DEEP RESEARCH · SANDS LAB

Sands Lab: The AI Security Platform Pivot Behind the SI Revenue Jump

Reviewing 2025 earnings, CAPEX, CTI data moat and 2026-2027 growth conditions

0. Bottom line first

My read is: revenue improved, but the quality transition is still being tested. The 2025 revenue jump was driven mainly by SI work and AI Deep consolidation; from 2026 onward, the key is whether proprietary solutions such as SANDY, GLX and MNX regain mix.

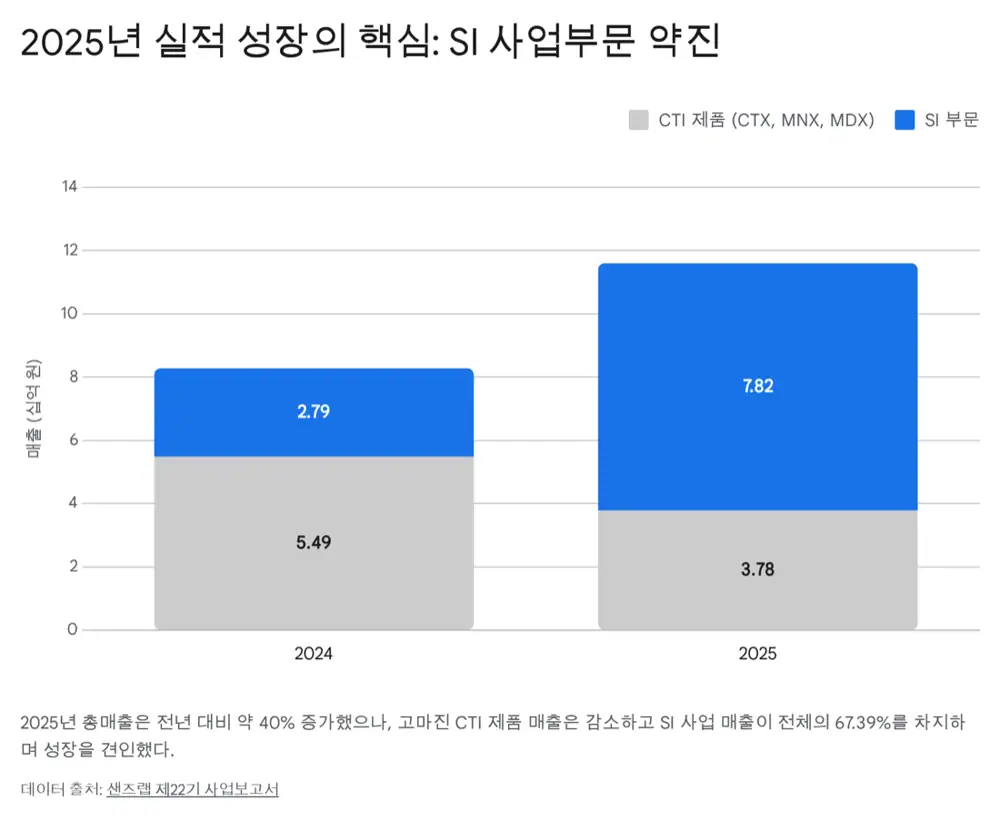

Official fact: 2025 consolidated revenue was KRW 11.61 billion, up about 40% from KRW 8.29 billion. SI revenue rose from KRW 2.79 billion to KRW 7.82 billion, while CTI products fell from KRW 5.50 billion to KRW 3.79 billion.

Interpretation: The top-line growth is real, but it was led by public-sector SI and M&A rather than high-margin CTI licenses, so the quality of controlling-shareholder earnings matters.

1. Real driver of 2025 earnings

| Item | 2024 | 2025 | Change | Mix change |

|---|---|---|---|---|

| Total revenue | KRW 8,297mn | KRW 11,612mn | +39.9% | 100% → 100% |

| CTI products | KRW 5,498mn | KRW 3,787mn | -31.1% | 66.2% → 32.6% |

| SI | KRW 2,799mn | KRW 7,825mn | +179.5% | 33.8% → 67.4% |

| Operating profit | -KRW 3,709mn | -KRW 1,770mn | Loss narrowed | - |

The cited drivers include a KRW 2.38 billion public-sector software supply contract with Korea Information Certificate Authority and a KRW 2.05 billion KISA cyber-security AI dataset modernization project. Sands Lab also acquired an 80.91% stake in AI Deep for KRW 1.84 billion on March 7, 2025; after consolidation, AI Deep contributed KRW 1.51 billion in revenue and KRW 440 million in net income over roughly nine months.

