DEEP RESEARCH · NVIDIA FY26 Q4

NVIDIA FY2026 Q4 Conference Call Q&A Analysis

A reconstruction of the AI infrastructure supercycle, the Blackwell/Rubin roadmap, inference demand, and key risks

0. Bottom line first

I read FY2026 Q4 as the quarter that showed NVIDIA moving from a GPU supplier into an AI-infrastructure utility that manufactures intelligence. The core data points are revenue of $68.13bn, data-center revenue of $62.3bn, FY27 Q1 guidance of $78bn, and management’s argument that “compute equals revenues.”

Official fact: The source reviews NVIDIA’s FY2026 Q4 results announced on February 25, 2026 and the conference-call Q&A, tying AI overinvestment concerns to actual demand, supply, and product-roadmap evidence.

Interpretation: The near-term stock reaction reflected profit taking and China risk, but the numbers themselves point more to AI infrastructure demand being constrained by supply than to demand weakness.

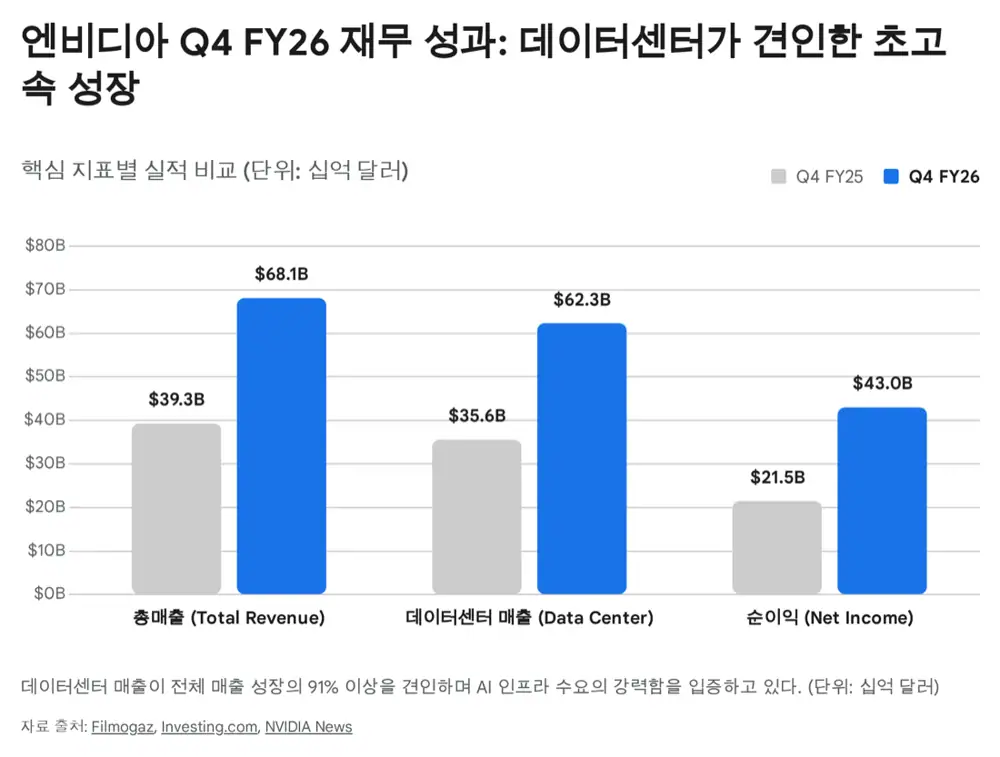

1. Financials: proof beyond expectations

NVIDIA’s FY26 Q4 exceeded Wall Street consensus across revenue, margins, cash flow, and next-quarter guidance. In the source’s framing, Morgan Stanley’s Joseph Moore called it one of the cleanest semiconductor “beat and raise” quarters, emphasizing the quality of the result rather than just the surprise.

| Metric | FY26 Q4 | FY26 Q3 | FY25 Q4 | YoY | Wall Street consensus |

|---|---|---|---|---|---|

| Total revenue | $68.13bn | $57.006bn | $39.331bn | Up 73.2% | $65.56bn |

| Data-center revenue | $62.3bn | $51.0bn | $35.6bn | Up 75% | $60.69bn |

| GAAP gross margin | 75.0% | 73.4% | 73.0% | Up 200bps | About 74.8% |

| Non-GAAP gross margin | 75.2% | 73.5% | 73.5% | Up 170bps | 75.0% |

| Non-GAAP EPS | $1.62 | - | $0.89 | Up 82% | $1.52-$1.53 |

| Free cash flow | $34.9bn | - | $15.5bn | Up 124% | - |

| FY27 Q1 guidance | $78bn, ±2% | - | - | - | $72.6bn |

Official fact: FY26 annual revenue was $215.94bn, up 65% year over year. Q4 data-center revenue of $62.3bn represented 91.4% of total revenue.

