DEEP RESEARCH · TSI

TSI: Battery-Mixing Equipment Turnaround and Value-Up

A results report on 2025 margin pressure, deferred 2026 orders, Corona Mix, CONEX, CNT dispersions, and the AndaH governance reset

0. Bottom line first

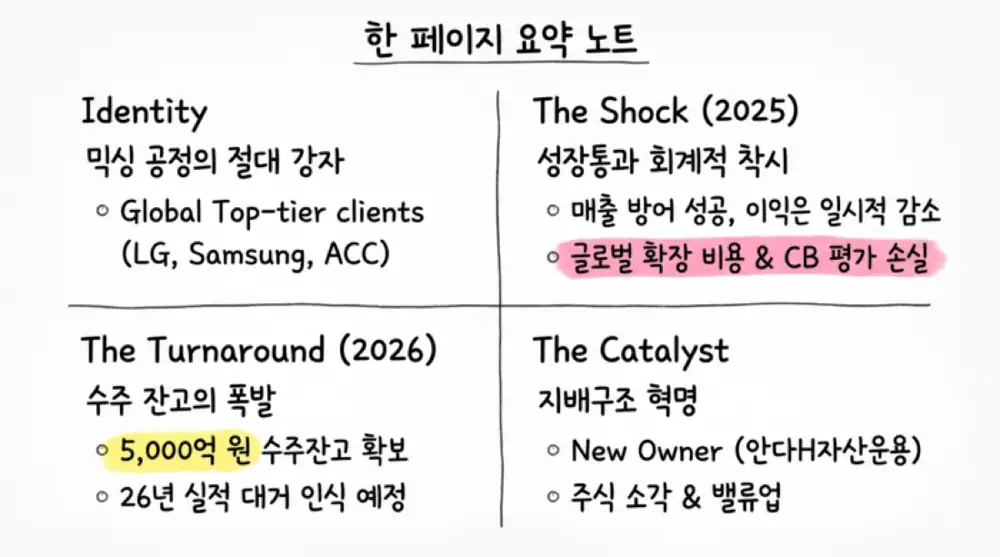

TSI's 2025 numbers show defended revenue but weaker profitability. The source focuses more on the 2026 deferral of a KRW 32.5B overseas mixing-system contract, roughly KRW 500B in backlog, the technology transition from Corona Mix to CONEX and CNT dispersions, and capital-efficiency work under AndaH Asset Management.

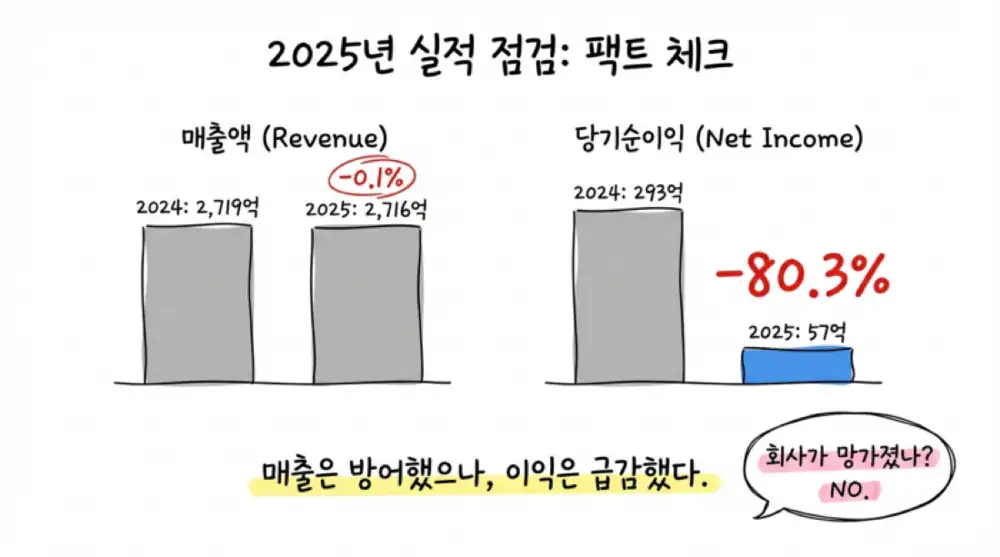

Official fact: 2025 consolidated revenue was KRW 271,611,111,572, down 0.1% YoY. Operating profit was KRW 10,646,702,282, down 31.9%, and net income was KRW 5,774,816,482, down 80.3%.

