DEEP RESEARCH · CAMUS E&C

CAMUS E&C 2025 Q4: P.C Turnaround and SK Hynix Fab Value Chain

A research-style read-through of precast concrete, the Yongin semiconductor cluster, and easing PF risk

0. Bottom line first

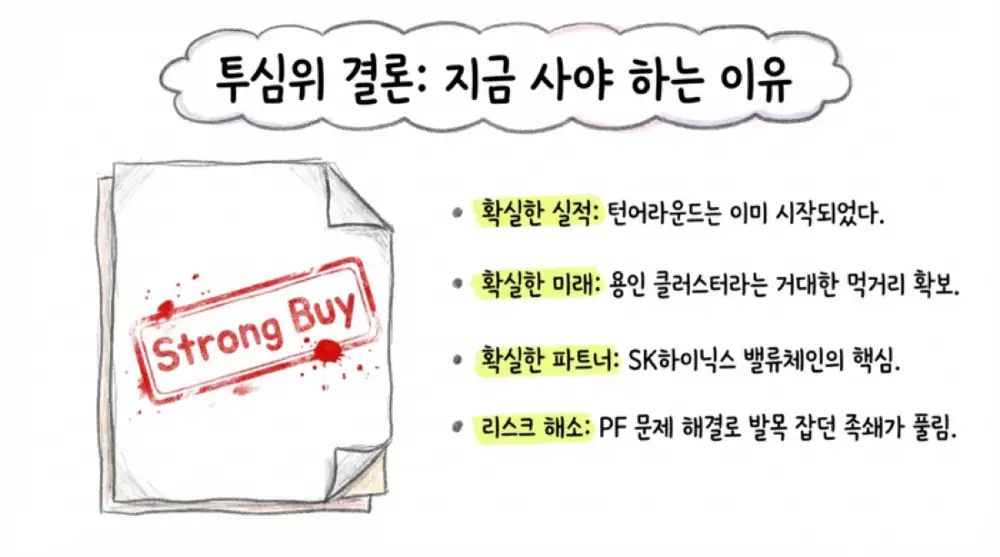

My core read is that CAMUS E&C is moving past the discount factors created by raw-material shocks and PF contingent liabilities, while entering a high-margin, large-order cycle tied to SK Hynix semiconductor fab precast-concrete work.

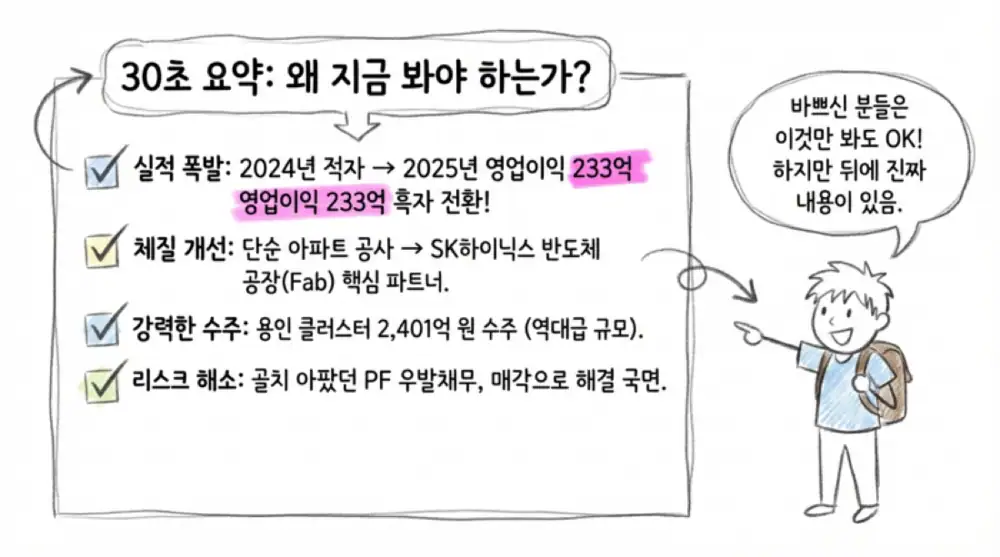

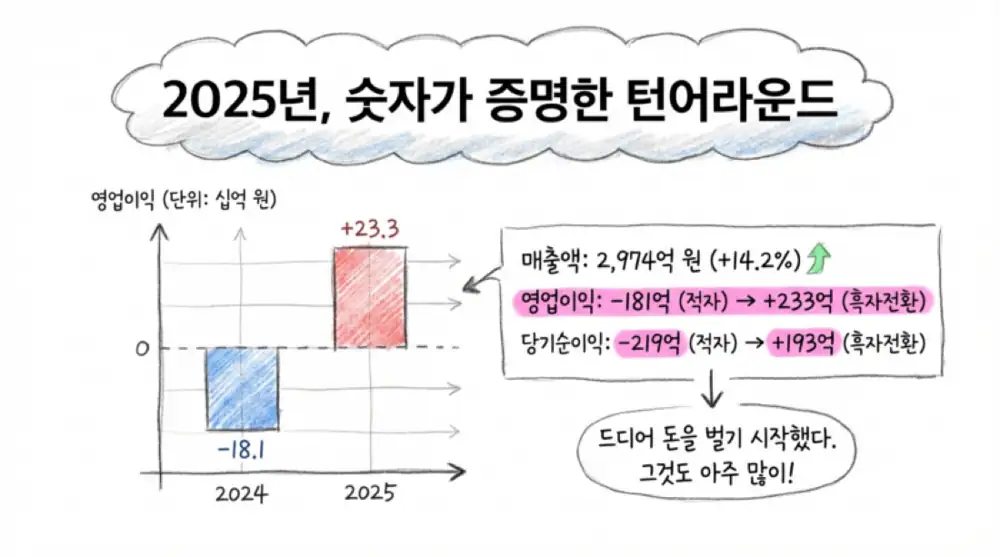

- 2025 preliminary consolidated revenue was KRW 297.4 billion, up 14.2% YoY.

