DEEP RESEARCH · DELL TECHNOLOGIES

Dell Technologies FY26 Q4: AI Servers, Memory Shock, and the FY27 $50 Billion AI Target

A research report on Dell's AI backlog, pricing power, storage attach, and FY27 setup

0. Bottom line first

My core read is that Dell is no longer just an AI-server assembler. The company is tying together supply chain, pricing, storage, networking, and deployment services in a way that can justify an AI infrastructure platform re-rating.

- FY26 Q4 revenue was $33.4bn, up 39% year over year, and Non-GAAP EPS was $3.89, up 45%.

- Full-year revenue was $113.5bn and EPS was $10.30, up 19% and 27% respectively.

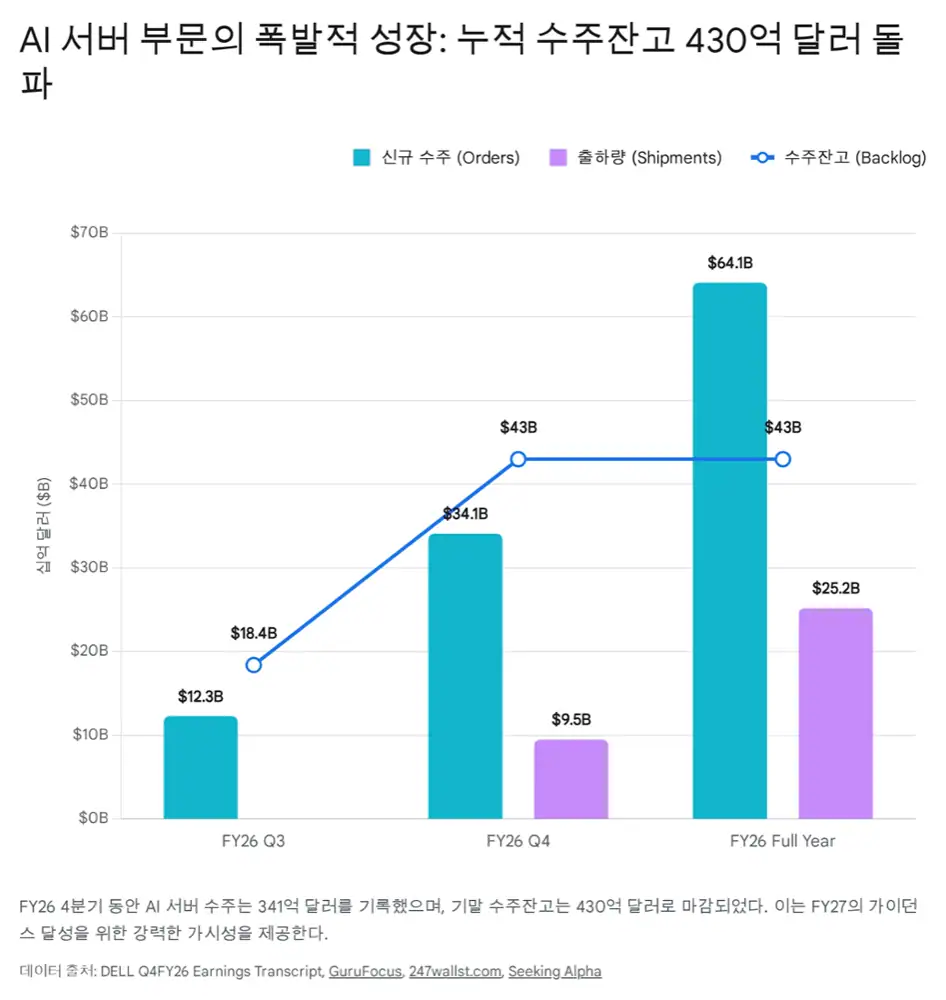

- AI servers delivered $34.1bn of Q4 orders, $9.5bn of shipments, $9.0bn of recognized revenue, and $43bn of ending backlog.

- The FY27 AI-server revenue target is $50bn. Management said the current backlog is almost entirely Grace Blackwell, while Vera Rubin is still in the five-quarter pipeline rather than backlog.

- Memory inflation is a near-term margin risk, but Dell is using dynamic pricing, long-term supply agreements, and Dell IP storage compression to widen the gap versus weaker competitors.

