DEEP RESEARCH · NURIFLEX 040160

NuriFlex (040160): Local-Energy, VPP, and ZEB Platform Research

Testing whether the company is moving from AMI hardware into an energy-data, control, billing, and trading platform

0. Bottom line first

I reconstruct NuriFlex from the source’s view that it should be valued not as a public-sector hardware supplier, but as a power-data collection, control, billing, and trading platform for the local-production/local-consumption, VPP, and ZEB transition. The key figures are KRW 2.78bn of cumulative Q3 2025 R&D, 12.16% of separate revenue, a KRW 99.7bn Guinea power-authority order, and a strategic treasury-share swap with Kukyoung G&M equal to 2%, or 241,000 shares worth about KRW 1.51bn.

Official fact: The source rebuilds the case from the November 13, 2025 quarterly report, the January 30, 2026 single-sales/supply contract disclosure, the February 25, 2026 earnings-structure change disclosure, and the February 27, 2026 corrected treasury-share disposal report.

Interpretation: Revenue decline and a wider net loss look weak at the surface, but a narrower operating loss, higher R&D intensity, and escrow-based revenue sharing point to a possible platform transition.

1. Business model and moat

Korea’s power market is entering a transition driven by grid congestion, regional data-center relocation, and regional electricity-price differentiation starting in 2026. The source sees this as a shift toward distributed energy resources, or DER, and local production/local consumption, with NuriFlex expanding from AMI solution sales into platform services.

| Q3 2025 cumulative separate revenue mix | Share | Meaning |

|---|---|---|

| VoIP solutions, including IP phones | 39.6% | Legacy communications solution base |

| Energy and industrial IoT solutions, including AMI, EMS, barcode/RFID | 39.0% | Core power-data and control business |

| Renewable-energy solutions, including solar equipment and ESS | 11.5% | Linked to ZEB and distributed energy |

| Nanomaterials | 6.46% | Potential expansion through NuriVista functional materials |

| Internet electronic billing service | 3.10% | Billing and notification data business |

| Healthcare | 0.34% | MediHub medical consulting platform |

Official fact: The source states that Smart Energy, including microgrid solutions and EMS, accounted for 24% of total revenue, or KRW 5.53bn, in Q3 2025. Other revenue includes leasing, technical services, platform maintenance, and rental revenue.

