DEEP RESEARCH · DRB INDUSTRIAL

DRB Industrial: 2025 Earnings Surprise and the Rubber-Track Supercycle

A 4Q results report on OE lock-in, replacement rubber tracks, the Doosan Bobcat contract, deep value, and clean-cap-table risk

0. Bottom line first

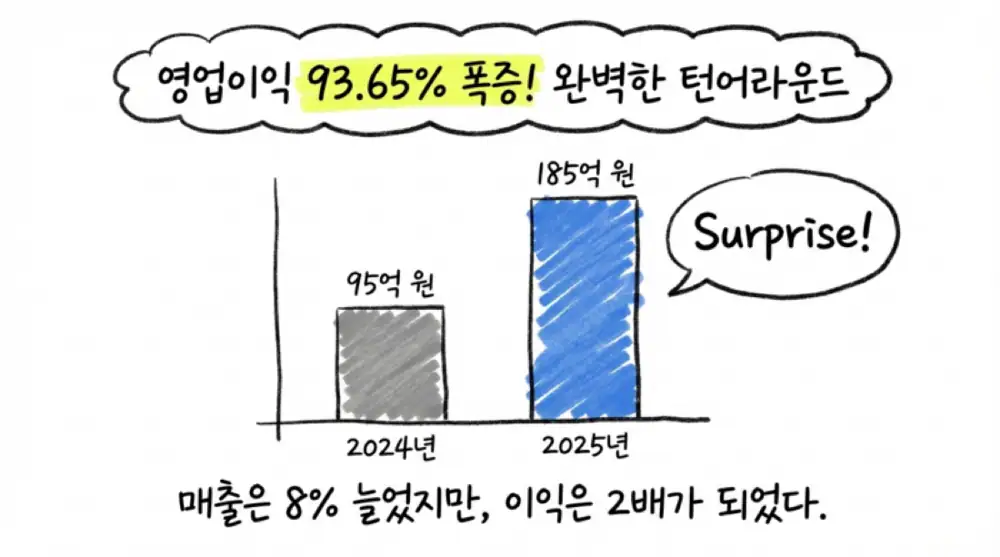

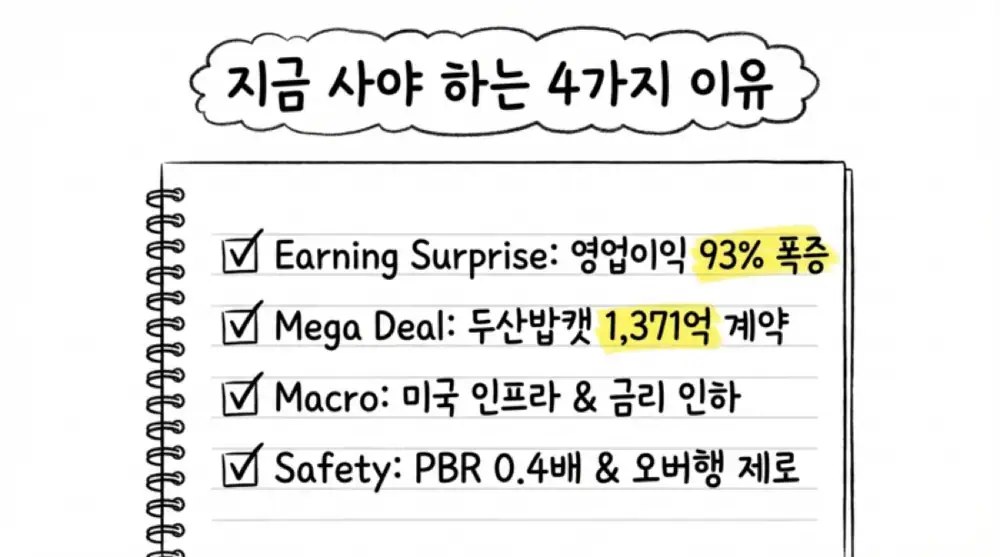

The key is not only KRW 18.56494B of 2025 operating profit, up 93.65% YoY. It is the structure behind that number: an OE-to-replacement rubber-track model, a KRW 137.15B Doosan Bobcat contract, and a clean capital structure with zero convertible-style overhang.

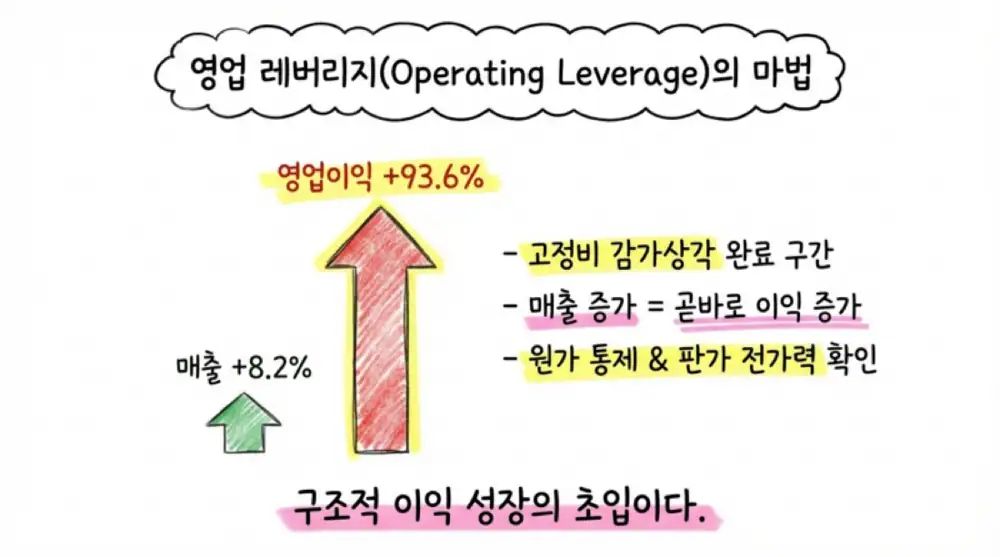

Official fact: The source cites 2025 consolidated revenue of KRW 364.6B, up 8.20% YoY, and operating profit of KRW 18.56494B, up 93.65% from KRW 9.58674B a year earlier.

