DEEP RESEARCH · WOLFSPEED

Wolfspeed FY2026 Q2: First Full Quarter After Chapter 11 and the SiC Pivot

EV softness, fresh-start accounting, AI data centers, 300mm SiC, and refinancing risk in one report

0. Bottom line first

On surface numbers, this quarter looked extremely weak. My focus is whether, after accounting noise and restructuring costs, Wolfspeed is actually shifting toward AI data centers, industrial energy, and 300mm SiC.

- FY2026 Q2 revenue was $168.5mn, in line with the midpoint of guidance but down 6.6% year over year and below the $199.38mn consensus cited in the source.

- Non-GAAP EPS was -$6.11, far worse than the -$0.63 estimate cited in the source.

- AI data-center revenue rose 50% sequentially and doubled over the last three quarters.

- The single-crystal 300mm SiC wafer milestone is central to long-term cost advantage and possible AR/VR, optics, and thermal-management expansion.

- The key near-term risk is the mid-2026 step-up in first-lien debt interest and the refinancing path.

1. Results: Power grew, Materials collapsed

| Metric | FY25 Q2 | FY26 Q1 | FY26 Q2 | QoQ | YoY |

|---|---|---|---|---|---|

| Total revenue | 180.5 | 196.8 | 168.5 | -14.4% | -6.6% |

| Power Products | 90.8 | 107.1 | 118.3 | +10.5% | +30.3% |

| Materials Products | 89.7 | 89.7 | 50.2 | -44.0% | -44.0% |

| GAAP gross margin | -21% | -39% | -46% | -7pp | -25pp |

| Adjusted EBITDA | N/A | N/A | -82.0 | N/A | N/A |

Power devices grew 30% year over year to $118.3mn, helped by Mohawk Valley stabilization and about $75mn of contribution. Materials fell 44% year over year to $50.2mn as demand softened and competition intensified.

Interpretation: A -46% gross margin alone makes the business look uninvestable, but the mix matters. Power is growing while Materials is breaking down. EV softness is real, and data-center/industrial energy growth is not yet large enough to cover the damage.