- Operating profit was KRW 23.3 billion, turning from a KRW 18.1 billion loss in 2024; pre-tax profit was KRW 19.4 billion and net income KRW 19.3 billion.

- As of 2025 Q3, the P.C segment accounted for 83.4% of revenue and the construction segment for 16.6%.

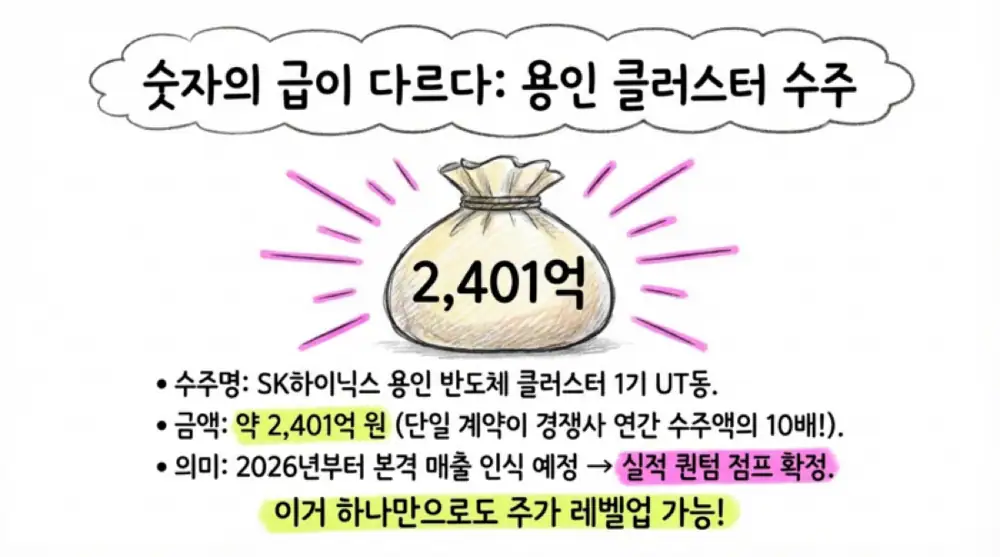

- The SK Hynix Yongin Semiconductor Cluster Phase 1 UT Building P.C work package disclosed in March 2025 is described in the source as about KRW 240.1 billion including VAT.

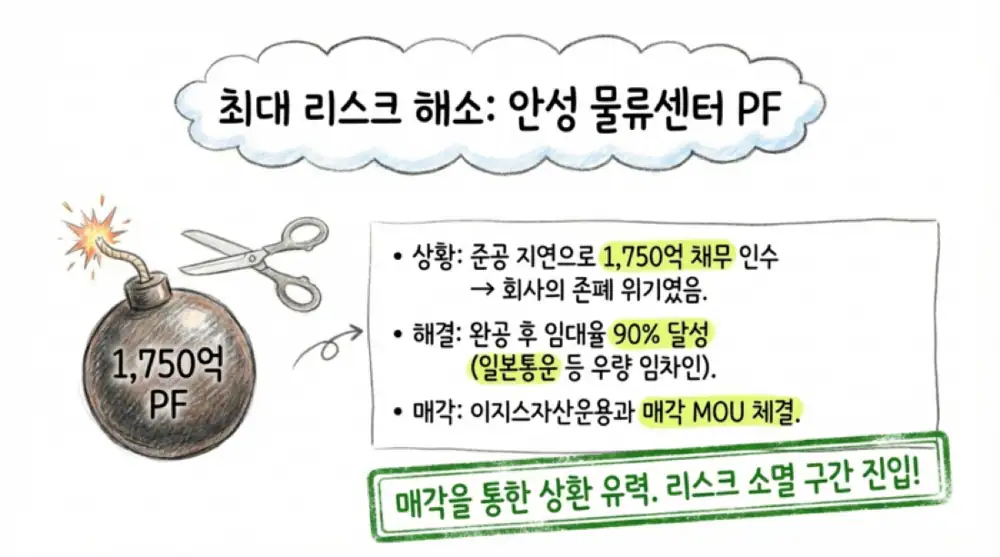

- The roughly KRW 175.0 billion Anseong Seongeun logistics-center PF debt-assumption risk from October 2024 is described as entering a resolution phase through above-90% occupancy and an IGIS Asset Management MOU.

