DEEP RESEARCH · NBR Motion

NBR Motion: From Rolling-Element Localization to Robot and EV Precision Materials

A valuation report on SPAC overhang, G5 precision machining, ceramic balls, CRB, and accounting noise

0. Bottom line first

My read is that NBR Motion is not merely a loss-making auto-parts company. It is a precision materials company that localized rolling elements for EV motors and robot reducers. Still, FI overhang and SPAC-merger costs can pressure the stock near term, so the source argues for holding in the short run and accumulating on weakness around KRW 13,400-15,000.

1. Governance and overhang: defenses versus selling pressure

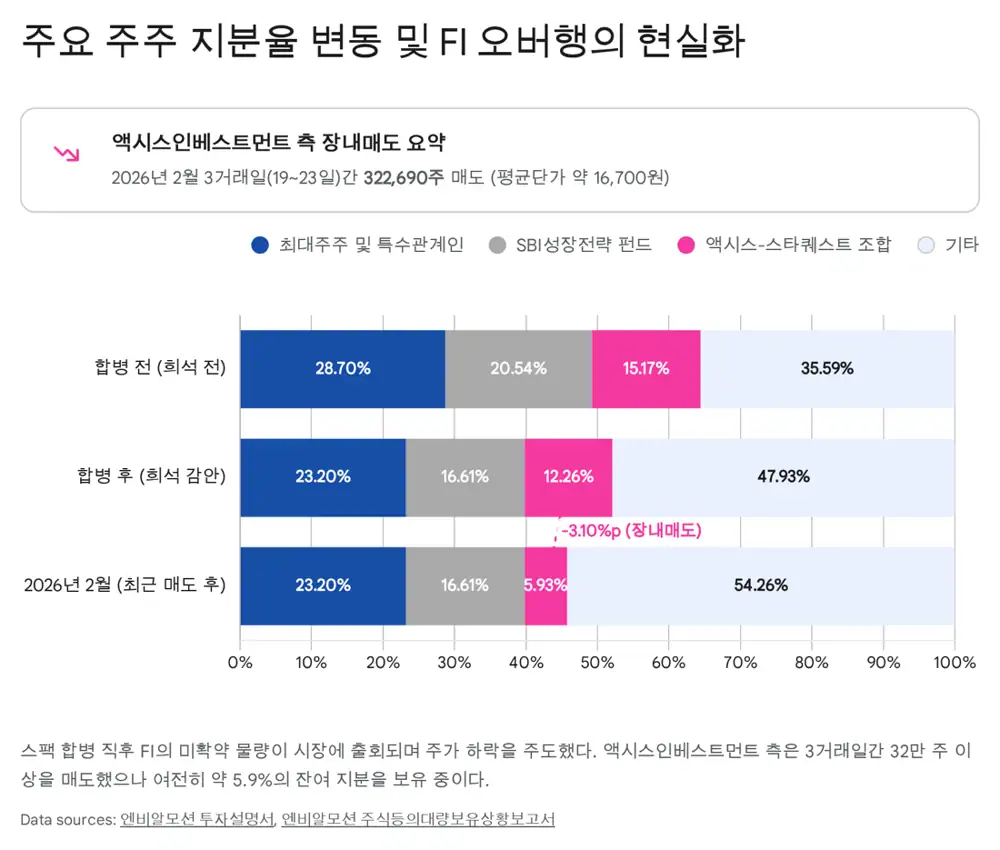

Official fact: NBR Motion listed on KOSDAQ in January 2026 through a SPAC merger with Mirae Asset Vision SPAC No. 3. The largest shareholder is NANO, an environmental and energy company. NANO held 23.95% before listing, but after applying the 1:0.2348245 merger ratio and potential dilution such as stock options, the effective post-listing ownership falls to about 19.36%.

Official fact: Including CEO Moon Doo-sung at 3.76% and President Oh Byung-kwon at 0.09%, the largest-shareholder side owns 23.20% on a diluted basis. The source calls this somewhat weak versus the 30% level often viewed as a management-control line.

The defenses are stronger than the raw ownership suggests. NANO and CEO Moon voluntarily extended the statutory one-year lockup by four years, for a total five-year lockup. Joint-purpose holding commitments cover 5,103,658 shares, or 44.60% on a diluted basis. A right of first refusal granted to CEO Moon or his designee covers 40.84% of shares.

Official fact: Major FIs include SBI Growth Strategy M&A Fund with 16.61% after the merger and StarQuest-Axis-Pacific Capital New Technology Investment Association No. 1 with 12.26%. Some FIs submitted staggered 1-month, 3-month, and 6-month selling commitments, but a meaningful portion remained freely tradable.