2. Controlling-shareholder earnings

| Item | 2024 | 2025 | Meaning |

|---|---|---|---|

| Consolidated net income | -KRW 2,300mn | -KRW 465mn | Headline loss narrowed |

| Net income to non-controlling interests | 0 | KRW 84mn | AI Deep minority stake, 19.09% |

| Net income to controlling shareholders | -KRW 2,300mn | -KRW 549mn | Actual parent-shareholder result |

Official fact: 2025 operating loss narrowed to KRW 1.77 billion from KRW 3.71 billion, and financial income of KRW 1.79 billion helped pre-tax loss improve to about KRW 37 million.

Interpretation: Public SI absorbed fixed costs, but a services-heavy structure is not enough for a true turnaround. The key is whether proprietary software such as SANDY, CTX and MDX rises in the mix.

3. CAPEX and technology roadmap

Investment cash flow was -KRW 4.14 billion in 2025. The source links KRW 380 million of tangible assets, KRW 630 million of intangibles and KRW 2.02 billion of R&D spending to SANDY, CPU-based GLX and MNX.

4. Moat and risks

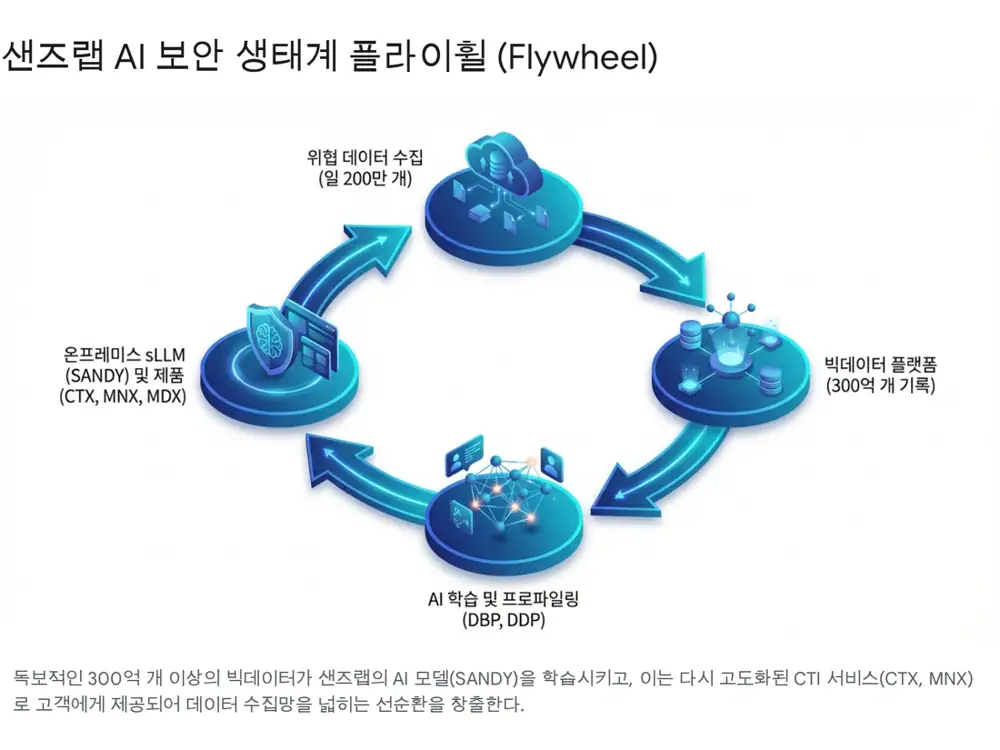

30bn threat data points

The source highlights more than 2bn malware samples analyzed since 2004 and more than 30bn threat-analysis data points.

DBP, DDP and MDX

NET-certified profiling and non-execution malware analysis are positioned as differentiators for APT and file-less attacks.