Interpretation: Profit grew far faster than revenue, suggesting fixed-cost absorption, cost reduction, SG&A control, and pricing power with global customers.

1. Source Images

All 25 images attached to the source are preserved below. The original screenshots and tables should be checked in this sequence.

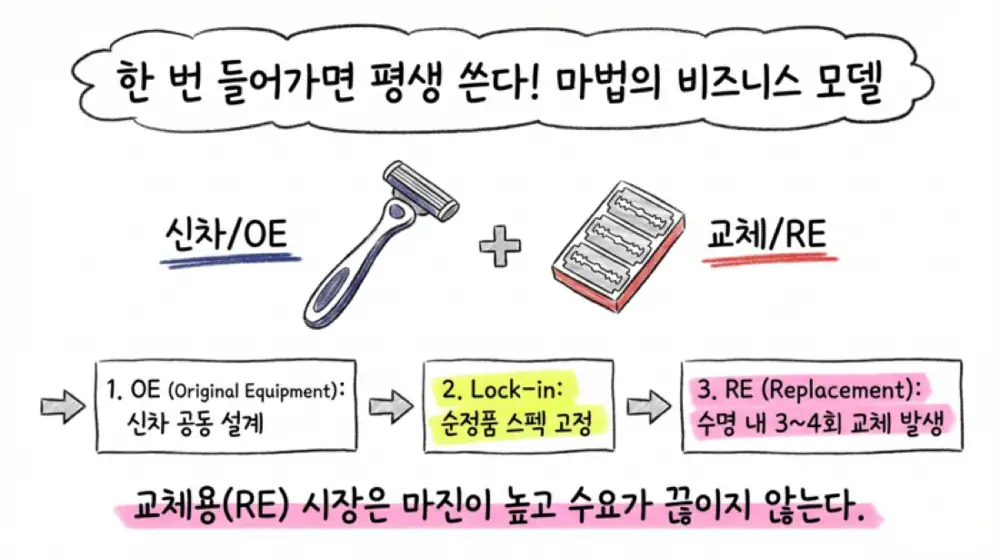

2. Business Model and Moat

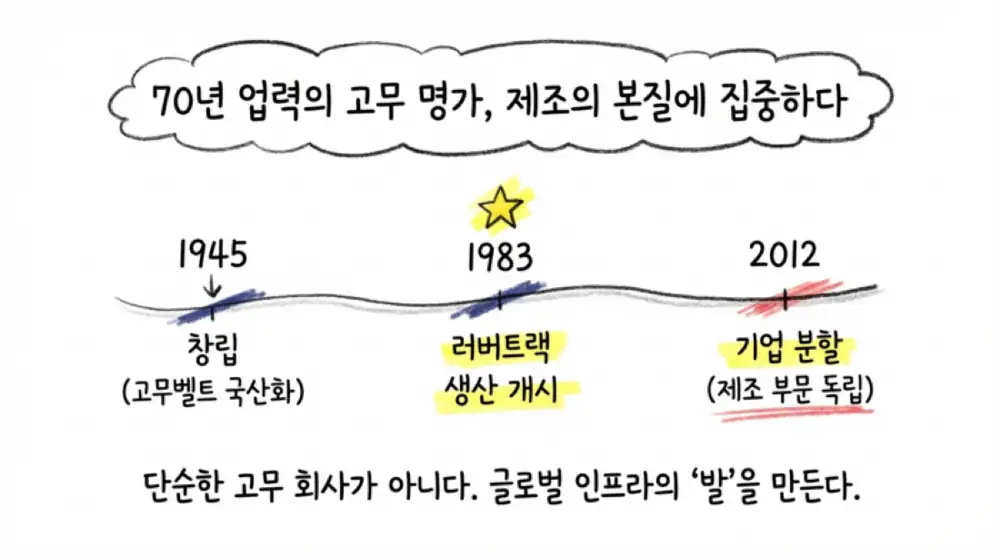

DRB Industrial was created on October 1, 2012 through the spin-off of the manufacturing business of the former Dongil Rubber Belt, now DRB Holding. Its business has two main pillars.

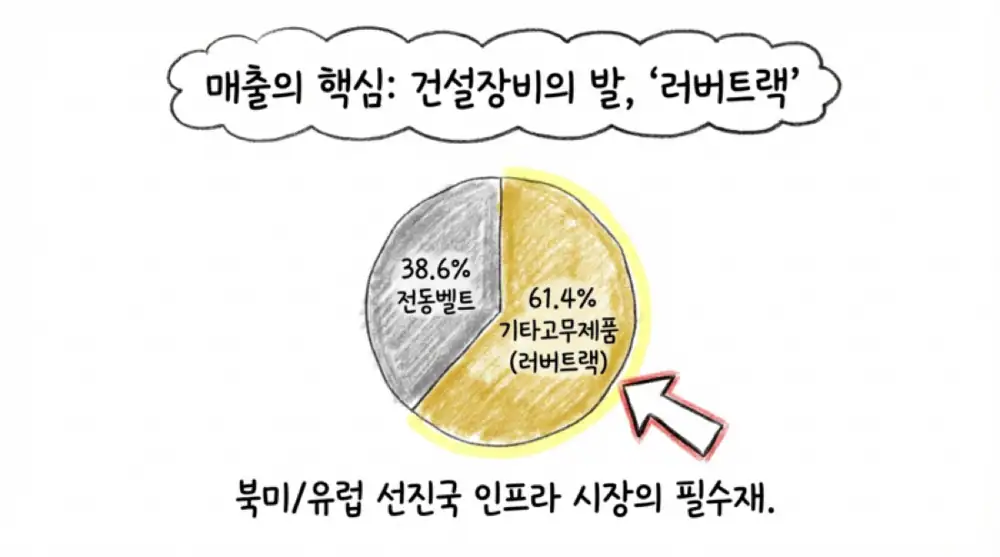

Other rubber products

Rubber tracks and pads for excavators, loaders, CTLs, and combines.

