DEEP RESEARCH · INFINEON Q&A

Infineon Q1 FY2026 Conference Call 질의 Analysis

A Q&A reconstruction of AI power guidance, negative FCF, the ams OSRAM acquisition, and SiC, FX, and regulatory risks

0. Bottom line first

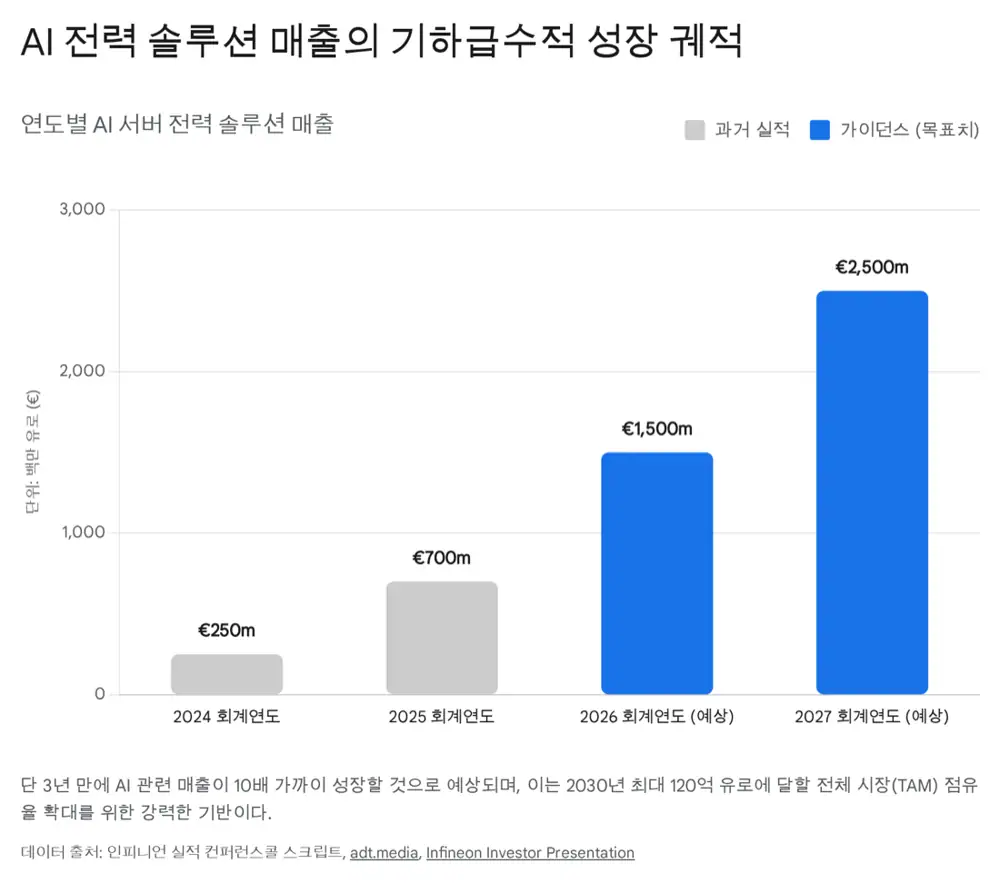

At the surface, FCF of EUR -199mn and 183 days of inventory are uncomfortable. I read them as a deliberate investment phase to secure AI power infrastructure. The key figures are EUR 1.5bn AI power revenue in 2026, EUR 2.5bn in 2027, EUR 500mn of accelerated CAPEX, and the EUR 570mn ams OSRAM sensor acquisition.

1. Financials and cash flow

Official fact: The source reports Q1 FY26 revenue of EUR 3.662bn, 7% year-on-year growth, about 14% constant-currency growth, segment result of EUR 655mn, segment result margin of 17.9%, and adjusted gross margin of 43.0%.

| Item | Source figure | Interpretation |

|---|---|---|

| FCF | EUR -199mn | Marvell automotive Ethernet acquisition, bonuses, and inventory build |

| Inventory | EUR 4.485bn, 183 days | Safety inventory for a recovery cycle |

| Backlog | EUR 21bn, up EUR 1bn QoQ | Six consecutive months of increase, supporting turnaround leverage |

2. Segment tone

Automotive

EUR 1.821bn revenue, down 5% QoQ, up 4% YoY, with 22.1% margin. SDV, ADAS, and 48V are offsets.

AI power

EUR 1.171bn revenue and 17.4% margin. AI server power-solution mix is the core driver.

Cyclical

GIP at EUR 349mn and 8.9%, CSS at EUR 321mn and 7.2%, leaving near-term weakness.

