DEEP RESEARCH · PIOLINK

PIOLINK: Network-Security Turnaround in the Cyber-Resilience Era

A review centered on 108.4% operating-profit growth and Japan zero-trust expansion.

0. Bottom line first

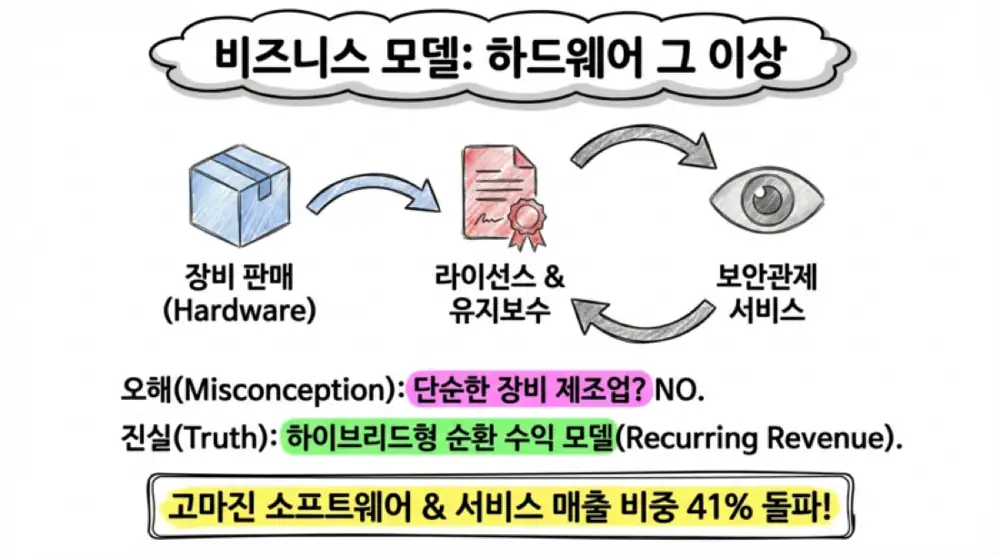

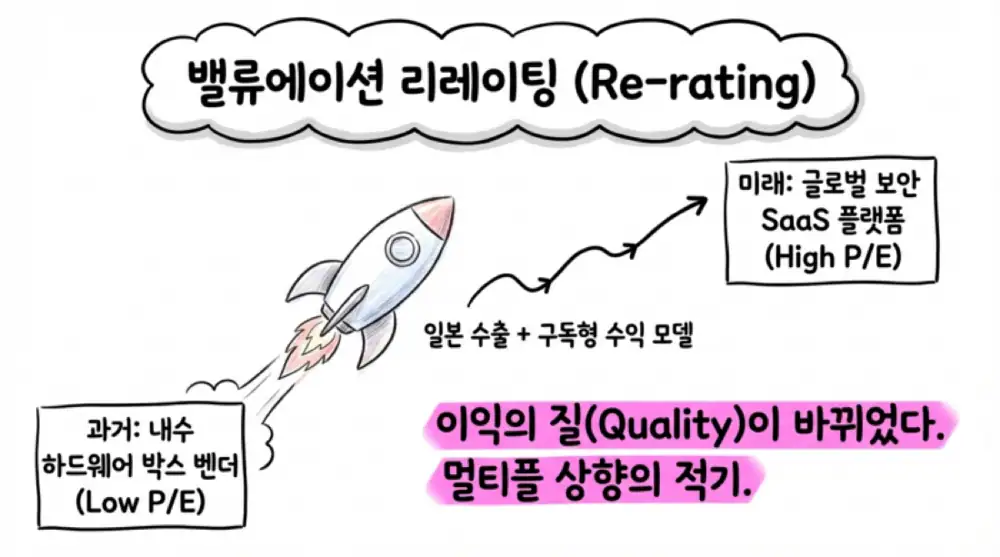

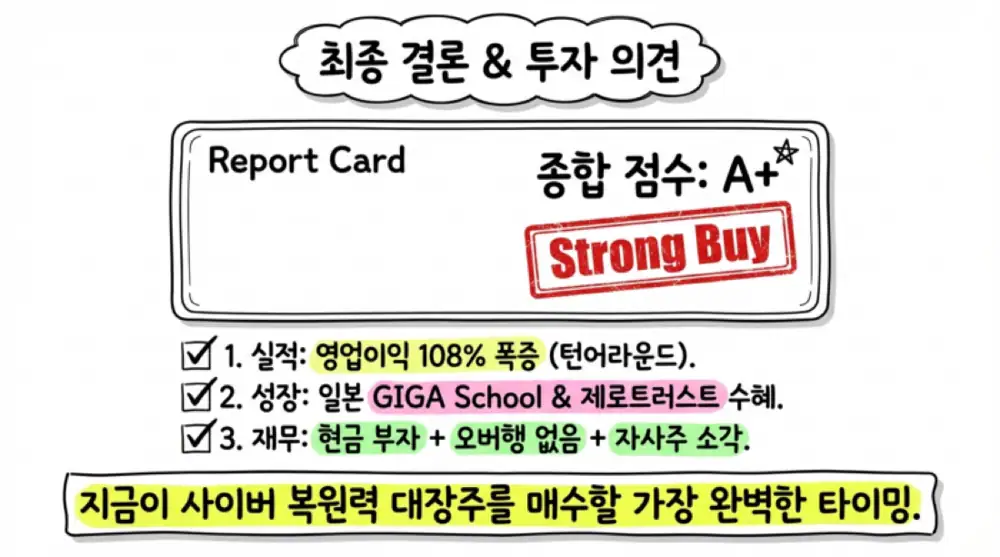

PIOLINK is moving from a hardware-box vendor into a recurring model combining security services and maintenance. The 