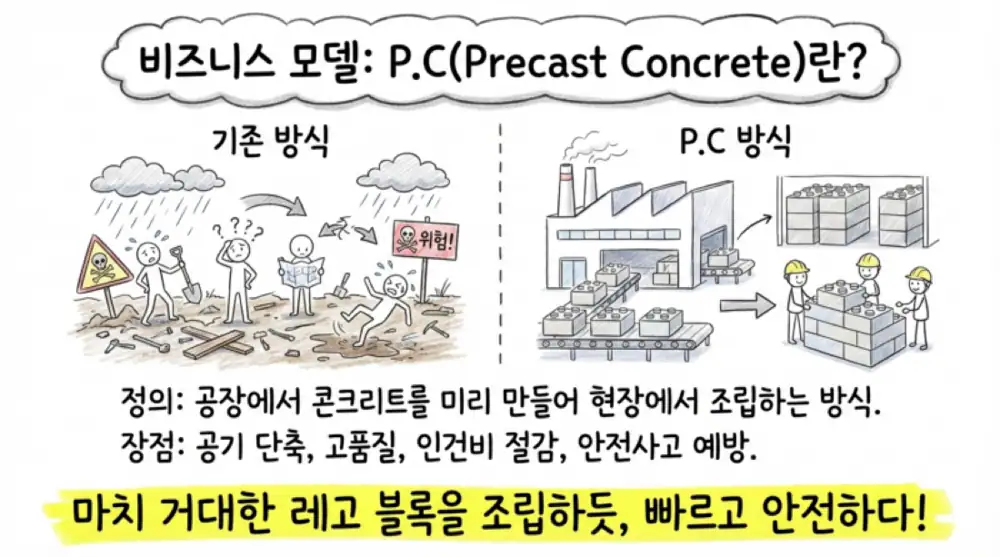

1. Business structure: high-tech transition in P.C construction

Official fact: CAMUS E&C was established in 1978 after importing industrialized construction technology from France’s Raymond Camus. It is a first-generation Korean company in P.C, or precast concrete, manufacturing and installation.

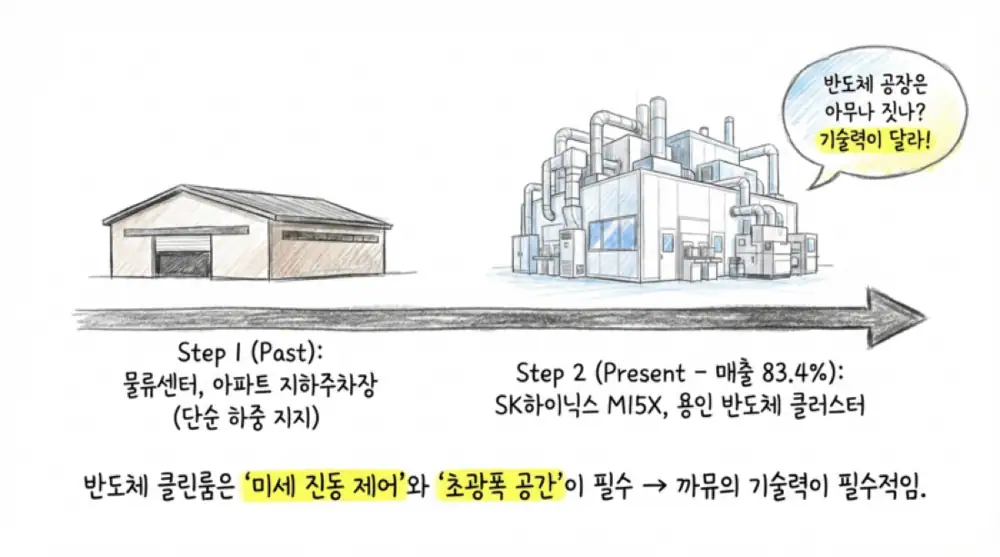

As of 2025 Q3 cumulative results, the P.C segment represented 83.4% of revenue and the construction segment, including public apartments and civil works, represented 16.6%. The source places the core equity-value driver overwhelmingly in the P.C business.

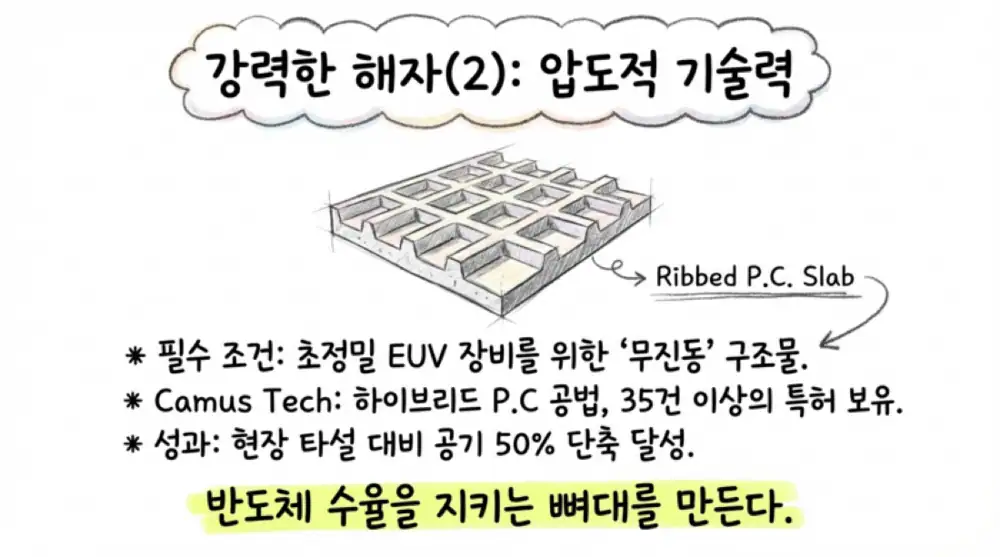

While P.C was historically used for logistics centers and apartment basement parking structures, the source argues that CAMUS E&C has been upgraded into a key vendor that produces and installs structural components for SK Hynix M15X and the Yongin semiconductor cluster. Cleanrooms require micro-vibration control and long-span space, making ultra-high-strength prestressed P.C members critical.

