DEEP RESEARCH · KBI GROUP

KBI Group: Environmental Cash Cow, Savings-Bank Acquisitions, and KBI Metal as Top Pick

A group-level capital-allocation report centered on unlisted KBI Gukinsanup and the next three-year top-pick thesis.

0. Bottom line first

My read is that KBI Group has used the environmental cash cow of waste treatment and steam sales to support manufacturing, and in 2025 made a major bet by re-entering finance through Raon Savings Bank and Sangsangin Savings Bank. In that transition, the source narrows the group top pick to KBI Metal.

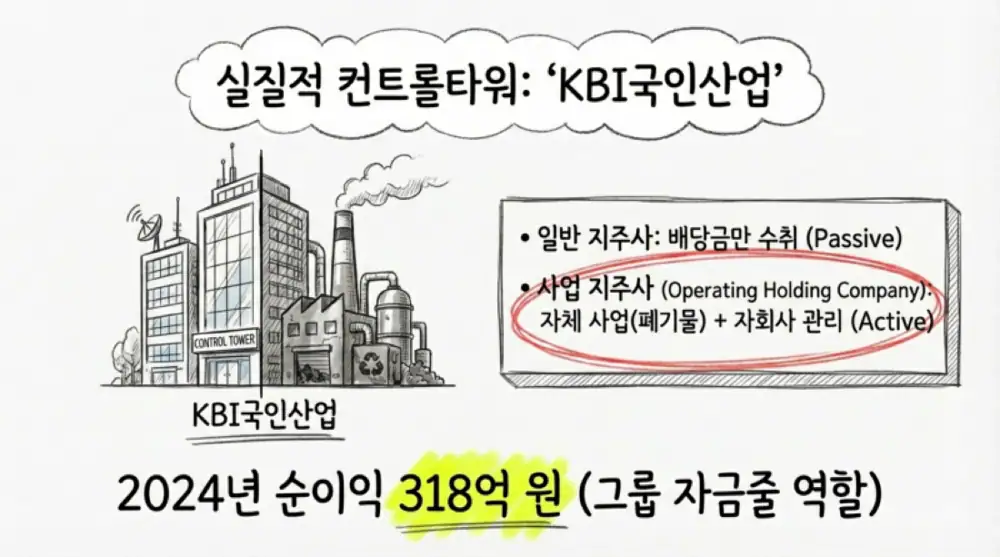

Official fact: The source says KBI Gukinsanup recorded KRW 383.6 billion in total assets, KRW 61.1 billion in revenue, and KRW 31.8 billion in net income at end-2024. KBI Group acquired 90.01% of Sangsangin Savings Bank for KRW 110.7 billion on October 31, 2025, and bought 60% of Raon Savings Bank for about KRW 10 billion in July 2025.

Interpretation: The group-level risk is savings-bank NPL cleanup and BIS-ratio normalization. The source sees the relatively independent listed momentum in KBI Metal, Korea’s No. 1 JCR copper-rod player.

1. Source images and governance

All source attachment images are preserved below. The following sections separate the holding company, manufacturing affiliates, and financial-acquisition risk.

