DEEP RESEARCH · DSR STEEL

DSR Steel (069730): Deep-Value Turnaround and the Meaning of an 11% Dividend

A research note on 2025 earnings recovery, third-generation succession, and the shipbuilding/infrastructure cycle

0. Bottom line first

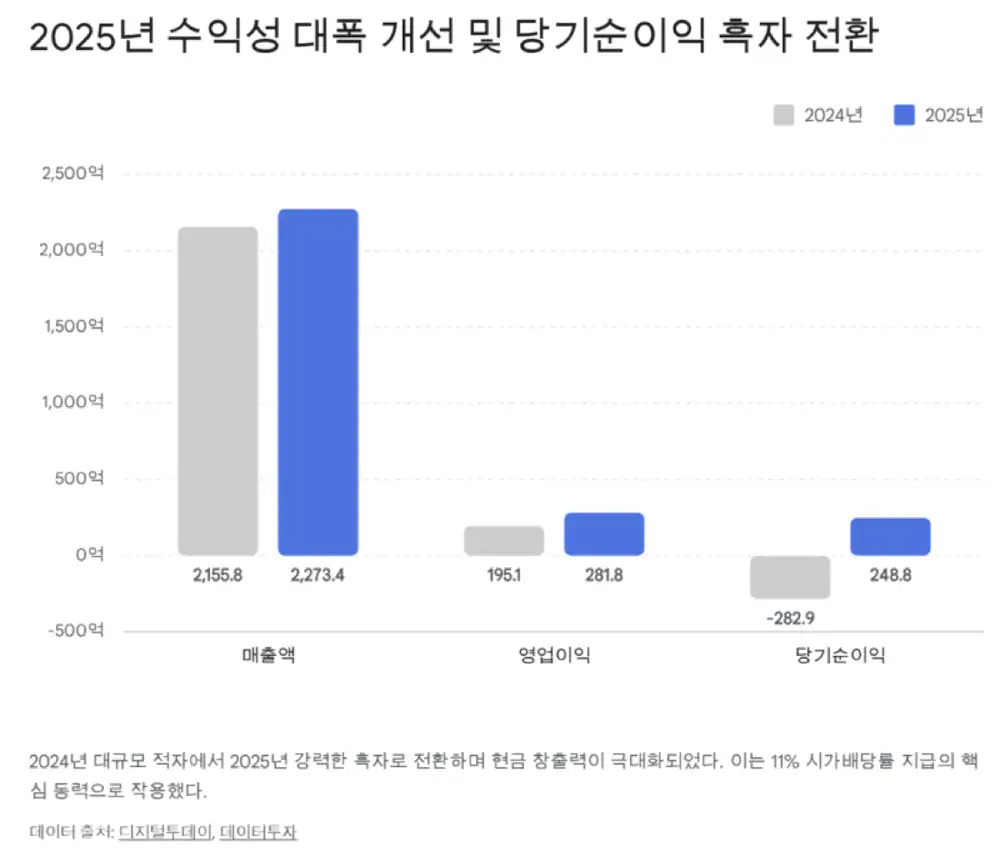

My core read is that this is not just a fourth-quarter dividend event. DSR Steel moved from a large net loss in 2024 to net profit in 2025, while announcing KRW 430 per share, about KRW 6.192 billion in total dividends, and an 11% indicated dividend yield at the disclosure point. That combination points to a setup where deep value, a turnaround, and owner-family alignment are operating at the same time.

| Key item | Source number/content | My read |

|---|---|---|

| 2025 revenue | KRW 227.34847 billion, up 5.4% YoY | Top-line growth is modest, but earnings leverage expanded. |

| 2025 operating profit | KRW 28.18405 billion, up 44.4% YoY | Cost control and industry recovery appear together. |

| 2025 net income | KRW 24.88368 billion profit, versus a KRW 28.29872 billion loss in 2024 | The roughly KRW 53 billion earnings swing is the valuation starting point. |

| Dividend | KRW 430 per share, about KRW 6.192 billion total, 11% yield | This is a different capital-allocation signal from the old KRW 25-100 dividend range. |

1. Business model and product portfolio

Official fact: The source describes DSR Steel as a primary special steel wire manufacturer founded on September 1, 1971. It purchases wire rod and processes it through drawing, stranding, plating, and heat treatment to supply higher-value special wire products. The disclosure reference is linked here: KRX annual report.

