DEEP RESEARCH · HS AD

HS Ad 2025 Q4: AI Transformation, Lower Cost Ratio, and Shareholder Returns

A research-style read focused on gross-cost ratio, intangible CAPEX, and the DASH ecosystem rather than headline revenue decline

0. Bottom line first

My core read is that HS Ad’s 2025 revenue decline does not automatically mean core deterioration. Cost of revenue fell from 56.1% to 51.4% of revenue, while the AI-based DASH ecosystem and intangible CAPEX point to a changing cost structure.

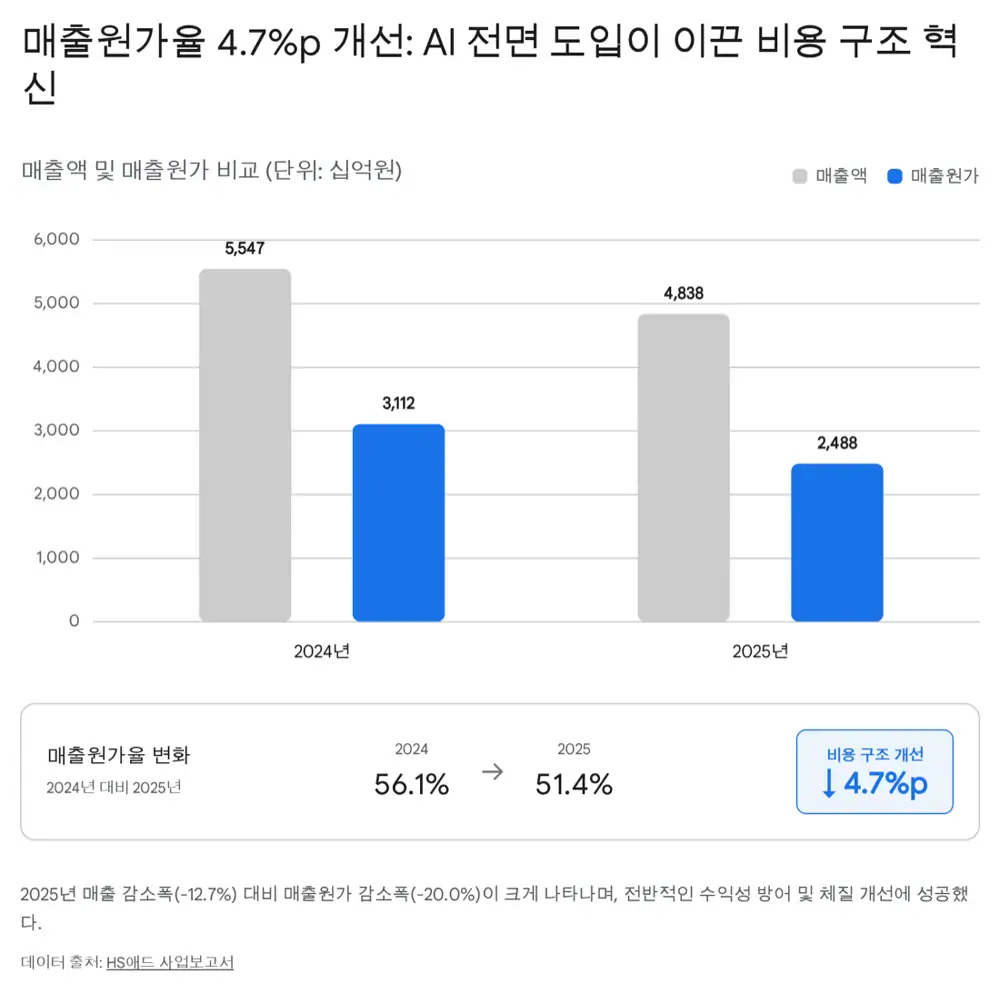

- 2025 consolidated revenue was KRW 483.85 billion, down 12.7% from KRW 554.73 billion in 2024.