Rubber belts

Transmission belts for autos, agricultural machinery, appliances, and precision machinery, plus conveyor belts for production and logistics lines.

OE supply mix

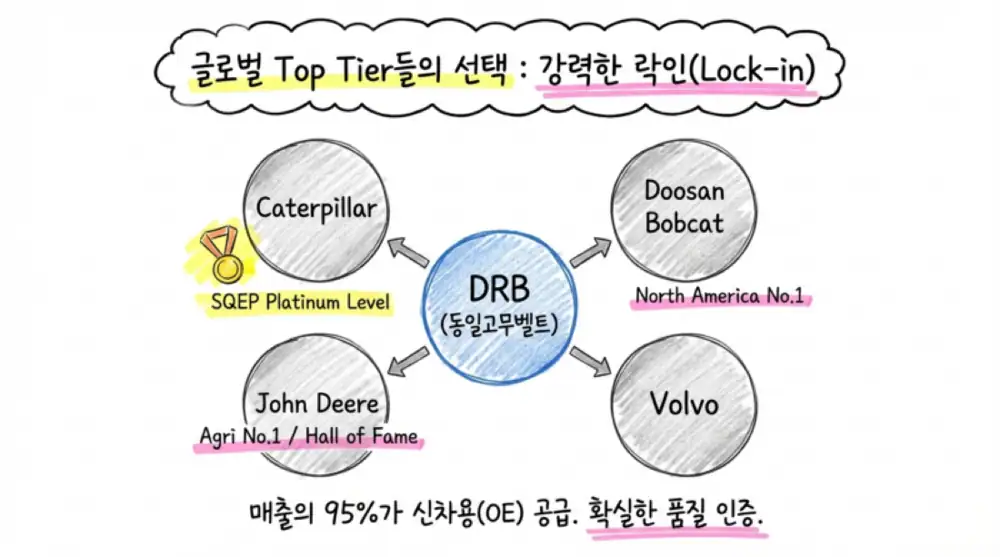

More than 95% of revenue comes from new-equipment OE supply, showing strong vendor positioning.

Official fact: The source names Caterpillar, Doosan Bobcat, John Deere, and Volvo CE as key customers, and mentions Caterpillar SQEP Platinum status plus John Deere Hall of Fame recognition for five consecutive years.