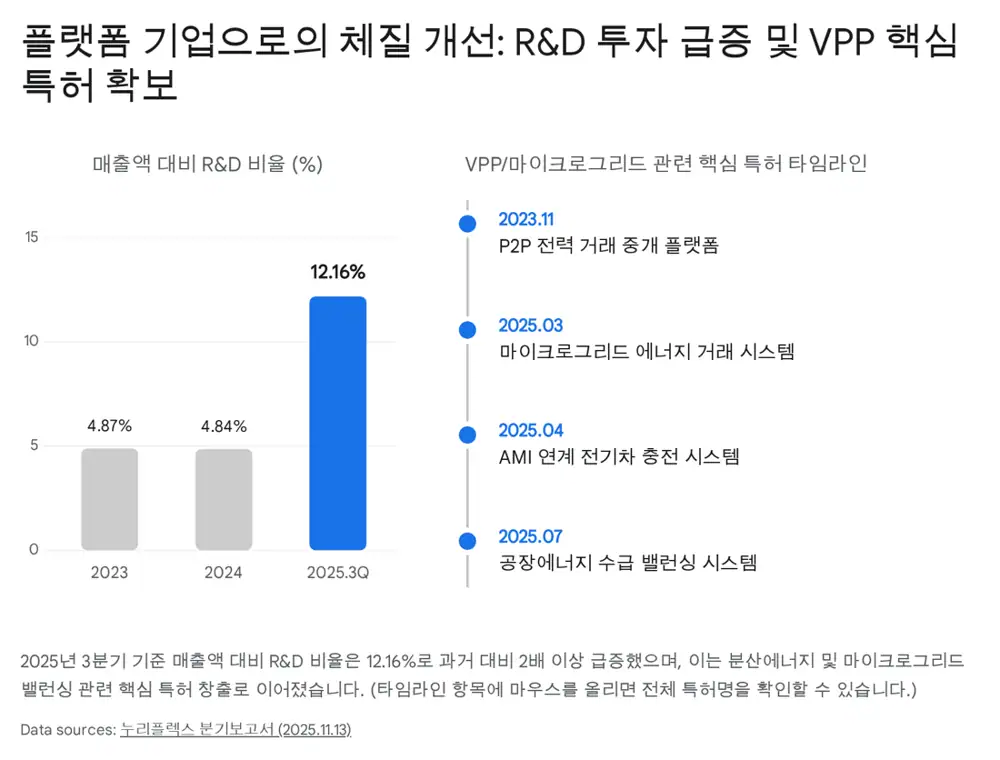

The moat evidence is R&D and patents. Cumulative Q3 2025 R&D expense was KRW 2.78bn, equal to 12.16% of separate revenue, far above 4.84% in the previous fiscal year and 4.87% in the year before that. The company operates three research labs covering energy IoT, VoIP solutions, and nanomaterials.

Microgrid trading

Energy user group management and energy trading systems using microgrid distributed resources.

EV charging

EV charging method and system using a community-level AMI network.

Factory energy

Factory-energy-based microgrid energy supply-demand balancing system and method.

Carbon credits

Brokerage method and device for energy savings and carbon-credit trading efficiency using energy data.

P2P power trading

System for providing a power-trading brokerage platform for peer-to-peer contracts.

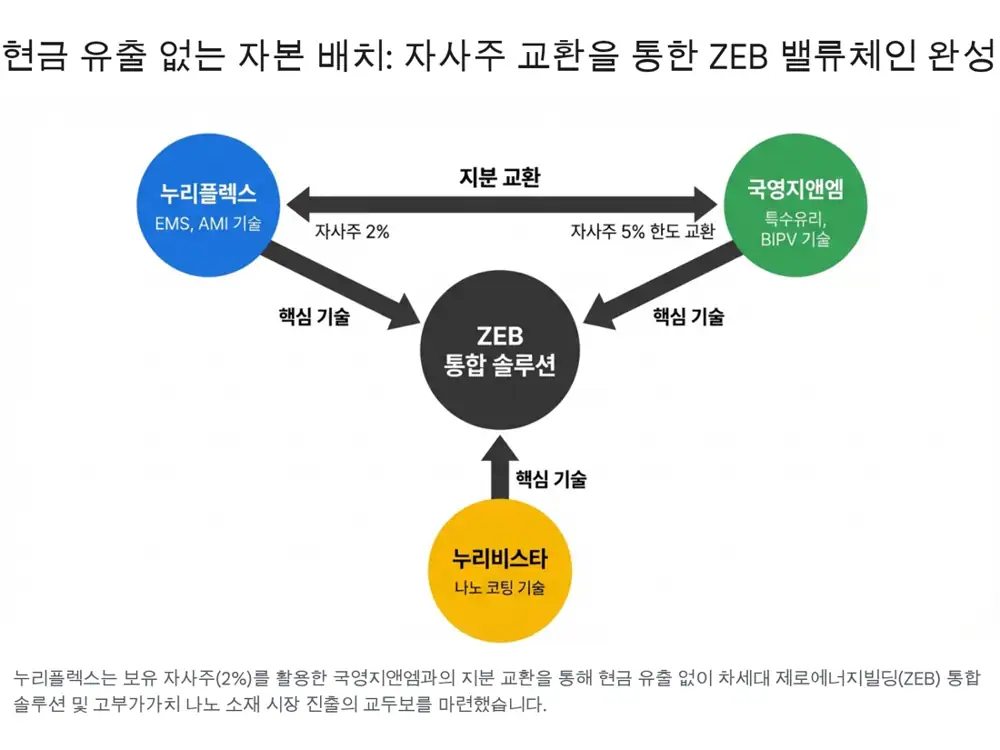

2. Local-energy and ZEB transition plus strategic alliance

The source treats regional electricity pricing under the distributed-energy law, expansion of distributed-energy zones, and the Ministry of Land, Infrastructure and Transport’s ZEB mandate roadmap as TAM expansion for NuriFlex. Power-intensive companies in the Seoul metropolitan area may be pushed toward self-generation and energy-efficiency solutions.