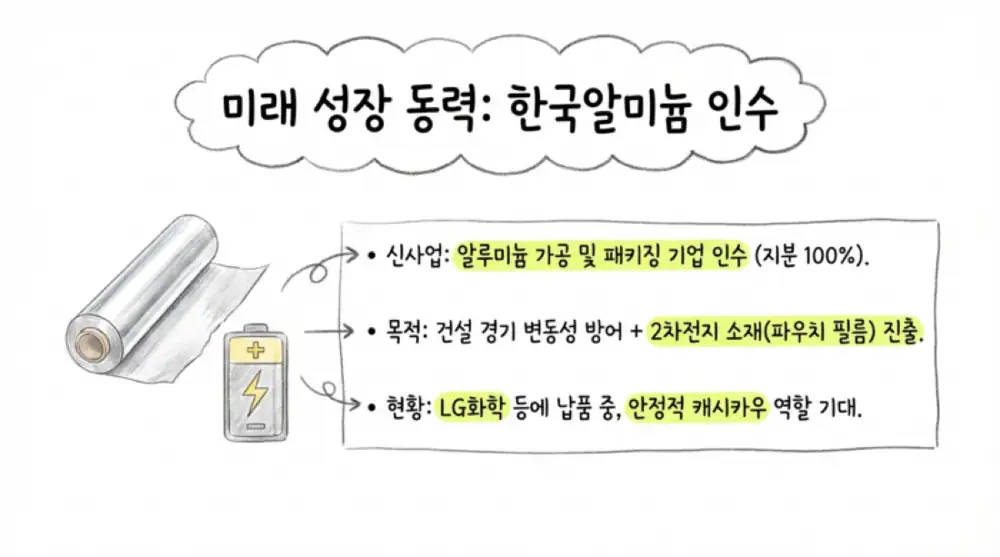

Korea Aluminum, acquired at 100% ownership in late 2023, operates secondary-battery LIB tab materials and pharmaceutical packaging businesses. The source breaks its revenue into 53.9% materials and 46.1% packaging.

2. Results: lost margin came back

Official fact: The 2025 preliminary consolidated results disclosed in February 2026 were revenue of KRW 297.4 billion, operating profit of KRW 23.3 billion, pre-tax profit of KRW 19.4 billion, and net income of KRW 19.3 billion. Operating profit turned from a KRW 18.1 billion loss and pre-tax profit from a KRW 21.5 billion loss in 2024.

| Metric | 2024 | 2025 preliminary | Read-through |

|---|---|---|---|

| Revenue | Prior-year base | KRW 297.4B | YoY +14.2% |

| Operating profit | -KRW 18.1B | KRW 23.3B | Large profit swing |

| Pre-tax profit | -KRW 21.5B | KRW 19.4B | Turned profitable |

| Net income | Loss | KRW 19.3B | Financial recovery |

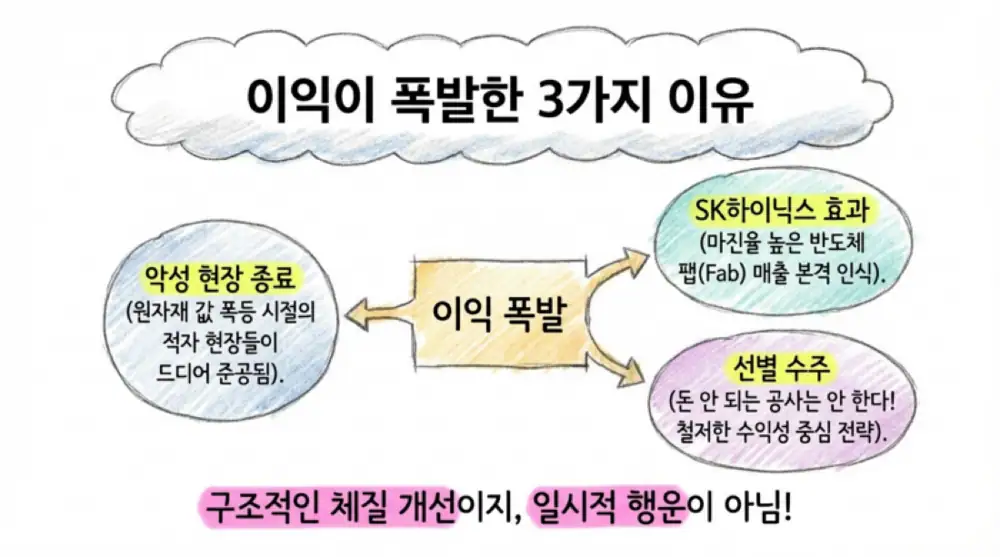

The improvement is attributed to three factors. First, loss-making fixed-price private construction projects from the 2021-2022 raw-material shock were mostly completed. Second, revenue recognition began in earnest for SK Hynix-related high-margin P.C work including Pyeongtaek P5, Cheongju M15X, and Yongin Cluster Phase 1. Third, management’s selective-order system focused on profitability rather than volume.

Interpretation: I read 2025 not as a one-off base effect, but as the beginning of a structural margin step-up in high-tech P.C. The next proof point is whether Yongin Semiconductor Cluster Phase 1 UT Building progress accelerates in 2026.