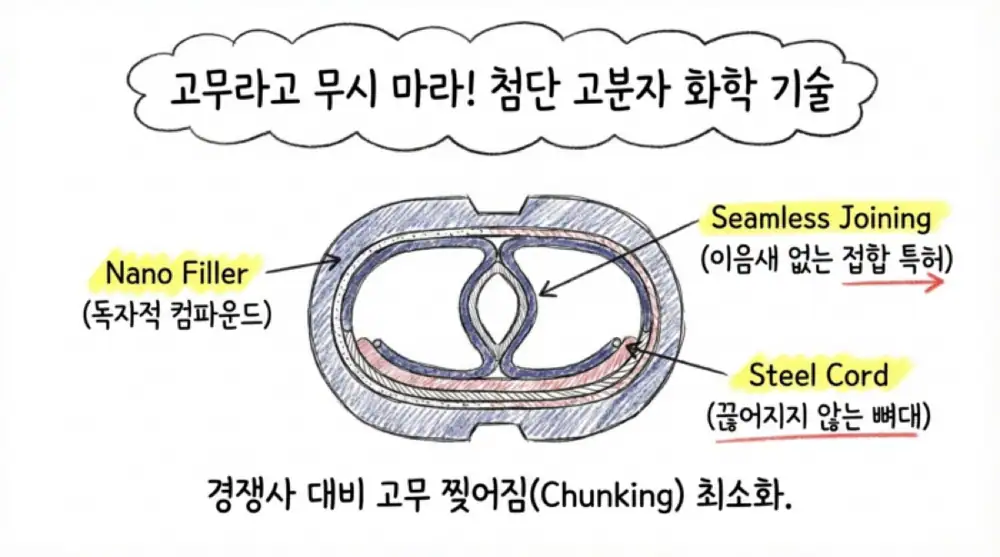

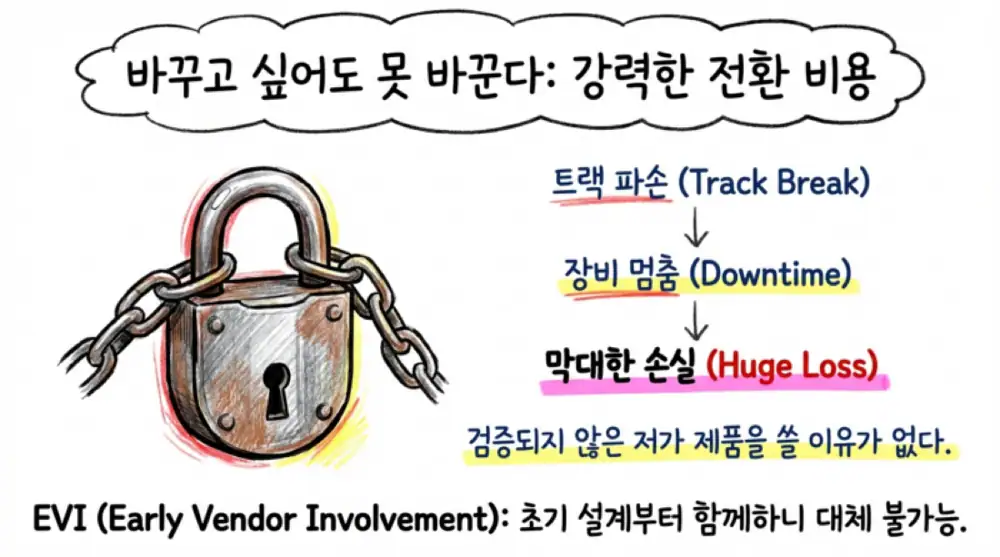

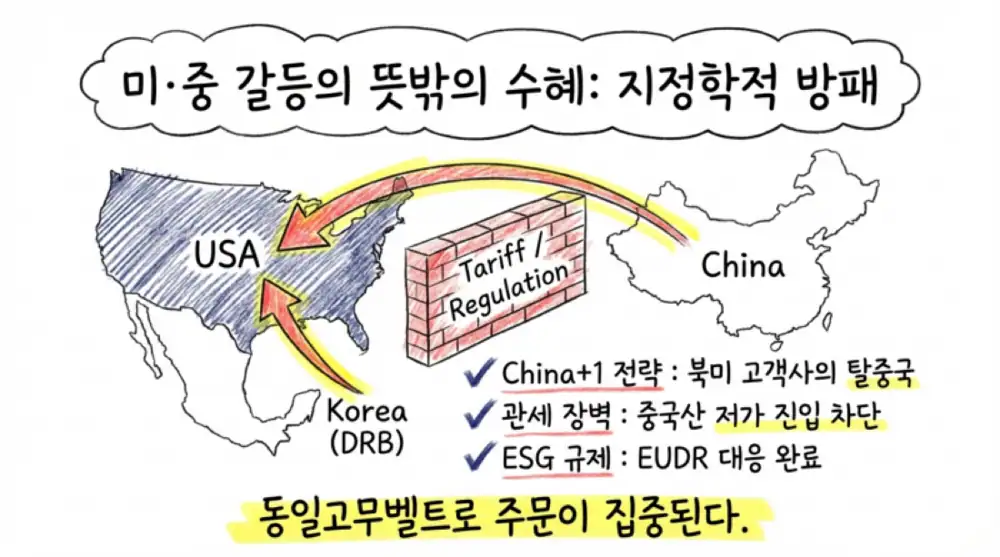

Interpretation: The moat is layered: nano-filler compounding and seamless steel-cord bonding, EVI-based customer lock-in, and North American supply-chain reshoring away from China.

3. Financials and Cash Flow

| Item | Source figure | How I read it |

|---|---|---|

| 2025 revenue | KRW 364.6B | Stable growth, +8.20% YoY |

| 2025 operating profit | KRW 18.56494B | +93.65% YoY, operating leverage visible |

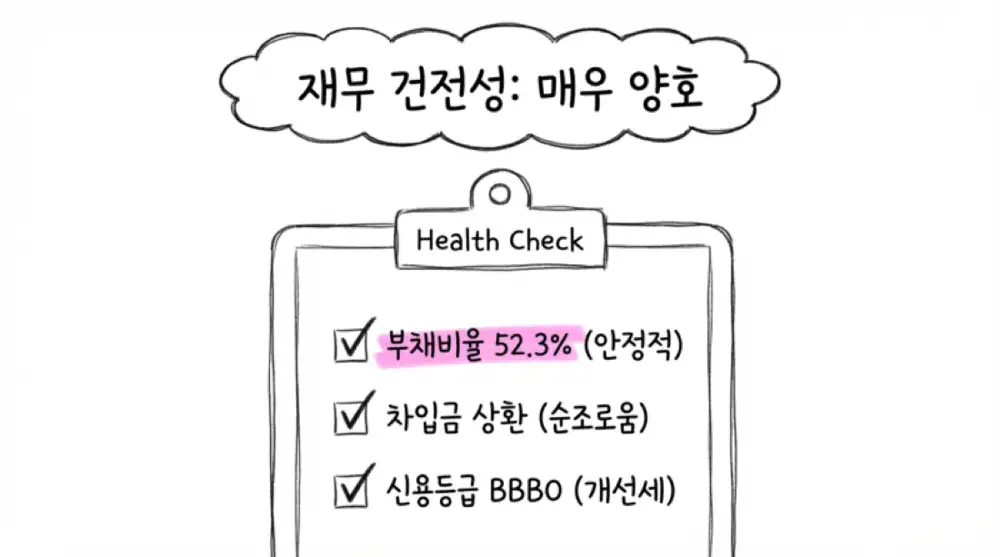

| Assets / liabilities / equity | KRW 355.3B / 125.2B / 239.0B | Debt-to-equity ratio of 52.3% |

| Credit rating | NICE Information Service BBB0 | Read as improving financial stability |