108.4% increase in preliminary 2025 operating profit signals that Japan-led overseas growth and customer diversification are starting to show in the financials.

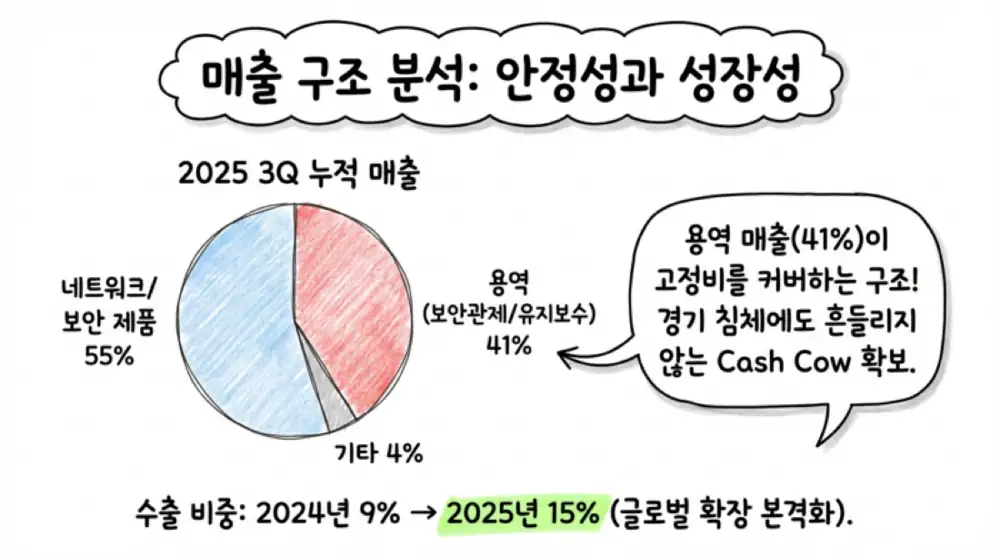

1. Business structure and revenue mix

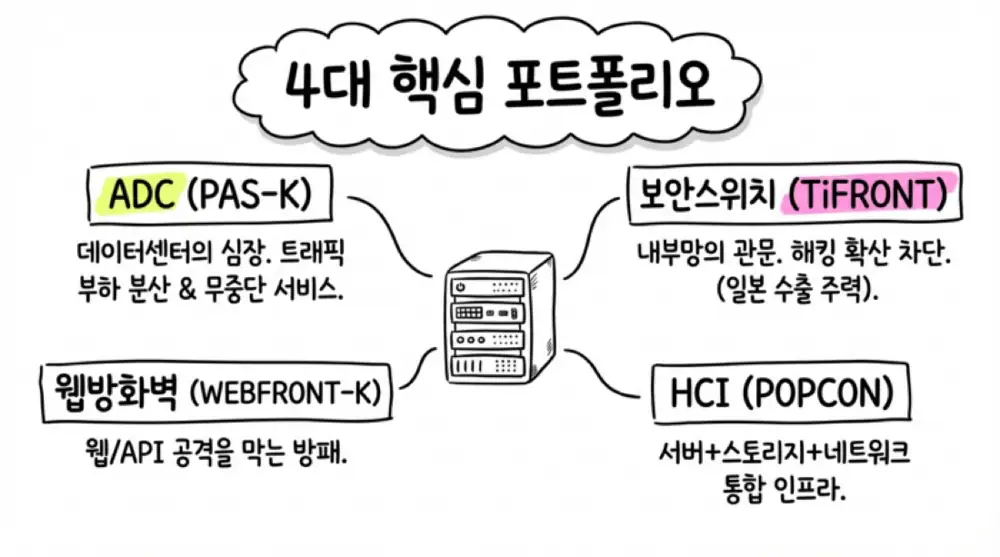

PIOLINK provides ADC, TiFRONT cloud security switches, WEBFRONT-K web firewalls, POPCON HCI, and managed security and consulting services.