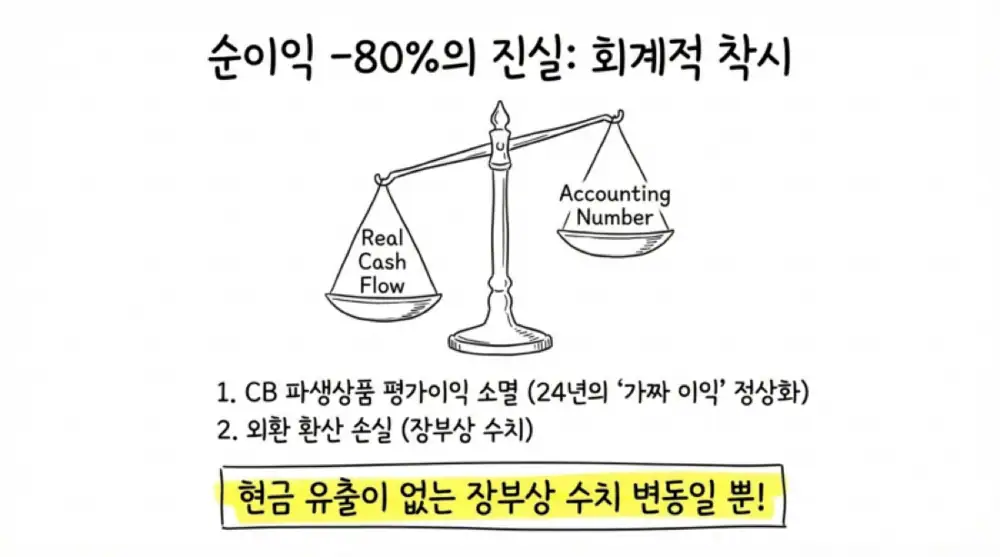

Interpretation: The collapse in net income reads less like a collapse in core revenue and more like growing pains from overseas SG&A, FX movement, and normalization of non-cash derivative gains tied to past convertible bonds.

1. Source Images

All 25 images attached to the source are preserved below. The equipment and disclosure screenshots can be checked in their original sequence.