3. Cash flow: the harvest-phase pattern

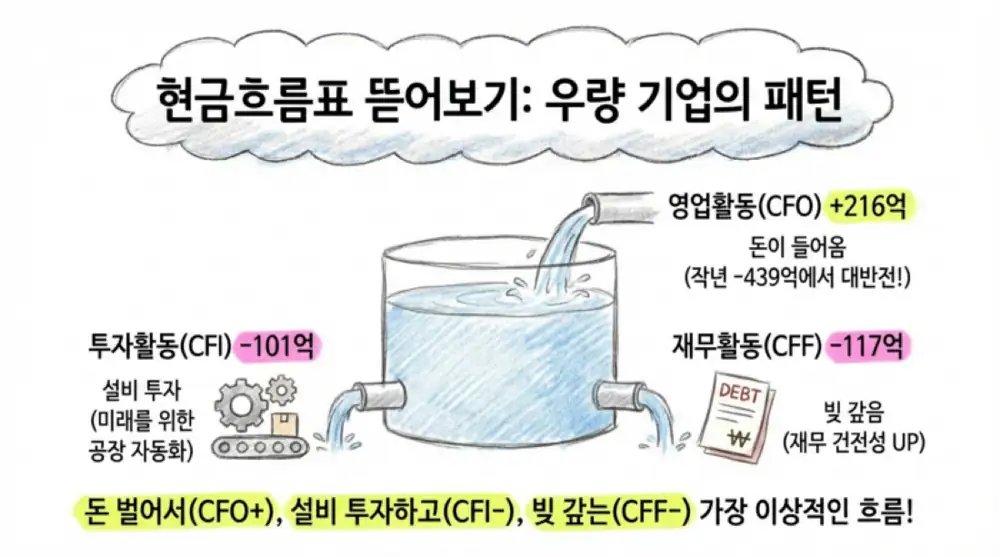

Official fact: 2025 Q3 cumulative operating cash flow was +KRW 21.6 billion, improving by more than KRW 65.5 billion from -KRW 43.9 billion in 2024 Q3 cumulative results.

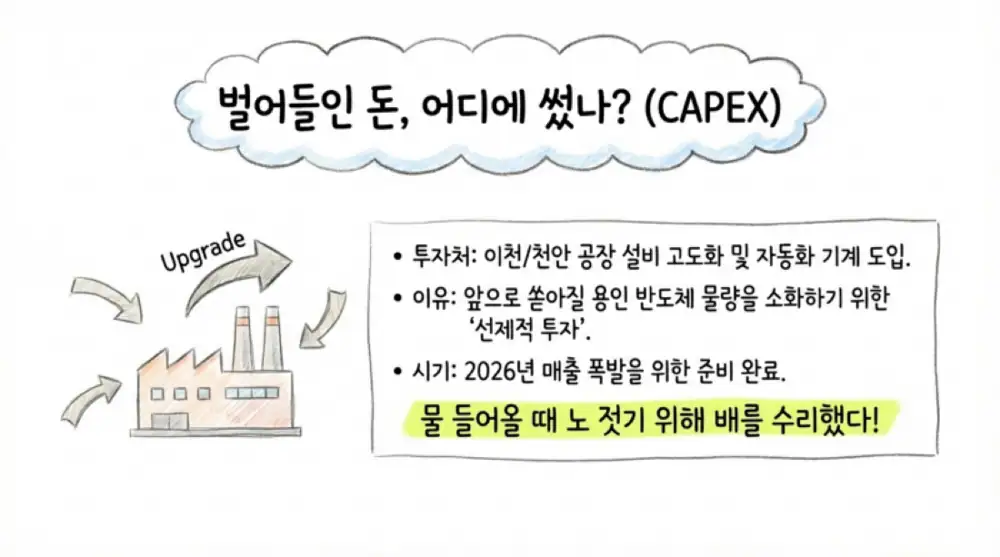

Investing cash flow was -KRW 10.1 billion. The source interprets this as CAPEX for the Icheon and Cheonan P.C plants: facility upgrades, layout improvements, and production automation. Financing cash flow was -KRW 11.7 billion, meaning repayment exceeded new borrowing.

Progress payments

Collection of construction receivables and progress payments from higher-quality projects turned core cash flow positive.

Productive CAPEX

Automation and capacity investment at Icheon and Cheonan are spending to handle semiconductor fab volumes.

Debt reduction

Net short-term debt repayment lightened the balance sheet.

Interpretation: The CFO(+), CFI(-), CFF(-) combination is the ideal harvest-phase pattern: core operations fund growth equipment and debt reduction at the same time.

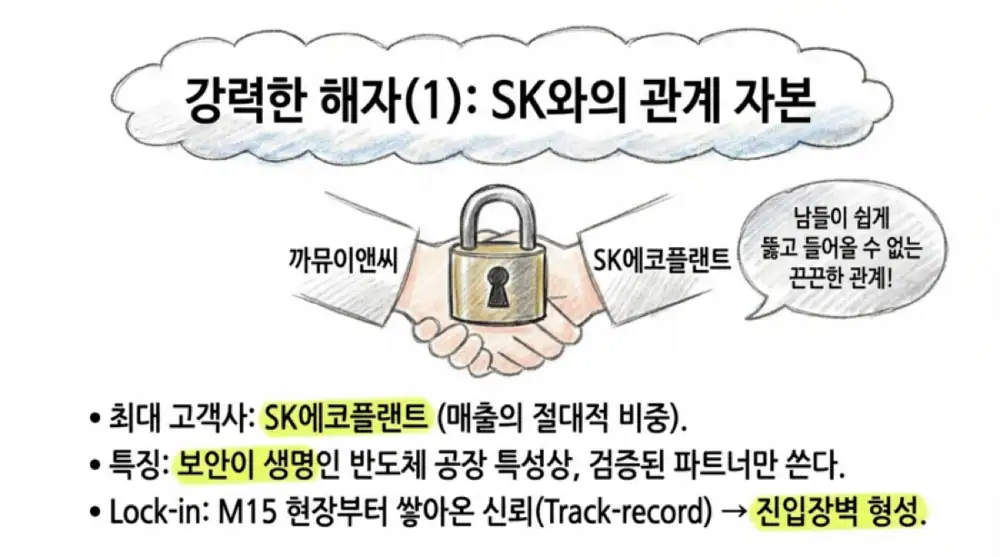

4. Moat: SK relationship capital, P.C technology, and OSC regulation

The key customer is SK Ecoplant, with SK Hynix’s next-generation fabs as the true end market. Fab construction costing tens of trillions of won requires security, schedule certainty, and coordination among many suppliers, making vendor replacement difficult once a track record is established.