| Category | Items | 9M 2025 revenue | Share | 9M 2024 |

|---|---|---|---|---|

| Network/security products | ADC, security switches, web firewalls, HCI | KRW 22,762,488 thousand | 55% | KRW 21,108,974 thousand |

| Services | Managed security, consulting, maintenance | KRW 16,856,542 thousand | 41% | KRW 14,021,479 thousand |

| Merchandise/other | Other sales | KRW 1,700,945 thousand | 4% | KRW 915,626 thousand |

| Total | Total revenue | KRW 41,319,975 thousand | 100% | KRW 36,046,079 thousand |

Interpretation: Services and maintenance at 41% of revenue show a shift toward software/service economics. Product export share rose from 9% in Q3 2024 to 15% in Q3 2025.

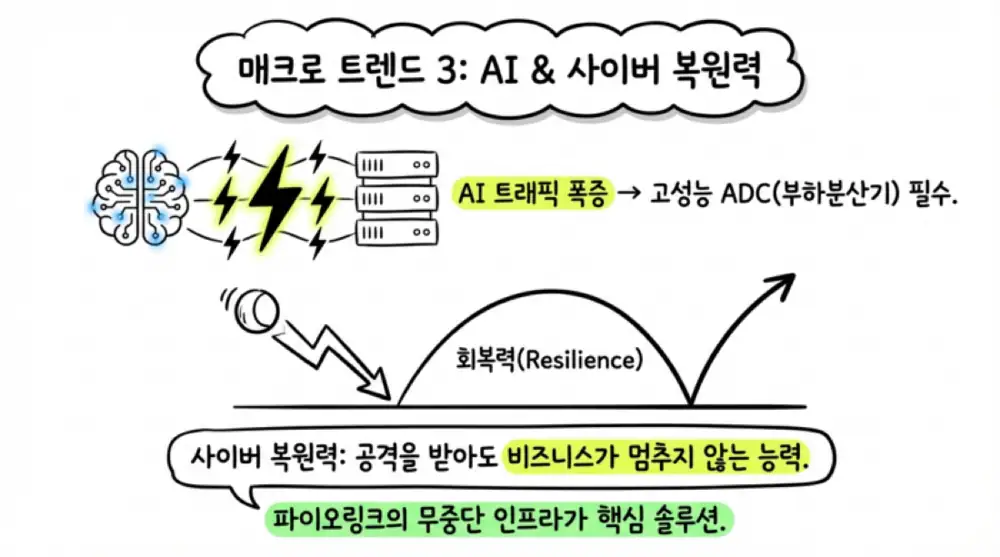

PAS-K

Load-balances large traffic volumes and supports uninterrupted services.

TiFRONT

A cloud security switch that blocks ransomware lateral movement at the L2/L3 switch layer.

SECaaS

24/7 managed security and consulting create high-margin recurring revenue.

