DEEP RESEARCH · AUTOIMMUNE BIOTECH

Korean Autoimmune Biotech Platform and Pipeline Comparison

A peer review of AprilBio, HanAll Biopharma, and GI Innovation across platform quality, commercialization, balance sheet, and catalysts

0. Bottom line first

Among the three companies, I view AprilBio as having the strongest risk-reward today. The thesis is the overlap of SAFA clinical validation, next-generation APB-A1 and APB-R3 mechanisms, roughly KRW 70bn in cash-like assets, and the APB-A1 Phase 1b catalyst expected in Q2 2026.

1. Platform competitiveness

Official fact: The source compares AprilBio’s SAFA, HanAll Biopharma’s FcRn inhibitor mechanism, and GI Innovation’s GI-SMART platform.

SAFA·REMAP

SAFA extends half-life through serum-albumin binding and supports convenience improvements such as IV-to-SC and weekly-to-monthly dosing. REMAP points to multi-specific antibodies, ADCs, solid tumors, and MASH.

FcRn inhibition

The mechanism blocks pathogenic IgG recycling and promotes autoantibody degradation. Batoclimab and IMVT-1402 aim to improve first-generation safety issues.

GI-SMART

The platform uses protein fusion and linker design. GI-301 is positioned as an IgE Trap with stronger binding than Xolair in the source narrative.

2. Pipeline and market potential

In TED, the source compares APB-A1 (CD40L), Tepezza (IGF-1R), and batoclimab (FcRn). It notes Tepezza generated USD 1.9bn in 2024 sales and USD 381mn in Q1 2025, while safety issues such as hearing loss and IV administration burden remain.

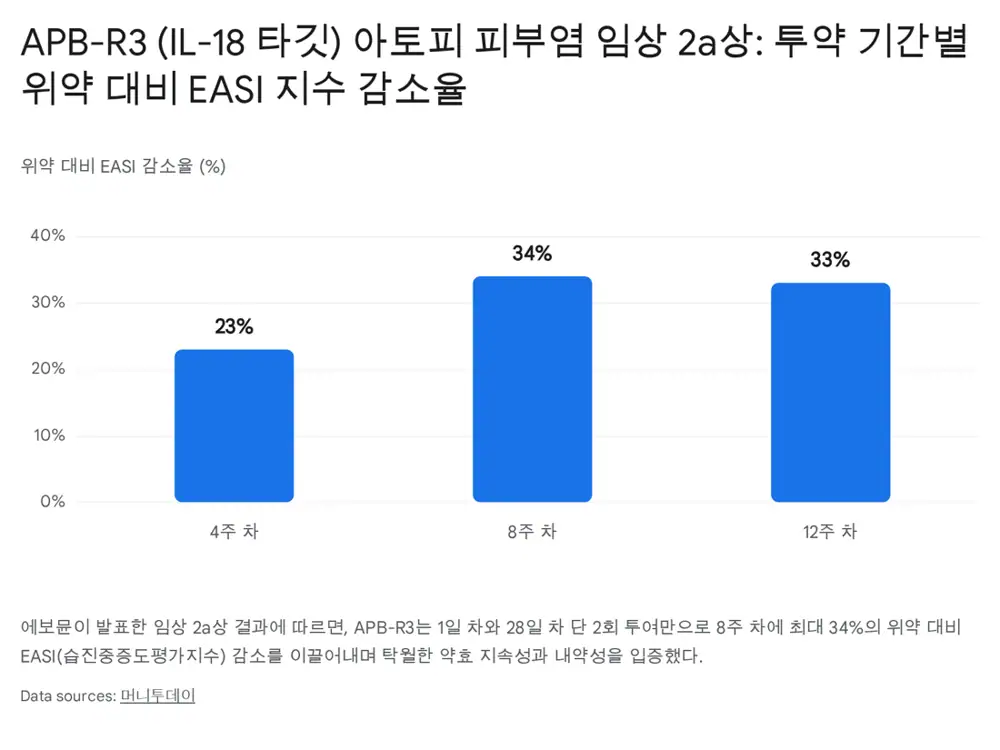

In atopic dermatitis, APB-R3 targets IL-18 against Dupixent’s IL-4/13 axis and non-responder limitations. The source says Evommune’s February 2026 APB-R3 Phase 2a result showed up to a 34% EASI reduction.

| Company | Core assets | Source catalysts | Main risk |

|---|---|---|---|

| AprilBio | APB-A1, APB-R3, SAFA/REMAP | Q2 2026 APB-A1 TED Phase 1b, H2 2026 APB-R3 Phase 2b | Early clinical data still needs confirmation |

| HanAll Biopharma | Batoclimab, IMVT-1402 | H1 2026 TED global Phase 3, 2027 Graves/MG events | Expectations and safety management |

| GI Innovation | GI-301 | CSU Phase 2 progress, need for additional L/O | Lack of near-term late-stage readout |

3. Finance and valuation

Interpretation: In biotech investing, I put more weight on data and cash runway than scientific appeal alone. AprilBio’s roughly KRW 70bn in cash-like assets and partner milestones reduce dilution risk. HanAll has a commercial cash cow with 2025 revenue of KRW 155.2bn. GI Innovation still carries valuation risk from a large rights offering despite milestone income.