Official fact: According to the February 25, 2026 large-shareholding filing, the Axis Investment side sold 322,690 shares over three trading days from February 19 to 23, 2026: 200,000 shares at KRW 16,870 on February 19, 75,827 shares at KRW 16,626 on February 20, and 46,863 shares at KRW 16,839 on February 23. Its stake fell from 9.03% to 5.93%, down 3.10 percentage points.

Interpretation: This FI selling directly explains much of the decline from the post-listing 52-week high of KRW 27,200 to below KRW 17,000, down about 37%. The remaining 5.93%, or about 617,000 shares, can become resistance whenever the stock rebounds.

Potential dilution check

- The company previously issued KRW 6.5 billion of BW with KRW 5,000 exercise price, equal to about 1.3 million shares, and KRW 2.0 billion of CB with KRW 5,750 conversion price, equal to about 347,000 shares.

- As of Q3 2025, about KRW 6.5 billion of bonds had converted into common shares, while the remaining KRW 3.0 billion IBK-Stonebridge BW and KRW 3.0 billion Aju IB CB were reclassified as ordinary bonds after conversion rights were extinguished by agreement.

- Stock options granted from late 2024 to early 2025 total 350,000 shares at KRW 3,000, including 150,000 shares for CEO Moon and 70,000 for President Oh. The source describes them as deeply in the money, worth more than 5x the exercise price versus a roughly KRW 17,000 share price. The exercise period runs from November 1, 2026 to the end of October 2029.

- The 350,000 options equal about 3.3% of roughly 10.4 million shares outstanding and remain a future EPS dilution factor.

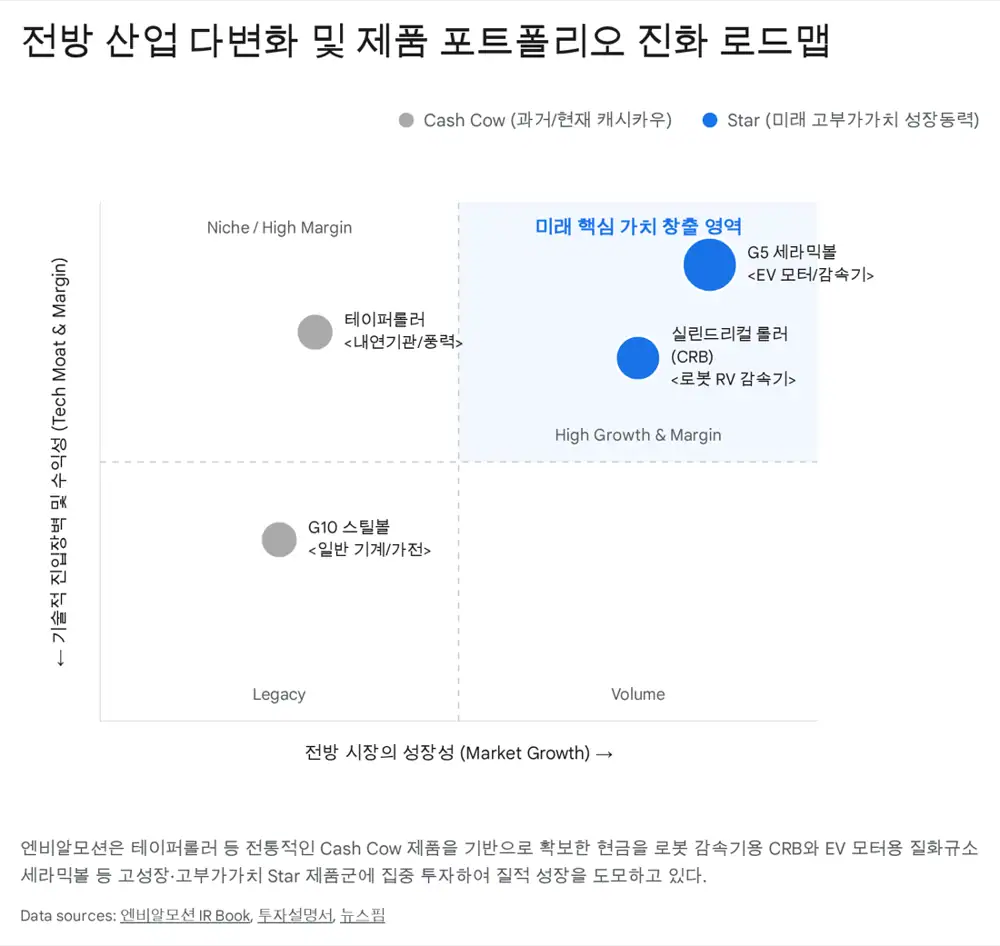

2. Products and moat: from G5 precision machining to ceramics

Official fact: NBR Motion's revenue portfolio is presented as taper rollers 58%, high-carbon chrome steel balls 27%, and bearing raceways 15%. The source frames the company as a technology-intensive business that machines rolling elements, which determine bearing friction, load support, noise, and fatigue life, at nanometer-level precision.

