DEEP RESEARCH · TPLEX

Tplex 2025 Q4: Rare-Metal Supply-Chain Reset and Advanced-Materials Re-rating

A research-style read-through of the stainless-bar cash cow, second-factory CAPEX, and tungsten shortage thesis

0. Bottom line first

My core read is that Tplex combines a 30-year profitable stainless-processing cash cow with upside from rare-metal supply-chain disruption and second-factory CAPEX in tungsten, nickel, and titanium.

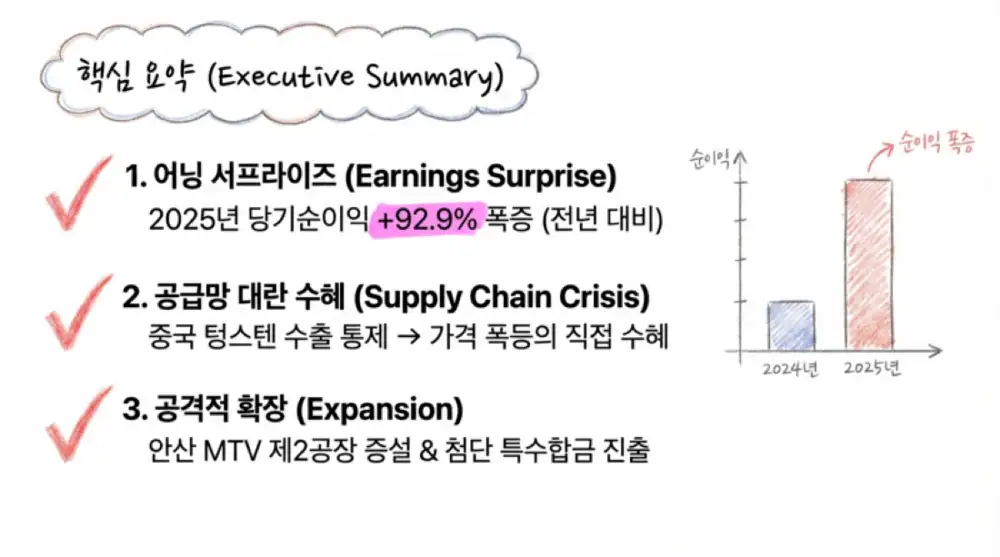

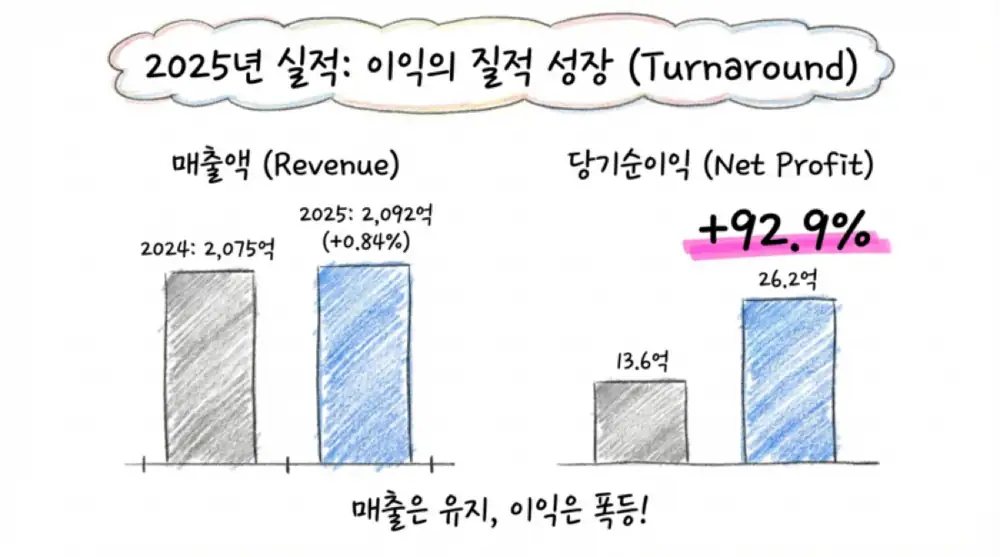

- 2025 separate revenue rose only 0.84% YoY to KRW 209.23 billion, but net income rose 92.90% to KRW 2.62 billion.

- 2025 operating profit rose 9.45% to KRW 5.24 billion, and pre-tax profit rose 113.28% to KRW 4.07 billion.

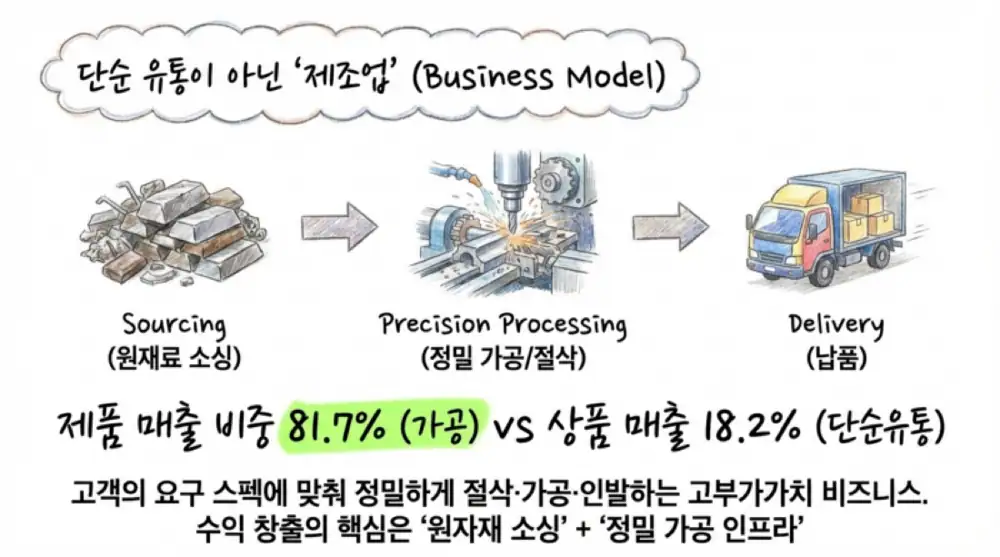

- Of KRW 156.8 billion in 2025 Q3 cumulative revenue, product revenue was KRW 128.1 billion, or 81.7%, while merchandise revenue was KRW 28.5 billion, or 18.2%.