Official fact: The source states that CAMUS E&C holds multiple Ministry of Land construction new technologies and more than 35 patents, including hybrid P.C column methods.

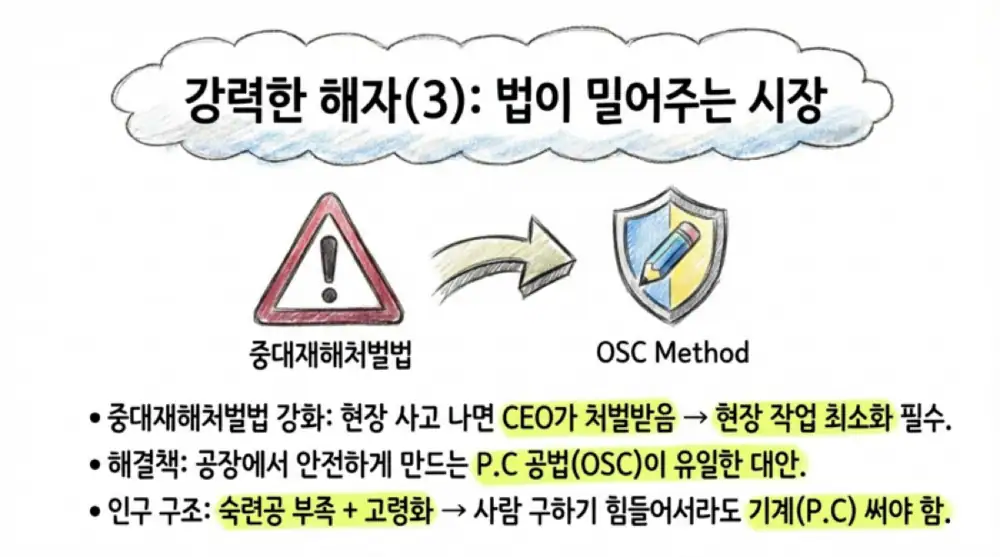

P.C members are manufactured in a controlled factory and assembled on site, reducing quality variance and shortening construction periods by up to 50%, according to the source. The Serious Accidents Punishment Act and aging construction labor force structurally support OSC, or Off-Site Construction, adoption.

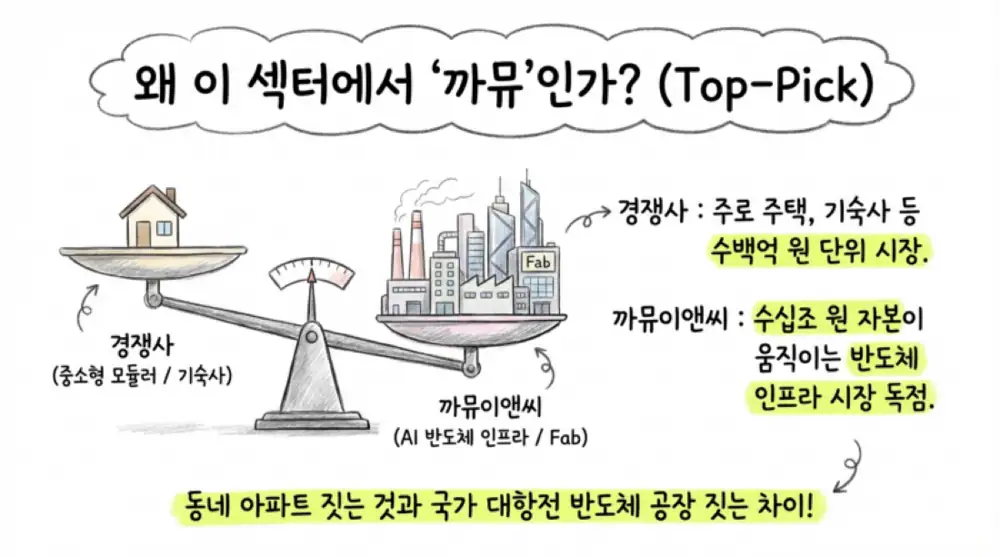

5. Why CAMUS E&C in the OSC sector

The source sees OSC as the main construction mega trend for the next three years. Skilled-labor shortages, aging workers, the Serious Accidents Punishment Act, ESG, and public-sector OSC adoption all push construction toward factory-made components.

Peer KC Industry is presented as focused on mid/small modular buildings such as military officer housing, rural renewal projects, and country homes, with about KRW 24.6 billion of 2025 orders. CAMUS E&C’s single Yongin Cluster Phase 1 UT Building P.C package is described by the source as about KRW 240.1 billion, making the scale comparison very different.

Interpretation: The capital-market point is not P.C itself but the quality of front-end CAPEX. CAMUS E&C is more exposed to AI semiconductor infrastructure than to small residential modular projects.

6. History, leadership, and financing

The company began as Samhwan Camus in 1978 and spent decades in public works, civil engineering, and LH apartment construction. In the 2020s it shifted toward a high-tech P.C specialist.