1. Results: AI servers changed Dell's scale

Official fact: Dell reported FY26 Q4 revenue of $33.4bn and Non-GAAP EPS of $3.89, ahead of Wall Street expectations of roughly $31.4bn-$31.6bn of revenue and $3.52-$3.53 of EPS.

| Item | Figure | Investment read |

|---|---|---|

| FY26 Q4 revenue | $33.4bn, +39% YoY | AI-server demand lifted the company profile |

| FY26 Q4 Non-GAAP EPS | $3.89, +45% YoY | Revenue growth translated into earnings |

| FY26 revenue | $113.5bn, +19% YoY | A major corporate transition point |

| FY26 EPS | $10.30, +27% YoY | Profitability improved with scale |

| Q4 AI-server orders | $34.1bn | Described as almost three times the prior quarter |

| AI-server backlog | $43bn | The backbone of FY27 visibility |

Interpretation: The most important point for me is that the five-quarter pipeline still grew after Dell converted $34.1bn of orders. That suggests AI infrastructure demand is spreading beyond hyperscalers into sovereign AI, Tier 2 CSPs, neoclouds, and enterprises.

2. Segments: ISG renaissance, CSG calculated pressure

ISG: AI and traditional servers move together

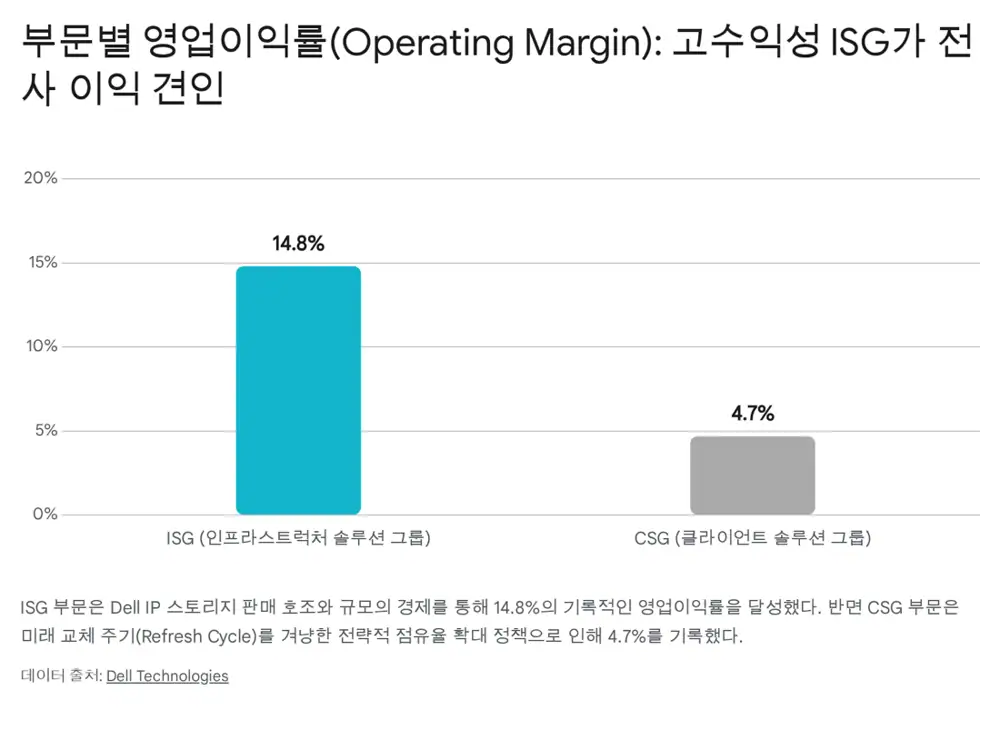

Infrastructure Solutions Group revenue was $19.6bn, up 73% year over year. Operating income was $2.9bn, and operating margin was 14.8%, up 240bp sequentially.

AI-server Q4 shipments were $9.5bn while revenue recognized was $9.0bn. The $500mn gap was in-transit product shipped near the January close and expected to convert to revenue when delivered.

Traditional server and networking revenue was also strong at $5.9bn, up 27% year over year. Management said moving from 14G servers to 16G/17G platforms can deliver a 7:1 consolidation benefit.

CSG: buy share first, raise price later

Client Solutions Group revenue was $13.5bn, up 14% year over year. Commercial revenue was $11.6bn, up 16%, while consumer revenue was $1.9bn and roughly flat.

CSG operating margin was only 4.7%, but the source frames this as strategy, not failure. Dell delayed pricing actions from October through December to gain share, lifted PC share by about 100bp, added more than 4,000 new customers, and then implemented a broad price increase on January 6.