Interpretation: This is not a simple steel trading business. Its economics depend on industrial material processing where safety and durability matter. Profitability is driven by raw-material pass-through and volume from shipbuilding, construction, and grid cycles.

Wire rope

Used in ship mooring, port handling, offshore plants, and construction tower cranes.

Hard drawn steel wire

Used in auto parts, precision springs, and submarine cable armoring.

ACSR

A high-voltage cable product tied to aging grid replacement and new transmission towers.

PC steel wire

Used as a structural backbone in large bridges and concrete structures.

2. Cash flow and the 2025 dividend

Official fact: 2025 consolidated revenue was KRW 227.34847 billion, operating profit was KRW 28.18405 billion, and net income was KRW 24.88368 billion. The source highlights the reversal from a KRW 28.29872 billion net loss in 2024. Media references include Digital Today and Data Tooza.

Interpretation: The important 2025 change is not the 5.4% revenue growth by itself, but the 44.4% operating-profit growth and the swing to net profit. The source attributes the margin improvement to reduced non-operating losses and the base effect from items such as roughly KRW 3.7824 billion in employee welfare fund contributions booked around 3Q 2024.

The dividend disclosure is the center of the note. The 2025 year-end dividend was KRW 430 per common share, about KRW 6.192 billion in total, and an 11% yield at the disclosure point. Compared with the source's history of KRW 25-100 per share dividends from 2006 to 2023, or roughly 0-2.7% yields, this looks more like a change in capital allocation than a routine cash payout. See Herald dividend article and Investing.com dividend history.

3. Customers, moat, and macro tailwinds

Official fact: The source presents HD Hyundai Heavy Industries, Hanwha Ocean, and Samsung Heavy Industries as key wire-rope demand sources. It says the big three shipbuilders have three to four years of dock backlog and mentions Hanwha Ocean's 45% revenue growth and operating-profit turnaround in fiscal 2024. Reference: shipbuilder financial comparison.

Interpretation: DSR Steel's demand is tied to shipbuilding, offshore plants, ports, construction, and grid investment. LNG carriers, ammonia carriers, aging infrastructure replacement, and grid buildout from AI data centers and EV adoption are the three-year demand pillars in the source thesis.

Certifications and process know-how

The source cites ISO 9001:2015, IATF 16949:2016, KS, JIS, RINA, RS, ABS, and KRQA as entry barriers.

Customer lock-in

Because the materials are safety-critical, proven suppliers are hard to replace; set-based supply further raises convenience.

Vietnam production base

DSR Vina is interpreted as a production-diversification tool that can partly manage tariff, quota, and anti-dumping risk.

4. Valuation and peer comparison

The source says DSR Steel traded in the KRW 3,600-4,000 range, with PBR of 0.29-0.3x, PER of 2.29-2.32x, and EPS of KRW 1,606. It also cites Judal AI investment analyses with a one-year target range of KRW 4,500-5,000 and a three-year target range of KRW 6,000-6,500. The linked materials are Judal 2026-02-17, Judal 2026-01-16, Judal 2026-01-08, Judal 2026-02-09, and Judal 2025-12-23.

| Company/group | Source basis | Investment angle |

|---|---|---|

| DSR Steel | PBR 0.29-0.3x, PER 2.29-2.32x, 11% dividend yield | An alpha-oriented deep-value and high-income candidate |

| Kiswire | 4Q25 operating profit of KRW 41.2 billion, up 57.8% YoY, annual revenue of KRW 1.8093 trillion | A larger core holding if scale and capacity matter most |

| Six steel-wire peers | Kiswire, Daeho P&C, Manho Rope & Wire, DSR Steel, Youngheung, Chungwoo | Market share and cost efficiency are key in an oligopolistic structure |