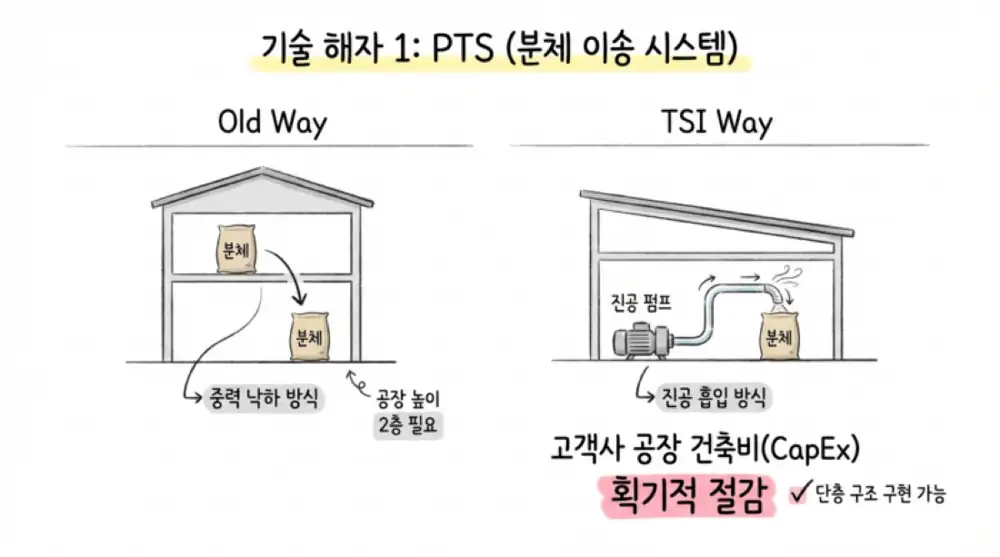

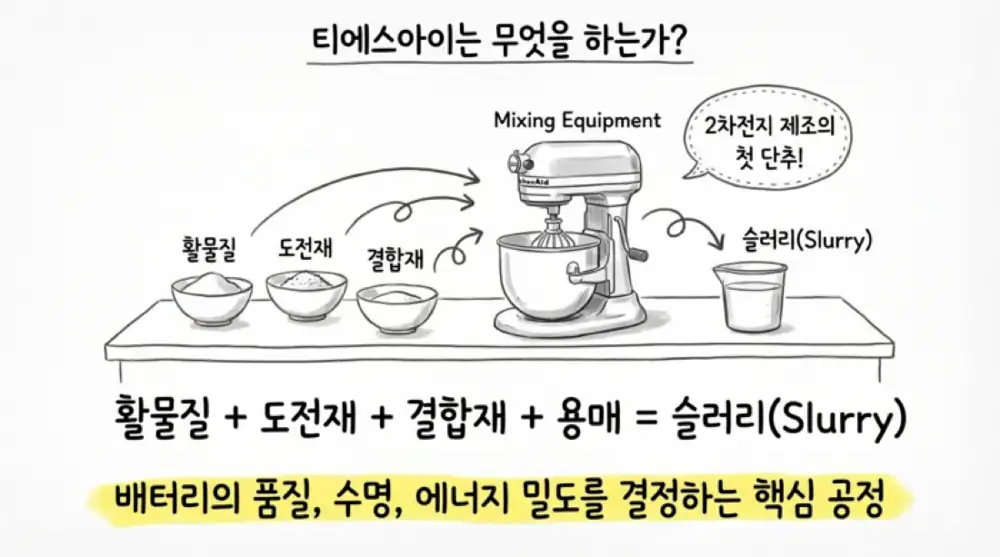

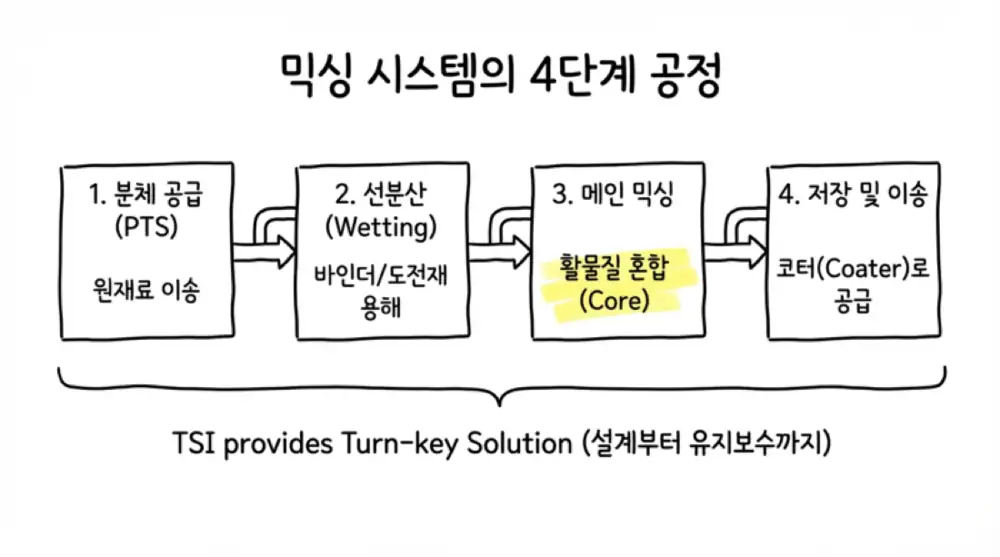

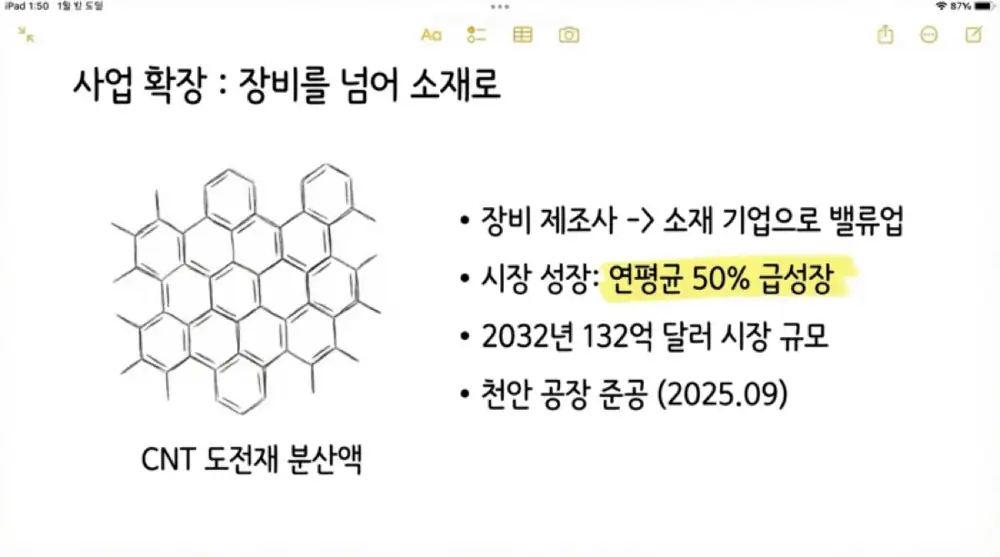

2. Technology Moat and Product Transition

Powder supply

A vacuum-pump Powder Transfer System improves metering and cleanliness even in single-floor plant layouts.