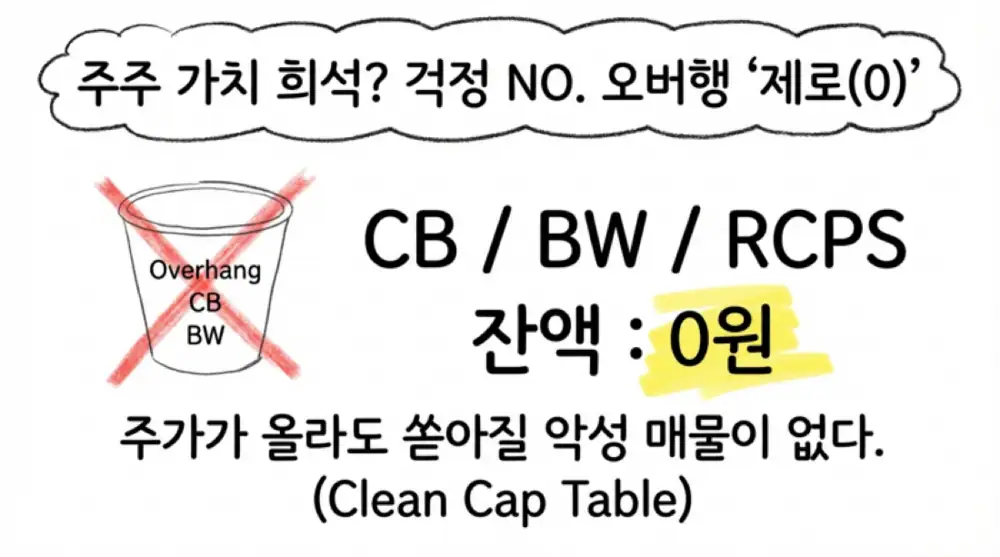

| Convertible balance | CB/BW/EB/RCPS KRW 0 | No dilution overhang in the source view |

| Capital / shares | KRW 6.95B / 13.9M shares | Clean cap table |

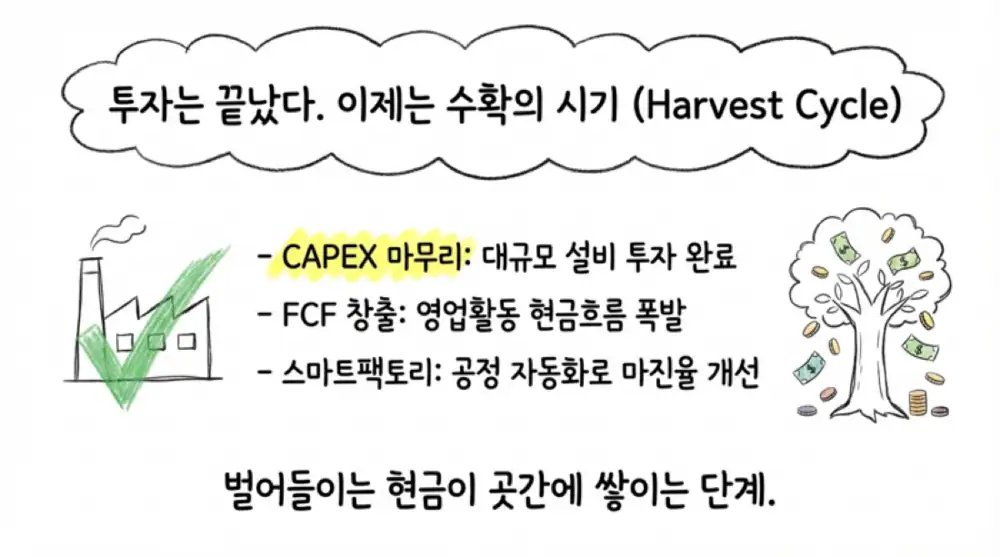

The source explicitly says detailed three-year cumulative CFO, CFI, and CFF figures could not be confirmed from public data. It instead cross-checks provisional results and 3Q summary financials to judge that the company is entering a harvest phase after capex.

Interpretation: The last two years of spending look more like old-equipment replacement, process automation, and smart-factory investment than aggressive new capacity expansion. The KRW 3.5B transfer from construction-in-progress and roughly KRW 6.7B of cumulative 3Q25 R&D show margin work and future preparation at the same time.

4. Macro and Sector Position

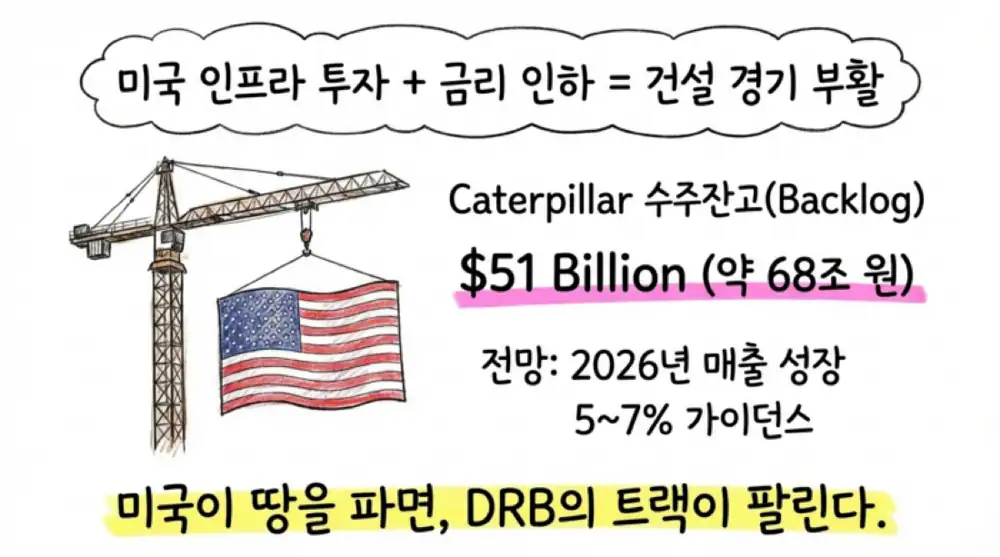

- U.S. infrastructure investment and potential rate cuts could stimulate compact construction equipment demand. The source cites Caterpillar's record year-end 2025 backlog of USD 51B, about KRW 68T, and 2026 sales growth guidance of 5~7%.