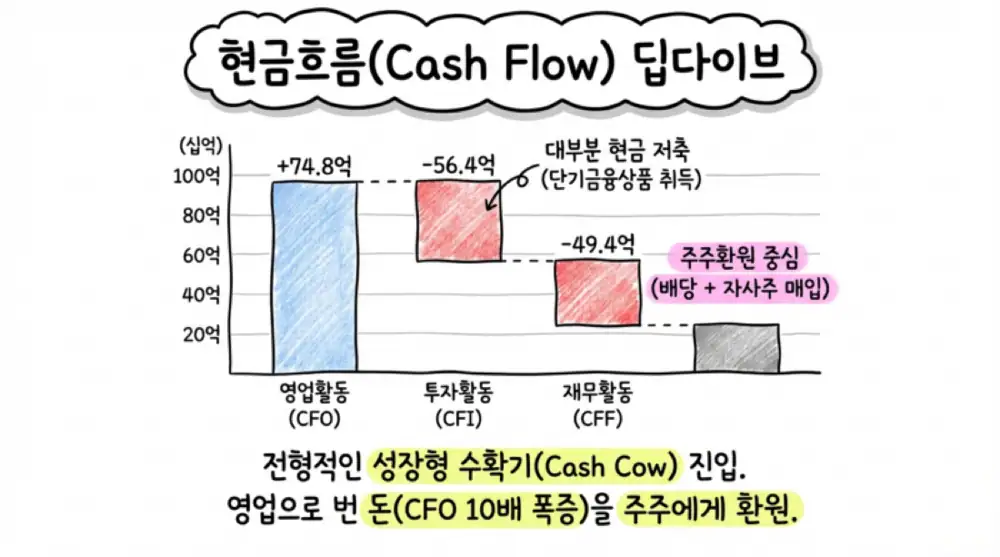

2. Cash flow and moat

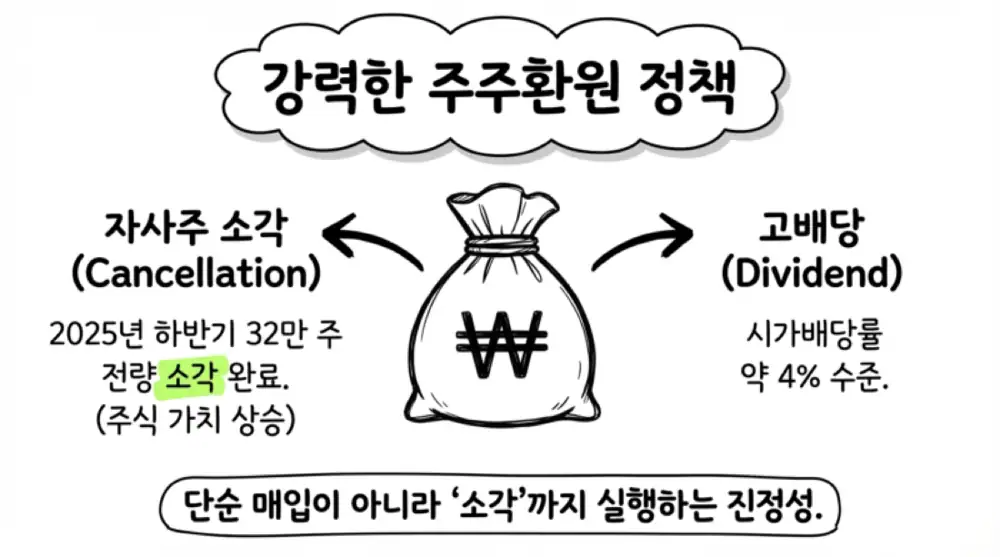

Official fact: 9M 2025 operating cash flow was KRW 7.48 billion, roughly 10x the KRW 0.76 billion in the prior year. Investment cash flow of -KRW 5.64 billion was mostly short-term financial products of -KRW 5.91 billion, while financing cash flow of -KRW 4.94 billion mainly reflected treasury-share purchases of -KRW 2.53 billion and dividends of -KRW 1.99 billion.