Core engine

Quarterly revenue was $62.3bn. Networking revenue was $11.0bn, up 263% year over year, or about 3.5x, and annual networking revenue exceeded $31.0bn.

Growth with supply pressure

Gaming revenue was $3.7bn, up 47% year over year. The source still notes several quarters of supply headwind as TSMC wafers and company resources concentrate on Blackwell.

Crossing $1bn

Professional Visualization rose 159% year over year to $1.3bn, crossing $1bn in quarterly revenue for the first time.

Next growth pool

Automotive revenue was $604mn, while the Physical AI ecosystem including robotics was framed as a $6bn annual contribution.

Profitability was also strong: Non-GAAP gross margin held at 75.2%, quarterly net income nearly doubled year over year to $43.0bn, and buybacks plus dividends for FY26 totaled $41.1bn.

2. Demand structure: three scaling laws

As important as the financials is Jensen Huang’s explanation of changing AI compute demand. The source separates demand into pre-training, post-training/reinforcement learning, and test-time compute.

Official fact: The source states that Blackwell, with the FP4 Transformer Engine and NVLink 72 switch, is designed to deliver 25x faster inference and 20x lower cost per token versus Hopper.

Interpretation: The concern that inference can migrate to cheap chips weakens as test-time compute grows. The longer a model thinks, the more inference becomes a large-cluster, software-optimized workload.

3. Product roadmap: Blackwell ramp and early Rubin

The source argues that NVIDIA’s lead comes from product design plus manufacturing and supply-chain execution. Blackwell is already in full production, with 9GW of infrastructure deployed and running at major CSPs and AI model companies.

Vera Rubin is described as combining next-generation HBM4 and high-speed switching to lower inference cost per token by up to 10x and improve performance per watt by 10x versus Blackwell. Compressing a typical two-year semiconductor generation cycle into one year reduces response time for AMD, Intel, and custom ASIC competitors.

4. Conference-call Q&A map

| Analyst | Question | Management answer |

|---|---|---|

| Vivek Arya, BofA | Cloud CapEx is nearing $700bn. Is this sustainable into 2027? | “Compute equals revenues.” Without compute there are no tokens and no growth; management is confident in customer cash-flow growth. |

| Joseph Moore, Morgan Stanley | What about rack-level bottlenecks and investments in Anthropic and the broader ecosystem? | Blackwell racks are complex 1.5mn-part systems, but 9GW is already operating. Ecosystem investment accelerates platform adoption. |

| Stacy Rasgon, Bernstein | What is the margin path and is there Blackwell/Rubin overlap risk? | Early ramp costs are pressure points, but long-term mid-70s gross margins are the goal. Both architectures can coexist. |

| Atif Malik, Citi | Does CUDA remain a moat as inference becomes a larger workload? | TensorRT-LLM depends on CUDA-based parallelization, and management cited up to 50x better performance per watt in inference. |

| Timothy Arcuri, UBS | What about custom ASIC competition and physical bottlenecks? | Generality is the weapon versus narrow ASICs. CUDA compatibility allows immediate model support, and TCO is central. |

| C.J. Muse, Cantor Fitzgerald | How do test-time compute and reinforcement learning change clusters? | Pre-training, post-training, and inference boundaries are blurring; Blackwell/NVLink 72 was designed for unified clusters. |

| Mark Lipacis, Evercore ISI | How diversified is growth beyond hyperscalers? | Enterprise is also growing about 2x. Management cited $30bn from sovereign AI and $6bn from Physical AI. |

| Harlan Sur, JPMorgan | What about GB300 ASP and supply constraints? | Demand should exceed supply all year. GB200/GB300 racks can expand both revenue and profit as high-value systems ship. |

4.1 CapEx and ROI debate

Vivek Arya’s question starts from concern that AI CapEx by the top cloud companies, including AWS, Microsoft, Alphabet, and Meta, is nearing $700bn this year and has risen $120bn above early-year expectations. Jensen Huang framed AI infrastructure not as a cost center, but as a revenue engine that produces tokens.

4.2 Ecosystem investment and Blackwell racks

Joseph Moore focused on whether the $10bn investment in Anthropic and capital deployed across OpenAI, CoreWeave, and the broader ecosystem are merely financial investments. The source reads them as a platform-lock-in strategy that increases adoption of CUDA and the newest chips. Annual FCF of $97bn is the ammunition behind that strategy.

4.3 Margins and architecture overlap

Stacy Rasgon asked about Non-GAAP gross margin of 75.2%, below prior high-75% levels, plus HBM3e and liquid-cooling ramp costs and the risk that Rubin fragments Blackwell demand. The CFO pointed to initial pressure, later recovery toward mid-70s margins, and coexistence of the two product generations.

