DEEP RESEARCH · INFINEON

Infineon: The Valuation Crossover Driven by AI Power Infrastructure

A review of 800VDC, Si·SiC·GaN turnkey power capability hidden behind the automotive semiconductor discount

0. Bottom line first

I think the market still frames Infineon as an automotive and industrial cycle name. But 300mm power wafers, SiC/GaN fabs, the 800VDC data-center transition, and the rising data-center share in PSS point to possible re-rating as an AI power-infrastructure company.

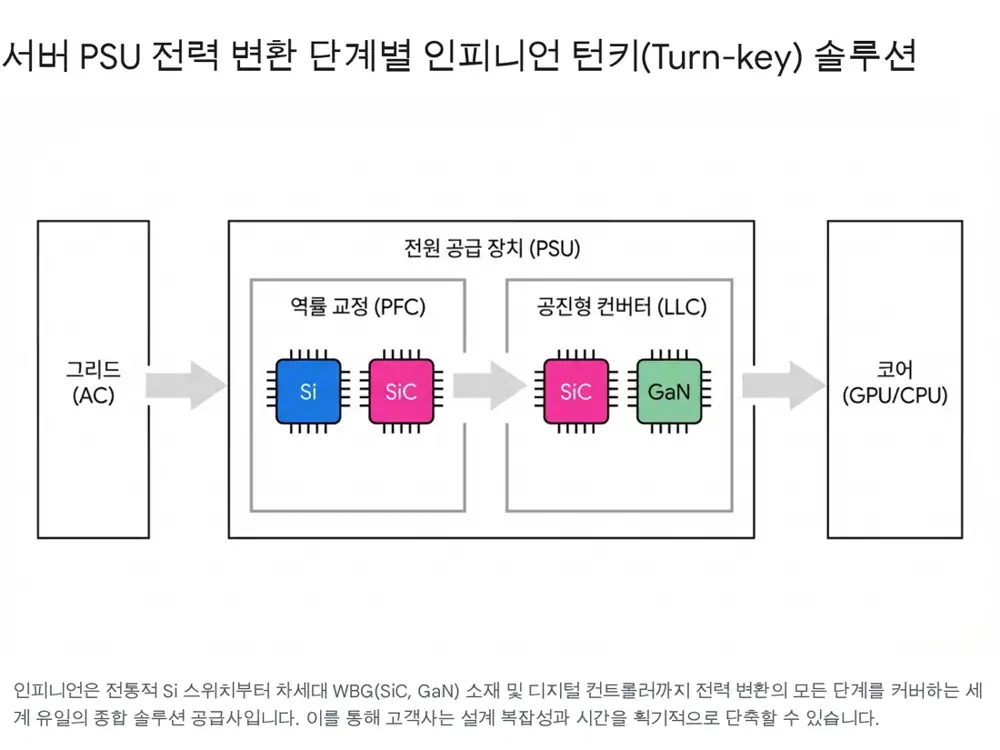

1. IDM moat and material portfolio

Official fact: The source describes Infineon as the No. 1 global power semiconductor IDM and says 300mm wafers produce 2.3x more dies than 200mm wafers while cutting die cost by about 30%.

2. The physics of 800VDC

The source says conventional CPU racks consumed 10-20kW, GB200/GB300 NVL72 consumes 125-140kW or more per rack, and the Vera Rubin generation expected in 2027 could reach 1MW per rack. Sending 1MW at 54V requires more than 18,500A and roughly 200kg of copper busbar per rack, which is the case for 800VDC.

| Item | Source figure | Investment implication |

|---|---|---|

| Voltage shift | 54V → 800V, about 15x | One-fifteenth current and lower losses |

| Copper reduction | Up to 45% | Rack design and cost improvement |

| Power efficiency | Up to 5% end-to-end improvement | Lower AI-factory operating cost |

| Maintenance | Up to 70% possible cost reduction | Incentive to adopt high-voltage architecture |

3. Earnings signal

Official fact: The source gives Q1 FY26 group revenue of EUR 3.662bn, PSS revenue of EUR 1.171bn, PSS margin of 17.4%, and adjusted gross margin of 43.0%.

Interpretation: PSS revenue fell on smartphone and consumer seasonality, but high-margin AI data-center mix lifted profitability. The source’s calculation puts AI plus data-center revenue at about 42% of PSS and about 13-14% of group revenue.

Automotive

EUR 1.821bn revenue and 22.1% margin. SDV, ADAS, and 48V architecture offset EV softness.

Power and sensor

Margin rose from 14.5% to 17.4%. AI power semiconductor mix is the driver.