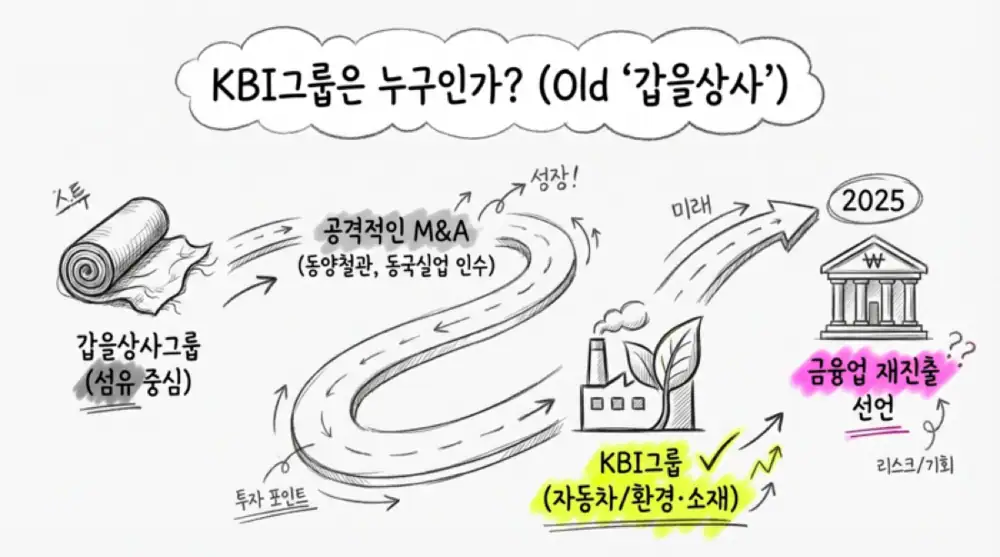

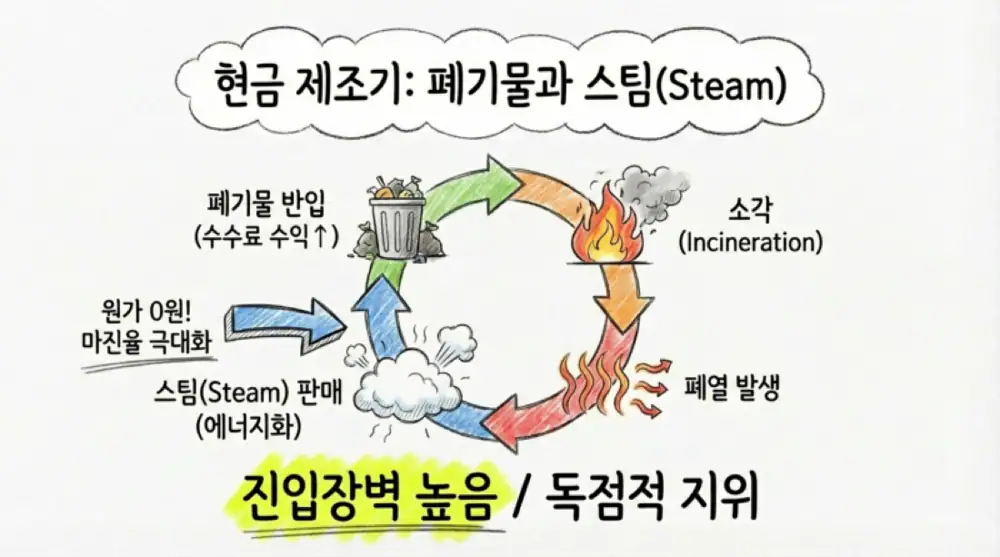

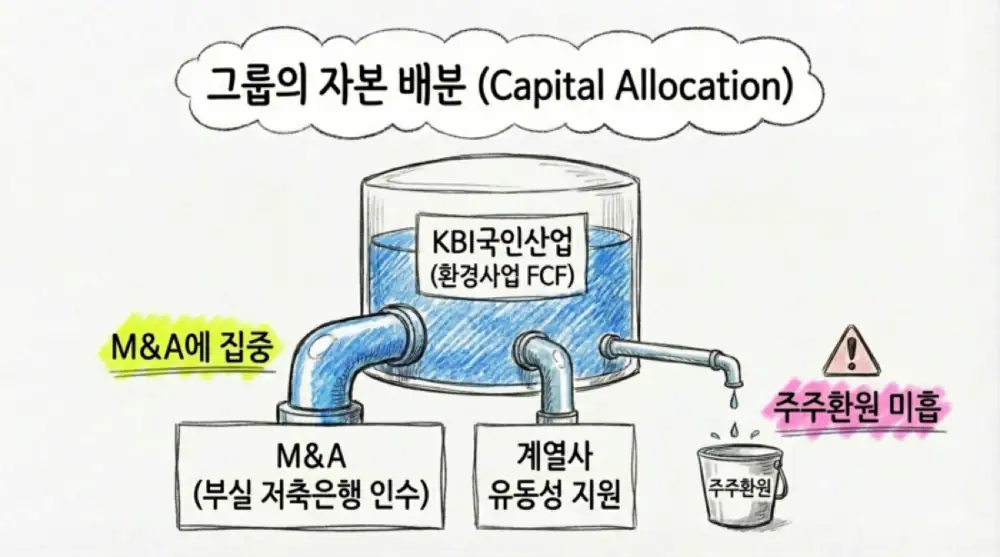

KBI Group does not have a listed pure holding company. Instead, unlisted KBI Gukinsanup, owned by the founder family, functions as the practical control tower. It generates cash from industrial waste incineration/landfill and waste-heat steam sales, which then fund group M&A and liquidity support.

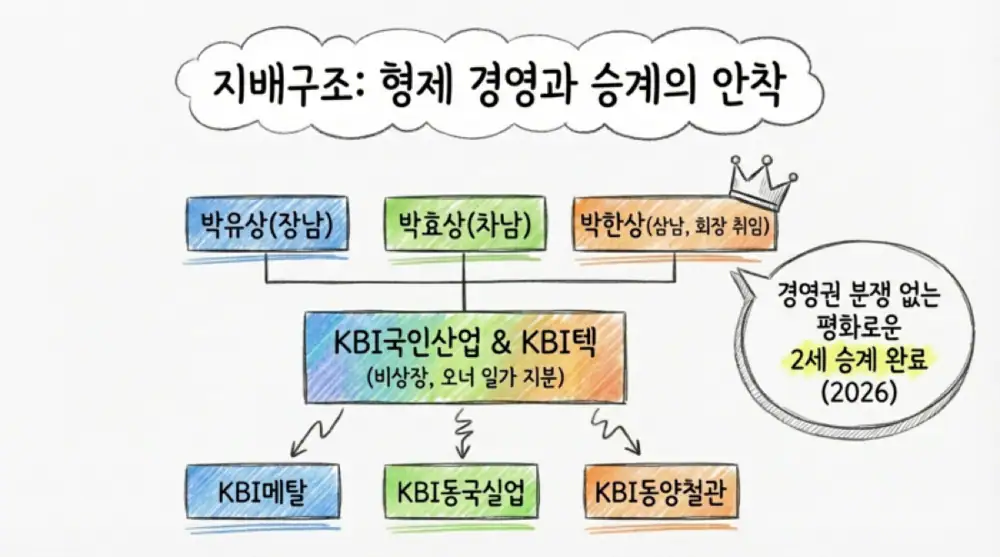

The governance structure is based on cooperation among the late founder Jae-eul Park’s three sons, Yu-sang Park, Hyo-sang Park, and Han-sang Park. The source interprets Han-sang Park’s appointment as chairman in early 2026 as completion of the second-generation succession.

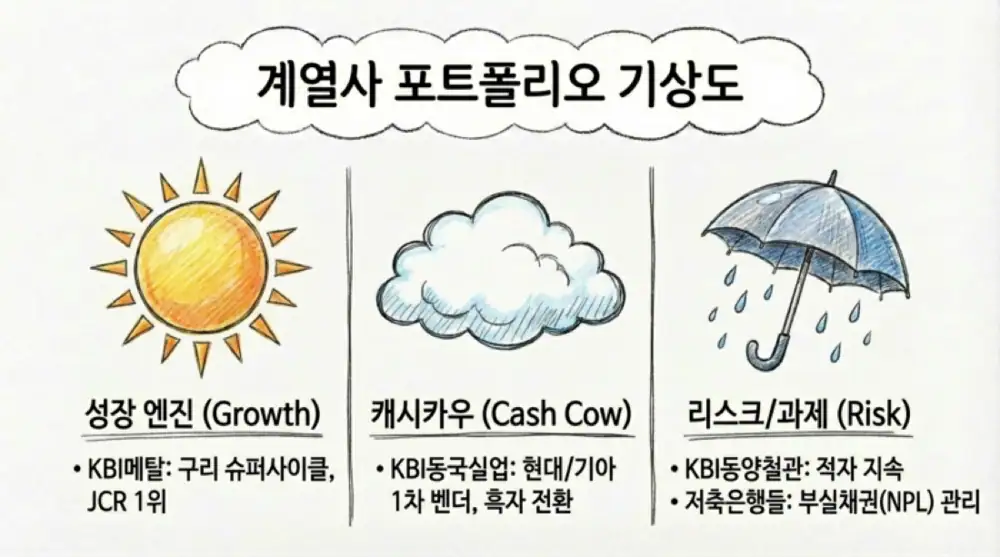

2. Affiliate portfolio

| Affiliate/area | Source facts | Investment lens |

|---|---|---|

| KBI Metal | About 45% domestic share in JCR copper rod, monthly 5,000-ton capacity, and 40+ domestic SME wire-company customers | Direct beneficiary candidate from AI data centers, grid replacement, and higher EV copper use |

| KBI Gukinsanup | Waste-treatment fees and waste-heat steam sales; source says steam manufacturing cost is effectively near zero | Cash reservoir for group M&A |