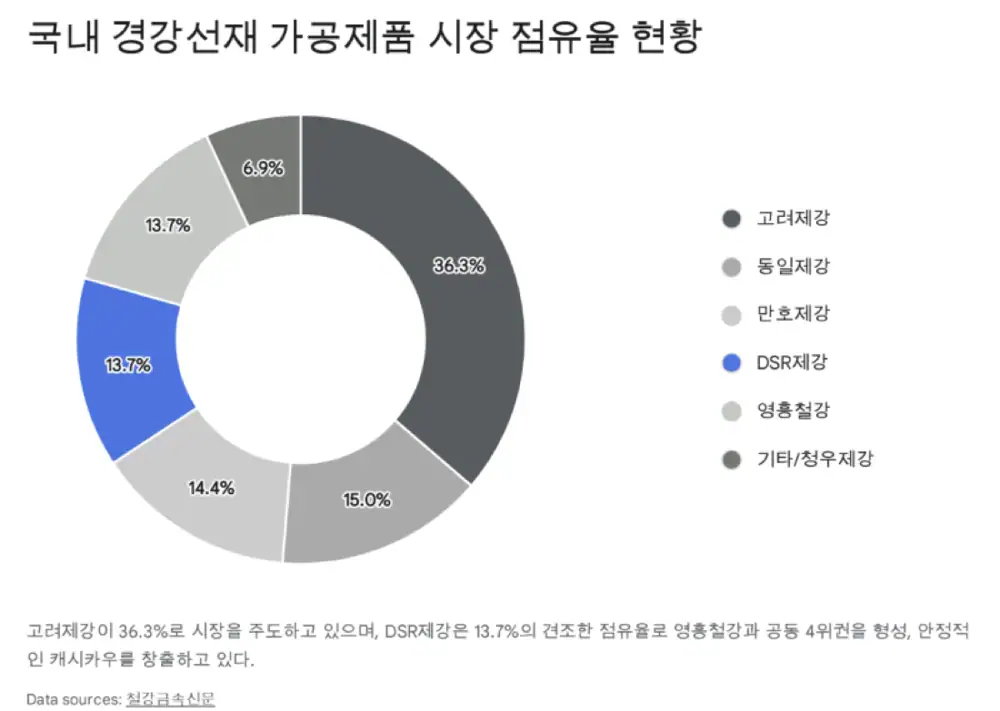

For October 2025 processed steel-wire sales share, the source lists Kiswire at 36.3%, Daeho P&C at 15.0%, Manho at 14.4%, and DSR Steel and Youngheung at 13.7% each. It adds that DSR Steel was ahead of Youngheung by about five tons in absolute volume. Source: Steel & Metal News share article.

5. Governance and the dividend link

Official fact: The source says DSR Steel is legally run by co-CEOs Hong Ha-jong and Hong Seok-bin, while Hong Yoo-kyung, born September 22, 1994, granddaughter of founder Hong Soon-mo and daughter of Hong Ha-jong, joined the company in September 2021, was formally appointed on October 1, and serves as head of management support.

The ownership details are specific. The source says Hong Ha-jong gifted 151,000 shares each to relatives Hong Seung-hyun, Hong Jin-woo, and Hong Yoo-kyung, totaling 453,000 shares or 3.14%. It also says Hong Yoo-kyung moved from 2.29% ownership, or 329,489 shares, as of August 26, 2025, after purchases including 5,923 shares on November 6, 10,000 shares at KRW 3,604 on November 7, 3,000 shares at KRW 3,536 on November 10, and 22 shares at KRW 3,560 on November 13. By the November 24, 2025 disclosure, she held 353,050 shares, or 2.45%. Links: Data Tooza ownership article, Digital Today purchase article, EBN gift article, and FerroTimes purchase article.

Interpretation: The most interesting point to me is the possible alignment between third-generation succession and high dividends. The source reads the 11% dividend as potentially connected to succession funding, additional share purchases, and gift-tax resources, not merely minority-shareholder appeasement. If that read is right, the dividend has a structural owner incentive behind it.

6. Financing, shareholder base, and overhang

Official fact: The source says no major external financial-investor funding, post-listing equity issuance, mezzanine issuance, outstanding CB/EB/RCPS, or unexercised stock options were found in public data over the recent five-year review.

Interpretation: This matters for a deep-value small cap. If there is no convertible or warrant overhang waiting to hit the market before the turnaround is reflected in the share price, the earnings recovery belongs more directly to existing shareholders. Still, “not found in public data” is a scope statement, so updated disclosures must be checked before any real investment decision.