Cash generation and shareholder returns

Official fact: Q4 operating cash flow was $4.7bn, and FY26 operating cash flow was $11.2bn. Q4 cash conversion cycle was negative 32 days, flat sequentially and one day better year over year.

Dell returned $2.2bn to shareholders in Q4 and $7.5bn for the year. Annual repurchases included 54mn shares, more than double the prior year. The FY27 annual dividend rose 20% to $2.52 per share, and the board authorized a new $10bn repurchase program.

AI servers and storage

$19.6bn of revenue and 14.8% operating margin, with Dell IP storage and operating leverage doing the work.

Share capture

$13.5bn of revenue. Dell accepted near-term margin pressure to expand the customer base before price resets.

Financial capacity

$11.2bn of annual CFO and a negative 32-day CCC are the capital base for large-scale AI-server execution.

3. Memory supercycle: risk and moat

Official fact: The source says DRAM spot prices rose 5.5 times over the last six months to $2.39 per gigabit, while NAND flash costs rose roughly four times to $0.20 per gigabyte.

Capacity is moving toward HBM and high-capacity enterprise DDR5 for AI data centers, creating shortages in general-purpose DRAM and NAND. The source frames this as a multi-year cycle that may extend beyond 2026 into 2027-2028.

Interpretation: This is dangerous for assemblers, but it may help Dell separate from the pack. Dell shortened quote validity, raised list prices, compressed discounts, and reduced promotions so component costs can be reflected in customer pricing much faster.

| Margin defense | Source detail | Meaning |

|---|---|---|

| Dynamic pricing | Cost pass-through moved from about 90 days to days or even one day | Less margin squeeze |

| Long-term supply agreements | LTAs with major component vendors | Better component access |

| PowerStore compression | 5:1 data reduction | Lower physical drive burden for customers |

| Data Protection | 75:1 compression and dedupe | Storage software moat strengthens |

| SMCI contrast | SMCI gross margin pressure around 9%-10% | Large platforms gain share in shortage cycles |

4. From Blackwell to Vera Rubin: pipeline over air pocket

The $43bn AI-server backlog is concentrated in NVIDIA Grace Blackwell and Blackwell systems. The market concern is that the next-generation 3nm Vera Rubin cycle, expected in the second half of 2026, could create a temporary buying pause.

Official fact: Management said Vera Rubin is not included in the current $43bn backlog but is well represented in the five-quarter pipeline. Management also expects the Rubin transition to be smoother than Blackwell.

Enterprise AI customers have passed 4,000. Agentic AI and inference workloads increase token usage and compute density. The source also cites Dell's NxtGen liquid-cooled AI factory in India with more than 4,000 Blackwell GPUs and Dell's sovereign AI work with S-AI across EMEA.

5. FY27 guidance and Wall Street views

Official fact: Dell's FY27 total revenue guide is $138bn-$142bn, with the $140bn midpoint implying 23% growth. The AI-server revenue target is $50bn, roughly double the prior year.

| Firm | Rating/target | Core logic |

|---|---|---|

| JPMorgan / Samik Chatterjee | Overweight, $155 → $165 | Raising profit outlook despite memory inflation signals confidence in downside protection |

| Barclays / Tim Long | Upgraded to Overweight, $148 → $168 | $34bn of AI orders was almost three times the prior quarter |

| Citi / Asiya Merchant | Buy, $160 → $180 | Accelerating AI adoption benefits the broader Dell portfolio |

| BofA / Wamsi Mohan | Buy, $150 → $135 | Memory pressure matters, but cost savings and supply-chain management help |

| Morgan Stanley / Erik Woodring | Underweight, $111 → $101 | Hardware budget softness, memory margin pressure, and demand elasticity remain concerns |

6. Q&A investment checkpoints

| Questioner | Core question | Management answer and my read |

|---|---|---|

| Tim Long / Barclays | AI-server margin and pull-through | Mid-single-digit AI margin is sustainable. Storage, networking, and deployment attach support the margin floor. |

| Mark Newman / Bernstein | Memory price shock | Traditional servers took pricing on December 10; PCs waited until January 6 after share gains. The 4.7% CSG margin looks like calculated pressure. |

| Louis Miscioscia / Daiwa | x86 server recovery | Demand exceeded supply. 14G-to-17G upgrades create 7:1 consolidation, and AI halo demand supports traditional servers. |

| Amit Daryanani / Evercore | Vera Rubin air pocket | Rubin should be smoother after Blackwell lessons. FY27 FCF confidence remained intact. |