- Cost of revenue fell 20.0%, from KRW 311.25 billion to KRW 248.81 billion, improving the cost-of-revenue ratio by 4.7 percentage points from 56.1% to 51.4%.

- Operating profit was KRW 27.495 billion, down only 7.0%, showing stronger profit defense than the revenue decline suggests.

- Net income attributable to owners of the parent was KRW 17.381 billion, effectively more than 100% of total net income of KRW 17.377 billion.

- 2025 software acquisition of KRW 520 million plus construction-in-progress intangible assets of KRW 3.52 billion, or about KRW 4.05 billion total, is the key evidence of DASH ecosystem investment.

1. 2025 results: revenue fell, but cost ratio fell more

Official fact: HS Ad’s 2025 consolidated revenue was KRW 483,851 million and operating profit was KRW 27,495 million. Compared with 2024 revenue of KRW 554,730 million and operating profit of KRW 29,573 million, they declined 12.7% and 7.0%, respectively.

| Financial metric | 2024 | 2025 | YoY |

|---|---|---|---|

| Revenue | KRW 554,730M | KRW 483,851M | -12.7% |

| Cost of revenue | KRW 311,251M | KRW 248,810M | -20.0% |

| Cost-of-revenue ratio | 56.1% | 51.4% | -4.7%p |

| Gross profit | KRW 243,478M | KRW 235,040M | -3.4% |

| SG&A | KRW 213,905M | KRW 207,545M | -2.9% |

| Operating profit | KRW 29,573M | KRW 27,495M | -7.0% |

| Net income | KRW 22,686M | KRW 17,377M | -23.4% |

| Net income attributable to owners | KRW 22,691M | KRW 17,381M | -23.4% |

| Net income attributable to non-controlling interest | -KRW 4M | -KRW 3M | Loss continued |

The source argues that in 2025 H2, key captive customer LG Electronics undertook restructuring and voluntary retirement, booked big-bath-type costs, and controlled B2C marketing and promotion budgets. Therefore, the revenue decline is interpreted largely as delayed budget execution at the customer level rather than core competitiveness erosion at HS Ad.

Interpretation: The key is that revenue fell 12.7%, cost of revenue fell 20.0%, and operating profit fell only 7.0%. I read this as early evidence that reduced outsourcing and AI-based production internalization are reaching the income statement.

2. Quality of earnings: nearly all income belongs to parent shareholders

Even strong consolidated net income matters less if it leaks to non-controlling interests. In HS Ad’s case, KRW 17.381 billion of 2025 net income was attributable to owners of the parent, compared with total net income of KRW 17.377 billion, effectively allocating all earnings to parent shareholders.

Official fact: Net income attributable to non-controlling interest was -KRW 3 million in 2025. The source interprets this as evidence that the 2023 merger of GⅡR with HS Ad and LBest, followed by the name change, successfully unified the governance structure.

3. CAPEX: software over physical assets

Official fact: 2025 tangible-asset acquisitions were about KRW 1.34 billion. By contrast, software acquisitions of KRW 520 million plus construction-in-progress intangible assets of KRW 3.52 billion equal about KRW 4.05 billion invested in the intangible platform ecosystem.

Construction-in-progress intangible acquisitions were only about KRW 48 million in 2024, so the 2025 spend reads as company-wide digital transformation. This investment path connects directly to HS Ad’s DASH product family.

Production automation

Commercialized in August 2024. An integrated work platform targeting 80% automation of digital-ad production with generative AI.

Performance analytics

Launched in November 2024. Quantifies TV and digital campaign purchase-conversion contribution through RSI and CXI models.

Agent orchestration

Built in H2 2025. Lets practitioners combine about 30 specialized AI agents into their own workflows.

The source views DASH.AI as the main contributor to the cost-ratio improvement, DASH I/O as justification for premium pricing, and DASH FLOW as core infrastructure for higher throughput per employee.

4. Financial strength and shareholder returns

Official fact: At the end of 2025, cash and cash equivalents were KRW 46.4 billion. Adding about KRW 4.3 billion of short- and long-term financial institution deposits gives the company substantial immediately deployable liquidity.