Pre-mixing

An inline process wets powder quickly, shortens dissolution time, and suppresses binder gel formation.

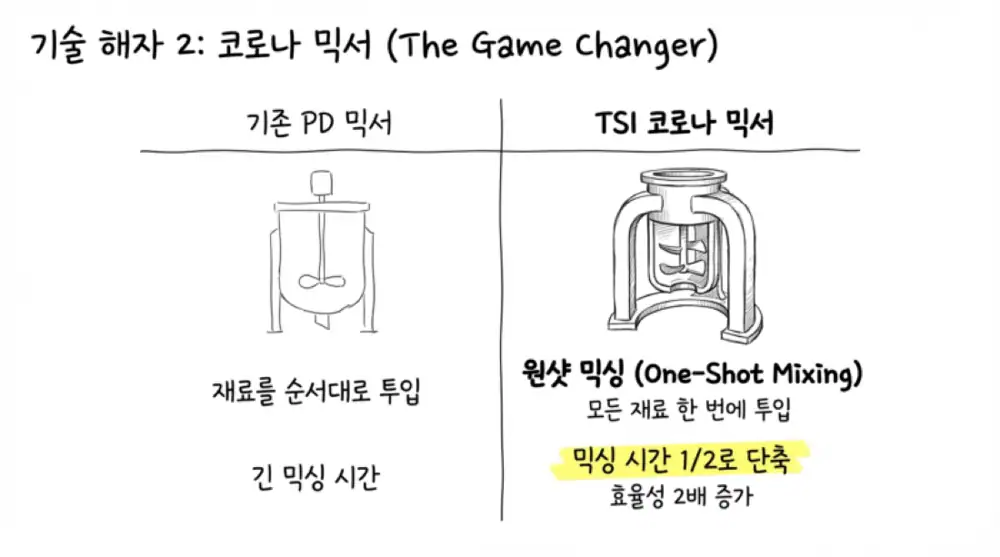

One-shot mixing

The source says it cuts mixing time to less than half of conventional PD mixers and offers more than twice the mixing efficiency of competing core products.