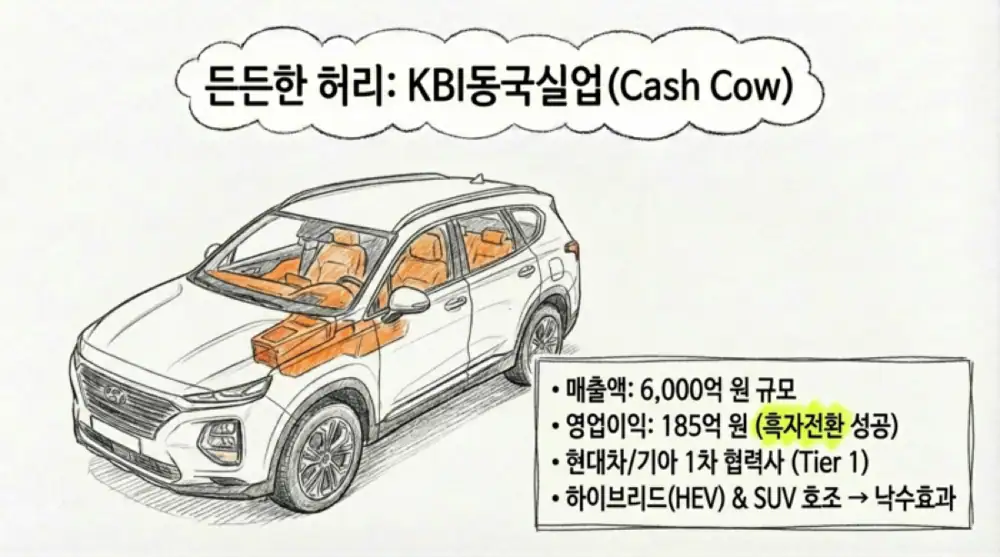

| KBI Dongkook Industrial | Hyundai/Kia Tier-1 auto-parts supplier; 2025 operating profit turned positive at KRW 18.55848 billion | Manufacturing cash cow defending group scale |

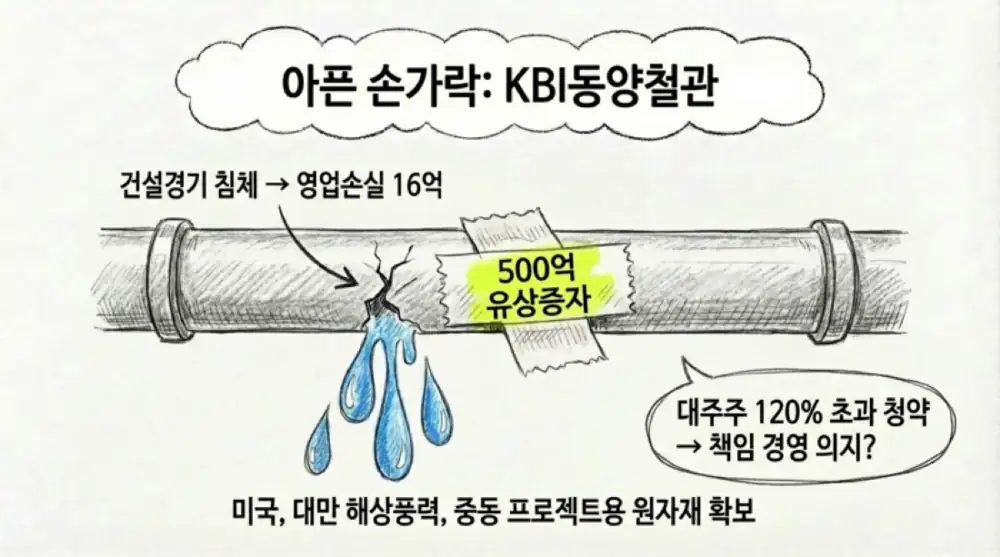

| KBI Dongyang Steel Pipe | 2025 revenue KRW 234.7 billion, down 6.2%, operating loss KRW 1.6 billion; KRW 50 billion rights offering | Turnaround attempt through US SAW pipe, Taiwan offshore wind, and Iraq pipeline projects |

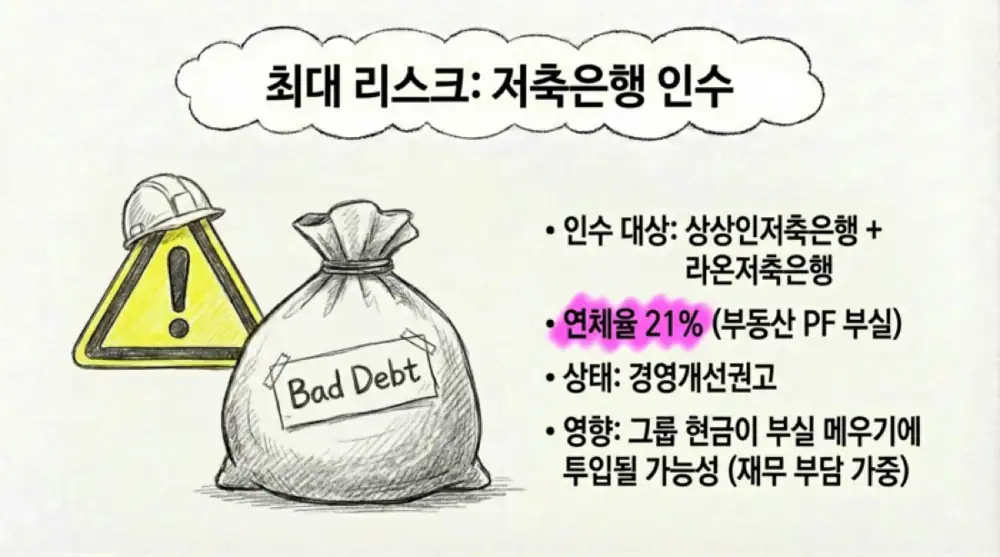

| Savings banks | Sangsangin 90.01% for KRW 110.7 billion; Raon 60% for about KRW 10 billion | Supply-chain finance synergy and real-estate PF cleanup risk coexist |