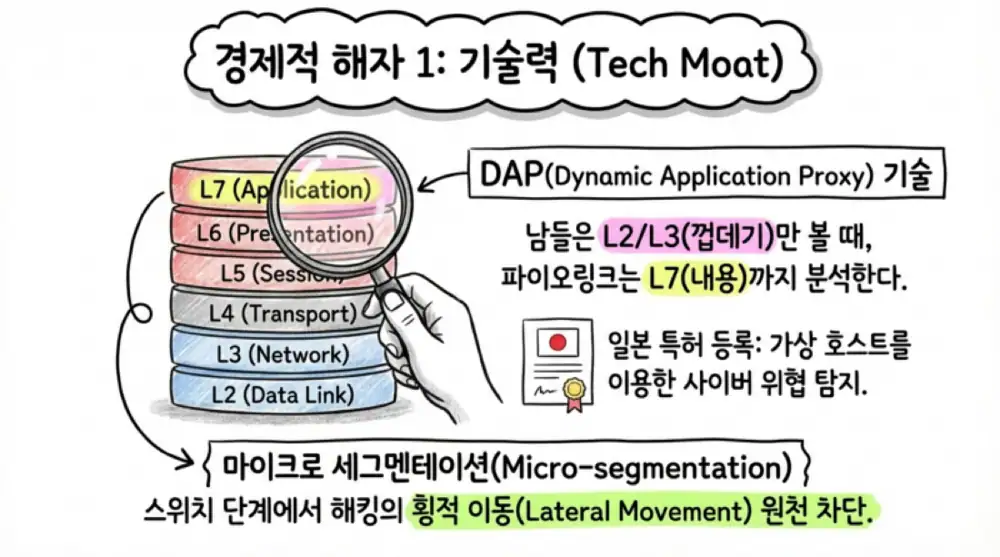

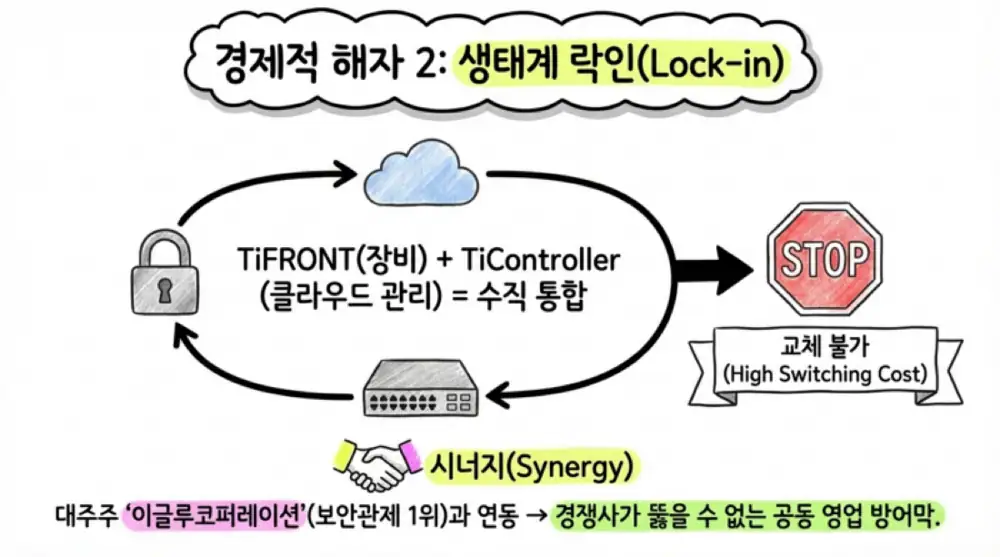

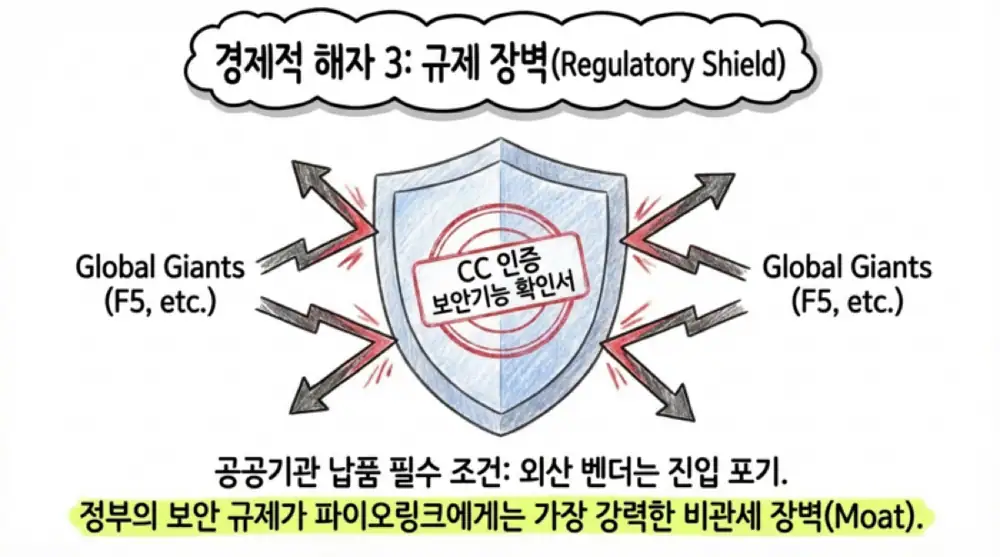

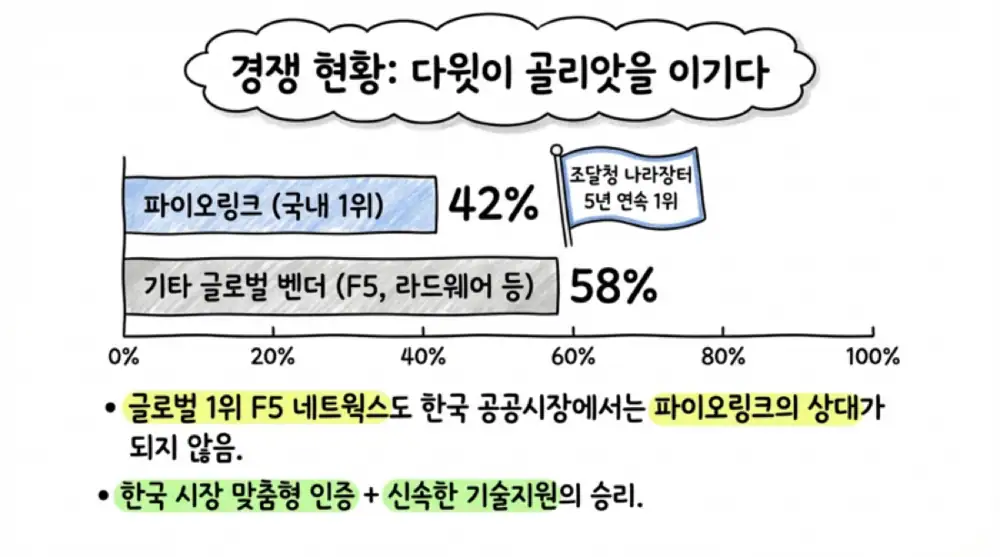

PIOLINK’s moat comes from DAP patents and L7 traffic processing, TiController cloud-management lock-in, the public-security ecosystem with IGLOO’s SIEM/SOAR, and certification barriers such as CC certification and National Intelligence Service security-function confirmation.