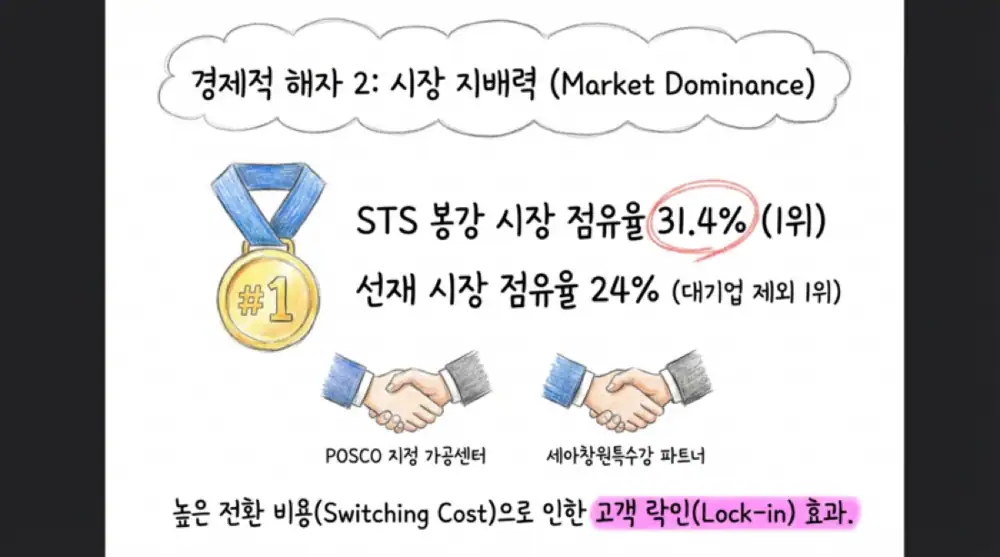

- The company has about 1,800 customers. The source states that it holds 31.4% share in Korean stainless bar and roughly 24% in wire excluding large-group affiliate SeAH Special Steel.

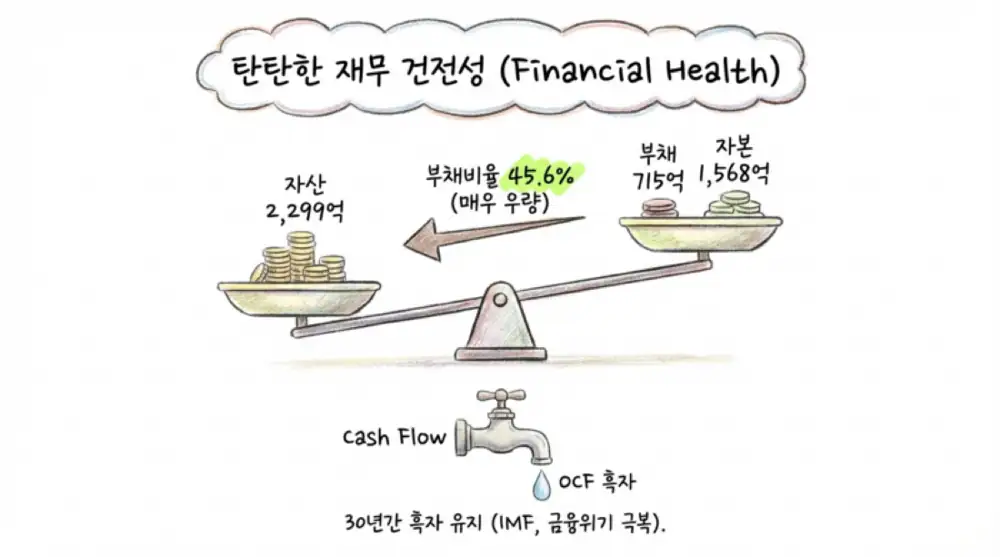

- At year-end 2025, assets were KRW 229.98 billion, liabilities KRW 71.54 billion, and equity KRW 156.84 billion, implying a debt-to-equity ratio of about 45.6%.

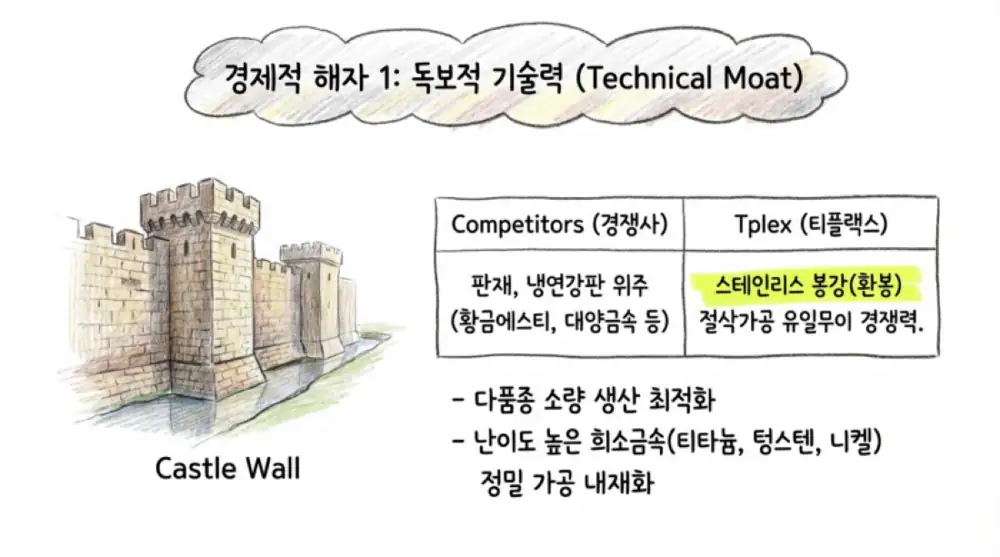

1. Business structure: materials company with high processing mix

Official fact: Tplex was founded in 1981 and listed on KOSDAQ in 2009 as a stainless-steel and rare-metal materials processing company.