| Ben Reitzes / Melius | Dell IP storage and margin | PowerStore 5:1 and Data Protection 75:1 compression/dedupe become stronger selling points when components inflate. |

| Erik Woodring / Morgan Stanley | Memory inflation assumptions | DRAM up 5.5x and NAND up 4x, but quote refresh and cost pass-through are now much faster. |

| Krish Sankar / Cowen | Enterprise AI and Agentic AI | More than 4,000 new enterprise customers. Agentic software sharply raises token and compute demand. |

| Wamsi Mohan / BofA | Pricing and pull-forward | Infrastructure customers prioritized supply assurance over price; PCs showed some pull-forward. |

| Samik Chatterjee / JPMorgan | $50bn guide and capacity | The $43bn backlog is almost all Grace Blackwell; Rubin is outside backlog, leaving later upside. |

| Aaron Rakers / Wells Fargo | $9.5bn shipments vs $9.0bn revenue | The $500mn gap is in transit. Traditional servers are driven more by ASP and dense configurations than by units. |

| Asiya Merchant / Citi | Storage and service attach | Storage, high-speed networking, and lifecycle deployment/maintenance attach challenge the low-margin assembler narrative. |

| David Vogt / UBS | PC share durability | Dell historically gains share in component shortage cycles, using LTAs and capital strength to absorb weaker competitors' share. |

7. Final view: platform control over short-term noise

As the source concludes, memory and PC margin noise looks more like a stress test of Dell's long-term thesis than a thesis-breaker. The more severe component inflation becomes, the more important supply contracts, cash flow, pricing systems, and Dell IP storage compression become.

Interpretation: I see two next catalysts. First, whether the FY27 $50bn AI-server target can move higher when Rubin orders convert. Second, whether storage, networking, and services attach to AI-server shipments strongly enough to justify a valuation framework beyond hardware.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224199250541

- 1. Investing.com earnings call transcript: https://www.investing.com/news/transcripts/earnings-call-transcript-dell-technologies-q4-2026-beats-expectations-with-record-earnings-93CH-4530107

- 2. Trefis: Dell stock pre-market: https://www.trefis.com/data/companies/DELL/no-login-required/tQvmxZYq/Dell-Stock-Pre-Market-12-Blowout-Earnings-AI-Fueled-FY27-Guidance

- 3. MarketBeat earnings result: https://www.marketbeat.com/instant-alerts/dell-technologies-nysedell-issues-earnings-results-beats-estimates-by-036-eps-2026-02-26/

- 4. Dell Technologies FY2026 results: https://investors.delltechnologies.com/news-releases/news-release-details/dell-technologies-delivers-fourth-quarter-and-full-year-fiscal-3

- 5. GuruFocus earnings call highlights: https://www.gurufocus.com/news/8660052/dell-technologies-inc-dell-q4-2026-earnings-call-highlights-record-revenue-and-ai-demand-propel-growth

- 6. MLQ.ai Dell Q4 report: https://mlq.ai/news/dell-technologies-reports-strong-q4-earnings-beat-with-massive-ai-server-growth/

- 7. MarketBeat earnings call highlights: https://www.marketbeat.com/instant-alerts/dell-technologies-q4-earnings-call-highlights-2026-02-27/

- 8. The Stack: Dell AI customers: https://www.thestack.technology/dell-breaks-records-says-traditional-server-demand-as-well-as-ai-surging/

- 9. IDC: memory crisis and PC outlook: https://www.idc.com/resource-center/blog/higher-asps-lower-unit-volumes-how-the-memory-crisis-is-reshaping-the-pc-and-smartphone-outlook/

- 10. IDC: global memory shortage crisis: https://www.idc.com/resource-center/blog/global-memory-shortage-crisis-market-analysis-and-the-potential-impact-on-the-smartphone-and-pc-markets-in-2026/

- 11. Fintool: SMCI margins: https://fintool.com/news/goldman-smci-sell-margin-erosion

- 12. Deep Research Global SMCI report: https://www.deepresearchglobal.com/p/super-micro-computer-company-analysis-outlook-report

- 13. Morningstar: Dell manages memory shortages: https://www.morningstar.com/news/marketwatch/20260226567/dells-stock-soars-as-record-earnings-signal-the-company-is-managing-memory-shortages-well

- 14. TradingView/Zacks Dell Q4: https://www.tradingview.com/news/zacks:242d20745094b:0-dell-q4-earnings-beat-estimates-revenues-rise-y-y-shares-up/

