DEEP RESEARCH · ASIA ECONOMY

Asia Economy: From Media Company to Hybrid Investment Holding Company

Governance reset, capital harvesting, NPL cleanup, and the 2025 cash-flow turnaround

0. Bottom line first

My read is that Asia Economy is no longer just an economic media outlet. It has become a hybrid investment holding company combining media cash flow, Keystone PE capital allocation, and Pine Construction-linked capital.

- In January 2025, All In Irum became the single largest shareholder with 9,091,575 shares, or 26.05%.

- Keystone PE holds 9.90% and, under the shareholder agreement described in the source, continues to lead practical management.

- Investment cash flow for the first nine months of 2025 was +KRW 15.787bn, a sharp reversal from -KRW 26.982bn in the prior-year period.

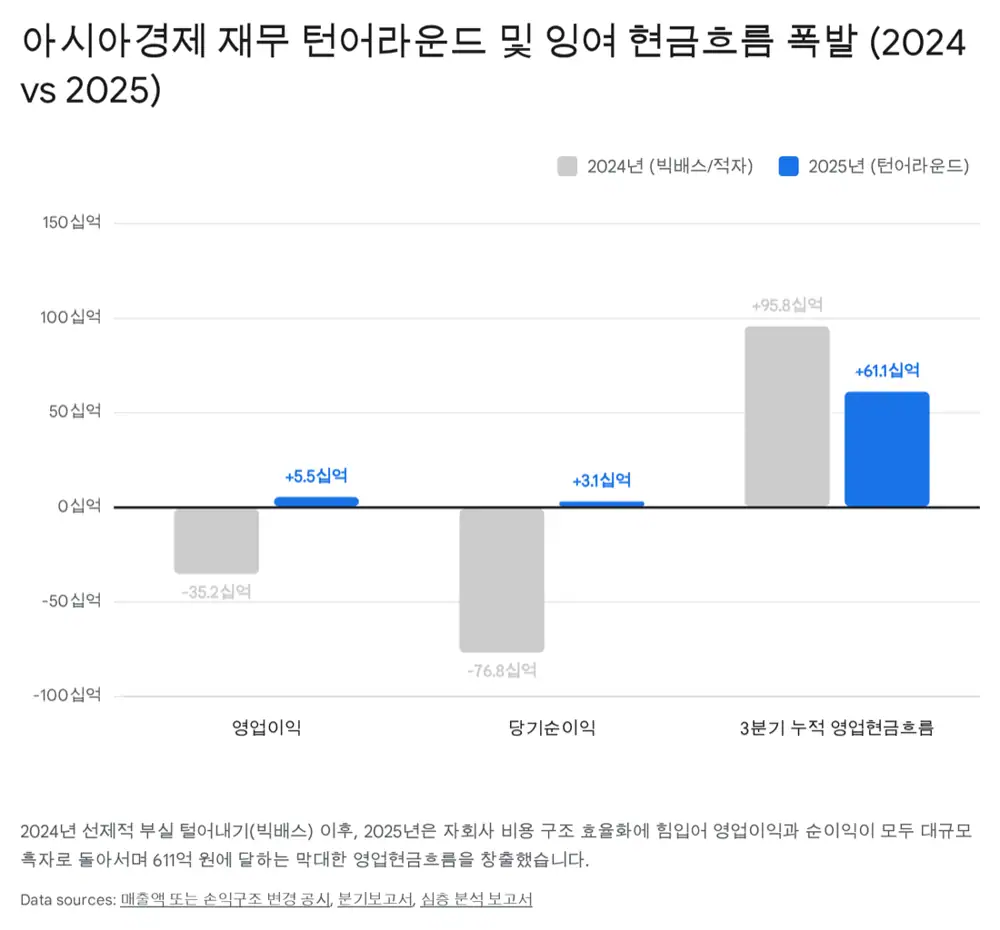

- 2025 consolidated revenue fell 6.2% to KRW 73.14bn, but operating profit turned positive at KRW 5.54bn and net income at KRW 3.11bn.

- Operating cash flow for the first nine months of 2025 was KRW 61.11bn, and cash and equivalents at quarter-end were KRW 75.036bn.

1. Business identity: beyond an economic media outlet

Asia Economy is known as an economic media company providing portal and internet information intermediary services. The source argues that, as of 2025 consolidated accounts, it should be understood as a hybrid investment holding company with specialty finance, lending, venture capital, and real-estate alternative investment arms.