Total liabilities were KRW 295.9 billion and equity was KRW 212.0 billion, for a debt-to-equity ratio of 139.5%. This improved by 33 percentage points from 172.5% in the prior year. Interest-bearing debt was only KRW 730 million of short-term borrowings, leading the source to describe the company as effectively debt-free.

| Value-up metric | Before 2024 | 2025-2027 target/action | 2030 long-term target |

|---|---|---|---|

| ROE | About 11-12% | Gradual uptrend | 15% |

| Payout ratio | 30%+ | Maintain 50%+, up to 60% | Continue 60%+ |

| Special dividend | None | KRW 300 per share annually | Consider additional returns |

| Treasury-share cancellation | None | All 359,765 shares cancelled | Additional cancellation based on surplus cash |

| Gross profit scale | KRW 243.5B | Portfolio upgrade and efficiency | KRW 320.0B |

Official fact: On August 13, 2025, HS Ad announced a value-up plan to return at least 50% of consolidated net income to shareholders for 2025-2027 and ultimately reach a 60% payout ratio. It also included a KRW 300 annual special dividend per share and cancellation of all 359,765 treasury shares.

5. 2026-2027 Q, P, C framework

The source frames 2026 as a turning point for experience-centered hyper-personalization and AI-agent marketing. It states that the Korean ad market was KRW 17.3 trillion in 2025 and that digital advertising already exceeded 62% of the market.

Volume

LG Electronics budget normalization, non-captive expansion, and AI-produced references for KB Kookmin Bank, Korea Tourism Organization, and the Ministry of Health and Welfare support volume growth.

Pricing power

If DASH I/O proves budget efficiency through RSI and CXI, HS Ad can justify premium pricing beyond simple agency fees.

Cost structure

The 80% digital-production automation goal and DASH FLOW workflow reduction internalize outsourcing costs and increase fixed-cost leverage.

Interpretation: If demand recovers while the lower cost structure holds, revenue recovery can be amplified into operating-margin improvement. That is the core thesis in the source.

6. Competitive edge: 40 years of domain knowledge and captive customers

The advertising value chain consists of advertisers, media owners, and agencies. In the past, media-buying power and creative talent mattered most; after personalization and media fragmentation, integrated data analysis and mass content generation became more important, according to the source.

HS Ad’s moat is not generic AI adoption, but the combination of 40 years of brand-marketing domain knowledge with AI. On top of infrastructure such as EXAONE, the company trains specialized models on its own planning frameworks and creative data, while about 30 AI agents reflect practitioner personas.

The source body also included this link: http://googleusercontent.com/assisted_ui_content/3

HS Ad is also positioned as one of Korea’s big three advertising agencies alongside Cheil Worldwide and Innocean, and the LG Group captive customer base is viewed as a source of downside rigidity and funding capacity for AI transformation.

7. Valuation, catalysts, and risks

Official fact: The source summarizes HS Ad’s share price near KRW 8,760, PER of 11.3x based on EPS of KRW 778, and PBR of 0.77x.

Two catalysts are presented: first, numerical proof of operating leverage in H1 2026; second, actual cash inflow from the value-up plan, including a basic dividend equal to 50-60% of net income and an annual KRW 300 special dividend for three years.

- Macro hard landing: If global recession and weak consumption lead advertisers such as LG Electronics to cut budgets, absolute order volume can fall and reverse operating leverage can emerge.

- Platform technology risk: Copyright issues or hallucinations in DASH-generated output could damage brand reputation and trust.

- SaaS expansion risk: The medium-term plan to move beyond internal efficiency into an external-customer SaaS model could face security concerns or weak adoption.