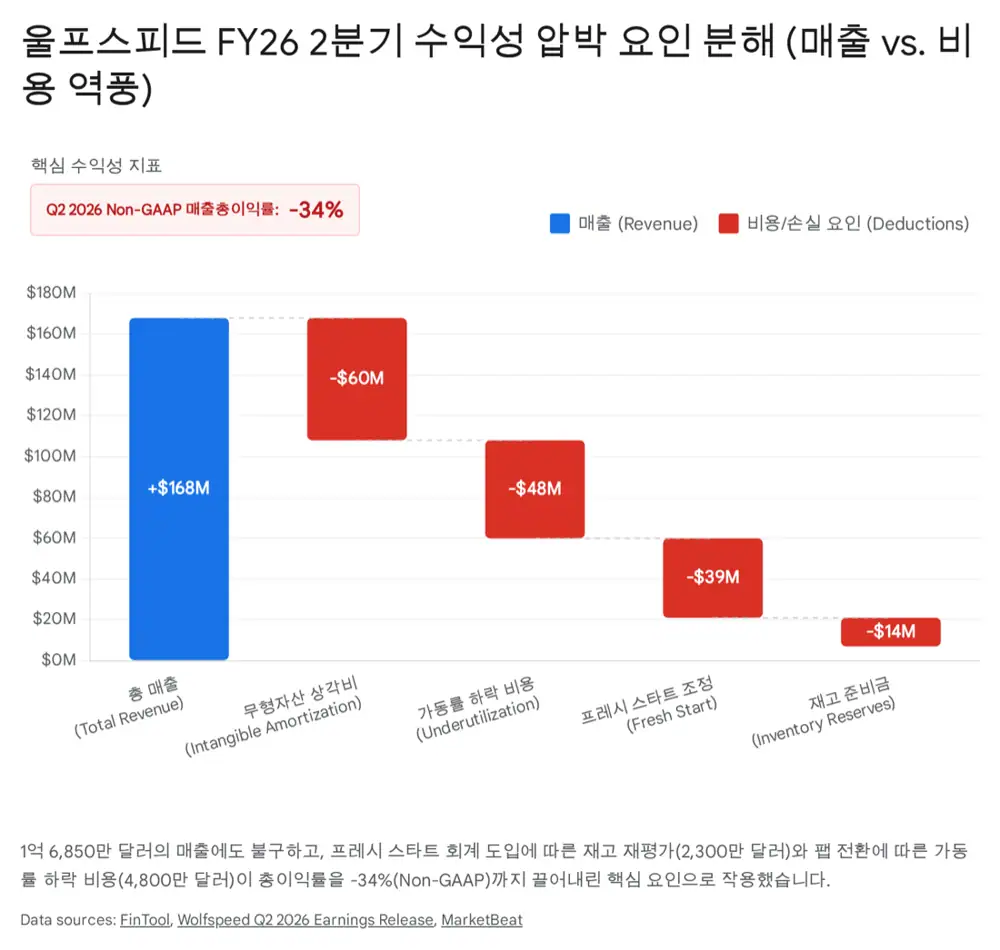

2. Loss quality: separate cash losses from accounting charges

Official fact: GAAP gross margin was -46%, Non-GAAP gross margin was -34%, reported operating loss was $158.4mn, and adjusted EBITDA was -$82.0mn.

Underutilization costs

Fixed-cost burden from closing 150mm Durham device production one month early and moving production to 200mm Mohawk Valley.

Fresh Start accounting

After Chapter 11 exit, assets and liabilities were reset to fair value based on a $2.6bn enterprise value.

Inventory step-up

Inventory revalued upward flowed through COGS when sold. This is not a direct cash outflow.

Specific inventory reserve

Write-downs tied to legacy product exits and demand shifts.

Fresh Start accounting also created about $60mn of quarterly intangible amortization. For near-term analysis, I separate accounting step-up in COGS from actual operating cash losses.

3. Liquidity: cash improved, but the L1 step-up remains

Official fact: Cash and short-term investments were $1.3bn at quarter-end. The company accelerated $700mn of cash refund through the 48D advanced manufacturing tax credit.

Wolfspeed repaid $175mn of first-lien debt in cash and converted about 1.5mn shares of second-lien convertible debt, removing $18mn of debt. Total debt fell about 70% versus the pre-bankruptcy level, and quarter-end net debt was about $600mn.

Debt repayment should save $25mn of annual interest, and total cash interest expense is down about 60% from before restructuring. OpEx savings from the 150mm closure and workforce cuts are about $200mn annualized, and CapEx fell more than 90% from about $400mn per quarter previously to $31mn this quarter.

Interpretation: The $1.3bn cash balance buys time, not a solution. Before the first-lien debt interest step-up in mid-2026, refinancing or maturity extension needs to succeed for the turnaround to work.

4. Q3 guidance: next quarter pressured the stock

Management guided Q3 revenue to $140mn-$160mn, below the $162.8mn consensus cited in the source and below Q2 revenue of $168.5mn.

- Customers are digesting pull-in inventory bought ahead of the Durham 150mm shutdown.

- During Chapter 11, some customers built dual sourcing with STMicroelectronics, Infineon, and others, creating temporary share leakage.

- Global EV demand weakness may continue through FY2026.

Interpretation: This guide drove the after-hours and premarket pressure. Long-term AI and 300mm logic is separate, but the market has not yet confirmed a bottom in EV and Materials demand.

5. Strategic pivot: from EV one-trick to four verticals

New CEO Robert Feurle described a move away from an EV-heavy one-trick strategy toward four verticals: automotive, industrial and energy, aerospace and defense, and materials.