Official fact: The global rolling-element market is concentrated, with Japanese players such as AKS and Tsubaki Nakashima holding more than 70-80%. Under ISO 3290-1, lower grades indicate higher precision. NBR Motion moved beyond G10-G20 and obtained development and global mass-production approvals for G5 Standard and SP-grade products.

Cold-forged metal flow

Optimizes internal grain flow to reduce asymmetry and improve durability.

Profile crowning

Micrometer-level roller geometry reduces edge stress, rolling resistance, and noise.

Carburizing/nitriding heat treatment

The source says it extends fatigue life from the industry-standard five years to as much as ten years.

The source says NBR Motion verified bearing assembly quality equal to or better than AKS, a subsidiary of NSK, and offers comparable G5 quality to Tsubaki Nakashima with a 5-10% price advantage. Excluding captive production by finished-bearing makers, it is described as global No. 3 in taper rollers and the only domestic producer.

Si3N4 ceramic balls for EVs

Official fact: EV motors require high-speed rotation above 15,000-20,000 RPM, and heat plus stray current can cause electrical pitting in bearings. Silicon nitride ceramic balls are about 40% lighter than steel balls and offer heat resistance, wear resistance, and electrical insulation.

Official fact: The source forecasts the automotive silicon-nitride-ball market to account for more than 54% of the total market by 2035 and grow at more than 6.3% CAGR. NBR Motion began a Ministry of Trade, Industry and Energy localization project for EV ceramic bearing balls in 2021 and achieved Korea's first G5-grade ceramic-ball processing certification and pilot production in 2024.

The source says NBR Motion signed an MOU with Cheomdan Lab to recycle waste ceramic substrates from semiconductor processes into ceramic-ball raw material, targeting more than 30% cost advantage versus Japanese competitors. It is currently running module-level durability tests with global customers such as H company, K company, Japanese N company, and German S company, with 2026-2027 SOP as the key catalyst.

CRB for robot reducers

Humanoid and industrial robot RV reducers need cylindrical roller bearings because they must support high load while preserving precise motion. The source says NBR Motion is localizing CRB by modifying taper-roller infrastructure, developing its own double-side grinder, and using high-speed cold-heading. It has secured initial development orders from Japanese RV-reducer and German bearing-module OEMs, targets 100% localization by 2026, and plans two dedicated mass-production lines in 2027.

3. Customer lock-in, backlog, and pass-through pricing

Official fact: NBR Motion is a registered supplier to Schaeffler, NSK, and SKF, the global top-three bearing makers. These three customers accounted for 88% of revenue in 2023, 89% in 2024, and 85% in H1 2025.

Interpretation: Customer concentration is a risk, but automotive drivetrain parts require RFQ, drawing design, prototypes, long durability tests, and PPAP over one to two years. After SOP, suppliers often remain locked in for five to eight years until model discontinuation.

- The North American GM Austin electric pickup and EV reducer G5 steel-ball project is cited as about KRW 2.1 billion of long-term potential revenue from 2026 to 2031.

- Schaeffler Slovakia approved G10 steel-ball mass production, and shipments began in December 2024.

- Schaeffler Hungary's BMW and AUDI reducer steel-ball volume is secured at KRW 5.2 billion over eight years, with export contribution expected from mid-2026.

- Steel balls for Hyundai/Kia wheel bearings through Iljin Bearing Group are expected to start in H2 2025 at about KRW 9.6 billion annually.

Official fact: As of Q2 2025, secured order value for major products was KRW 120.3 billion and remaining backlog was KRW 95.8 billion. The source says many contracts run as far as 2030, supporting downside resilience for the next two to three years.

| Item | Use/application | Production/delivery | Total order | Q2 2025 backlog |

|---|---|---|---|---|

| High-precision steel balls | 35 G5/G10 types, including Europe/North America exports | Through Dec. 2025, monthly delivery | KRW 16.8bn | KRW 11.2bn |

| EV steel balls | EV reducers for BMW and others, Schaeffler Hungary | Aug. 2025-2030 | KRW 4.1bn | KRW 4.0bn |

| Wheel-hub steel balls | Seven types for Hyundai/Kia via Iljin Bearing Group | Aug. 2025-2028 | KRW 22.8bn | KRW 22.8bn |

| Taper rollers | 25 ICE/HEV types and high-precision low-noise EV products | After July 2026 | About KRW 21.5bn | About KRW 19.0bn |

| Raceways etc. | European commercial-truck wheel hubs and HVAC valves | Through Dec. 2025 | KRW 16.0bn | KRW 12.1bn |