3. Finance re-entry and risk

The source frames the 2025 savings-bank acquisitions as KBI Group’s return to lending finance after 25 years. It links the move to the old Gap-Eul Trading group’s past experience operating Gap-Eul Mutual Credit Depository before exiting finance after the IMF-era restructuring.

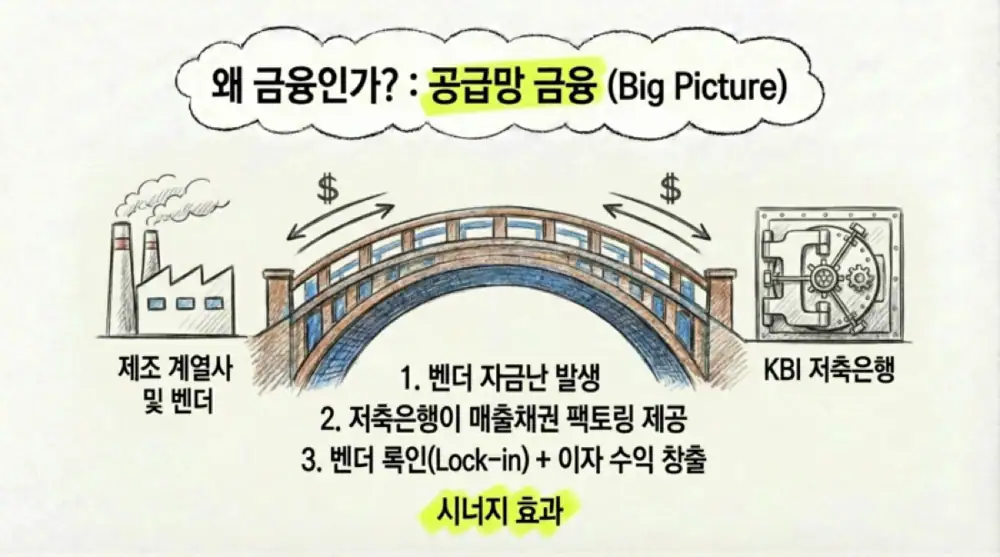

Supply-chain finance

As of Q2 2025, corporate loans accounted for 73.4% of Sangsangin Savings Bank’s loan book and 75.7% of Raon’s. The strategic argument is vendor factoring and working-capital lending to manufacturing affiliates and suppliers.

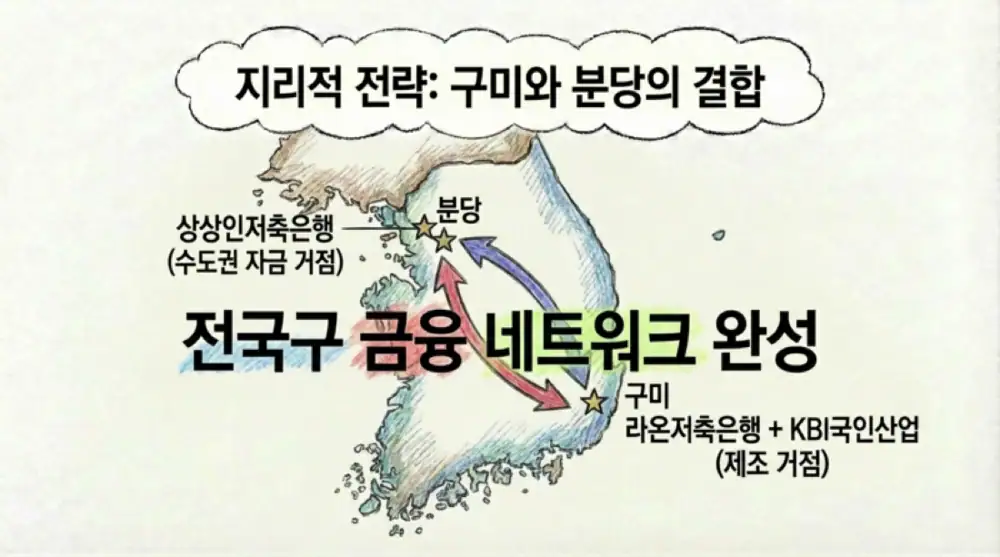

Gumi and metro Seoul

Raon is based in Gumi, while Sangsangin is centered in Bundang/Seongnam, targeting both the Daegu-Gyeongbuk manufacturing network and metropolitan liquidity.

NPL and BIS

Sangsangin’s delinquency ratio reached 21% due to real-estate PF trouble and it received a management-improvement recommendation in March 2025. Raon also had a management-improvement recommendation history.