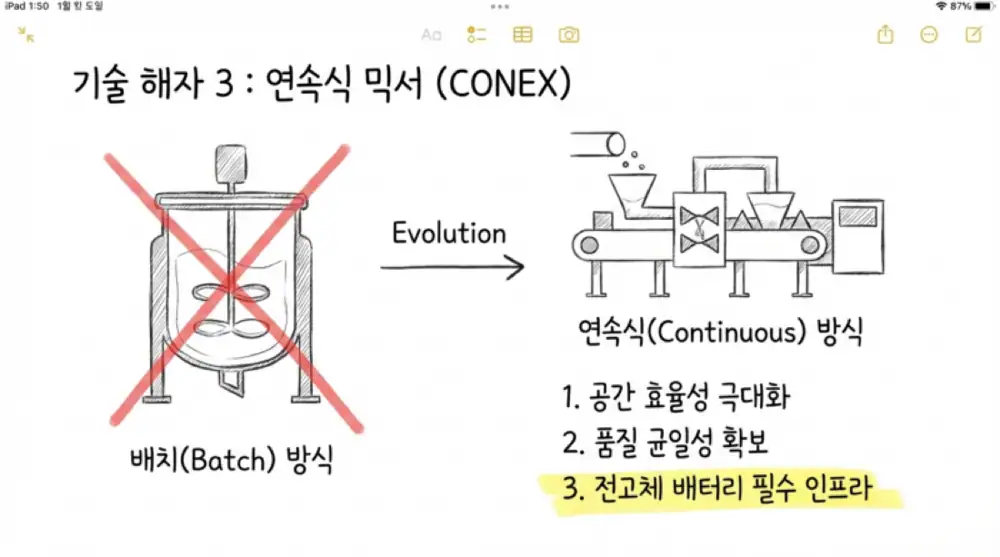

Continuous mixing

A next-generation process that continuously feeds powder and solvent, mixes slurry in real time, and sends it to the coater.

The source says TSI has references with global cell makers such as LG Energy Solution, Samsung SDI, and Europe's ACC. Once the equipment is verified, mass-production references and joint R&D history become barriers to entry.

Official fact: In the source, CNT conductive dispersion demand is expected to grow from 16,000 tons in 2022 to 881,000 tons in 2032, with the related market exceeding USD 13.2B by 2032.

Interpretation: The move from equipment into materials makes sense because mixing-equipment operating data and fluid-dynamics know-how can be applied directly to CNT dispersion processes. The Cheonan North BIT campus and pilot line are the test bed for that shift.

3. 2025 Results Diagnosis

| Item | 2024 | 2025 | Change |

|---|---|---|---|

| Revenue | KRW 271,986,540,655 | KRW 271,611,111,572 | -0.1% |

| Operating profit | KRW 15,629,831,816 | KRW 10,646,702,282 | -31.9% |

| Pre-tax profit | KRW 35,274,810,480 | KRW 6,428,312,943 | -81.8% |

| Net income | KRW 29,340,169,510 | KRW 5,774,816,482 | -80.3% |

| Total assets | KRW 366,093,197,831 | KRW 303,438,357,431 | -17.1% |

| Total liabilities | KRW 240,704,512,502 | KRW 175,578,337,489 | -27.0% |

| Total equity | KRW 125,388,685,329 | KRW 127,860,019,942 | +2.0% |

- Revenue was about KRW 271.6B, nearly flat YoY. Given the EV demand chasm, the source reads this as solid revenue defense from backlog-based percentage-of-completion recognition.