- The key check is APB-A1 patient efficacy and safety.

- HanAll has greater commercialization visibility if late-stage trials succeed, but expectations are high.

- GI Innovation needs GI-301 Phase 2 progress and a new licensing event.

4. Final view

My top pick is AprilBio, based on financial downside support, SAFA platform validation, CD40L/IL-18 next-generation targets, and a dense 2026 data calendar.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224199374788

- Source link 1: https://www.medipana.com/news/articleView.html?idxno=405991

- Source link 2: https://www.sisajournal-e.com/news/articleView.html?idxno=411192

- Source link 3: https://www.insightkorea.co.kr/news/articleView.html?idxno=241011

- Source link 4: https://biz.chosun.com/stock/stock_general/2026/02/11/GZQVBYFDHRCPNIVGC4M7WE3H5I/

- Source link 5: https://m.sedaily.com/article/20004525

- Source link 6: https://m.medigatenews.com/news/1343274662

- Source link 7: https://www.digitaltoday.co.kr/aigongsi/3818/gi-innovation-yuhan-gi301-milestone-fee

- Source link 8: https://www.biospectator.com/news/view/26630

- Source link 9: https://pmc.ncbi.nlm.nih.gov/articles/PMC11126416/

- Source link 10: https://pmc.ncbi.nlm.nih.gov/articles/PMC9312457/

- Source link 11: https://pmc.ncbi.nlm.nih.gov/articles/PMC11175988/

- Source link 12: https://pmc.ncbi.nlm.nih.gov/articles/PMC8988977/

- Source link 13: https://pmc.ncbi.nlm.nih.gov/articles/PMC11137266/

- Source link 14: https://www.mayo.edu/research/clinical-trials/diseases-conditions/thyroid-eye-disease

- Source link 15: https://www.frontiersin.org/journals/ophthalmology/articles/10.3389/fopht.2023.1295902/full

- Source link 16: https://www.delveinsight.com/insights/tepezza-market-sales-forecast

- Source link 17: https://www.mdpi.com/1422-0067/25/21/11628

- Source link 18: https://pmc.ncbi.nlm.nih.gov/articles/PMC10511347/

- Source link 19: https://clinicaltrials.gov/study/NCT07308964

- Source link 20: http://www.aprilbio.com/board/board.php?bo_table=news&idx=43

- Source link 21: https://nhsjs.com/2025/thyroid-eye-disease-and-the-changing-landscape-of-new-drugs-in-development/

- Source link 22: https://www.pharmaceutical-technology.com/analyst-comment/the-7mm-atopic-dermatitis-market-to-experience-growth-reaching-22-4bn-by-2033/

- Source link 23: https://www.grandviewresearch.com/industry-analysis/dupixent-market-report

- Source link 24: https://www.medicalnewstoday.com/articles/drugs-adbry-vs-dupixent

- Source link 25: https://www.goodrx.com/conditions/eczema/adbry-vs-dupixent

- Source link 26: http://oreateai.com/blog/adbry-vs-dupixent-navigating-the-cost-landscape-of-advanced-eczema-treatments/dd1d406baed97f0699a0fdf68aab7609

- Source link 27: https://synapse.patsnap.com/article/what-are-the-market-competitors-for-dupixent

- Source link 28: https://www.delveinsight.com/report-store/interleukin-inhibitors-market-forecast

- Source link 29: https://pmc.ncbi.nlm.nih.gov/articles/PMC9056466/

- Source link 30: https://pmc.ncbi.nlm.nih.gov/articles/PMC9464283/

- Source link 31: https://pmc.ncbi.nlm.nih.gov/articles/PMC11946805/

- Source link 32: https://skin.dermsquared.com/skin/article/view/3041

- Source link 33: https://pmc.ncbi.nlm.nih.gov/articles/PMC10864083/

- Source link 34: https://www.doctronic.ai/blog/adbry-vs-dupixent-comparing-two-leading-eczema-treatments/

- Source link 35: https://www.healthline.com/health/drugs/adbry-vs-dupixent

- Source link 36: https://file.alphasquare.co.kr/media/pdfs/company-ir/20250306_%ED%95%9C%EA%B5%AD%ED%88%AC%EC%9E%90%EC%A6%9D%EA%B6%8C-%EC%97%90%EC%9D%B4%ED%94%84%EB%A6%B4%EB%B0%94%EC%9D%B4%EC%98%A4_%EA%B8%B0%EC%97%85_Report.pdf

- Source link 37: https://www.mt.co.kr/thebio/2026/02/11/2026021113261739622

- Source link 38: https://comp.wisereport.co.kr/company/c1010001.aspx?cmp_cd=397030&cn=

- Source link 39: https://kind.krx.co.kr/external/2026/01/27/000469/20260127001534/70791.htm

- Source link 40: https://m.finance.daum.net/quotes/A397030/news/disclosure/20251124089743

- Source link 41: https://money2.daishin.com/PDF/Out/intranet_data/Product/ResearchCenter/Report/2026/02/56599_MMB_260211.pdf

- Source link 42: https://www.sisajournal-e.com/news/articleView.html?idxno=412709