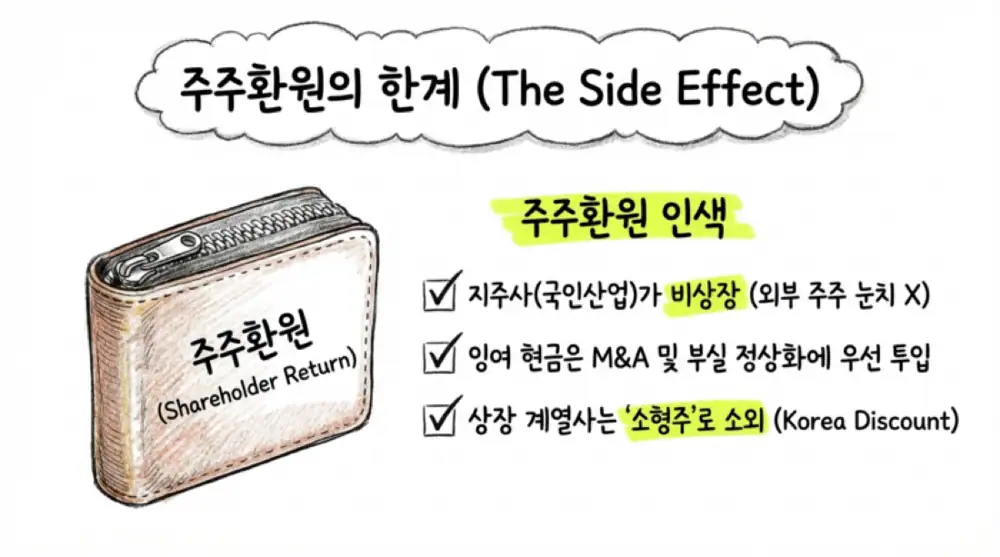

Interpretation: For the next two to three years, group financial management may focus less on new manufacturing expansion and more on NPL write-offs, capital injections, and BIS-ratio defense. That can structurally limit shareholder returns at listed affiliates.

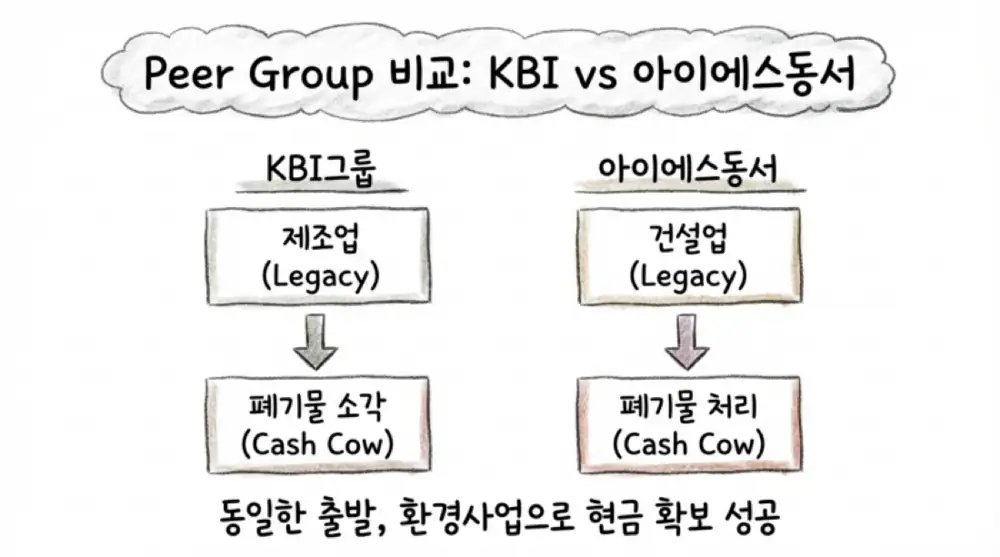

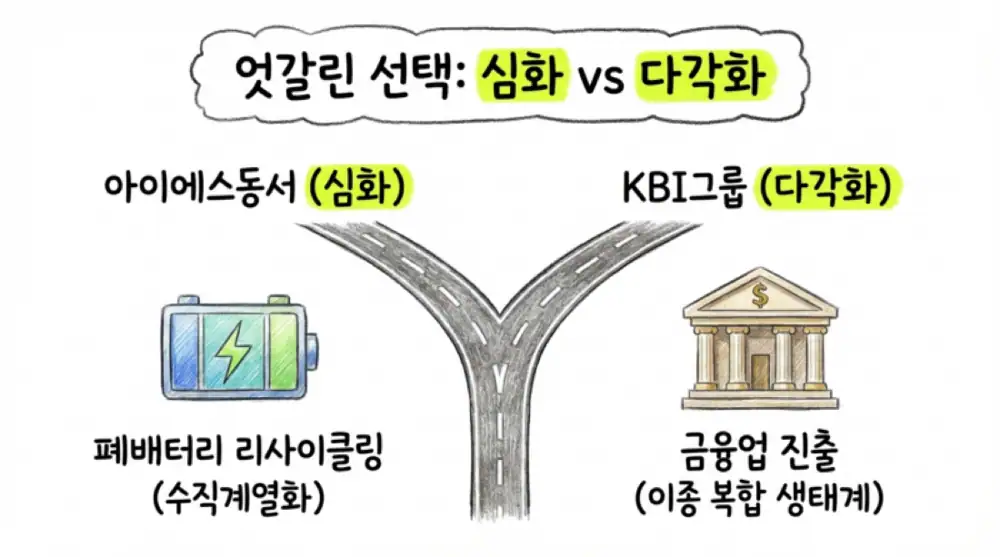

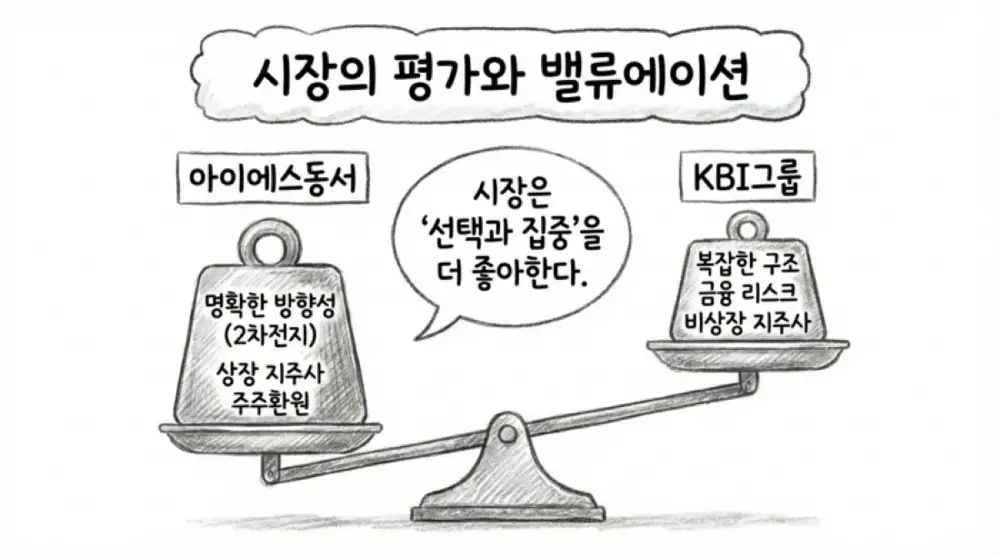

4. Comparison with IS Dongseo

| Comparison | KBI Group | IS Dongseo |

|---|---|---|

| Post-environment evolution | Auto parts, metals/wire, steel pipe, environment, plus savings-bank finance | Vertical integration from environment into used-battery recycling |