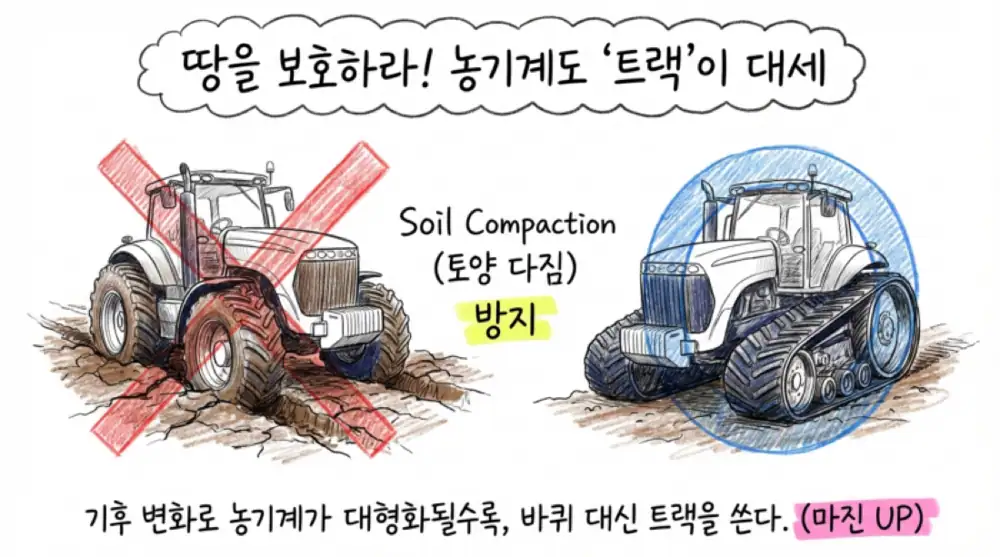

- Larger farm equipment and soil-compaction concerns support rubber-track adoption in 200 HP-plus tractors and combines.

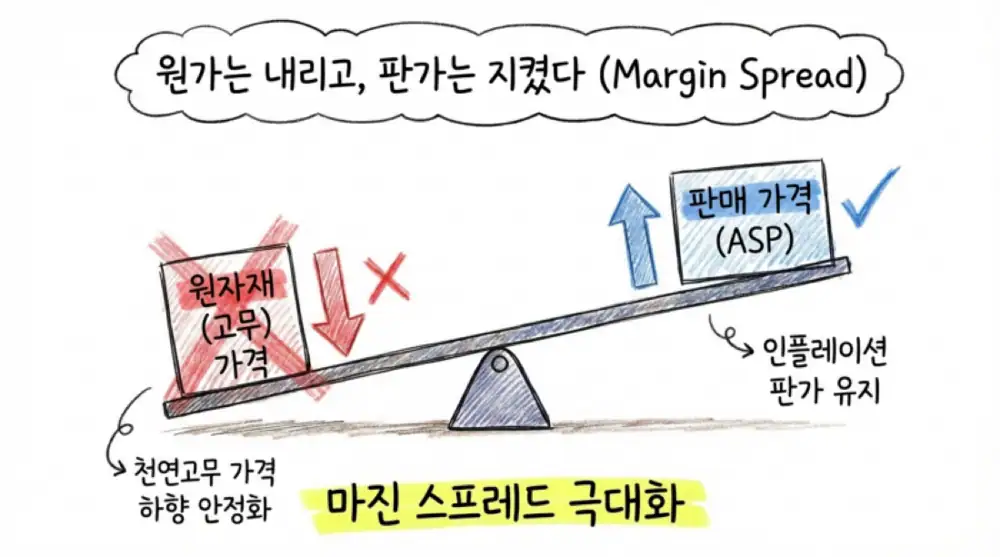

- The source assumes natural rubber stays in a CNY 14,000~18,000 per ton range in 2026 and synthetic rubber remains about 9.7% lower YoY, supporting margin-spread expansion.