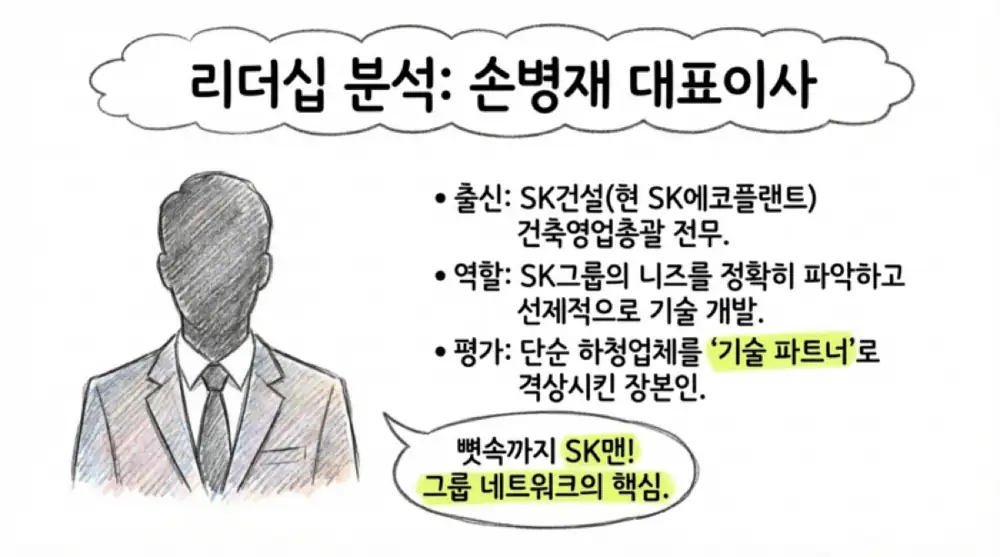

Official fact: CEO Byung-jae Son was born in 1964, studied business at Seoul National University, earned a Ph.D. in business from Sogang University, and received a real-estate master’s degree from Konkuk University, according to the source. He served as SK Construction’s executive in charge of building sales from 2004 to 2012, as an executive at SK Discovery, became CAMUS E&C CEO in May 2014, and also led Hunid from 2016 to 2019.

The source interprets Son’s SK Group network as relationship capital that helped CAMUS E&C win major projects such as Cheongju M15X and the Yongin semiconductor cluster.

| Timing | Financing type | Amount | Purpose and result |

|---|---|---|---|

| Dec. 2023 | Private bond, 44th tranche | KRW 15.0B | Used for about KRW 14.5B Korea Aluminum share acquisition; fully repaid in 2024 Q3 |

| Sep. 2024 | Third-party paid-in capital increase | About KRW 19.96B | Working/facility capital for raw-material inflation and Icheon P.C plant upgrades and automation |

The detailed mezzanine balance and conversion prices were not available in the provided source text, but the largest KRW 15.0 billion private bond is described as repaid in the cash-flow statement, reducing harmful interest-burden risk.

7. Shareholder structure and the SK ecosystem read

Official fact: As of February 5, 2026, total shares outstanding were 59,750,830 and the largest shareholder plus related parties held 53.66%, or 32,062,368 shares.

| Shareholder | Relationship | Shares | Stake |

|---|---|---|---|

| Base Co. | Controlling company | 26,728,957 | 44.74% |

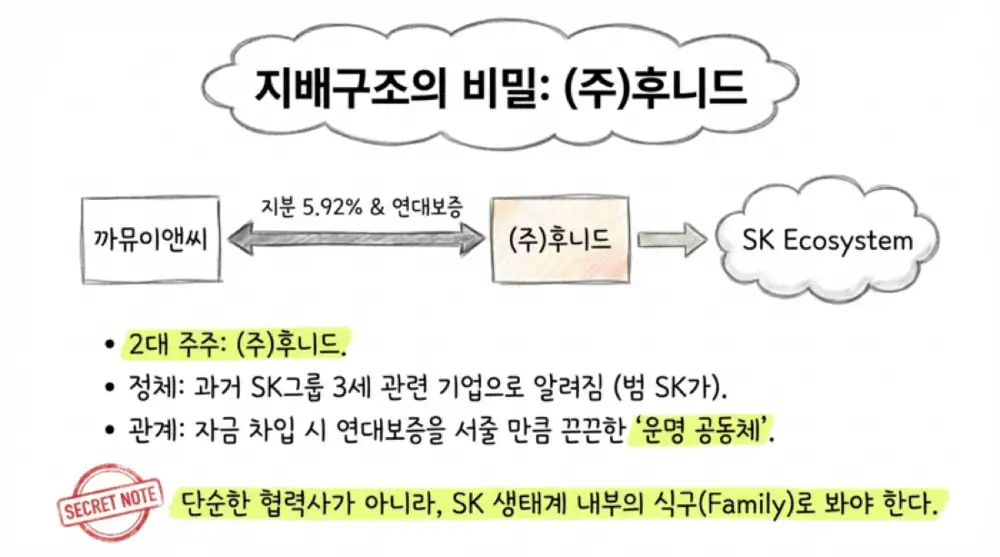

| Hunid | Affiliate | 3,539,781 | 5.92% |

| Keumyang International | Affiliate | 1,350,000 | 2.26% |

| Key executives | Byung-jae Son 0.17%, Chang-ho Kim 0.31%, Young-ae Kim 0.23%, Hwan-jin Choi 0.03% | - | - |

The source highlights Hunid, a related party with 5.92%, as a company previously covered in the media for its links to SK Group third-generation family members, and notes that Son was once Hunid CEO. It also states that Hunid provided a KRW 6.0 billion joint guarantee for CAMUS E&C borrowings, while CAMUS E&C pledged subsidiary investment assets for Hunid loans.