Its segments include stainless round bars, plates, CDM machinery/equipment parts, and rare metals. It cuts, processes, and draws titanium, tungsten, nickel, molybdenum, and other materials to customer specifications.

Official fact: Of KRW 156.8 billion in 2025 Q3 cumulative revenue, product revenue was KRW 128.1 billion or 81.7%, while simple wholesale merchandise revenue was KRW 28.5 billion or 18.2%.

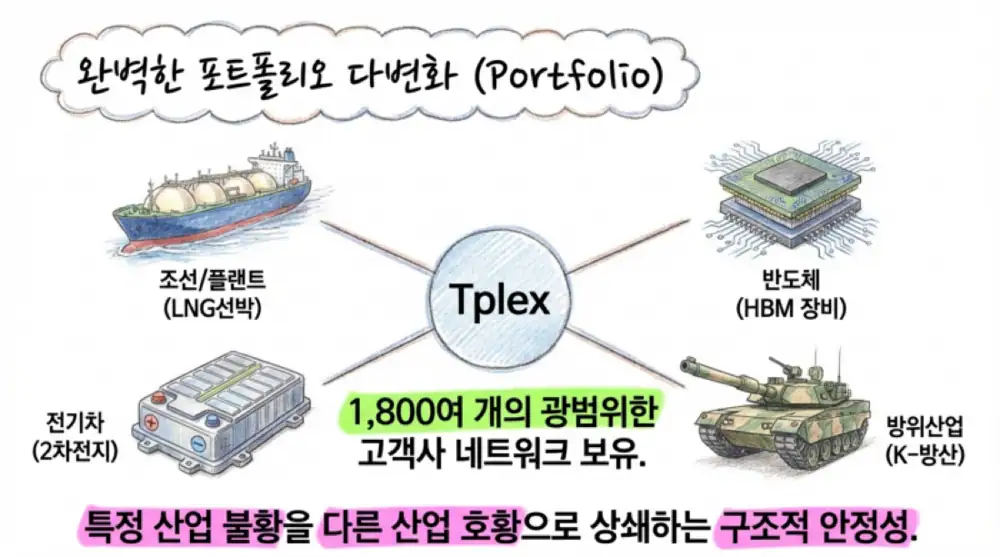

End markets include shipbuilding, petrochemical plants, power equipment, semiconductor manufacturing equipment, secondary batteries, displays, automotive parts, defense, and aerospace. The roughly 1,800-customer base reduces dependence on one industry.

Bar and wire niche

Unlike listed peers focused on plates and sheets, Tplex is differentiated in round bars and wire processing.

Rare-metal processing

It processes hard-to-machine tungsten, titanium, and nickel into machinery and parts.

Diversified customers

More than 1,800 customers and decade-plus relationships create switching costs and lock-in.

2. 2025 results: profit improved despite flat revenue

Official fact: On a 2025 separate basis, revenue was KRW 209.23 billion, operating profit KRW 5.24 billion, pre-tax profit KRW 4.07 billion, and net income KRW 2.62 billion.

| Metric | 2024 | 2025 | Change |

|---|---|---|---|

| Revenue | KRW 207.49B | KRW 209.23B | +0.84% |

| Operating profit | KRW 4.79B | KRW 5.24B | +9.45% |

| Pre-tax profit | KRW 1.91B | KRW 4.07B | +113.28% |

| Net income | KRW 1.36B | KRW 2.62B | +92.90% |

| Total assets | KRW 235.11B | KRW 229.98B | -2.18% |

| Total liabilities | KRW 78.27B | KRW 71.54B | -8.60% |

| Total equity | KRW 158.43B | KRW 156.84B | -1.00% |

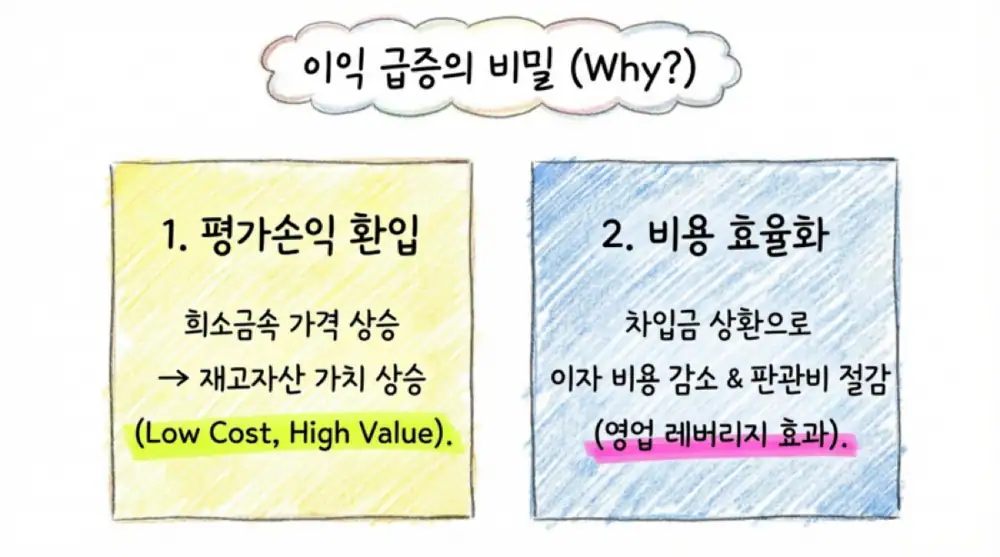

Interpretation: Revenue was nearly flat, but pre-tax profit and net income jumped because of inventory valuation reversals from stronger tungsten and special-alloy prices, lower interest expense after debt repayment, and SG&A efficiency.