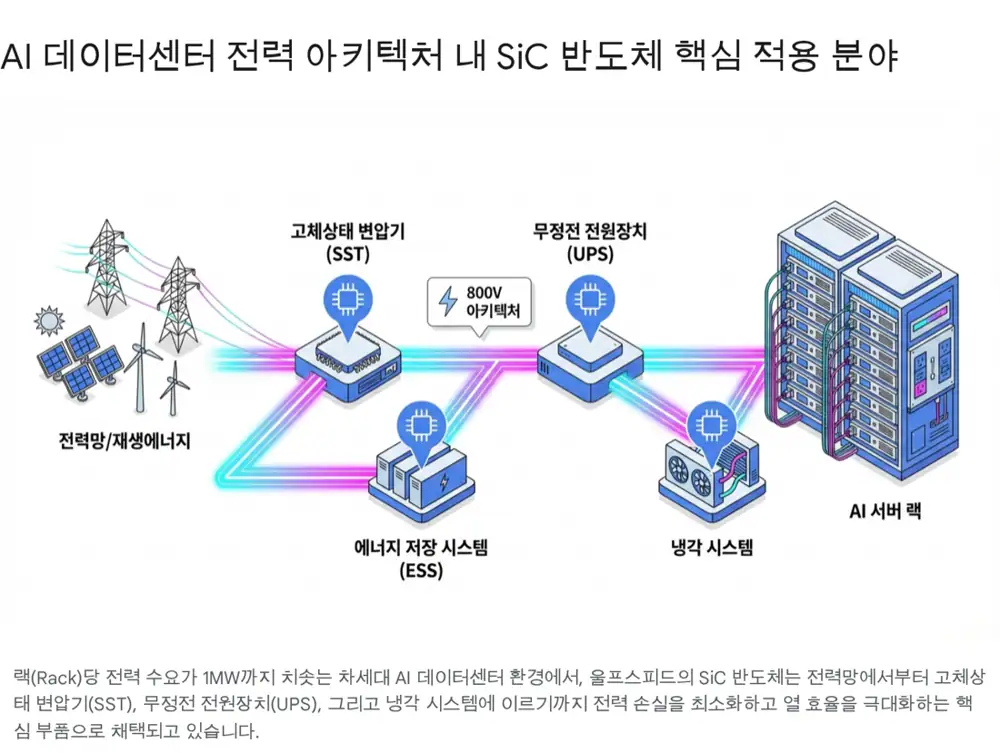

Official fact: AI data-center revenue grew 50% sequentially and doubled over the last three quarters.

The data-center power argument is that rack power moves from legacy 10kW levels to 100kW and eventually 600kW-1MW mega-racks by around 2029. Wolfspeed positions SiC across generation/grid, ESS, SST, UPS, and cooling systems, which account for about 40% of data-center power use according to the source.

In EVs, the Toyota BEV onboard-charger SiC partnership is presented as a reliability signal, while Hopewind supports the solar and wind inverter opportunity.

6. 300mm SiC: the long-term cost moat

Official fact: The source says Wolfspeed demonstrated the industry's first single-crystal 300mm, or 12-inch, SiC wafer. The industry is still transitioning from 150mm to 200mm, and Wolfspeed is already producing 200mm-based power devices at Mohawk Valley.

| 300mm implication | Source figure/detail | Investment point |

|---|---|---|

| Area increase | 2.25x versus 200mm | More chips per wafer |

| Good die increase | More than 2.3x after edge-loss effects | Lower long-term cost per chip |

| New applications | AR/VR, telecom, optics, thermal management | Market expansion beyond power semis |

| Supply chain | 100% U.S. vertical integration | Geopolitical premium |

The source emphasizes SiC's thermal conductivity, optical refractive-control properties, and mechanical strength for potential AR/VR lens and thermal-substrate uses. It also cites Yole Group's Poshun Chiu describing the milestone as a key to new strategic-material opportunities.

7. Q&A and Wall Street reaction

| Questioner | Core question | Management answer and investment implication |

|---|---|---|

| Brian Lee / Goldman Sachs | EV diversification and L1 step-up | Sales organization is moving to application verticals. L1 cash interest steps up in mid-2026, and refinancing options are being evaluated. |

| Christopher Rolland / Susquehanna | AI data-center TAM and demand bottom | SiC is positioned across the path from 100kW to MW racks. Short-term demand forecasting remains uncertain. |

| Jed Dorsheimer / William Blair | Refinancing benefit and 300mm usage | Interest savings depend on financing instruments. Mohawk Valley and Siler City initial investments are complete; customer demand drives utilization. |

| Joe Cardoso / JPMorgan | EV customer positioning | Toyota and U.S. vertical integration support customer confidence, though JPMorgan lowered its target on weak EV visibility. |

| Firm | Rating/target | Core rationale |

|---|---|---|

| Piper Sandler / Harsh Kumar | Overweight, $6 → $20 | Positive on debt falling from $13.6bn to $1.7bn and CapEx down 90% |

| Susquehanna / Christopher Rolland | Neutral, $30 → $20 → $15 | Concern over $140mn-$160mn Q3 guide, negative gross margin, and customer defection risk |

| Goldman Sachs / Brian Lee | Buy, $19 → $17 | AI data-center power demand is positive, but L1 step-up is a near-term valuation risk |

| JPMorgan / Samik Chatterjee | Neutral/Underweight, $20 → $17 | EV demand weakness and materials competition hurt investor confidence |

8. Final view

Wolfspeed is hard to judge by EPS alone because accounting losses and operating transition costs overlap. The $23mn Fresh Start inventory step-up and intangible amortization are non-cash, but adjusted EBITDA of -$82mn and a down Q3 guide are still heavy.