4.4 Inference and CUDA

Atif Malik’s question addresses the risk that inference workloads invite lower-cost substitutes. Jensen Huang argued that TensorRT-LLM and CUDA optimization drive multi-GPU parallelization, response speed, and customer revenue. The source treats the 1.5mn modern AI models on Hugging Face being optimized for CUDA as a lock-in effect.

4.5 ASICs and unified clusters

Microsoft Maia, Google TPU, and Amazon Trainium remain structural risks. The source argues, however, that AI algorithm evolution outruns ASIC design and production cycles, and that cloud customers supporting diverse new open-source models prefer general GPU clusters as the safer asset.

4.6 Customer diversification and supply constraints

Mark Lipacis and Harlan Sur together expose the breadth of growth and the supply bottleneck. Enterprise demand is described as roughly doubling year over year, sovereign AI as $30bn, and Physical AI as $6bn. On supply, CoWoS and other bottlenecks constrain revenue upside, while management is said to imply more than $500bn of Blackwell/Rubin opportunity and a possible 20-30% ASP lift for GB300 systems.

5. Risks and the market-reaction paradox

The roughly 5-7% stock decline after earnings is better read as investor psychology and geopolitical risk than as a failure of the numbers. The source separates three risks.

Zero China revenue assumption

The FY27 Q1 $78bn guidance excluded China data-center compute revenue entirely. H20 and other China-specific chips, plus Huawei and other domestic competitors, remain risks.

Growth-rate pressure

At a quarterly revenue scale near $70bn, growth naturally slows from 100-200% to 70% or 50%. That is psychologically difficult for growth-stock multiples.

Portfolio imbalance

As wafers and company resources concentrate on Blackwell, gaming GPU supply can face structural headwinds.

Interpretation: China was historically a market with potential above 20% of revenue, so losing access is a long-term valuation discount. At the same time, issuing $78bn guidance while assuming zero China data-center compute revenue demonstrates the strength of non-China AI infrastructure demand.

6. Overall investment view

I read the quarter as evidence that the industrial paradigm is moving from software manually coded by humans to AI infrastructure where machines learn and reason. Hyperscaler CapEx anxiety is weakened by the token-economics logic that “compute equals revenues” and by test-time reasoning that can require more than 100x compute.

Near term, China export controls, small margin moves, base effects, and gaming supply sacrifice can create volatility. Still, the Blackwell ramp, early Vera Rubin introduction in H2 2026, and the vertically integrated CUDA/NVLink/Spectrum-X Ethernet ecosystem remain difficult for competitors to replicate.

The source argues that NVIDIA trades around 21x FY2026 earnings and 16x expected FY2027 earnings, which it does not view as excessive for a dominant AI infrastructure company. The key catalyst is conversion of the roughly $500bn supply-constrained opportunity cited by Morgan Stanley and Bank of America into high-priced GB300 and related system revenue.

My conclusion is that near-term profit taking and China-related corrections do not automatically imply a weaker fundamental story. This document is still a research note, and actual investment decisions should be made separately based on each investor’s risk tolerance and portfolio context.

Sources

- 네이버블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224198933506

- Source link 1: AI Concerns Among Factors Driving Nvidia Post-Earnings Selloff, BofA Says: https://news.futunn.com/en/post/69316407/ai-concerns-among-factors-driving-nvidia-post-earnings-selloff-bofa

- Source link 2: Nvidia CEO Jensen Huang Pushes Back On Fears Surrounding Big Tech's $700 Billion CapEx Surge: https://finviz.com/news/322791/nvidia-ceo-jensen-huang-pushes-back-on-fears-surrounding-big-techs-700-billion-capex-surge-compute-equals-revenues-in-the-new-ai-world

- Source link 3: NVIDIA Corporation (NVDA) Q4 2026 Earnings Call Transcript: https://seekingalpha.com/article/4874926-nvidia-corporation-nvda-q4-2026-earnings-call-transcript

- Source link 4: Nvidia Earnings Report Q4 2026: NVDA Beats Big, Stock Jumps to ...: https://www.filmogaz.com/168568

- Source link 5: NVIDIA (NVDA) Q4 2026 Earnings Call Transcript: https://www.fool.com/earnings/call-transcripts/2026/02/25/nvidia-nvda-q4-2026-earnings-call-transcript/

- Source link 6: Nvidia Beats by $2 Billion and Guides Higher but Wall Street Sells Anyway: https://247wallst.com/investing/2026/02/27/nvidia-beats-by-2-billion-and-guides-higher-but-wall-street-sells-anyway/

- Source link 7: NVIDIA Announces Financial Results for Fourth Quarter and Fiscal 2026: https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-fourth-quarter-and-fiscal-2026

- Source link 8: NVIDIA Q4 FY26 Earnings Discussion : r/AMD_Stock - Reddit: https://www.reddit.com/r/AMD_Stock/comments/1rekmto/nvidia_q4_fy26_earnings_discussion/