At year-end 2025, total assets were KRW 229.9 billion, liabilities KRW 71.5 billion, and equity KRW 156.8 billion, for a debt-to-equity ratio of about 45.6%. The source sees the stainless business, which has stayed profitable for about 30 years, as a stable operating-cash-flow engine that can buy inventory ahead of raw-material increases and recover it through selling-price hikes.

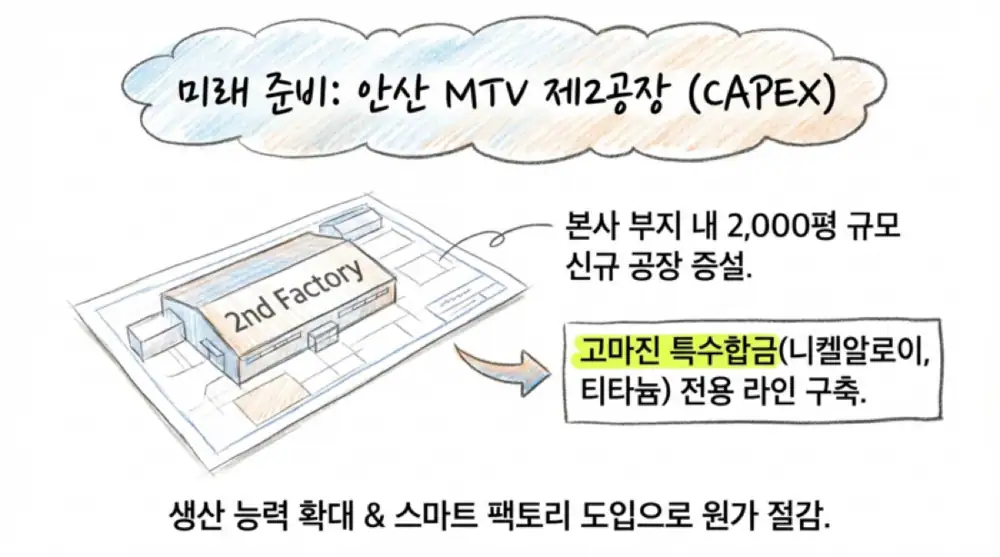

3. Capital policy: second-factory investment and buybacks

Official fact: The company has launched a master plan to build a 2,000-pyeong second factory on its roughly 17,000-pyeong headquarters site in Ansan Siwha Multi-Techno Valley ahead of its 50th anniversary in 2031.

The investment aims to move the portfolio into nickel alloys, rare metals, plates, and high-value special alloys. Adding smart-factory processes to existing infrastructure with 22 overhead cranes is expected to internalize outsourced processing and shorten lead times.

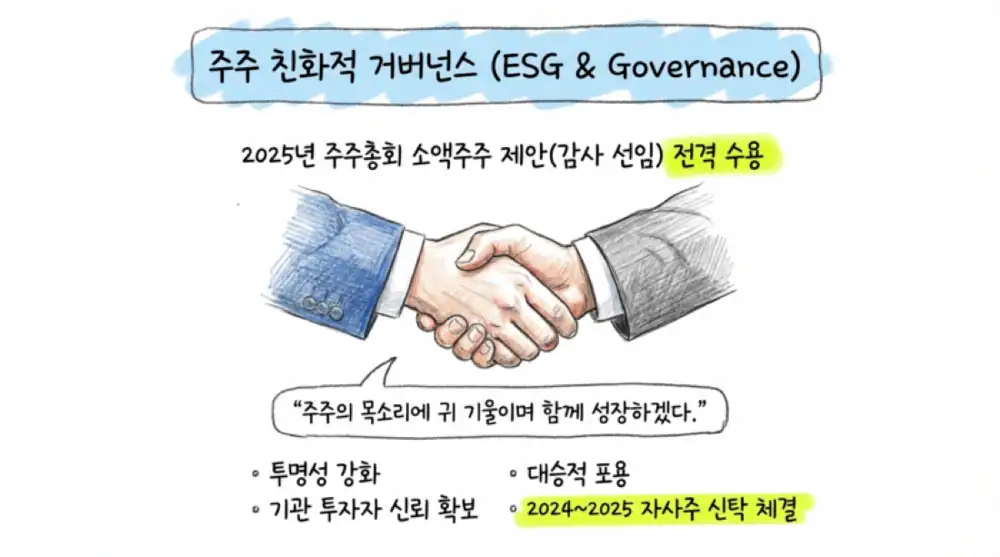

Official fact: After a KRW 2.0 billion share repurchase in 2024, Tplex signed a KRW 3.0 billion treasury-share trust contract with Shinhan Securities in 2025, covering 955,414 shares.

4. History and management: from small metal shop to mid-sized enterprise

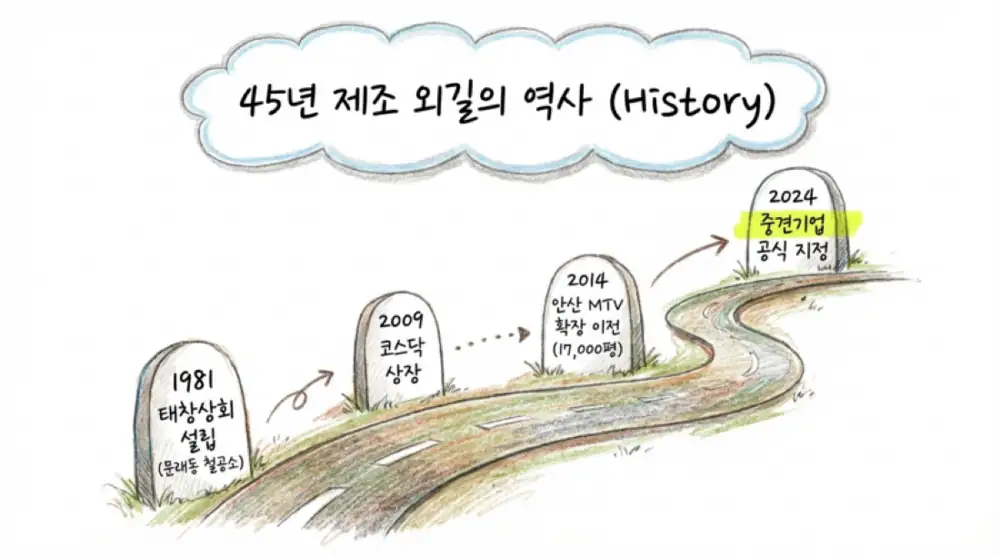

Tplex started in 1981 as Taechang Trading in Mullae-dong, Yeongdeungpo, Seoul, and incorporated as Taechang Stainless in 1991. It changed its name to Tplex in 2007 and listed on KOSDAQ in April 2009.