8. Meaning of the source’s action plan

The source views HS Ad as at an inflection point from traditional advertising into a software- and data-based MarTech company, with the stock price depressed by market misreading of fundamentals.

| Source item | Presented view | Caution |

|---|---|---|

| Entry strategy | KRW 7,900-8,500 as an accumulation band | Author scenario, not a recommendation |

| First target | KRW 9,800 | Psychological resistance and near three-year high |

| Long-term target | KRW 11,500 | Requires external penetration of AI platform and visible 15% ROE path |

| Exit condition | Loss of captive share, two consecutive operating-loss quarters, or break below KRW 7,500 | Core issue is whether the structural-improvement story is impaired |

One-line conclusion: HS Ad’s 2025 numbers should be read through the 4.7 percentage-point cost-ratio improvement, intangible CAPEX, quality of parent-attributable earnings, and shareholder-return plan rather than revenue decline alone.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224215466787

- Samsung-LG Electronics marketing-spend gap - IT Chosun: https://it.chosun.com/news/articleViewAmp.html?idxno=2023092158469

- LG Electronics 2026 post-big-bath turnaround outlook - Global Epic: https://www.globalepic.co.kr/view.php?ud=2026011210514643695ebfd494dd_29

- HSAD commercializes generative AI for advertising - Yonhap: https://www.yna.co.kr/view/AKR20240813057100003

- HSAD launches DASH I/O - Herald Economy: https://biz.heraldcorp.com/article/3852445

- HSAD launches DASH I/O - MADTimes: https://www.madtimes.co.kr/news/articleView.html?idxno=22251

- HSAD customer-experience index - The PR: https://www.the-pr.co.kr/news/articleView.html?idxno=52381

- HSAD AI-agent platform - Yonhap: https://www.yna.co.kr/view/AKR20250618034500003

- HSAD DASH FLOW - Daum: https://v.daum.net/v/G25FogDxjz

- HSAD DASH FLOW and DASH 2.0 strategy - AD.co.kr: https://op.ad.co.kr/journal/column/show.do?ukey=585141

- HSAD raises payout ratio up to 60% - Yonhap: https://www.yna.co.kr/view/AKR20250813147800003

- HS Ad 2025 value-up plan - Stockplus: https://spn.stockplus.com/news/api/v1/disclosure_views/koscom/373290

- 2026 AI marketing trends - OpenAds: https://openads.co.kr/content/contentDetail?contsId=17922

- 2026 digital advertising experience - MADTimes: https://www.madtimes.co.kr/news/articleView.html?idxno=25869

- 2026 digital marketing keywords - MADTimes: https://www.madtimes.co.kr/news/articleView.html?idxno=26263

- Korean broadcasting advertising market outlook: https://journal.kbjc.net/news/articleView.html?idxno=20751

- 2025 ad-market review and 2026 outlook - AD.co.kr: https://m.ad.co.kr/mobile/magazine/592246

- 2025 advertising trends - Banronbodo: https://www.banronbodo.com/news/articleView.html?idxno=23516

- Google 2026 AI agent trends: https://contents.premium.naver.com/aidx/aix/contents/251221163912594ch

- HS Ad to make 80% of digital ads with AI - Chosun Biz: https://biz.chosun.com/industry/business-venture/2024/08/13/UG3KQOVNO5EI3JS6WU4I7RMU7Y/

- HSAD DASH I/O launched - MK: https://www.mk.co.kr/en/business/11166115

- HSAD brand-customized agents - Maily: https://maily.so/itis/posts/g1o4g8xlove

- 2026 AI sales forecasts - Next Unicorn: https://www.nextunicorn.kr/insight/bae934bdbf1c2635

- Listed advertising companies brand reputation - Energy News: https://www.energy-news.co.kr/news/articleView.html?idxno=222985

- HS Ad investment analysis 2025.11.28 - Judal: https://www.judal.co.kr/?view=stockAI&shareToken=Ue6ElZ7CowU8Jc3V

- HS Ad investment analysis 2025.12.31 - Judal: https://www.judal.co.kr/?view=stockAI&shareToken=xe6GwCW3j0wR2t5c

- HS Ad investment analysis 2026.01.08 - Judal: https://www.judal.co.kr/?view=stockAI&shareToken=UeIVOWRaMe7dhkxq

- In-body source link - Google assisted UI content: http://googleusercontent.com/assisted_ui_content/3