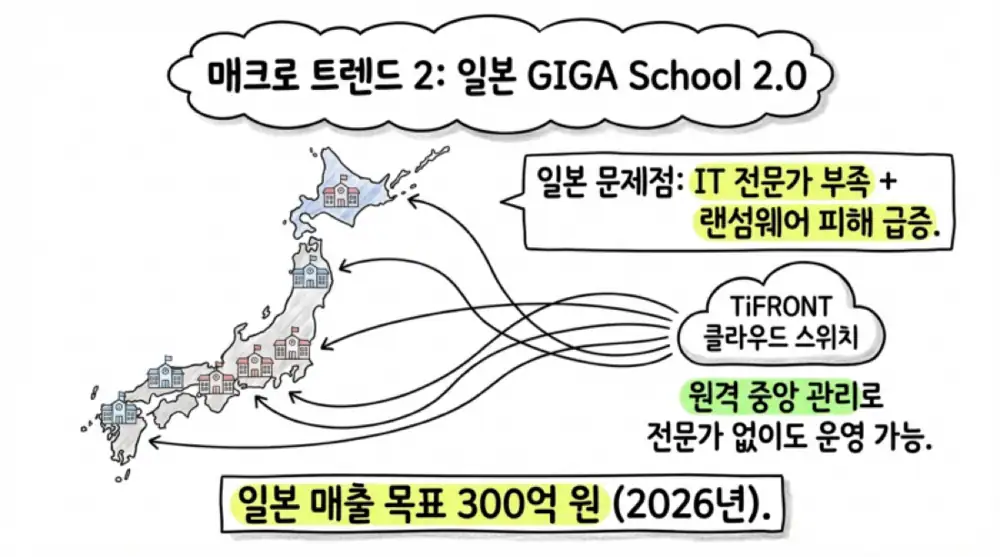

3. Zero trust and Japan expansion

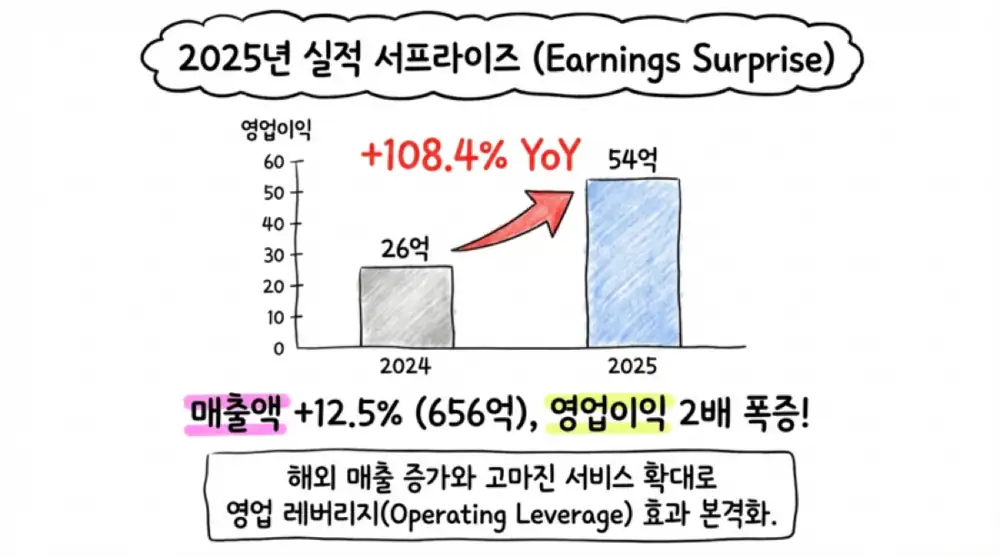

4. 2025 preliminary results and 2026 points

| Item | 2025 preliminary |

|---|---|

| Revenue | KRW 65.63492 billion, YoY +12.5% |

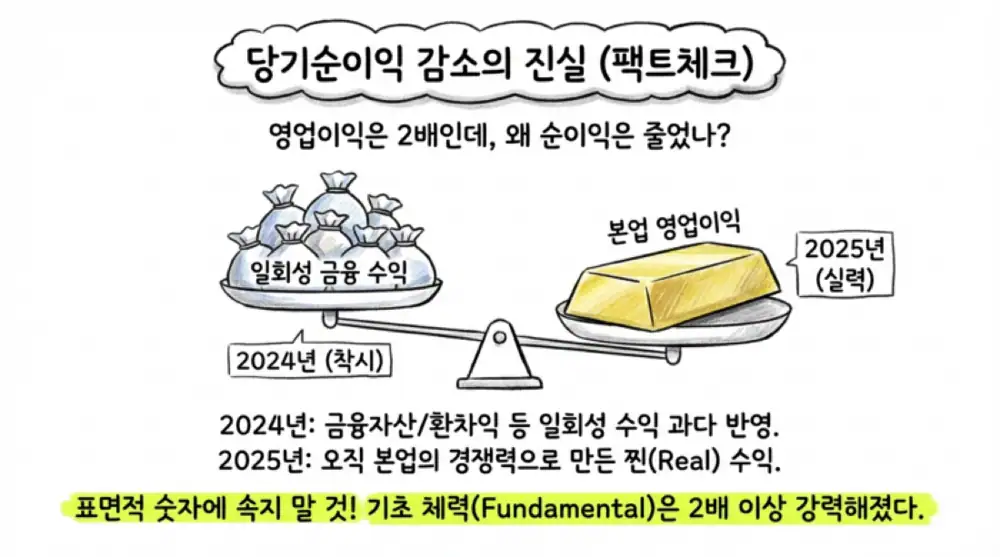

| Operating profit | KRW 5.40252 billion, YoY +108.4% |

| Net income | KRW 5.4 billion, down 39.2% from KRW 7.5 billion in 2024 |

Interpretation: The source argues the net-income decline should be viewed against the unusually high 2024 non-operating base. The operating-profit line, the core business indicator, more than doubled.

- The September 2024 establishment of Japanese subsidiary Pio Platform is the starting point for Japan zero-trust demand.

- The source presents a target of KRW 30 billion in Japan-only revenue by 2026.