Official fact: In 2014, the company moved and expanded its headquarters and processing infrastructure to Ansan Siwha MTV on a 17,000-pyeong site. In 2022 it posted record results of KRW 257.7 billion revenue and KRW 21.3 billion operating profit, and in April 2024 it was officially classified as a mid-sized company.

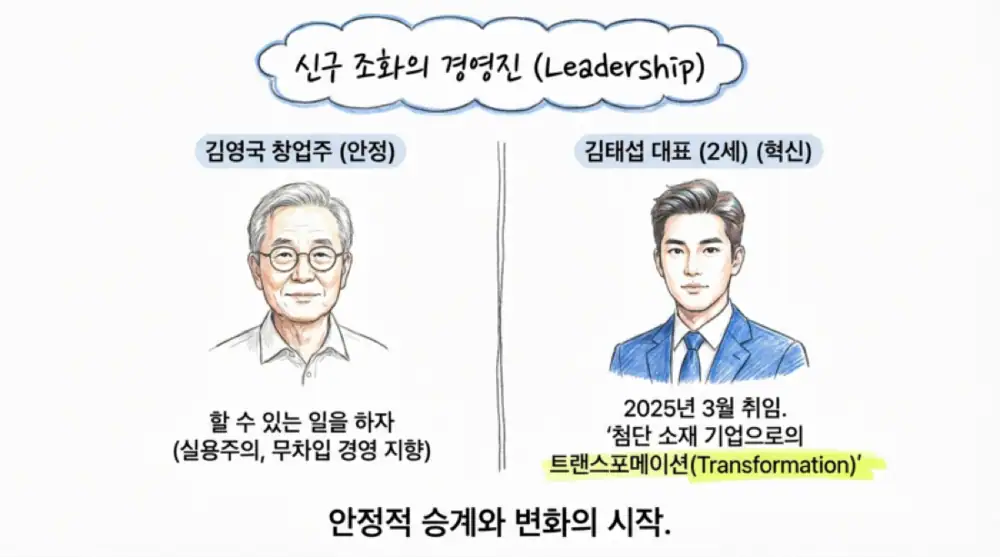

Management is a two-top structure of founder and co-CEO Young-guk Kim and his son and co-CEO Tae-seop Kim. Young-guk Kim built the 1,800-customer base over 45 years and emphasizes practical focus rather than reckless expansion.

Tae-seop Kim became president and CEO on March 31, 2025. The source summarizes his agenda as shareholder friendliness, horizontal communication, safety, and sales focus on plates and special alloys, pushing the company from commodity stainless into advanced rare-metal and special-alloy materials.

5. Shareholders and governance

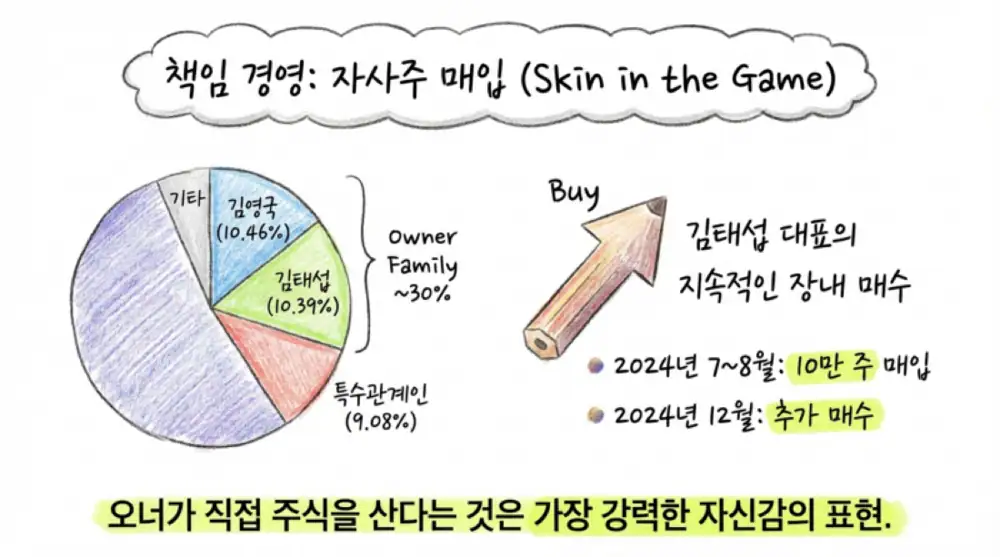

Official fact: As of the second half of 2025, Young-guk Kim held 10.46% or 2,538,401 shares, while Tae-seop Kim held 10.39% or 2,522,358 shares.

| Shareholder | Relationship | Shares | Stake |

|---|---|---|---|

| Young-guk Kim | Founder, co-CEO | 2,538,401 | 10.46% |

| Tae-seop Kim | Second-generation manager, co-CEO | 2,522,358 | 10.39% |

| Tae-soo Kim | Related party | 1,667,452 | 6.87% |

| Young-nam Kim | Related party | 256,014 | 1.05% |

| Other related parties | Young-seok Lee, Hae-soon Jung, and others | 283,664 | 1.16% |

| Total | Largest shareholder and related parties | 7,267,889 | About 29.93% |

On July 11, 2024, Young-guk Kim gifted 1,698,788 common shares, or about 7.25 percentage points, to Tae-seop Kim. Tae-seop Kim then bought 108,902 shares in the market from late July to early August and another 12,350 shares on December 24.