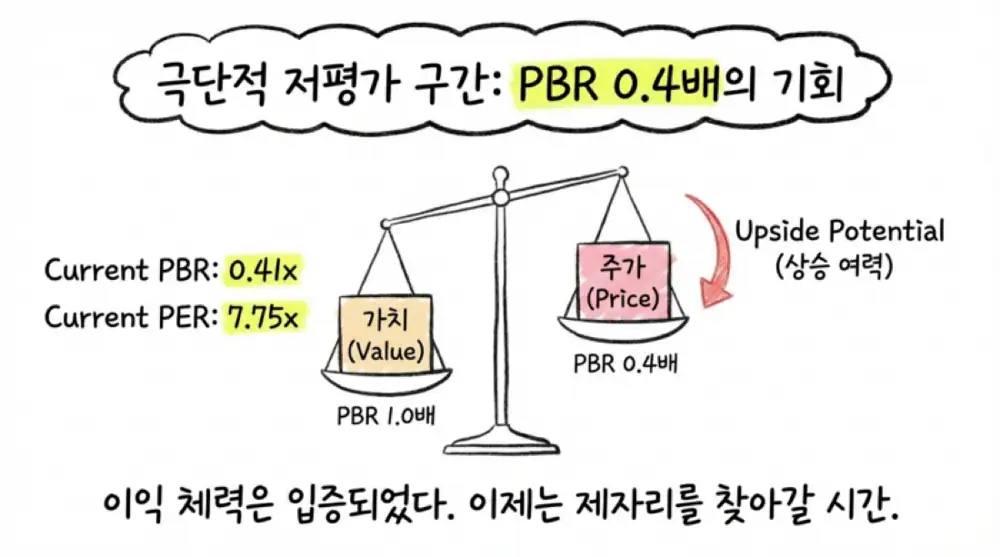

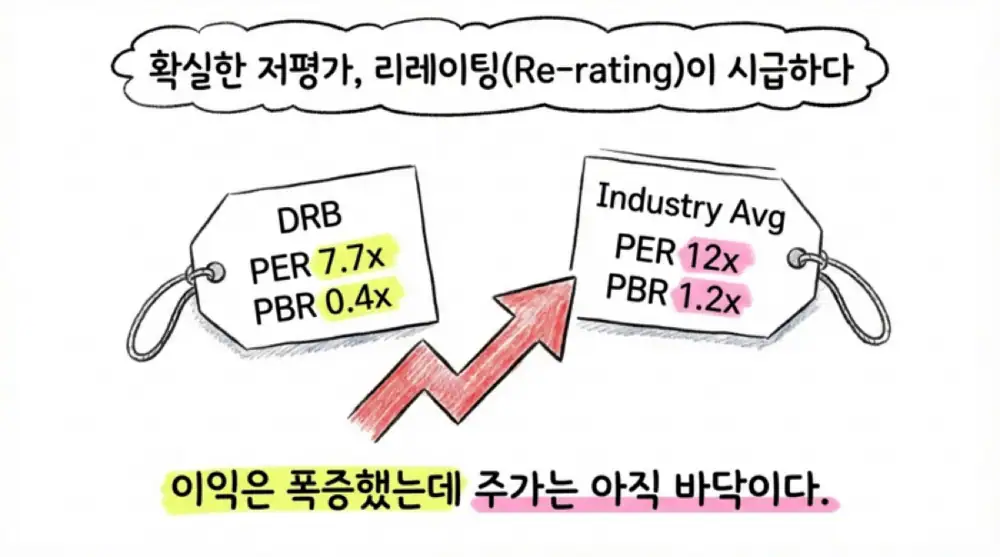

- Valuation is presented at PBR 0.41x and PER 7.75x, compared with ordinary construction-equipment parts companies at PBR 1.0~1.5x.

5. Shareholders, Investments, and Competition

| Topic | Key detail |

|---|---|

| Control | DRB Holding 44.13%, Kim Se-yeon 15.58%, Gochon Scholarship Foundation 4.05%, and friendly ownership of 69.78% |

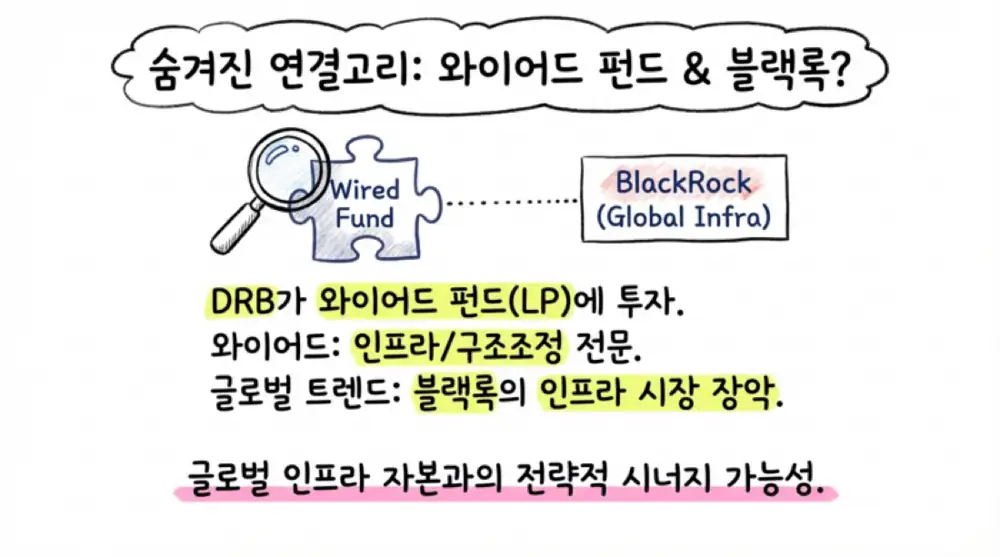

| Strategic investment | About KRW 9.7B in Wired Corporate Financial Stability PEF, 46.64% stake |

| New business investment | DRB Healthcare book value KRW 6.22B, 66.05% stake |

| Competitors | Bridgestone No. 1, DRB No. 2, Camso/Michelin in the No. 3 group, and McLaren, Mattracks, and Chinese players below |

The source also treats Kim Se-yeon's policy and global network, plus CEO Taniyama Ken's manufacturing and global-sales background after his March 2025 appointment, as part of the long-term competitive setup.

Interpretation: Chinese suppliers may offer 20~30% lower prices, but for construction machinery, downtime can create tens of millions of won of opportunity loss. That is why total cost of ownership matters more than sticker price.