Bottoming

GIP posted EUR 349mn and 8.9%; CSS posted EUR 321mn and 7.2%.

4. Valuation and catalysts

The source compares Infineon’s 12-month forward EV/EBITDA of about 12.2-13.7x with MPS at 40-90x or more, NXP at 14.6-15.5x, and onsemi at 13.8-16.7x. If the market recognizes Infineon as an AI power-infrastructure name, the source argues for an 18-20x or higher re-rating.

- Early ramp of the Dresden Smart Power Fab in summer 2026

- Sustained double-digit data-center share within PSS

- End of ATV/GIP inventory correction and normalized utilization

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224199622803

- Source link 1: https://www.infineon.com/press-release/2025/INFXX202507-122

- Source link 2: https://www.techpowerup.com/338633/infineon-to-start-300-mm-gan-wafer-production-as-tsmc-exits-market

- Source link 3: https://waferpro.com/200mm-wafer-vs-300mm-wafer/

- Source link 4: https://www.ieee-pels.org/magazine/infineon-reveals-first-300-mm-power-gan-wafers/

- Source link 5: https://www.microchipusa.com/electrical-components/200mm-vs-300mm-silicon-wafers

- Source link 6: https://www.infineon.com/press-release/2024/infxx202410-013

- Source link 7: https://www.infineon.com/technology/ultra-thin-silicon-power-wafer-technology

- Source link 8: https://www.infineon.com/content/dam/infineon/row/public/documents/technology/online-media-briefing-we-power-ai.pdf

- Source link 9: https://www.infineon.com/assets/row/public/documents/24/59/whitepaper-scaling-ai-data-center-power-delivery-with-si-sic-and-gan.pdf

- Source link 10: https://www.infineon.com/applications/information-communication-technologies/hyperscale-computing

- Source link 11: https://www.infineon.com/press-release/2025/INFXX202510-003

- Source link 12: https://blogs.nvidia.com/blog/gigawatt-ai-factories-ocp-vera-rubin/

- Source link 13: https://www.powerelectronicsnews.com/powering-the-future-how-nvidia-and-infineon-are-reinventing-ai-data-center-architecture/

- Source link 14: https://www.edn.com/the-shift-to-800-vdc-power-architectures-in-ai-factories/

- Source link 15: https://www.nb.com/en/us/insights/the-800-volt-gorilla-inside-ai-data-centers

- Source link 16: https://developer.nvidia.com/blog/nvidia-800-v-hvdc-architecture-will-power-the-next-generation-of-ai-factories/

- Source link 17: https://forums.developer.nvidia.com/t/nvidia-800-v-hvdc-architecture-will-power-the-next-generation-of-ai-factories/333814

- Source link 18: https://navitassemi.com/wp-content/uploads/2025/10/Redefining-Data-Center-Power-GaN-and-SiC-Technologies-for-Next-Gen-800-VDC-Infrastructure.pdf

- Source link 19: https://www.infineon.com/row/public/documents/corporate/investors/presentations/2025/2025-11-26-power-roadshow-v01-00-en.pdf

- Source link 20: https://www.powersemiconductorsweekly.com/2025/10/13/infineon-backs-nvidias-800-vdc-power-architecture-to-enable-the-next-generation-of-ai-data-centers/

- Source link 21: https://www.gartner.com/en/newsroom/press-releases/2025-11-17-gartner-says-electricity-demand-for-data-centers-to-grow-16-percent-in-2025-and-double-by-2030

- Source link 22: https://www.datainsightsmarket.com/reports/ai-server-power-ics-167778

- Source link 23: https://www.infineon.com/assets/row/public/documents/corporate/press/market-news/2024/we-power-ai-online-media-briefing.pdf

- Source link 24: https://www.ti.com/about-ti/newsroom/news-releases/2025/ti-teams-with-nvidia-to-bring-efficient-power-distribution-to-ai-infrastructure.html

- Source link 25: https://flex.com/resources/advancing-the-transition-to-800-vdc-data-centers-with-nvidia

- Source link 26: https://www.investing.com/pro/BMV:IFXN/explorer/ev_to_ebitda_ltm

- Source link 27: https://finbox.com/OTCPK:IFNN.F/explorer/ev_to_ebitda_fwd

- Source link 28: https://www.tikr.com/blog/monolithic-power-systems-stock-2026-outlook-after-80-returns

- Source link 29: https://simplywall.st/stocks/us/semiconductors/otc-ifnn.f/infineon-technologies/valuation

- Source link 30: https://multiples.vc/public-comps/nxp-semiconductors-valuation-multiples

- Source link 31: https://finbox.com/DB:XS4/explorer/ev_to_ebitda_ltm/