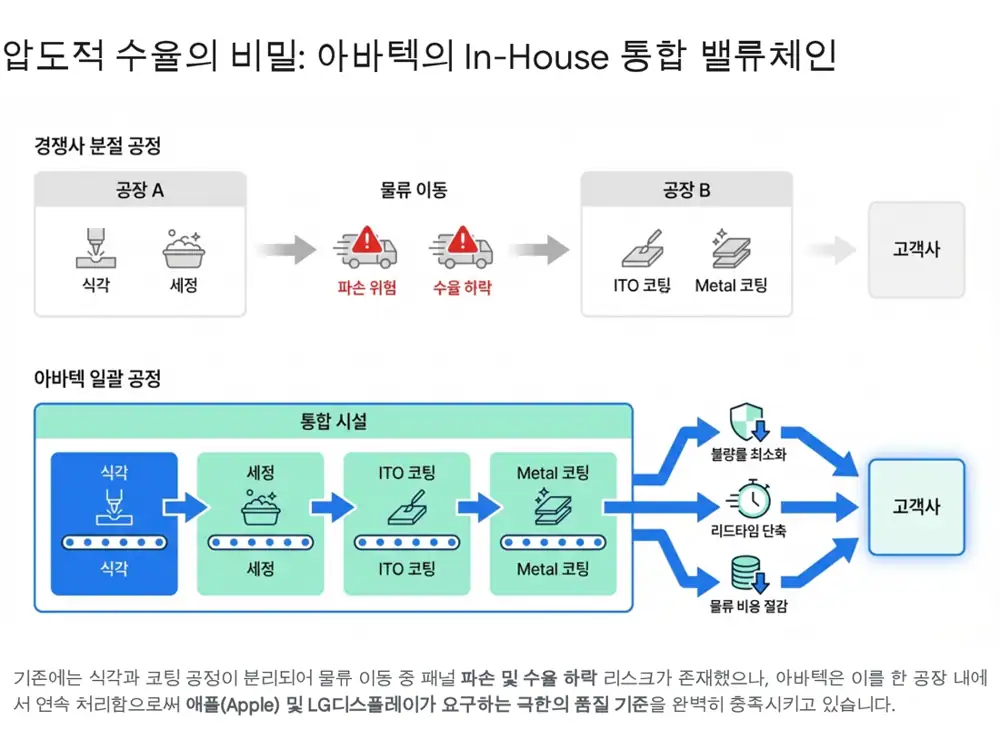

5.1 In-house batch processing

Glass Slimming sits at the late end of panel manufacturing. If a tiny scratch or break occurs there, the cost of prior color-filter and TFT substrate work is also damaged. That is why panel makers such as LG Display outsource etching only to a small number of fully qualified partners.

AVATEC's advantage is an in-house batch system that continuously handles Glass Slimming, ITO coating, and Metal coating in one factory. In the old value chain, etched glass had to be trucked to a separate coating specialist, creating scratch risk from vibration and dust and increasing lead time. AVATEC's in-line setup reduces defects, logistics cost, and delivery time at once.

5.2 LG Display and captive market

AVATEC is a core strategic supplier of LG Display and a partner connected by equity ownership. In July 2024, LG Display sold 1.6% of its AVATEC stake, or 250,000 shares, through a block deal at KRW 12,574 per share, lowering its stake from 11.23% to 9.63%.

Interpretation: The source interprets this not as weaker cooperation but as LG Display raising liquidity for its KRW 1tn eighth-generation IT OLED investment. A stake in the 9% range still signals a strategic alliance, and LG Display's IT OLED expansion can translate into AVATEC etching and coating volume.

5.3 MLCC micro technology

An MLCC is made by spreading ceramic dielectric powder and metal electrodes thinner than paper, stacking hundreds to thousands of alternating layers, and firing them at high temperature. Because the shrinkage rates of ceramic and metal must be controlled uniformly to prevent cracks while preserving electrical properties, the entry barrier resembles semiconductor micro-processing.

AVATEC transferred thin-film control know-how accumulated over more than 20 years of display-parts coating, including vacuum deposition and wet coating, into MLCC manufacturing. The source cites sub-150nm dielectric-material dispersion technology, ultra-thin product development, a niche in high-voltage/high-reliability solar-inverter products, R&D spending around 0.98% of revenue, and eight Korean patents as moat evidence.

6. Valuation, Catalysts, and Risks

The source argues that the market is leaving AVATEC on low PER/PBR multiples by focusing only on 2025 revenue contraction and the declining LCD display industry frame. The counterargument is that legacy LCD exposure is shrinking while IT hybrid OLED slimming and solar/automotive MLCC are filling the gap.

| Upside logic | Counterpoint to monitor |

|---|---|

| Permanent retirement of 1.93mn treasury shares, or 12.4% of total shares, makes per-share value more sensitive. | Earnings growth must translate into actual controlling-shareholder income and cash flow for EPS improvement to persist. |

| More than KRW 50.7bn of net cash and a 7.4% debt ratio reduce enterprise-value burden on an EV/EBITDA view. | If the KRW 90bn CAPEX is delayed again, the market may discount growth visibility. |

| SolarEdge AI data-center power and Apple's IT OLED expansion are potential multiple-rerating catalysts. | If Apple's high-end IT demand disappoints or solar recovery remains slow, utilization recovery can be delayed. |

6.1 Rerating catalysts

- SolarEdge AI data-center revenue visibility: If SolarEdge reports concrete profitable-growth and AI data-center power progress after 1H26, AVATEC's MLCC utilization recovery may begin to show in quarterly financials.