6. Growth Points and Watchpoints

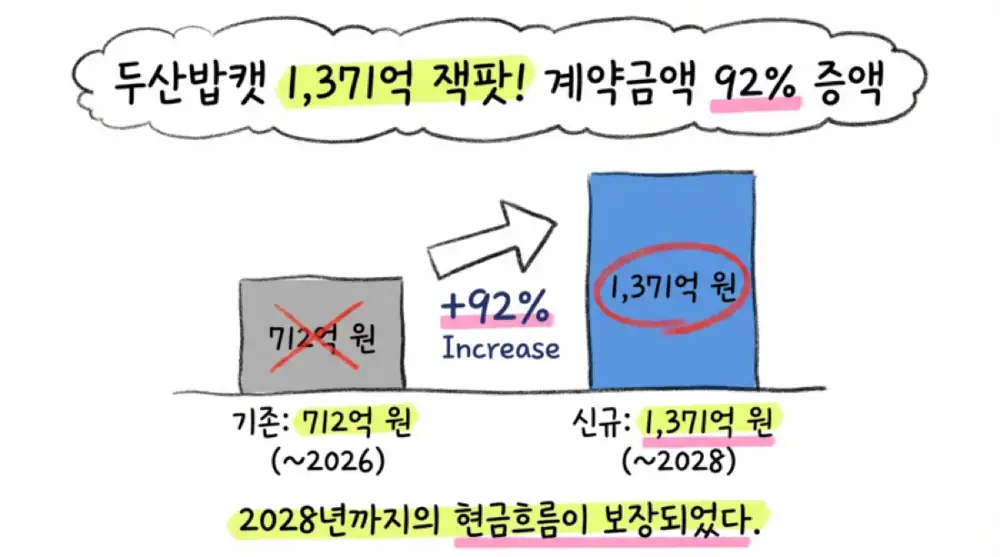

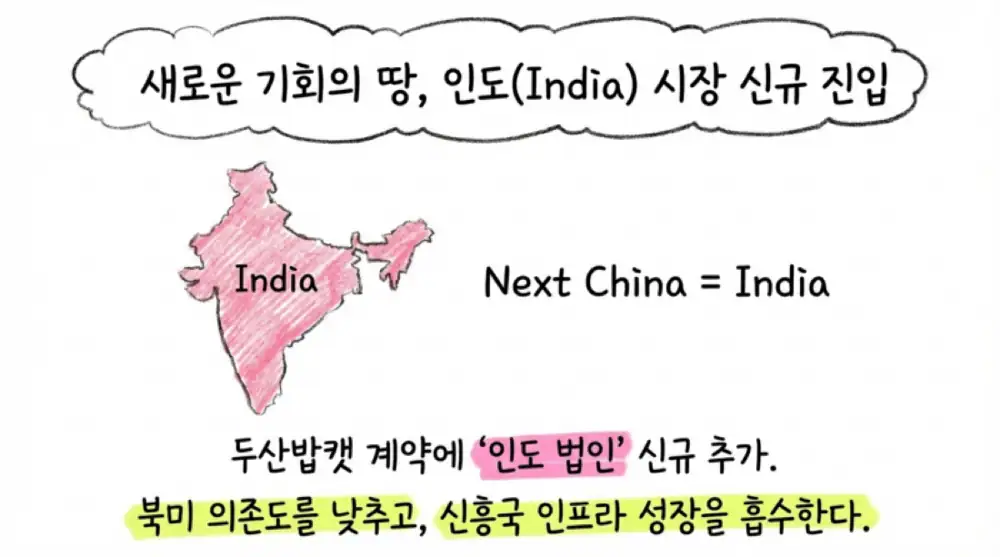

The Doosan Bobcat contract was expanded from KRW 71.2B ending September 2026 to KRW 137.15B ending December 2028, up about 92%, or roughly KRW 65.8B. The source says this equals 35.12% of 2022 revenue.

- The amended contract adds Doosan Bobcat India Private Limited alongside North America and EMEA, creating exposure to Indian infrastructure demand.

- Future growth areas include smart factories, 3D SLAM autonomous forklifts, data-driven urban vertical farms, and polymer-based flexible sensors.

- The source frames overhang risk as “zero,” but actual follow-up still needs the construction-machinery cycle, raw material prices, customer ordering timing, and new-business execution.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224195833406

- Source 2: https://www.kookje.co.kr/news2011/asp/newsbody.asp?code=0200&key=20240529.22010008535

- Source 3: https://www.datatooza.com/article/20260225161427748952ef3f6154_80

- Source 4: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250814002972&docno=&viewerhost=&

- Source 5: https://www.judal.co.kr/?view=stockAI&shareToken=w22Bn1RsoFpdfdnw

- Source 6: https://www.judal.co.kr/?view=stockAI&shareToken=42pcITm72LmD8yv8

- Source 7: https://www.judal.co.kr/?view=stockAI&shareToken=EPXiDmr5vLPVj1pc

- Source 8: https://www.judal.co.kr/?view=stockAI&shareToken=iS0RVjSeSDo2db4H

- Source 9: https://www.drb-industrial.com/industrial/index.php?pCode=MN0000008

- Source 10: https://ko.wikipedia.org/wiki/%EB%8F%99%EC%9D%BC%EA%B3%A0%EB%AC%B4%EB%B2%A8%ED%8A%B8

- Source 11: https://www.drb-industrial.com/industrialen/index.php?pCode=MN0000017

- Source 12: https://market.us/report/global-rubber-track-market/

- Source 13: https://www.sunsirs.com/uk/detail_news-28150.html

- Source 14: https://www.globalepic.co.kr/view.php?ud=202601141033397445ebfd494dd_29

- Source 15: https://www.biztribune.co.kr/news/articleView.html?idxno=349084

- Source 16: https://seekingalpha.com/news/4544371-caterpillar-anticipates-sales-growth-near-top-of-5-percentminus-7-percent-range-in-2026

- Source 17: https://www.marketsandmarkets.com/ResearchInsight/rubber-track-market.asp

- Source 18: https://www.marketsandmarkets.com/Market-Reports/rubber-track-market-236156766.html

- Source 19: https://www.echemi.com/cms/2782479.html

- Source 20: https://tradingeconomics.com/commodity/synthetic-rubber

- Source 21: https://www.360iresearch.com/library/intelligence/rubber-track-system

- Source 22: https://dataintelo.com/report/global-rubber-tracks-for-construction-machinery-market

- Source 23: https://www.weforum.org/people/kim-seo-yeon/

- Source 24: https://www.belfercenter.org/event/4th-korean-security-summit-harvard-korea-oracle-global-trends

- Source 25: https://www.privateequityinternational.com/institution-profiles/wired-partners.html

- Source 26: https://thevc.kr/wiredpartners

- Source 27: https://www.blackrock.com/corporate/newsroom/press-releases/article/corporate-one/press-releases/blackRock-agrees-to-acquire-global-infrastructure-partners

- Source 28: https://www.kedglobal.com/alternative-investments/newsView/ked202111040021

- Source 29: https://www.youtube.com/watch?v=b_9qOHBn-HM

- Source 30: https://www.researchandmarkets.com/reports/6223033/rubber-track-market-report-trends-forecast

- Source 31: https://reports.valuates.com/market-reports/QYRE-Auto-36N1272/global-rubber-tracks