- 15. The Motley Fool Dell transcript: https://www.fool.com/earnings/call-transcripts/2026/02/26/dell-dell-q4-2026-earnings-call-transcript/

- 16. Dell Technologies IR transcript: https://investors.delltechnologies.com/static-files/9e5d4126-0f17-4ceb-b26c-a2563b8bcbc9

- 17. Dell Technologies IR talking points: https://investors.delltechnologies.com/static-files/3ab662a3-5383-4ae9-9d98-7c2c9adfbf39

- 18. TradingView/GuruFocus Evercore view: https://www.tradingview.com/news/gurufocus:44de48d73094b:0-dell-stock-is-climbing-evercore-sees-double-digit-eps-growth-potential/

- 19. Seeking Alpha: FY26 AI shipments: https://seekingalpha.com/news/4526096-dell-targets-25b-in-ai-server-shipments-for-fy26-as-ai-backlog-pipeline-hit-records

- 20. CTV: AI server revenue forecast: https://www.ctvnews.ca/business/article/dell-shares-jump-on-forecast-it-will-double-ai-server-revenue/

- 21. Seeking Alpha: $50B FY27 AI target: https://seekingalpha.com/news/4558386-dell-outlines-50b-ai-revenue-target-for-fy-27-as-company-exits-record-year

- 22. Seeking Alpha: memory cost pressure: https://seekingalpha.com/news/4558735-tech-firms-margins-under-pressure-from-rising-memory-costs

- 23. Gotraka: DRAM and NAND price spikes: https://www.gotraka.com/blogs/news/the-global-memory-crunch-dram-and-nand-price-spikes-reshape-computing-markets

- 24. Investing.com: structural shift in tech economics: https://www.investing.com/analysis/the-end-of-cheap-memory-why-2026-marks-a-structural-shift-in-tech-economics-200675634

- 25. Nasdaq: DELL vs SMCI: https://www.nasdaq.com/articles/dell-vs-smci-which-ai-server-stock-offers-better-growth-opportunity

- 26. Finviz: DELL vs SMCI: https://finviz.com/news/314795/dell-vs-smci-which-ai-server-stock-offers-better-growth-opportunity

- 27. LetsDataScience: NVIDIA chip cycle: https://www.letsdatascience.com/blog/nvidia-just-shipped-the-most-powerful-ai-chip-ever-made

- 28. NVIDIA Rubin platform: https://nvidianews.nvidia.com/news/rubin-platform-ai-supercomputer

- 29. Reddit hardware Rubin discussion: https://www.reddit.com/r/hardware/comments/1q5d97x/a_discussion_on_the_announced_specs_of_rubin_vs/

- 30. Dell AI predictions 2026: https://www.dell.com/en-us/blog/ai-predictions-2026-reflecting-on-the-past-shaping-the-future/

- 31. HPCwire: Dell and NxtGen: https://www.hpcwire.com/aiwire/2026/01/30/dell-technologies-enables-nxtgen-to-build-indias-largest-ai-factory/

- 32. Dell sovereign AI EMEA: https://www.dell.com/en-us/dt/corporate/newsroom/announcements/detailpage.press-releases~usa~2026~1~sovereign-ai-selects-dell-technologies-to-power-next-generation-ai-data-centers-across-emea.htm

- 33. Intellectia: Dell FY27 demand: https://intellectia.ai/news/stock/dell-expects-strong-revenue-for-fy27-amid-ai-demand

- 34. Seeking Alpha: Dell jumps after Q4: https://seekingalpha.com/news/4557911-dell-jumps-as-q4-results-guidance-blow-past-wall-streets-forecast-on-ai-strength

- 35. Trefis: blowout earnings: https://www.trefis.com/stock/dell/articles/591740/dell-stock-pre-market-12-blowout-earnings-ai-fueled-guidance/2026-02-27

- 36. 24/7 Wall St. live earnings: https://247wallst.com/investing/2026/02/26/live-earnings-will-dell-technologies-dell-spike-after-q4-results/

- 37. Futunn: AI revenue expected to double: https://news.futunn.com/en/post/69369524/dell-s-fy2026-q4-earnings-call-ai-revenue-expected-to

- 38. Barchart: $50B AI revenue in sight: https://www.barchart.com/story/news/472791/with-50-billion-ai-revenue-in-sight-and-up-20-today-is-dell-stock-still-a-buy

- 39. MLQ.ai: upbeat Q1 revenue guidance: https://mlq.ai/news/dell-issues-upbeat-q1-revenue-guidance-well-above-expectations/