Official fact: According to the February 27, 2026 corrected material report, NuriFlex entered a strategic alliance with Kukyoung G&M through a treasury-share swap equal to 2% of issued shares, or 241,000 shares worth about KRW 1.51bn.

The alliance combines NuriFlex’s AMI and EMS technology with Kukyoung G&M’s high-insulation, high-shielding special glass and BIPV, or building-integrated photovoltaics, to jointly develop a ZEB integrated solution. Staged tasks include real-time monitoring and analysis of building energy use, minimizing heating and cooling loads through smart-glass control, and pilot construction of a high-efficiency building model aligned with ZEB certification standards.

3. Overseas-order risk and escrow hedge

Despite the positive platform transition, energy infrastructure and overseas public-sector projects carry large working-capital and collection-delay risks. The source isolates this as a major financial risk.

| Risk item | Source figure | Interpretation |

|---|---|---|

| Total current trade receivables, carrying amount | About KRW 61.7bn | Collection-delay risk in overseas B2G infrastructure |

| Receivables tied to NURIFLEX GHANA LTD | KRW 43.6bn | High country-specific credit concentration |

| Past loss allowance | More than KRW 4.0bn; later in the source, more than KRW 10.0bn of bad-debt allowance is mentioned | Conservative reflection of Ghana power-sector debt and delayed collection |

Interpretation: Past emerging-market expansion produced a working-capital backlash through delayed collection. That makes the structure of new orders more important than headline order size alone.

Official fact: The January 30, 2026 single-sales/supply contract shows a KRW 99.7bn, or USD 69.55mn, smart prepaid AMI system project with Guinea’s power authority, EDG.

4. Operating leverage through Q, P, and C

The source decomposes NuriFlex into Q, meaning volume and orders, P, meaning pricing and margin, and C, meaning cost structure, using 2025 earnings-change disclosures and Q3 report notes.

| Axis | 2024 | 2025 | Deep-research interpretation |

|---|---|---|---|

| Q: revenue and orders | Consolidated revenue KRW 129.3bn | Consolidated revenue KRW 101.5bn | Revenue fell KRW 27.7bn, or 21.45%. The Guinea order of KRW 99.7bn equals 77.1% of 2024 revenue. |

| P: pricing power | Mostly simple hardware supply and fixed-price contracts | Escrow-based revenue-sharing model introduced | The Guinea contract recovers 70% through a 50% share of electricity-sales revenue. |

| C: cost structure | Operating loss of KRW -8.15bn | Operating loss of KRW -6.08bn | Despite lower revenue, the operating loss improved by KRW 2.06bn, or 25.35%. |

| Net-income gap | KRW -4.40bn | KRW -6.66bn | The core business improved, but net loss widened due to lower non-operating income such as FX losses. |

On Q, the 2026 KRW 99.7bn order creates visibility for the next two to three years despite the 2025 revenue decline. On P, sharing electricity-sales revenue through escrow becomes the basis for pricing power rather than one-off supply pricing. On C, the source attributes the narrower operating loss to lower low-margin hardware mix, better software technical-service and Smart Energy/EMS mix, and control of variable costs such as outsourced processing.

Interpretation: A narrowing operating loss while R&D is around 12% of revenue can be read as movement toward fixed-cost break-even coverage. If Guinea and ZEB revenue are added next year, operating leverage sensitivity may increase.