3. Q&A reconstruction

| Question topic | Management answer | My read |

|---|---|---|

| AI growth and FCF pressure | Non-AI recovery is gradual, while Dresden, Kulim, and AI equipment investments are required. | In 2026, securing supply capacity matters more than near-term cash flow. |

| ams OSRAM growth and China EV | The sensor business could generate about EUR 230mn in 2026 and sustain high-single-digit growth; China EV risk is addressed by reducing generic Si exposure and shifting to SiC, sensors, and SDV. | This is a portfolio pivot to defend margins. |

| SiC slowdown concern | Infineon is not dependent on one EV OEM and has broad solar, ESS, and charging-infrastructure customers. | The argument is better downside resilience than STMicroelectronics or onsemi. |

| M&A funding | No equity issuance; funded with debt and cash, with margin upside after Kulim transfer. | The sensor portfolio is strengthened without dilution. |

| FX | Each EUR/USD cent affects quarterly revenue by EUR 25mn and operating profit by EUR 10mn. | Dollar weakness is an external reported-revenue variable. |

4. Risks and conclusion

The source lists near-term risks: constrained dividend growth from about EUR 1.4bn adjusted FCF, China EV price competition, and euro strength depressing translated dollar revenue. Still, I think the summer 2026 Dresden fab ramp and AI power revenue recognition can shift the frame from automotive semiconductor leader to AI power-infrastructure leader.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224199654422

- Source link 1: http://googleusercontent.com/assisted_ui_content/1

- Source link 2: https://www.infineon.com/row/public/documents/corporate/investors/presentations/2026/2026-02-04-q1-fy26-analyst-call-v01-00-en.pdf

- Source link 3: https://www.investing.com/news/transcripts/earnings-call-transcript-infineon-technologies-sees-7-growth-in-q1-2026-93CH-4483740

- Source link 4: https://fintool.com/news/infineon-ai-investment-2-7-billion

- Source link 5: https://www.infineon.com/press-release/2026/infxx202602-0431

- Source link 6: https://www.infineon.com/assets/row/public/documents/corporate/investors/presentations/2026/20260203-ifx-ams-osram-acquisition-v01-00-en.pdf

- Source link 7: https://www.infineon.com/assets/row/public/documents/corporate/press/2026/infxx202602-042e.pdf

- Source link 8: https://www.infineon.com/assets/row/public/documents/corporate/investors/analyst-consensus/vara-consensus-on-infineon-as-of-2026-01-27-v01-00-en.pdf

- Source link 9: https://www.infineon.com/press-release/2026/infxx202602-042

- Source link 10: https://seekingalpha.com/article/4865629-infineon-technologies-ag-ifnny-q1-2026-earnings-call-transcript

- Source link 11: https://www.infineon.com/row/public/documents/corporate/investors/presentations/2026/2026-02-04-q1-fy26-intro-statement-analyst-call-v01-00-en.pdf

- Source link 12: https://www.adt.media/software-defined-vehicles/infineon-prioritises-ai-and-sdvs-in-2026/2616555

- Source link 13: https://www.intelmarketresearch.com/power-supply-unit-for-ai-data-centers-market-30653

- Source link 14: https://www.binance.com/en/square/post/32281409477002

- Source link 15: https://iconnect007.com/article/147669/infineon-meets-fy-2025-targets-raises-ai-power-revenue-goal-for-fy-2026/147666/ein

- Source link 16: https://www.infineon.com/assets/row/public/documents/corporate/investors/presentations/2025/2025-11-12-q4-fy25-investor-presentation-v01-00-en.pdf

- Source link 17: https://www.24marketreports.com/semiconductor-and-electronics/global-ai-server-acdc-power-supply-forecast-market

- Source link 18: https://www.infineon.com/assets/row/public/documents/corporate/press/2026/hv-2026-hanebeck-en.pdf

- Source link 19: https://www.eetimes.com/ams-osram-sells-sensor-business-to-infineon-to-focus-on-digital-photonics/

- Source link 20: https://silicon-saxony.de/en/infineon-and-ams-osram-expansion-of-leading-position-in-sensors-and-acquisition-of-ams-osrams-portfolio-of-non-optical-analog-mixed-signal-sensors/

- Source link 21: https://www.morningstar.com/stocks/xhan/ifx/earnings-transcript

- Source link 22: https://capital.com/en-int/analysis/infineon-stock-forecast

- Source link 23: https://www.perplexity.ai/finance/IFNNF/news/G2601316

- Source link 24: https://www.investing.com/news/analyst-ratings/kepler-cheuvreux-lowers-infineon-stock-price-target-to-eur42-on-fy-2026-caution-93CH-4241612