- Source link 9: Nvidia stock: Wall Street analysts stay bullish as traders balk: https://qz.com/nvidia-stock-earnings-ai-buildout-capex-jensen-huang

- Source link 10: NVIDIA Earnings Call: Jensen Huang Proclaims Arrival of AI Inflection Point: https://news.futunn.com/en/post/69254232/nvidia-earnings-call-jensen-huang-proclaims-arrival-of-ai-inflection

- Source link 11: NVIDIA Corporation (NVDA) Q3 2026 Earnings Call Transcript | Seeking Alpha: https://seekingalpha.com/article/4845855-nvidia-corporation-nvda-q3-2026-earnings-call-transcript

- Source link 12: Morgan Stanley Analysts Predict Strong Performance for Nvidia in Q4: https://www.binance.com/en/square/post/02-25-2026-morgan-stanley-analysts-predict-strong-performance-for-nvidia-in-q4-295357734640289

- Source link 13: Earnings call transcript: NVIDIA Q4 2026 beats expectations, stock rises - Investing.com: https://www.investing.com/news/transcripts/earnings-call-transcript-nvidia-q4-2026-beats-expectations-stock-rises-93CH-4526215

- Source link 14: NVIDIA's China AI Market Projections and Rubin Ramp Timeline Clash in Earnings Call | Bitget News: https://www.bitget.com/news/detail/12560605225837

- Source link 15: NVIDIA Corporation (NVDA) Q2 2026 Earnings Call Transcript | Seeking Alpha: https://seekingalpha.com/article/4817296-nvidia-corporation-nvda-q2-2026-earnings-call-transcript

- Source link 16: Nvidia (NVDA) Q4 2025 Earnings Call Transcript | The Motley Fool: https://www.fool.com/earnings/call-transcripts/2025/02/26/nvidia-nvda-q4-2025-earnings-call-transcript/

- Source link 17: Nvidia Q4 earnings: Can it push the AI trade higher — again? - Quartz: https://qz.com/nvidia-earnings-preview-q4-2026

- Source link 18: NVIDIA Corporation (NVDA) Discusses Rubin and Blackwell Performance Advancements and TPU Comparisons Transcript | Seeking Alpha: https://seekingalpha.com/article/4858585-nvidia-corporation-nvda-discusses-rubin-and-blackwell-performance-advancements-and-tpu

- Source link 19: 1NVDA - NVIDIA Corp Earnings Call Transcripts - Morningstar: https://www.morningstar.com/stocks/xmil/1nvda/earnings-transcripts

- Source link 20: Prediction: Nvidia Stock Will Soar to This Price in 2026 as the AI Boom Expands From Data Centers to Robotaxis | Nasdaq: https://www.nasdaq.com/articles/prediction-nvidia-stock-will-soar-price-2026-ai-boom-expands-data-centers-robotaxis

- Source link 21: Nvidia Stock Is Stuck, But JPMorgan Anticipates Another 'Beat-And-Raise' - Finviz: https://finviz.com/news/318536/nvidia-stock-is-stuck-but-jpmorgan-anticipates-another-beat-and-raise

- Source link 22: NVIDIA Corp. (NVDA): https://s201.q4cdn.com/141608511/files/doc_financials/2026/q4/NVDA-Q4-2026-Earnings-Call-25-February-2026-5_00-PM-ET.pdf

- Source link 23: Should You Buy the Dip in Nvidia Stock Today?: https://www.barchart.com/story/news/451531/should-you-buy-the-dip-in-nvidia-stock-today

- Source link 24: Nvidia's strong execution, guidance means growth concerns are 'overblown,' analysts say (NVDA:NASDAQ): https://seekingalpha.com/news/4557737-nvidias-strong-execution-guidance-means-growth-concerns-are-overblown-analysts-say

- Source link 25: Bank of America resets Nvidia price target after earnings: https://www.thestreet.com/investing/stocks/bank-of-america-resets-nvidia-price-target-after-earnings

- Source link 26: Nvidia Q4 2026 Earnings: Record $68.1B Revenue, Stock Drops on AI Outlook - News and Statistics: https://www.indexbox.io/blog/nvidia-reports-record-q4-2026-revenue-amid-market-skepticism/

- Source link 27: Can Nvidia's stock approach $400? Here's why earnings may mark the start of a big rally.: https://www.morningstar.com/news/marketwatch/2026021753/can-nvidias-stock-approach-400-heres-why-earnings-may-mark-the-start-of-a-big-rally

- Source link 28: Morgan Stanley and BofA Double Down on Nvidia Before Q4 Earnings - Gotrade: https://www.heygotrade.com/en/news/morgan-stanley-and-bofa-double-down-on-nvidia-before-q4-earnings