- Apple's IT OLED model expansion: If hybrid OLED adoption expands beyond iPad Pro into MacBook and other large-area IT devices from 2026, AVATEC's processed etching area can increase.

6.2 Key risks

- Global IT demand slowdown: Prolonged high rates or macro weakness could make Apple's premium IT product sales miss expectations, delaying OLED slimming utilization growth through LG Display and AVATEC.

- Additional KRW 90bn CAPEX delay: If SolarEdge inventory digestion or global solar recovery is slow, the expansion schedule already delayed to June 2027 could move again. The source still views this as more of a safety valve against idle-capacity fixed costs than an existential risk.

6.3 Final investment conclusion in the source

The source concludes that AVATEC is a Strong Buy at the early stage of long-term growth. The logic has three parts. First, the portfolio has shifted from LCD to advanced OLED and from a single display-component company to a composite electronic-parts company with MLCC. Second, the large investment delay is interpreted as a financial-defense strategy synchronized with demand recovery. Third, permanent retirement of 12.4% of tradable shares and the DC pension conversion are presented as improvements in capital allocation and accounting quality.

In strategy terms, the source recommends trusting the high-profit mix shown in 4Q25, accumulating on share-price corrections, and holding through late 2026 to 2H27, when the KRW 90bn MLCC factory could come online and revenue growth plus fixed-cost leverage could appear together.

7. Appendix: MLCC in SolarEdge Inverters and the Competitive Field

The end of the source includes a separate memo explaining the role of MLCC inside SolarEdge inverters, how AVATEC entered the supplier base, and the industrial MLCC competitors. That memo describes SolarEdge as a global No. 1 company in power optimizers and inverter systems that maximize solar-panel generation efficiency.

Voltage-noise filtering

MLCCs in solar inverters reduce voltage noise in circuits and help deliver stable power to semiconductors and core components.

High voltage, high reliability

Because solar equipment is exposed outdoors for long periods, high-capacity, high-voltage, high-reliability industrial MLCCs are needed.

Ultra-thin-film control

The source presents AVATEC's transfer of display post-process thin-film control technology into MLCC manufacturing as the basis for becoming a supplier.

Official fact: The source memo states that AVATEC used sub-150nm dielectric-material dispersion technology to develop high-voltage 50V~100V-class and above, high-reliability X7R products for solar inverters, passed more than one year of quality and reliability validation, and signed an approximately KRW 3.4bn supply contract with SolarEdge in August 2022.

| Competitor | Source memo description |

|---|---|

| Murata Manufacturing | Presented as the global No. 1 MLCC player with about 34~40% share and strong competitiveness in high-reliability products. |

| Samsung Electro-Mechanics | Presented as the global No. 2 player expanding automotive, industrial, and solar high-voltage MLCC lineups based on ultra-small, ultra-high-capacity technology. |

| TDK, Taiyo Yuden, Yageo, Kyocera AVX | Mentioned as major competitors leading renewable-energy and high-voltage MLCC markets. |

The Tistory OG card displayed an AVATEC (A149950) Company Guide snapshot, homepage http://www.avatec.co.kr, phone number 053-592-4060, IR contact 053-602-4022, address 100 Dalseo-daero 85-gil, Dalseo-gu, Daegu, and KOSDAQ IT H/W sector information.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224215700794

- AVATEC 4Q operating profit KRW 2.7bn, profit turn - Daum: https://v.daum.net/v/plR3h2qFEJ

- AVATEC 2025 fourth-quarter results - Investing.com: https://kr.investing.com/news/company-news/article-93CH-1844058

- AVATEC analysis: OLED slimming plus MLCC - YouTube: https://www.youtube.com/watch?v=Dw-FPpCnIpw

- AVATEC to start MLCC second plant in 1H - TheElec: https://www.thelec.kr/news/articleView.html?idxno=20051

- AVATEC highlighted for OLED iPad glass-substrate etching - BigDataNews: https://www.thebigdata.co.kr/view.php?ud=202404080515558785cd1e7f0bdf_23

- AVATEC IT OLED tablet volume upside - DailyInvest: http://www.dailyinvest.kr/news/articleView.html?idxno=60149

- AVATEC delays MLCC expansion completion to June 2027 - MPENews: https://www.mpenews.co.kr/news/articleView.html?idxno=3603

- SolarEdge Q4 and full-year commentary - Renewable Energy Industry: https://www.renewable-energy-industry.com/news/world/article-7245-solaredge-on-recovery-path-solaredge-increases-revenue-in-q4-and-full-year-losses-decline-stock-still-under-pressure

- SolarEdge Q4 2025 Prepared Remarks: https://investors.solaredge.com/static-files/b31321e9-5a8e-42c0-9646-9eaa2e5fe9ce

- SolarEdge Fourth Quarter and Full Year 2025 Financial Results: https://investors.solaredge.com/news-releases/news-release-details/solaredge-announces-fourth-quarter-and-full-year-2025-financial

- SolarEdge reduces net loss in 2025 as revenue increases to US$1.1 billion - PV Tech: https://www.pv-tech.org/solaredge-reduces-net-loss-in-2025-as-revenue-increases-to-us1-1-billion/

- AVATEC and LGD OLED investment theme - iNews24: https://www.inews24.com/view/1579502

- AVATEC fourth-quarter maximum results outlook, fourth day up +1.43% - Dealsite: https://dealsite.co.kr/articles/47161/089059

- AVATEC 149950 - Tistory: https://spp5908.tistory.com/16710

- AVATEC homepage: http://www.avatec.co.kr