Official fact: At the 2025 annual shareholders’ meeting, a minority-shareholder group holding 1.02% or 248,373 shares proposed Hee-chan Koo as standing auditor, and the board and Tae-seop Kim accepted the proposal and approved the appointment.

Interpretation: Accepting a minority-shareholder-nominated auditor can be read positively by institutions as a governance and accounting-transparency signal.

6. Competition and second-factory strategy

The Korean stainless value chain runs from upstream steelmakers such as POSCO and SeAH Besteel/SeAH Changwon Special Steel to processing centers that cut and distribute materials to end users. Listed peers such as Hwangkum Steel and BNG Steel focus more on plates and thin sheets, while Tplex is stronger in bars and wire.

Official fact: The source states that Tplex is No. 1 in Korea’s stainless bar market with 31.4% share and No. 1 in wire excluding SeAH Special Steel, with about 24% share.

The second factory has three strategic goals: enter higher-value special alloys such as nickel alloys, titanium, and tungsten; expand the plate business; and raise internal processing ratio to reduce cost.

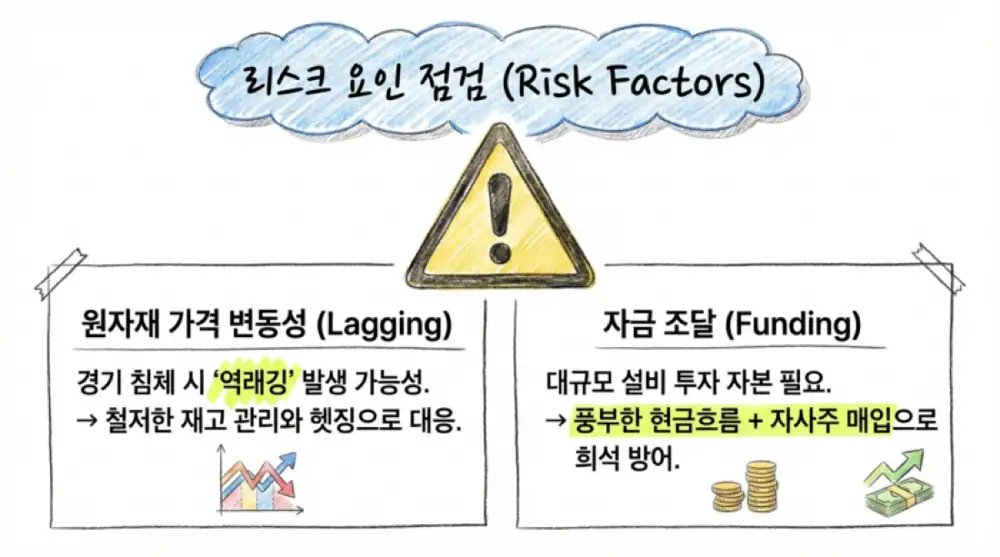

7. Risks: raw-material lagging and financing

- Raw-material price risk: Rising nickel, chromium, and tungsten can lift inventory values and selling prices, but declines can cause negative lagging and inventory write-downs.

- FX risk: Tae-seop Kim identified FX and nickel-price uncertainty as a key management challenge in his New Year message.

- Overhang risk: The provided source text did not explicitly show outstanding CB/BW balances or put-option timing.

- Additional financing: Since major CAPEX such as the second factory is planned, future mezzanine issuance or paid-in capital increases remain variables to monitor.

Interpretation: The 2024 KRW 2.0 billion and 2025 KRW 3.0 billion buybacks, together with stable cash flow, make near-term toxic overhang look lower, but CAPEX scale and funding method still need tracking.