| Capital allocation | Environmental cash directed into two troubled savings-bank acquisitions | More than KRW 500 billion deployed for 100% of IS TMC and the setup of IS BM Solution |

| Shareholder return | Practical holding company is unlisted, reducing capital-market pressure | Listed holding-company pressure supports IR, buybacks, and cancellations |

| Valuation | No listed flagship holding company, so quality subsidiaries are valued as fragmented small parts/theme stocks | Construction weakness lowered EV/EBITDA from 4.0x to 3.5x, but battery-recycling subsidiaries with 16-24% operating margins provide support |

The source cites IS Dongseo’s 2023 used-battery operating margin of 16.44% and a plan to triple processing capacity to 62,000 tons by 2026. It argues that KBI chose finance/manufacturing diversification rather than deeper environmental vertical integration.

5. Group top pick: KBI Metal

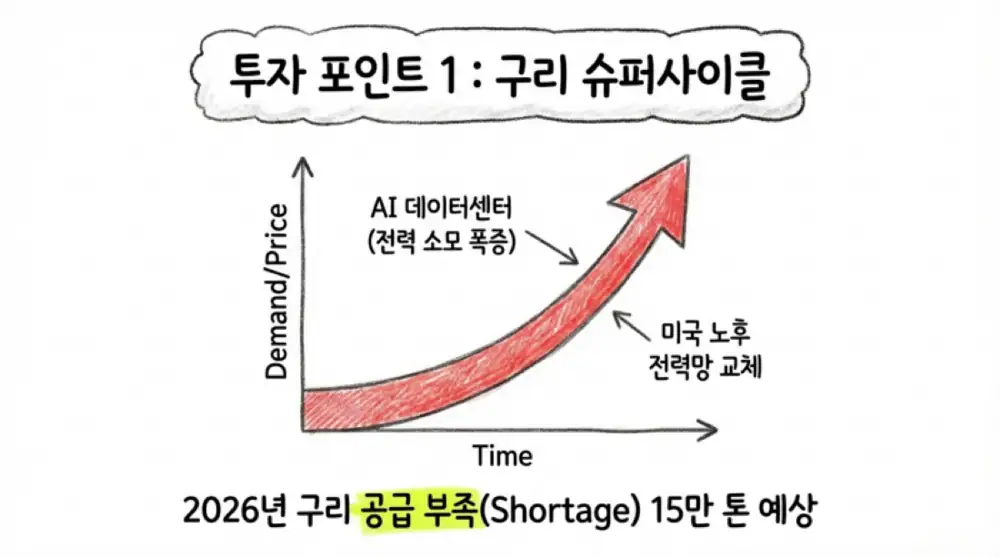

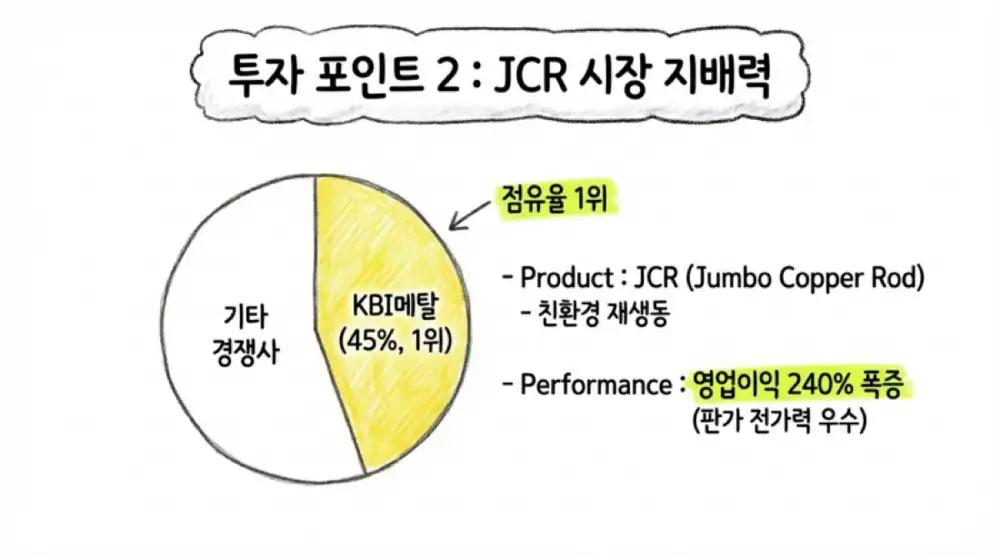

Official fact: The source presents KBI Metal as Korea’s No. 1 JCR player with about 45% domestic share. H1 2024 consolidated revenue was KRW 366.0 billion, up 3.3% YoY, while operating profit was KRW 17.5 billion, up 240.3%. Cumulative exports as of August 2024 were USD 335 million, up 129.0% YoY.

| Top-pick logic | Source facts/numbers | My checkpoint |

|---|---|---|

| Copper supercycle | ICSG forecast: 2026 copper mine production +0.9%, refined copper use +2.1%, and more than 150,000 tons of shortage | Whether higher copper prices pass through into ASP and spread |

| Price outlook | Goldman Sachs long-term bullish view and a cited 2026 average copper price above USD 15,000/ton | Managing both raw-material upside and hedging P&L |