5. Cash flow and capital allocation

The source argues that cash flow and capital allocation matter more than income-statement narrative. In public-sector and overseas B2B infrastructure, profits can still translate into weak cash flow if receivables are delayed.

| Item | Source figure | Meaning |

|---|---|---|

| Operating cash flow | Q3 2024 cumulative KRW -16.5bn → Q3 2025 cumulative KRW -0.99bn | Sharp reduction in cash outflow |

| Cash and cash equivalents | KRW 11.6bn | Immediate liquidity |

| Short-term financial products | KRW 6.2bn | Additional liquid resources |

| Cash plus short-term financial products | About KRW 17.8bn | Capacity to fund R&D and new business |

| Kukyoung G&M alliance | Treasury shares equal to 2%, 241,000 shares, about KRW 1.51bn | Secures BIPV and special-glass CAPEX infrastructure through partnership without cash outflow |

Interpretation: The source treats the wider 2025 net loss, KRW -6.66bn, as largely accounting-driven from FX valuation effects. The more important signal is the reduction in operating cash outflow from KRW -16.5bn to KRW -0.99bn.

6. Mispricing and catalysts

The source criticizes the market for treating NuriFlex as an old Korea Electric Power meter-modem supplier and reacting only to the 21.4% revenue decline and 51% wider net loss, or KRW -6.66bn. In contrast, the author emphasizes a KRW 2.06bn reduction in operating loss, up 25.35%, R&D above 12% of revenue, and microgrid/VPP patents as evidence of a platform turnaround.

KRW 99.7bn Guinea order

Disclosed on January 30, 2026. Two-year buildout with 30% L/C collection, followed by four years of receiving 50% of electricity-sales revenue through escrow.

ZEB turnkey solution

The February 27, 2026 Kukyoung G&M share swap combines BIPV hardware with NuriFlex EMS software.

Overseas collection and policy timing

Credit risk with overseas power authorities remains, as seen in Ghana receivables, and the actual pace of regional pricing and ZEB regulation should be tracked.

The source’s final expression is close to “BUY,” but this report is a reconstruction of the source’s logic, not a buy or sell recommendation. The indicators I would track are the first L/C payment or initial system shipment, real pilot construction with Kukyoung G&M, the Smart Energy revenue share, and further improvement in operating cash flow.

Sources

- 네이버블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224200603420

- Source link 1: 지역별 차등전기료 2026년 시행 > 뉴스 - 부경타임즈: http://bgtimes.kr/bbs/board.php?bo_table=news&wr_id=3390

- Source link 2: [ESG정책브리핑] 분산에너지법 시행...지역별 전기요금 차등화: https://www.esgeconomy.com/news/articleView.html?idxno=6799

- Source link 3: '분산특구 쌍둥이' 차등요금제는 난항…정부용역·與법안 '촉각' - Daum: https://v.daum.net/v/20251105165746496

- Source link 4: 가상발전소 관련주 심층 분석: 2026년 지역별 차등 요금제 시행에 따른 수혜주 전망: https://newsjjin.com/vpp-market-regional-pricing-strategy/

- Source link 5: 유틸리티 - 지역별 차등 요금제가 불러올 나비효과 - 유진투자증권: https://www.eugenefn.com/common/files/amail/20251125_B55_tjdgus2009_880.pdf

- Source link 6: (2026신) 제로에너지건축물(ZEB) 통합 인증시스템 - AI and Architecture - 티스토리: https://ai-and-architecture.tistory.com/63

- Source link 7: ZEB(제로에너지건축물) 5등급 의무화, 태양광 설치 안 하면 허가 불가?ㅣ태양광 정보: https://www.youtube.com/watch?v=0x1iDGN5-Z0

- Source link 8: How Ghana slid into energy sector debt and the lessons we must not ignore: https://citinewsroom.com/2026/01/how-ghana-slid-into-energy-sector-debt-and-the-lessons-we-must-not-ignore/

- Source link 9: Mahama Administration Pays US$1.470 Billion to Clear Energy Sector Debt and Restore World Bank Guarantee within First Year | Ministry of Finance: https://www.mofep.gov.gh/news-and-events/2026-01-12/mahama-administration-pays-us1.470-billion-to-clear-energy-sector-debt-and-restore-world-bank-guarantee-within-first-year