8. Tungsten supply shock and rare-metal option

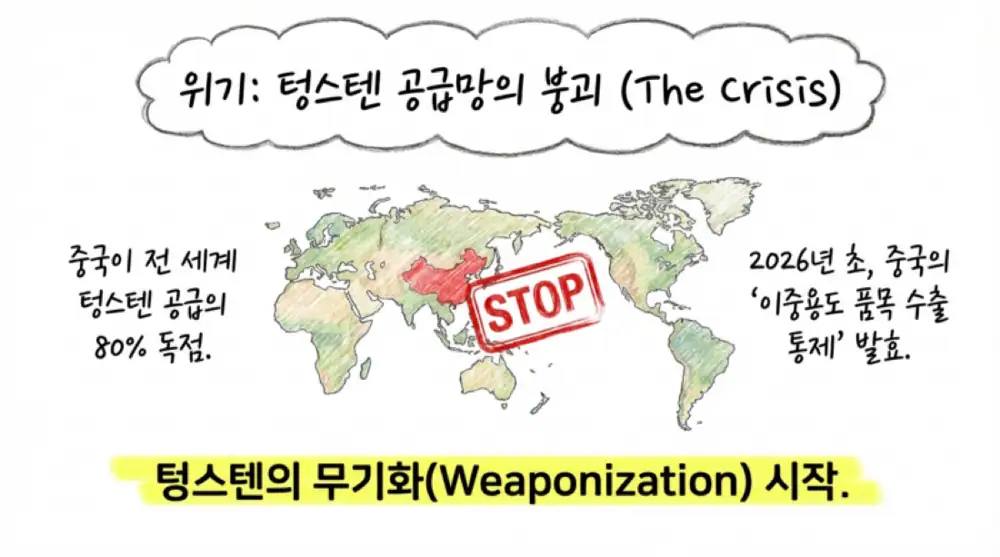

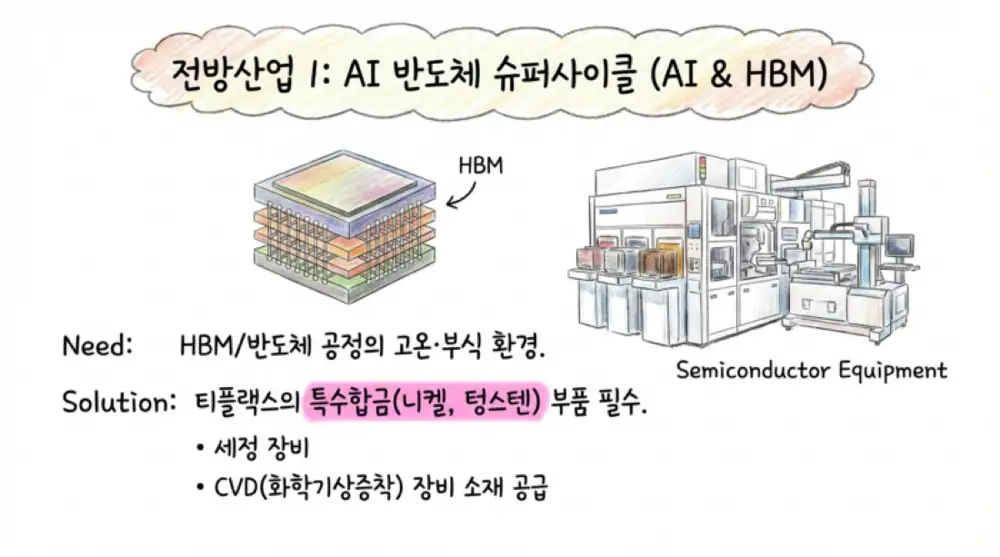

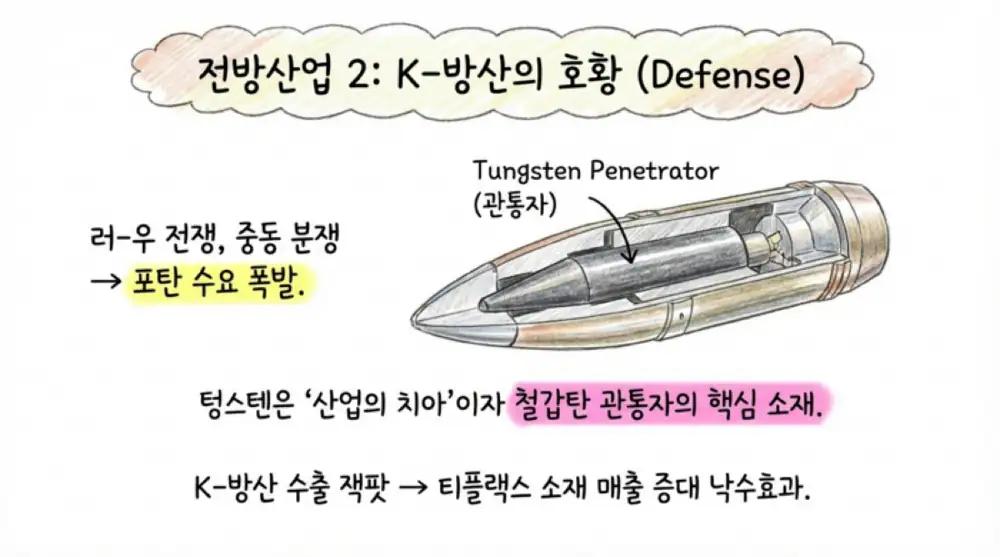

The source identifies the global tungsten crunch and growth in AI semiconductors and defense as the mega trends that can change Tplex’s valuation over the next three years. Tungsten has the highest melting point among metals at 3,422°C and density of 19.3g/cm³, making it essential for cemented-carbide tools, aerospace, semiconductor microcircuits, and armor-piercing defense materials.

Official fact: The source states that China controls more than 80% of tungsten production and more than 90% of processing. In early 2026, China announced a dual-use export-control catalogue and introduced an export-license system limited to 15 approved exporters.

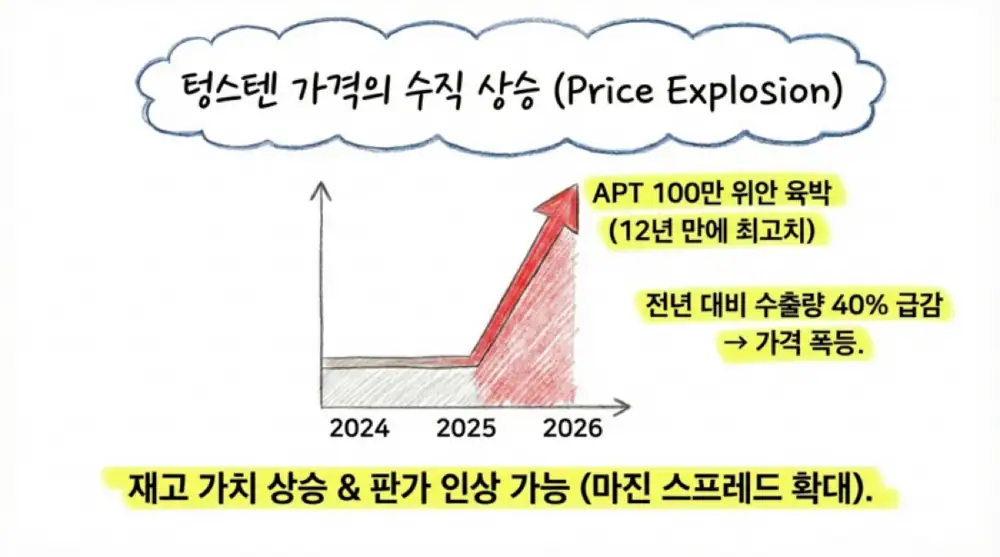

Chinese environmental regulation, a 6.5% mining-output decline, and a 40% export-volume drop pushed APT prices from RMB 500,000-600,000 per ton in mid-2025 to RMB 750,000 in early January 2026 and RMB 990,000 in late January, according to the source. Domestic Chinese prices reached USD 1,125-1,150/mtu and Rotterdam prices exceeded USD 1,100/mtu, a 12-year high.