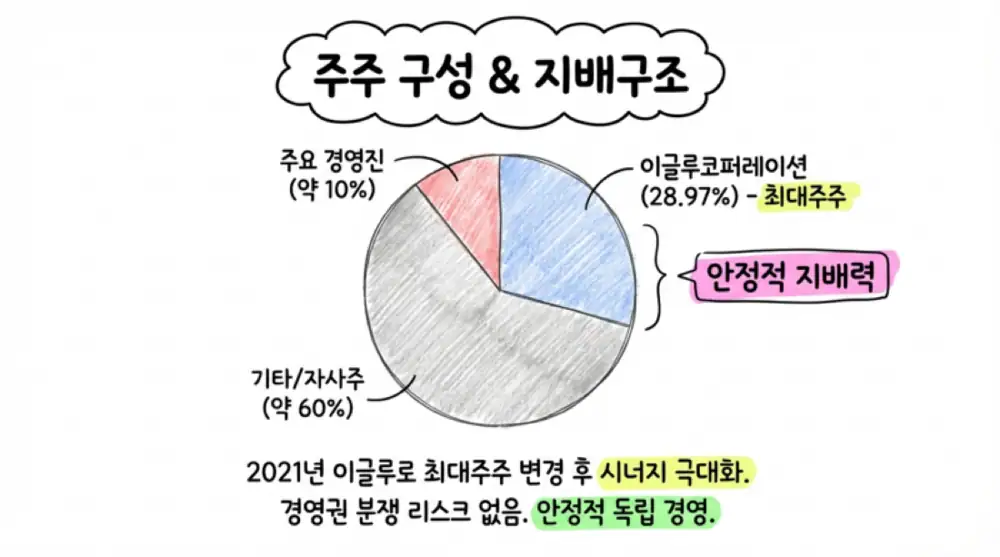

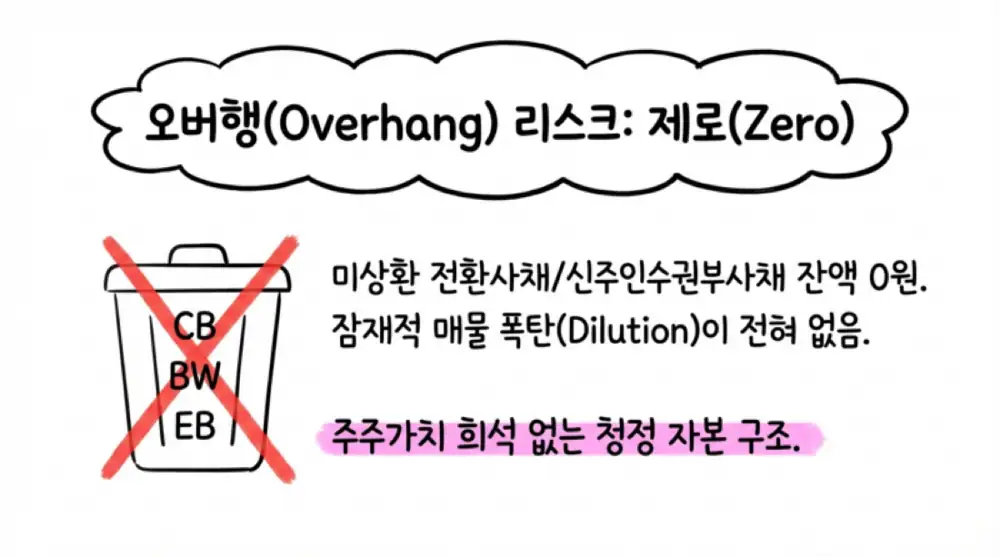

- Public data shows no CB/BW convertible overhang balance.

- The largest shareholder, IGLOO Corporation, strengthens governance stability and security value-chain synergy.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224195827623

- Reference 2: https://www.piolink.com/kr/company/News.php?vType=view&idx=634

- Reference 3: https://byline.network/2023/03/0315_05/

- Reference 4: https://piolinkin.tistory.com/205

- Reference 5: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=517

- Reference 6: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=870

- Reference 7: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=872

- Reference 8: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=877

- Reference 9: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=898&page=1

- Reference 10: https://www.igloo.co.kr/newsroom/press/%E3%88%9C%ED%8C%8C%EC%9D%B4%EC%98%A4%EB%A7%81%ED%81%AC-%EC%9D%B8%EC%88%98-%EC%9D%B8%EA%B3%B5%EC%A7%80%EB%8A%A5-%EB%B9%85%EB%8D%B0%EC%9D%B4%ED%84%B0-%ED%81%B4%EB%9D%BC%EC%9A%B0%EB%93%9C-%EC%97%AD/

- Reference 11: https://www.mt.co.kr/tech/2022/11/23/2022112308413719477

- Reference 12: https://v.daum.net/v/KfSuQFCENF?f=p

- Reference 13: https://stibee.com/api/v1.0/emails/share/zGKsQJ6jnd-QGf5w3gaNIMPyO1BgUzI

- Reference 14: https://m.boannews.com/html/detail.html?idx=136577

- Reference 15: https://v.daum.net/v/20180314164938085?f=p

- Reference 16: https://www.dailysecu.com/news/articleView.html?idxno=204294

- Reference 17: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=851&page=1

- Reference 18: https://www.inews24.com/view/1415669

- Reference 19: https://www.newswire.co.kr/newsRead.php?no=932968

- Reference 20: http://kani.or.kr/board/view?bd_id=notice04&wr_id=587

- Reference 21: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=811

- Reference 22: https://cinsight.etoday.co.kr/detail/00492353

- Reference 23: https://m.ddaily.co.kr/page/view/2021040114135543963

- Reference 24: https://www.datanet.co.kr/news/articleView.html?idxno=120587

- Reference 25: https://www.datatooza.com/article/20260225105313956152ef3b9429_80

- Reference 26: https://www.pinpointnews.co.kr/news/articleView.html?idxno=432115

- Reference 27: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=846

- Reference 28: http://www.dailyinvest.kr/news/articleView.html?idxno=64511

- Reference 29: https://marketin.edaily.co.kr/News/ReadE?newsId=03958966642266992

- Reference 30: https://www.etoday.co.kr/news/view/2434742

- Reference 31: https://www.piolink.com/kr/company/News.php?bbsCode=media_press&vType=view&idx=860

- Reference 32: https://byline.network/2025/11/17-525/