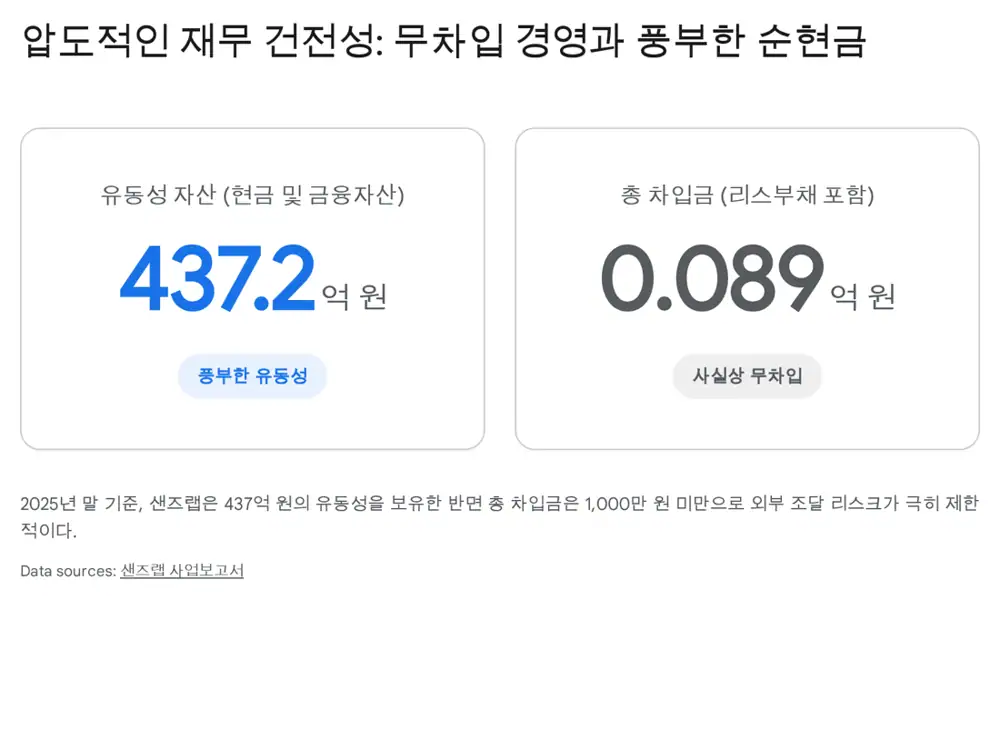

KRW 43.7bn liquidity

KRW 34.0bn of cash plus KRW 9.7bn of financial assets, with near-zero interest-bearing debt, provides runway.

5. Valuation and follow-up points

The source says the March 2026 share price was in the KRW 6,000-7,000 range, more than 70% below the KRW 27,300 post-IPO high. Around KRW 100 billion market cap, subtracting KRW 43.7 billion of net cash implies roughly KRW 50 billion of operating enterprise value.

- Watch for major B2B orders for SANDY and GLX.

- Track whether MNX expands into telecom or appliance partnerships.

- If SI remains above 67% of revenue, controlling-shareholder profit turnaround can be delayed.

- Competition from large IT services firms and global security vendors is a key risk.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224215549928

- KIND 계약: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250214000306&docno=&viewerhost=&

- Daum 수주공시: https://v.daum.net/v/Vna3zYFO1O

- 샌즈랩/KISA 설명회: https://www.sandslab.io/bbs/board.php?bo_table=m06_01&wr_id=94

- 한경 수주공시: https://www.hankyung.com/article/202406288240L

- KIND 사업보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250312001252&rcpno=20250312000774&orgid=F&tran=Y&langTpCd=0

- KIND 분기보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250514000899&docno=&viewerhost=&

- 아이티비즈 SANDY: https://www.it-b.co.kr/news/articleView.html?idxno=73725

- 전자신문 CES 2026: https://www.etnews.com/20260116000044

- 데일리시큐 MNX: https://www.dailysecu.com/news/articleView.html?idxno=203868

- 디일렉 GLX: https://www.thelec.kr/news/articleView.html?idxno=40611

- 데이터넷 SANDY: https://www.datanet.co.kr/news/articleView.html?idxno=191035

- 샌즈랩 70억 R&D: https://www.sandslab.io/bbs/board.php?bo_table=m06_01&wr_id=84

- 삼성SDS 2026 보안 전망: https://www.samsungsds.com/kr/insights/cybersecurity-threats-and-response-2026.html

- 데일리시큐 정보보호 30조: https://www.dailysecu.com/news/articleView.html?idxno=149244

- Mordor 한국 보안시장: https://www.mordorintelligence.kr/industry-reports/south-korea-cybersecurity-market

- 2025/2026 사이버 위협 PDF: https://minwho.kr/data/bbsData/17718282461.pdf

- 동아일보 SANDY: https://www.donga.com/news/It/article/all/20240215/123530644/1

- 주달 2026-01-31: https://www.judal.co.kr/?view=stockAI&shareToken=0lSMHDsMoIgQW2UP

- Investing.com: https://www.investing.com/equities/sands-lab

- Investing.com NG: https://ng.investing.com/equities/sands-lab-historical-data

- 주달 2026-02-17: https://www.judal.co.kr/?view=stockAI&shareToken=LTviwSQJEIkyo8Sa