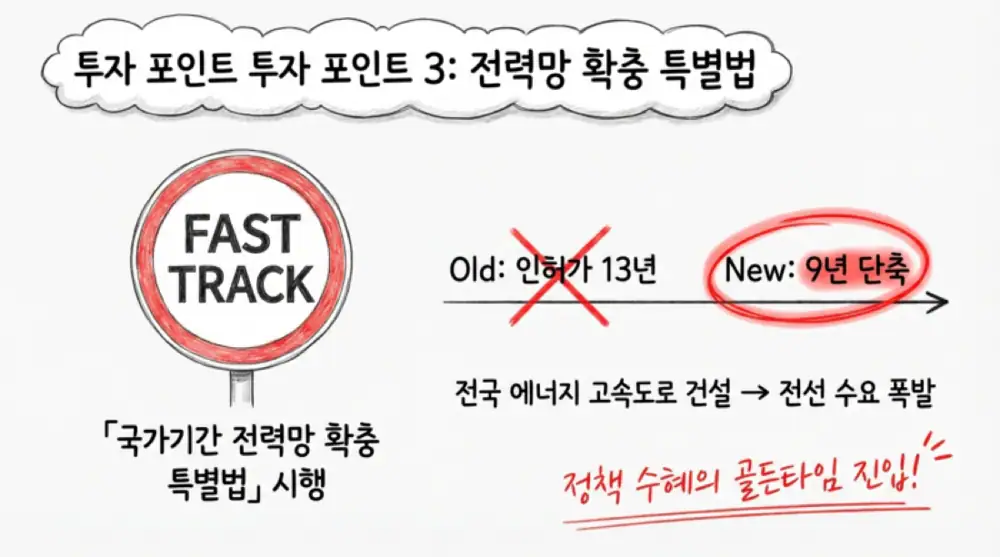

| Grid special act | National backbone power-grid expansion enforcement decree passed cabinet in September 2025; target to cut 345kV transmission/substation build time from 13+ years to within a standard 9-year period | Whether grid investment turns into copper-rod demand |

| Compensation incentives | Resident support up to 3-3.5x, KRW 2 billion per km for local governments, and an extra 10% for fast approvals | Speed of permitting bottleneck relief |

| Valuation | Share price in the KRW 1,700s, PBR 0.52x, down from a prior high of KRW 4,745 | Re-rating requires sustained operating profit and more stable derivative losses |

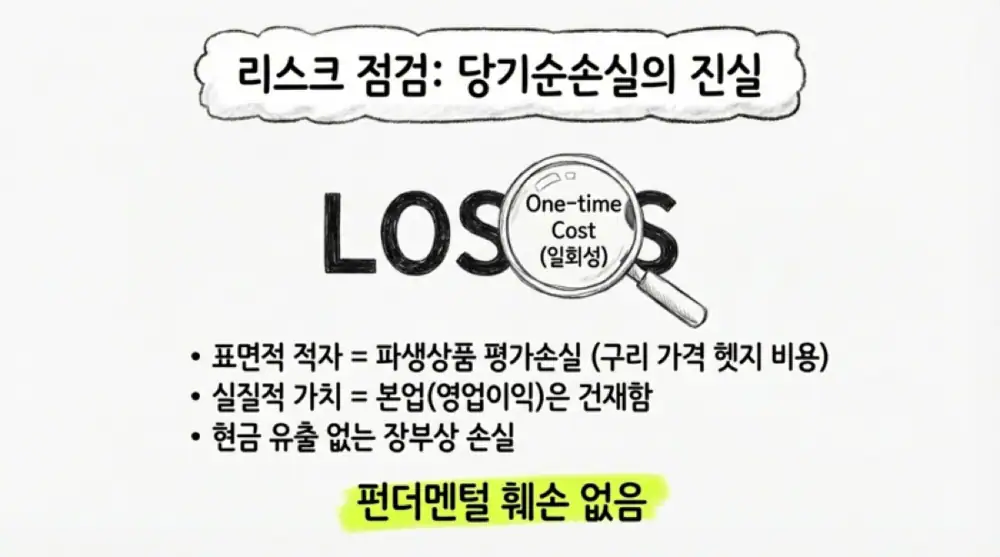

Interpretation: KBI Metal is relatively separated from holding-company financial distress and has clear external momentum from power grids, AI data centers, and EV copper demand. Risks still include Korea Future Materials, an LS Cable affiliate, entering recycled copper, and derivative valuation losses from copper futures and currency forwards.

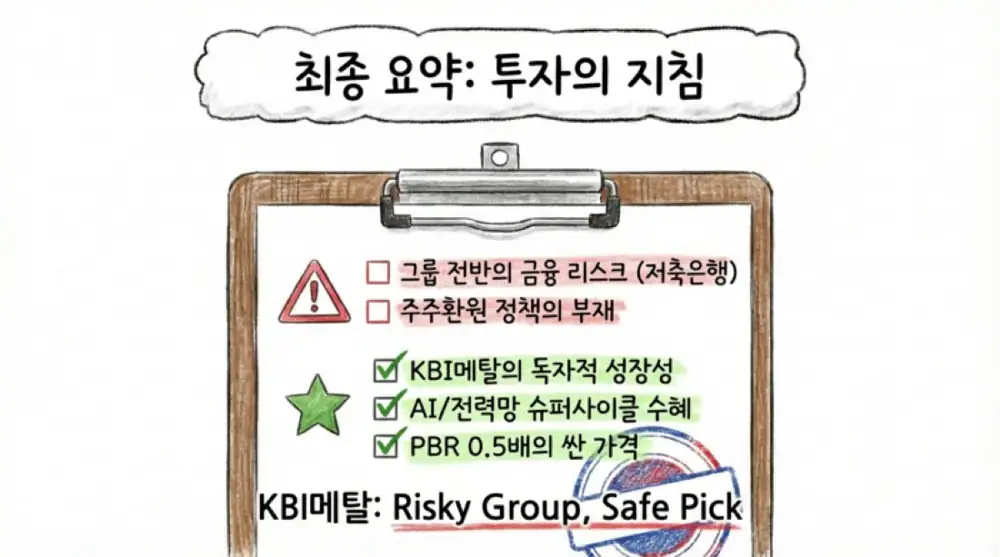

6. Final read

The source frames KBI Group as carrying both a shield, the environmental cash cow of waste treatment and renewable steam energy, and a risky spear, savings-bank acquisitions. My practical takeaway is selective exposure: avoid treating the whole group as one simple buy case, and focus on whether KBI Metal can capture the AI infrastructure and national grid cycle while avoiding the financial-sector risk pocket.