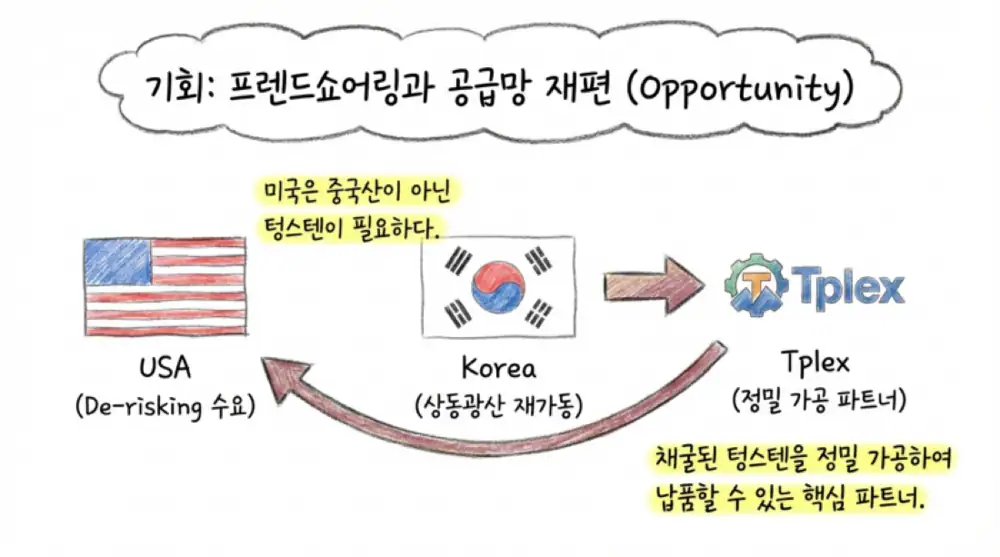

The United States discussed more than USD 30 billion of investment to diversify critical-mineral supply chains away from China, while Korea’s Sangdong tungsten mine in Yeongwol, Gangwon Province is drawing global attention. If a Korean-mined-tungsten-to-US supply chain forms, demand for regional partners that can cut and alloy the material precisely can increase.

9. AI semiconductor and K-defense demand

Samsung Electronics and SK Hynix HBM investment increases demand for stainless, nickel, and tungsten-alloy components used in semiconductor cleaning and CVD equipment. The post-Russia-Ukraine-war expansion of K-defense exports also connects to tungsten carbide and special alloys used in penetrators for armor-piercing shells.

Interpretation: The important point is that Tplex is not just a raw-material trader; it cuts, draws, and processes materials. Tungsten and nickel alloys are difficult to machine, so when supply chains tighten, customers can prefer proven domestic processing partners.

One-line conclusion: Tplex’s preferred growth segment is rare metals and high-value special alloys. The 92.9% increase in 2025 net income is only the starting point; the next proof point is whether the second factory, rare-metal prices, and AI/defense demand actually change the revenue mix.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224195825287

- Interview with founder Young-guk Kim - Edaily: https://www.edaily.co.kr/News/Read?newsId=01338246625898808&mediaCodeNo=257

- Interview with CEO Tae-seop Kim on second factory - ETNews: https://www.etnews.com/20250422000375

- Tae-seop Kim co-CEO interview - Daum: https://v.daum.net/v/0pEsvJc6F7

- Tplex 2025 results - SteelDaily: https://www.steeldaily.co.kr/news/articleView.html?idxno=198363

- Tplex January revenue KRW 24.7B - Chosun Biz: https://biz.chosun.com/industry/business_info/2026/02/23/3V6NR33IDZBEDO5ZIVPCKI5U4Y/

- Tplex diversification review - Newsworker: https://insite.newsworker.co.kr/news/articleView.html?idxno=400484

- Tplex triple increase - SeoulPn: https://go.seoul.co.kr/news/newsView.php?id=20260212500452

- Second factory plan - The Economist Korea: https://economist.co.kr/article/view/ecn202504220024

- Tae-seop Kim treasury-share purchase - FerroTimes: https://www.ferrotimes.com/news/articleView.html?idxno=42774

- Tplex New Year interview - Steel & Metal News: http://www.snmnews.com/news/articleView.html?idxno=563529

- Tplex ownership data - WiseReport: https://comp.wisereport.co.kr/company/c1070001.aspx?cmp_cd=081150&cn=

- Young-guk Kim share gift - FerroTimes: https://www.ferrotimes.com/news/articleView.html?idxno=35621

- Tae-seop Kim share purchase - Steel & Metal News: http://www.snmnews.com/news/articleView.html?idxno=563366

- Tplex second-factory feature - Daum: https://v.daum.net/v/3FbSIkmejK?f=p

- Tae-seop Kim KRW 230B revenue target - FerroTimes: https://www.ferrotimes.com/news/articleView.html?idxno=45549

- Tungsten market outlook - Research Nester: https://www.researchnester.com/kr/reports/tungsten-market/6785

- Tungsten market size - Market Reports World: https://www.marketreportsworld.com/ko/market-reports/tungsten-market-size-research-report-2025-to-2034-14722578

- Tungsten prices have risen 500% - NAI500: https://nai500.com/blog/2026/02/tungsten-prices-have-risen-500-in-a-year-heres-why-the-rally-isnt-over/

- China tungsten export controls - Discovery Alert: https://discoveryalert.com.au/strategic-materials-security-chinas-tungsten-controls-2026/

- China export controls and tungsten prices - BusinessPost: https://www.businesspost.co.kr/BP?command=article_view&num=385352

- Western tungsten scramble - PRNewswire: https://www.prnewswire.com/news-releases/western-tungsten-scramble-heats-up-as-china-locks-down-80-of-global-supply-302685137.html

- Tungsten prices soar - Quest Metals: https://www.questmetals.com/blog/tungsten-prices-soar-to-amidst-chinese-export-curbs-and-global-supply-tightness

- APT price exceeds RMB 750,000 - China Tungsten Online: http://news.chinatungsten.com/jp/tungsten-product-news/174344-jp-776.html

- APT price nears RMB 1,000,000 - China Tungsten Online: http://news.chinatungsten.com/jp/tungsten-product-news/174526-jp-780.html

- Tungsten price at 12-year high - CNews: https://thecommoditiesnews.com/news/articleView.html?idxno=9209

- Sangdong tungsten mine video - YouTube: https://www.youtube.com/watch?v=sScg-i2Hdcw