Official fact: The source says bearing-steel purchase prices are negotiated quarterly with steelmakers and wire-rod suppliers such as POSCO based on global steel prices, and 100% of raw-material cost changes are passed through to customers such as Schaeffler and NSK on a quarterly or semiannual basis.

4. Q/P/C and operating risks

The end market is diversifying from internal-combustion applications into EVs, wind power, defense, aerospace, and industrial robots. The source cites a forecast that global EV sales will grow more than 25% YoY in 2025 and argues that heavier EV battery loads can increase taper-roller demand.

Volume growth

EVs, robot-reducer CRB, and China-exclusion supply-chain shifts create new demand.

ASP uplift

G5 precision parts and Si3N4 ceramic balls raise product mix quality.

85% utilization

Pricing assumes 85% target utilization, so exceeding it amplifies fixed-cost leverage.

Official fact: The source says the company earned profits in 2022 and 2023 when revenue was around KRW 65 billion and KRW 68 billion and utilization stayed in the high-80% range. In 2024 and 2025, revenue stayed in the KRW 63 billion range and operating losses were about KRW 3.9 billion.

Interpretation: If the KRW 95.8 billion backlog and new GM Austin and Schaeffler Hungary projects lift Changwon/Miryang utilization above 85%, the same fixed-cost structure can become operating leverage.

Critical risks

- Precision metal parts can corrode during long-distance ocean transport because of temperature/humidity changes and moisture absorption by packaging. A 2024 Hungary taper-roller export issue created about KRW 1.32 billion of return, disposal, and rework costs.

- Raceway products for European commercial trucks represent about 15% of revenue but are not produced directly. They are 100% outsourced to Damon Industry, an affiliate in which NBR Motion owns 29.6%. Labor disruptions, fire, or financial stress there could create supply-chain concentration risk.