The source presents a scenario in which KBI Metal recovers to the mid-KRW 2,000s and approaches KRW 3,000 over three years if derivative valuation losses fade and copper shortage becomes visible after 2026. That should be read as the author’s scenario, not advice; quarterly earnings, hedge losses, and the savings-bank cleanup pace still need monitoring.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224195829553

- 원문 보조 콘텐츠 링크: http://googleusercontent.com/assisted_ui_content/1

- 원문 외부 이미지: https://lh7-rt.googleusercontent.com/docsz/AD_4nXcf6QfRndNQsP12WW6zKRQ9k99Y9oyyj19Rd_Uj2XfpaV_ilEvX0bFyzXl8FtAgrmCwK8N1Imeim8J0jv0TThBxodP5aWtXwa7ohN3IRfa2IRdmZFCM36ovDEOXox6qqxN6jIJQBmgvUkSCf0tIRsFWUyj1Rg?key=psOc7HOlnGrkk0zl6BfaPw

- KBI그룹 박한상 회장 체제 전환 - Daum: https://v.daum.net/v/5inciKAiDB

- KBI 라온·상상인저축은행 인수 - 파이낸셜투데이: http://www.ftoday.co.kr/news/articleView.html?idxno=350196

- KBI메탈 미국 전력망 수혜 가능성 - 이투데이: https://www.etoday.co.kr/news/view/2409465

- KBI메탈 기업분석 - 네이버 프리미엄콘텐츠: https://contents.premium.naver.com/prover/wisdomessenger/contents/251216195516231ow

- 현대차 2025년 실적 - 다나와 자동차: https://mauto.danawa.com/news/?Tab=N1&pcUse=n&Work=detail&no=5963648

- 현대자동차 2025년 영업익 - FETV: https://www.fetv.co.kr/news/article.html?no=211255

- KBI동국실업 2025년 영업이익 흑자전환: https://www.digitaltoday.co.kr/news/articleView.html?idxno=633673

- KBI동양철관 2025년 영업손실 - 스틸데일리: https://www.steeldaily.co.kr/news/articleViewAmp.html?idxno=198518

- KBI동양철관 적자전환 - 디지털투데이: https://www.digitaltoday.co.kr/news/articleView.html?idxno=633416

- KBI동양철관 500억 유상증자 - 페로타임즈: https://www.ferrotimes.com/news/articleView.html?idxno=43639

- KBI동양철관 500억 유상증자 - Daum: https://v.daum.net/v/KdVySIOJZJ

- KBI동양철관 심층진단 - 뉴스밸류: https://www.newsvalue.kr/news/articleView.html?idxno=22571

- 상상인저축은행 KBI그룹 품으로 - KB의 생각: https://kbthink.com/news-list/view.html?newsId=20251031155148579

- 상상인저축은행 KBI그룹 품으로 - 연합인포맥스: https://news.einfomax.co.kr/news/articleView.html?idxno=4381647

- 상상인저축은행 지분 매수 - 뉴스1: https://www.news1.kr/finance/general-finance/5960843

- KBI메탈 다음 금융: https://m.finance.daum.net/quotes/A024840/news/stock/20251031150647365

- KBI그룹 상상인저축은행 자본확충 우려 - 녹색경제신문: https://www.greened.kr/news/articleView.html?idxno=332786

- KBI그룹 상상인저축은행 1107억원 인수 - 서울경제TV: https://www.sentv.co.kr/article/view/sentv202510310164?d=pc

- 상상인저축은행 90% 1107억원 매각 - 마켓인: https://marketin.edaily.co.kr/News/ReadE?newsId=05448086642338496

- KBI그룹 금융업 복귀 - 시사오늘: http://www.sisaon.co.kr/news/articleView.html?idxno=177233

- 아이에스동서 코엔텍 인수 - 뉴스웨이: https://www.newsway.co.kr/news/view?ud=2020060513412068137

- 아이에스동서 리포트 - 삼성증권: https://www.samsungpop.com/common.do?cmd=down&contentType=application/pdf&inlineYn=Y&saveKey=research.pdf&fileName=2010/2023071916440385K_02_05.pdf

- 아이에스동서 환골탈태 - 버핏연구소: https://buffettlab.co.kr/news/view.php?idx=41912&mcode=m331evx&page=629

- 아이에스동서 폐배터리 로드맵 - 팍스경제TV: https://www.paxetv.com/news/articleView.html?idxno=168256

- 아이에스동서 리사이클링 밸류체인 - 시사캐스트: http://www.sisacast.kr/news/articleView.html?idxno=52774

- 아이에스동서 폐배터리 처리용량 확대: https://www.isdongseo.co.kr/board/view/53?boardno=611&page=4&keyname=&keyword=

- ICSG 2026년 구리 생산 증가율 전망 - 철강금속신문: http://www.snmnews.com/news/articleView.html?idxno=561680

- KBI메탈 구리 가격 전망 - Investing.com: https://kr.investing.com/news/stock-market-news/article-1078783

- 국가기간 전력망 확충 특별법 시행령 자료: https://www.motir.go.kr/attach/down/095a2dda9c864e1d90d751f7668a1117/9bc0ea2d9521fc471a6868fd9b6d9367

- 국가기간 전력망 확충 특별법 시행령 - 국가법령정보센터: https://law.go.kr/LSW/lsRvsDocInfoR.do?lsiSeq=273843

- KBI메탈 JCR ROD 기사 - 핀포인트뉴스: https://www.pinpointnews.co.kr/news/articleView.html?idxno=316045

- KBI메탈 투자분석 2026.01.02 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=PIdf19npBZ0L27d5

- KBI메탈 투자분석 2025.12.17 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=7vw3TvyOvH5k3auO

- KBI메탈 투자분석 2026.01.18 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=ta52izzq75Q7wEpD

- KBI메탈 JCR ROD 국내 1위 - 이투데이: https://www.etoday.co.kr/news/view/2439437

- KBI메탈 투자분석 2025.11.30 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=whK6L7PM00KbNBbE