7. Risks and final scenario

Re-rating

Profit recovery, an 11% dividend, low PBR/PER, and shipbuilding/infrastructure demand all get recognized.

Dividend value stock

Even if the share price moves slowly, dividend income and valuation support maintain the thesis.

Tariffs and demand slowdown

Trump 2.0 steel/aluminum tariffs, low-cost Chinese steel, and slower hard-drawn wire exports to the U.S. remain risks.

The source treats Trump's proposed 25% additional tariff on all steel and aluminum imports, under Section 232 logic, as the largest macro risk. It says the risk affected U.S.-bound hard-drawn wire exports in late 2025, while Vietnam production, domestic shipbuilding volume, and European/emerging-market infrastructure exports may offer offsets. Tariff reference: Korea Economic TV news.

The source's final thesis is aggressive: a roughly KRW 53 billion earnings swing from a KRW 28.2 billion loss in 2024 to KRW 24.8 billion profit in 2025, no visible mezzanine or fund overhang, and owner alignment shown by Hong Yoo-kyung's 2.45% stake and the KRW 430 dividend. In this report, I treat that not as a recommendation but as a research hypothesis that must be checked against continuing disclosures and numbers.

Sources

- KRX 사업보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250226001246&docno=&viewerhost=&

- 디지털투데이: 당기순이익 흑자전환: https://www.digitaltoday.co.kr/news/articleView.html?idxno=628212

- 데이터투자: 연간 영업이익: https://www.datatooza.com/article/20260206172201397652ef31c35f_80

- 이야드: 2025년 3분기 수익성: https://www.eyard.net/news/view?id=561832

- 철강금속신문: 2025년 3분기 수익성: http://www.snmnews.com/news/articleView.html?idxno=561832

- KRX 분기보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250515001008&docno=&viewerhost=&

- 헤럴드경제: 주당 430원 배당: https://biz.heraldcorp.com/article/10686929

- Investing.com: DSR제강 배당 기록: https://kr.investing.com/equities/dsr-wire-dividends

- 네이버 프리미엄콘텐츠: 조선 3사 비교: https://contents.premium.naver.com/busymoon/kicpakpmg/contents/250531102529034bs

- 주달: DSR제강 투자분석 2026-02-17: https://www.judal.co.kr/?view=stockAI&shareToken=ROSLQiaPmEfJudGi

- 한국경제TV YouTube: 철강 관세: https://www.youtube.com/watch?v=8wgFVy91gBE

- 주달: DSR제강 투자분석 2026-01-16: https://www.judal.co.kr/?view=stockAI&shareToken=nJ6T7KMaSHQaXSlS

- 주달: DSR제강 투자분석 2026-01-08: https://www.judal.co.kr/?view=stockAI&shareToken=ttN7whAqxR2fpYsk

- 주달: DSR제강 투자분석 2026-02-09: https://www.judal.co.kr/?view=stockAI&shareToken=31h7w0NdXmlSloss

- 주달: DSR제강 투자분석 2025-12-23: https://www.judal.co.kr/?view=stockAI&shareToken=iaIaFJZYsA9I41YB

- 스틸프라이스: 고려제강 영업이익: http://www.steelprice.co.kr/news/articleView.html?idxno=60979

- 데이터투자: 홍유경 본부장 지분율: https://www.datatooza.com/article/20251124171148138952ef33d7b3_80

- 디지털투데이: 홍유경 본부장 장내매수: https://www.digitaltoday.co.kr/news/articleView.html?idxno=604613

- EBN: 홍하종 대표 지분 증여: https://www.ebn.co.kr/news/articleView.html?idxno=652488

- 뉴스엔: 홍유경 관련 기사: https://m.newsen.com/news_view.php?uid=201202091042411001

- 페로타임즈: 홍유경 보통주 장내매수: https://www.ferrotimes.com/news/articleView.html?idxno=38540

- 철강금속신문: 고려제강 판매점유율: http://www.snmnews.com/news/articleView.html?idxno=299322

- Original blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224204123869

- KRX annual report original href: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250226001246&docno&viewerhost&

- KRX quarterly report original href: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250515001008&docno&viewerhost&