Interpretation: Looking only at traffic or advertising revenue misses the point. The investment question is whether media-driven information, network, and cash flow can become capital-allocation capability through the finance portfolio.

2. Governance: KMH to Keystone PE to All In Irum

Before mid-2021, KMH Group was the largest shareholder. In July 2021, Keystone PE acquired 26.33% of common shares through Keystone Dynamic No. 5 investment SPC and also bought KRW 7bn face value of the third BW from Leisure Plus. The BW represented roughly 14.78% of existing shares, or about 6.51mn convertible shares, taking Keystone PE's control to 40.07%.

On January 21, 2025, the 45.52% stake held by Keystone Angels No. 2 PEF was distributed in kind to LPs due to fund dissolution and liquidation. All In Irum bought 3,030,525 shares from Lee Kwan-geun off-market at KRW 1,720 per share and, together with distributed shares, became the single largest shareholder with 9,091,575 shares, or 26.05%.

| Shareholder | Stake at end-Q3 2025 | Note |

|---|---|---|

| All In Irum | 26.05% | Single largest shareholder, construction-capital backing |

| Keystone Private Equity | 9.90% | Practical management lead |

| Broadhigh Asset Management | 9.48% | Major institutional investor |

| HTC Korea | 7.18% | Related party of largest shareholder |

| Employee stock ownership association | 5.07% | Employee-held stake |

| JS Pan Asia | 2.39% | Related party of largest shareholder |

| Treasury shares | 3.01% | Shareholder-return resource |

Official fact: The source says All In Irum CEO Nam Yoon-kwang also serves as head of management support at Pine Construction, and All In Irum borrowed about KRW 5.2125bn until January 20, 2026, with Pine Industrial Development joint guarantee, to buy Lee Kwan-geun's stake.

The source also states that practical management remains with Keystone PE under the shareholder agreement, while All In Irum secured a put option exercisable against Keystone PE after March 31, 2026. The current structure therefore reads as a two-track model combining Pine Construction-linked capital and Keystone PE restructuring capability.

3. Investment cash flow: from expansion to harvesting

From 2021 to 2023, the company built finance vehicles including A-Capital, Scala Corporate Finance Loan, and Next Elevation. In the first nine months of 2024, CFI was -KRW 26.982bn, including about KRW 14.498bn of long-term financial product purchases, KRW 3bn of additional subsidiary share purchases, and KRW 908mn of fair-value equity purchases.

From 2H 2024 into 2025, the capital-allocation posture shifted from new investments to asset monetization and deleveraging. CFI for the first nine months of 2025 turned positive at +KRW 15.787bn.

| Item | 9M 2024 | 9M 2025 | Meaning |

|---|---|---|---|

| Disposal of short-term financial products | KRW 572,950,122 | KRW 39,777,698,170 | Financial assets converted to cash |

| Disposal of long-term financial products | KRW 0 | KRW 5,149,651,607 | Recovery of tied-up capital |

| Disposal of FVOCI equity securities | KRW 0 | KRW 9,500,915,874 | Non-core equity monetization |

| Purchase of tangible assets | -KRW 6,479,155,104 | -KRW 1,955,910,682 | Traditional capex reduced |

| Purchase of intangible assets | -KRW 8,000,000 | -KRW 159,704,545 | CMS and software investment |

| Investment cash flow | -KRW 26,982,204,530 | +KRW 15,787,982,404 | Shift into liquidity harvesting |

4. Subsidiaries: A-Capital normalization is central

A-Capital is a specialty finance company founded in 2007 and consolidated through Keystone Bankers No. 1 in 2021. At the end of Q3 2025, assets were KRW 171.6bn, including KRW 87.9bn of loans, KRW 7.0bn of installment financing, and KRW 2.3bn of lease assets.

High rates and Korean real-estate PF stress after 2022 created provisioning and impairment pressure, contributing to Asia Economy's KRW 35.1bn consolidated operating loss in 2024. Management chose to sell bad loans at discounts to dedicated NPL buyers such as UAMCO and remove them from the books.

Official fact: The source cites an NPL market in which UAMCO acquired about KRW 3.7221tn of NPLs, or 47% of the market. A-Capital recorded KRW 8.79bn of revenue and KRW 6.84bn of net income for the first nine months of 2025.