Interpretation: The source connects this governance and relationship network to the idea that CAMUS E&C functions as a friendly captive company inside the SK ecosystem. This should be tracked with a clear distinction between disclosed facts and interpretation.

8. Risks: PF debt and overhang

Official fact: In October 2024, failure to meet the completion obligation for the Anseong Seongeun logistics center caused about KRW 175.0 billion of PF loans to be transferred to CAMUS E&C through overlapping debt assumption, according to the source. This exceeded the company’s capital of about KRW 112.2 billion.

The completed logistics center is described as well-suited for automation, with 50-meter clear height and 7,000kVA receiving capacity. It secured strong 3PL tenants including Nippon Express and reached occupancy above 90%. IGIS Asset Management is described as handling asset management for the seller PFV while signing an acquisition MOU.

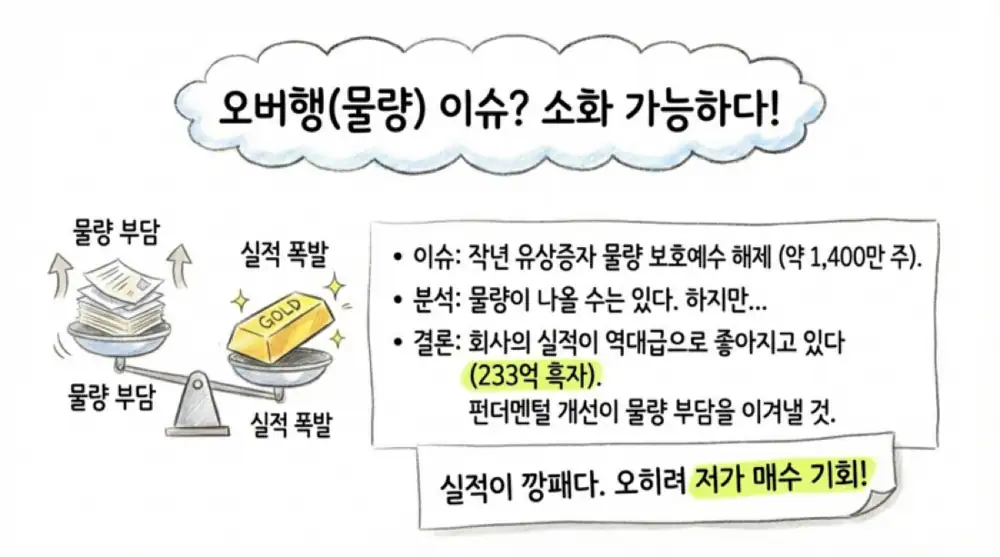

Official fact: In September 2024, the company issued about 14,598,550 new common shares through a third-party allotment, equivalent to about 24% of shares outstanding at the time. The one-year resale restriction expired on October 18, 2025.

Interpretation: Overhang is a textbook risk, but the source argues that 2025 operating profit of KRW 23.3 billion, 2026 SK Hynix project revenue recognition, and potential dividend resumption can help absorb the shares.

9. Final read

CAMUS E&C is moving from a builder exposed to construction cycles into a core P.C partner for SK Hynix semiconductor clusters. The 2025 results are the first strong signal that this transition is reaching the income statement and cash-flow statement.

One-line conclusion: the 2026 watch points are the speed of Yongin semiconductor-cluster P.C progress recognition, completion of PF debt resolution, and absorption of the capital-increase overhang. If all three align, the valuation discount can narrow quickly.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224195835978

- CAMUS E&C wins SK hynix Yongin cluster PC work - DigitalToday: https://www.digitaltoday.co.kr/news/articleView.html?idxno=556635

- CAMUS E&C SK hynix Yongin Cluster PC work disclosure - Hankyung: https://www.hankyung.com/article/202503116647L

- CAMUS E&C SK hynix contract amount increase - Finance Today: https://www.fntoday.co.kr/news/articleView.html?idxno=373800

- CAMUS E&C quarterly report - KRX: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20251114000458&docno=&viewerhost=&

- KC Industry 2025 PC modular orders - Hankyung: https://www.hankyung.com/article/202601064880O

- Korean builders OSC trends - KDB: https://file.kdb.co.kr/fileView?groupId=24988A2D-709F-0A12-C780-DDE888CFD135&fileId=EF956EB5-F0B9-391C-BF8D-3D9980A24119

- Regulatory reform for OSC construction - Ikld: https://www.ikld.kr/news/articleView.html?idxno=313706

- Anseong logistics-center PF debt relief signal - MarketIn: https://marketin.edaily.co.kr/News/ReadE?newsId=05300486642363096

- Anseong logistics-center debt assumption repayment plan - Stockplus: https://news.stockplus.com/m?news_id=13928865

- IGIS Anseong logistics-center 90% occupancy - Busan FN: https://busan.fnnews.com/news/202511061044254420

- IGIS pursues Anseong logistics-center acquisition - Corebeat: https://www.corebeat.co.kr/article/1102

- PF debt relief signal - Daum: https://v.daum.net/v/YbroBeFYIZ?f=p

- CEO Byung-jae Son profile - DeepSearch: https://www.deepsearch.com/analytics/people-analysis/%EC%86%90%EB%B3%91%EC%9E%AC/1964-08-15?p-symbol=KRX%3A013700

- Hunid-related PSPD press release: https://www.peoplepower21.org/economy/1632700