Interpretation: My first checkpoint is refinancing in the first half of 2026. If it is resolved on favorable terms without damaging dilution, the long-term case around $1.3bn cash, 200mm Mohawk Valley, 300mm SiC, and 50% AI data-center growth remains alive. If not, the capital structure can overpower the technology moat.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224199405300

- 1. Investing.com: Wolfspeed shares tumble: https://www.investing.com/news/earnings/wolfspeed-shares-tumble-as-q2-results-miss-estimates-guidance-disappoints-93CH-4486158

- 2. Stock Titan: Wolfspeed 424B3: https://www.stocktitan.net/sec-filings/WOLF/424b3-wolfspeed-inc-prospectus-filed-pursuant-to-rule-424-b-3-dc3b80bbf189.html

- 3. Investing.com Wolfspeed transcript: https://www.investing.com/news/transcripts/earnings-call-transcript-wolfspeeds-q2-2026-results-disappoint-stock-dips-93CH-4486298

- 4. Intellectia: Wolfspeed Q2 FY2026: https://intellectia.ai/news/etf/wolfspeed-q2-fiscal-2026-results-miss-expectations

- 5. Fintool: Wolfspeed crash after Q2: https://fintool.com/news/wolfspeed-q2-crash-chapter-11

- 6. Fintool: WOLF Q1 2026 transcript: https://fintool.com/app/research/companies/WOLF/documents/transcripts/q1-2026

- 7. Wolfspeed Q2 FY2026 earnings release PDF: https://s29.q4cdn.com/278875087/files/doc_earnings/2026/q2/earnings-result/Wolfspeed_Q2_2026_Earnings_Release.pdf

- 8. The Motley Fool transcript: https://www.fool.com/earnings/call-transcripts/2026/02/04/wolfspeed-wolf-q2-2026-earnings-call-transcript/

- 9. Investing.com Q2 FY2026 slides: https://www.investing.com/news/company-news/wolfspeed-q2-fy26-slides-pivoting-to-ai-data-centers-amid-financial-restructuring-93CH-4486326

- 10. TechPowerUp: 300mm SiC breakthrough: https://www.techpowerup.com/345133/wolfspeed-achieves-300mm-silicon-carbide-sic-technology-breakthrough

- 11. Semiconductor Today: single-crystal 300mm SiC: https://www.semiconductor-today.com/news_items/2026/jan/wolfspeed-130126.shtml

- 12. Stock Analysis: WOLF forecast: https://stockanalysis.com/stocks/wolf/forecast/

- 13. Semiconductor Today: AI data center growth: https://www.semiconductor-today.com/news_items/2026/feb/wolfspeed-160226.shtml

- 14. Fintool: Q2 FY2026 earnings: https://fintool.com/app/research/companies/WOLF/earnings/Q2%202026

- 15. Wolfspeed investor relations quarterly results: https://investor.wolfspeed.com/financials/quarterly-results/default.aspx

- 16. MarketBeat Q2 highlights: https://www.marketbeat.com/instant-alerts/wolfspeed-q2-earnings-call-highlights-2026-02-07/

- 17. Nasdaq: expert outlook: https://www.nasdaq.com/articles/glimpse-expert-outlook-wolfspeed-through-8-analysts

- 18. MarketBeat forecast: https://www.marketbeat.com/stocks/NYSE/WOLF/forecast/

- 19. Stock Titan Q2 results: https://www.stocktitan.net/news/WOLF/wolfspeed-reports-financial-results-for-the-second-quarter-of-fiscal-02jc6c6wndmw.html

- 20. Seeking Alpha: $140M-$160M Q3 target: https://seekingalpha.com/news/4547658-wolfspeed-outlines-140m-160m-q3-revenue-target-as-ai-data-center-momentum-offsets-ev-softness

- 21. Seeking Alpha: weak outlook: https://seekingalpha.com/news/4547898-wolfspeed-falls-after-weak-outlook-as-analysts-mull-lackluster-demand-in-ev-market

- 22. FinancialContent: 300mm wafer and AI: https://markets.financialcontent.com/concordmonitor/article/tokenring-2026-1-21-wolfspeed-shatters-power-semiconductor-limits-worlds-first-300mm-silicon-carbide-wafer-arrives-to-power-the-ai-revolution

- 23. ADT: 300mm SiC manufacturing maturity: https://www.adt.media/electric-vehicle-technology/wolfspeed-brings-300mm-sic-wafers-to-manufacturing-maturity/2602060

- 24. Power Electronics News: 300mm SiC wafer: https://www.powerelectronicsnews.com/wolfspeed-achieves-300-mm-sic-wafer-production/

- 25. Ticker Nerd WOLF forecast: https://tickernerd.com/stock/wolf-forecast/

- 26. Stock Analysis WOLF ratings: https://stockanalysis.com/stocks/wolf/ratings/

- 27. TipRanks Christopher Rolland: https://www.tipranks.com/experts/analysts/christopher-rolland

- 28. Market Chameleon: 300mm SiC path: https://marketchameleon.com/articles/b/2026/1/13/wolfspeed-300mm-silicon-carbide-breakthrough-ai-arvr-power