5. Valuation and investment conclusion

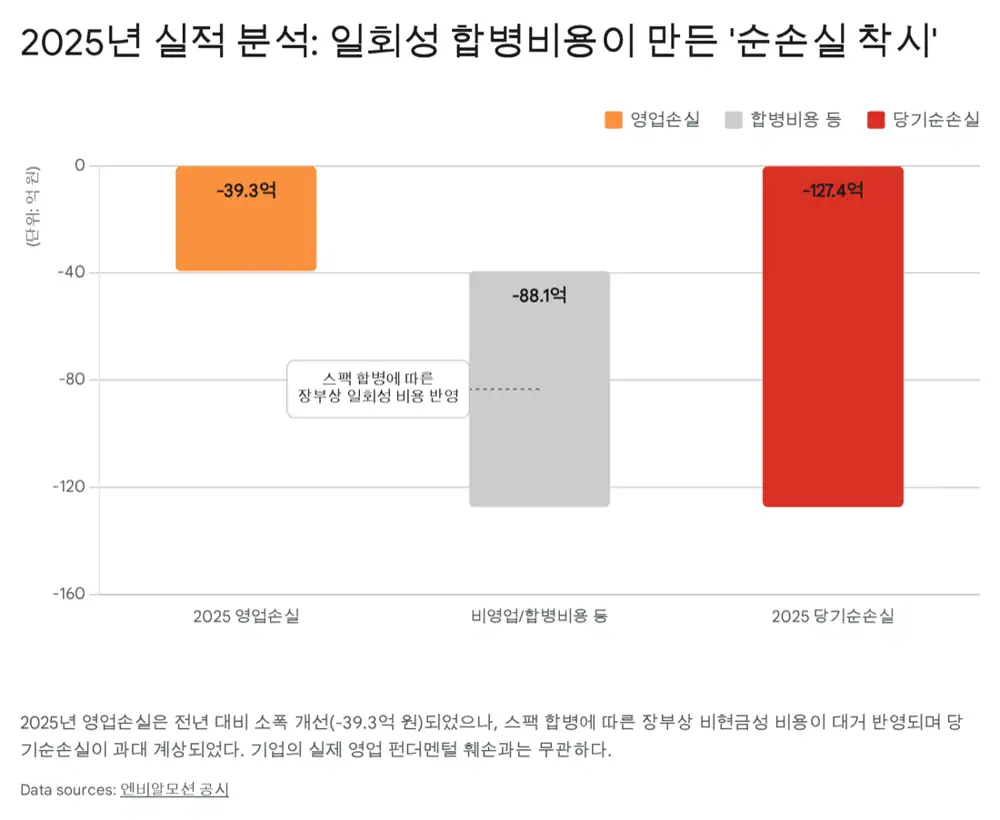

Official fact: Preliminary 2025 results released on February 27, 2026 showed revenue of KRW 63.1 billion, down 1.2% YoY. Operating loss was about KRW 3.93 billion, narrowing 4.3% from KRW 4.10 billion. Net loss, however, jumped 68% YoY to KRW 12.74 billion.

Official fact: The source attributes the net-loss spike to SPAC merger cost and listing-related one-off expenses under K-IFRS 1102 share-based payment accounting. About KRW 8.8 billion of listing-premium-like share-based payment expense hit the income statement, but it was non-cash and did not send one won of cash out of the company.

Interpretation: The market combined the KRW 12.7 billion net-loss headline with FI selling and created panic selling. The stock fell from KRW 27,200 to KRW 17,040, down about 37%. I read this as a price error from accounting and supply-demand events, not operating deterioration.

Official fact: The SPAC merger brought in about KRW 9.5-10.0 billion of cash, increasing equity from KRW 18.7 billion to KRW 33.8 billion and reducing liabilities from KRW 59.4 billion to KRW 51.9 billion. About KRW 6.75 billion is planned for HPR taper-roller grinding-line overhaul and automatic inspection equipment, with remaining funds for CRB and semiconductor/EV ceramic bearing R&D.

The source notes that Japan's Tsubaki Nakashima trades with negative P/E due to losses and P/S of 0.2x. But treating NBR Motion as the same generic steel-ball maker would miss its robot-reducer and advanced-mobility materials re-rating potential.

Robot CRB SOP

Completion in 2026 and mass supply to Japanese and German RV-reducer leaders is the first trigger.

Ceramic-ball mass production

The scenario is entering a Japan-dominated market at 30% lower cost after tests with H, K, and German S customers.

Utilization above 85%

Backlog of KRW 95.8 billion plus GM Austin and Schaeffler Hungary projects can trigger operating leverage.

The source's conclusion as of March 2026 is “Hold” in the short run, then “Accumulate on Weakness.” The hold case rests on 320,000 FI shares sold in three trading days, the remaining 5.9% stake, and the KRW 12.7 billion one-off accounting loss shock. The suggested buying window is KRW 13,400-15,000, when downside support appears and FI selling fades.

The three core points are: the 2025 net loss is distorted by non-cash SPAC merger accounting; G5 precision machining and 10% price competitiveness create global customer lock-in; and ceramic balls plus robot CRB in H2 2026 could change the multiple from traditional parts to advanced EV and humanoid-robot components.

Sources

- 원문 / Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224201915876

- 엔비알모션, 로봇 감속기 핵심 부품 해외 수주 - 뉴스핌: https://www.newspim.com/news/view/20251104000320

- 엔비알모션 투자분석 2026.02.23 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=dleKKr47oCjEXOIc

- 실리콘 질화물 볼 시장 전망 - Research Nester: https://www.researchnester.com/kr/reports/silicon-nitride-balls-market/7108

- 하이브리드 세라믹 베어링 시장 - Business Research Insights: https://www.businessresearchinsights.com/ko/market-reports/hybrid-ceramic-bearings-market-104778

- 엔비지·첨단랩 질화규소 세라믹 볼 국산화 - 한국베어링산업협회: https://koreabearing.or.kr/35/?bmode=view&idx=144279071

- 엔비알모션 로봇 감속기 핵심 부품 수주 - 와이드경제: https://www.widedaily.com/news/articleView.html?idxno=281912

- 2026.01.28 Signal Report - 네이버 프리미엄콘텐츠: https://contents.premium.naver.com/nomadand/nomad/contents/260128054313022bj

- NBR Motion Registration Statement - English DART: https://englishdart.fss.or.kr/dsbh001/main.do?rcpNo=20251014000385

- 엔비알모션 투자분석 2026.01.22 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=RLhv8cC96tQtqeXl

- Tsubaki Nakashima stock analysis - Finbox: https://finbox.com/TSE:6464

- Tsubaki Nakashima financial ratios - Investing.com: https://www.investing.com/equities/tsubaki-nakashima-co-ltd-ratios

- Tsubaki Nakashima stock research - Stockopedia: https://www.stockopedia.com/share-prices/tsubaki-nakashima-co-TYO:6464/