Scala Corporate Finance Loan is summarized with 99% corporate loans, 1% individual loans, a 99.91% equity ratio, and KRW 150mn of net income in Q3 2025. Next Elevation is the VC arm connecting the media network to deal sourcing.

5. Four engines behind the 2025 CFO jump

Official fact: According to the February 27, 2026 disclosure, 2025 consolidated revenue fell 6.2% to KRW 73.14bn, but operating profit improved by KRW 40.7bn from a KRW 35.16bn loss to KRW 5.54bn profit, and net income improved by more than KRW 79.8bn from a KRW 76.75bn loss to KRW 3.11bn profit.

One-time impairments removed

2024 absorbed provisions and impairments, creating a base effect in 2025.

Debt repayment

9M 2025 financing cash flow was -KRW 39.617bn, and short-term debt repayment was KRW 94.0018bn.

Interest receipts

Interest receipts from loans and leases were KRW 9.65044bn, with about KRW 230mn of dividends received.

B2B cash cow

Financial news and data supplied to HTS, MTS, Naver, and portals support locked-in cash flow.

Interpretation: The KRW 61.11bn of 2025 CFO is important because of quality, not only size. Bad assets were removed, about KRW 94bn of short-term debt was repaid, and B2B media cash flow supported finance-subsidiary normalization.

6. Cash-flow waterfall and treasury-share purchase

Cash and cash equivalents at end-Q3 2025 were KRW 75.036bn, up about KRW 37.278bn from the opening KRW 37.758bn. Operating cash flow of +KRW 61.1bn, investment cash flow of +KRW 15.7bn, and financing cash flow of -KRW 39.6bn worked together.

Official fact: On February 27, 2026, the company signed a KRW 10bn treasury-share acquisition trust with NH Investment & Securities. The contract runs from March 3, 2026 to March 2, 2027, with stated purposes of share-price stabilization, shareholder value enhancement, and employee performance compensation.

The source interprets this as roughly 2.44% of shares based on 33,853,686 floating shares. It also frames the buyback as a defense against overhang from the KRW 9.2bn fifth private CB issued in February 2024, with KRW 1,208 conversion price, 4.0% yield to maturity, 2.0% coupon, and a put option from 2H 2025.

7. Final view

Asia Economy has moved from media company to hybrid investment holding company over five years. After the 2024 KRW 76.7bn net loss and real-estate PF concerns, NPL sales and deleveraging produced 2025 operating profit of KRW 5.54bn, net income of KRW 3.11bn, and 9M CFO of KRW 61.11bn.

Interpretation: The next checkpoints are threefold: whether A-Capital normalization is repeatable, whether the KRW 10bn buyback actually absorbs floating supply, and whether All In Irum/Pine Construction capital plus Keystone PE management can turn the media-finance-real estate mix into recurring numbers.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224198938994

- 1. 한국기자협회: 아시아경제 사모펀드 매각 논의: http://www.journalist.or.kr/news/article_print.html?no=49843

- 2. 모바일한경: 최대주주 올인이룸 변경: https://plus.hankyung.com/apps/newsinside.view?aid=202501248421r&category=&sns=y

- 3. KIND: 71209 최대주주 변경: https://kind.krx.co.kr/external/2025/01/24/000009/20250124000007/71209.htm

- 4. 미디어스: 사모펀드가 운영하는 최초 언론사: https://www.mediaus.co.kr/news/articleView.html?idxno=219734

- 5. KIND: 아시아경제 분기보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=searchInitInfo&acptNo=20251114003042&docno=

- 6. KIND: 아시아경제 정정 최대주주변경: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250124000009&docno=&viewerhost=&

- 7. 이투데이 CInsight: 아시아경제 지배구조: https://cinsight.etoday.co.kr/detail/00665676

- 8. 아시아경제: 상반기 부실채권 매각: https://cm.asiae.co.kr/article/2026021107275577119

- 9. 땅집고: NPL 매각 9조원 시대: https://realty.chosun.com/site/data/html_dir/2025/12/16/2025121603188.html

- 10. 한국금융신문: NPL 2025 딜 리뷰: https://www.fntimes.com/html/view.php?ud=2025123016500864086a663fbf34_18

- 11. Daum: 유암코 은행권 NPL 매입: https://v.daum.net/v/22JplUFYkv?f=p

- 12. 넘버스: 유암코 공모채: https://www.numbers.co.kr/news/articleView.html?idxno=11155