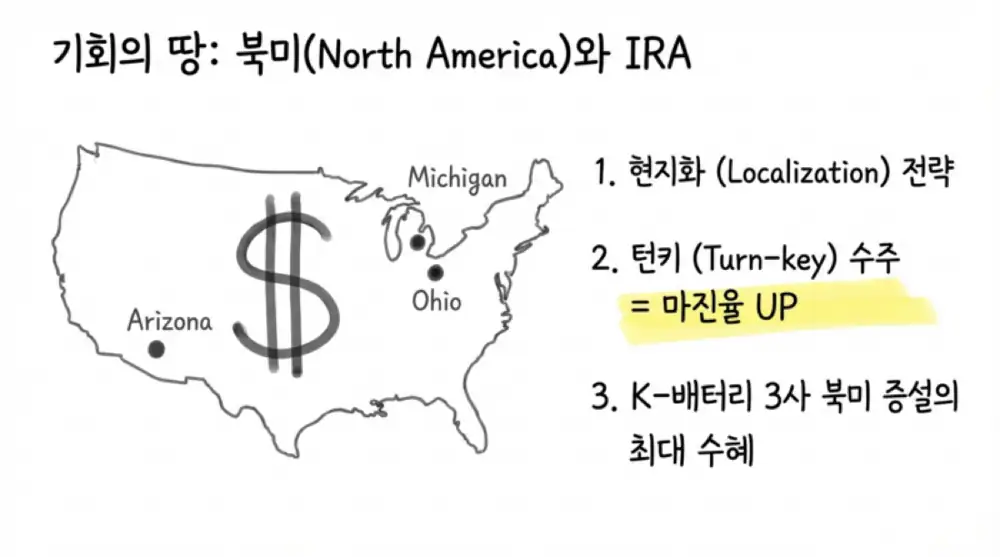

- The key reason for operating-profit decline is higher SG&A. The source points to Pyeongtaek and Cheonan campuses plus overseas entities in Michigan, Ohio, Poland, France, and Hungary.

- The source states exports were more than 91% of cumulative 3Q25 revenue, about KRW 180B, so FX translation can materially affect pre-tax earnings.

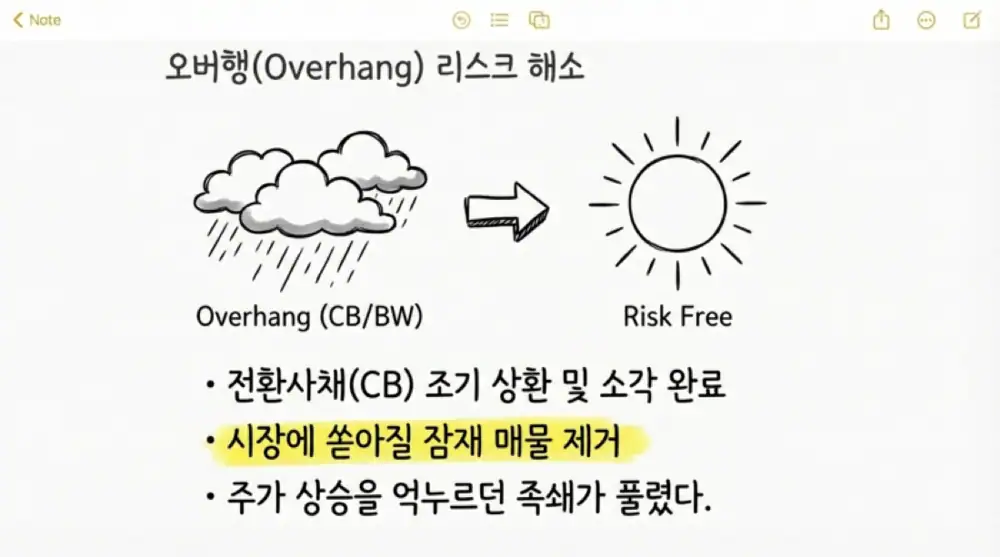

- Past private unsecured CB issuance from the 2nd through 6th tranches totaled KRW 58B. Derivative gains from these instruments inflated 2024 earnings, and early redemption and cancellation reduced that non-cash benefit in 2025.

4. 2026 Order Momentum

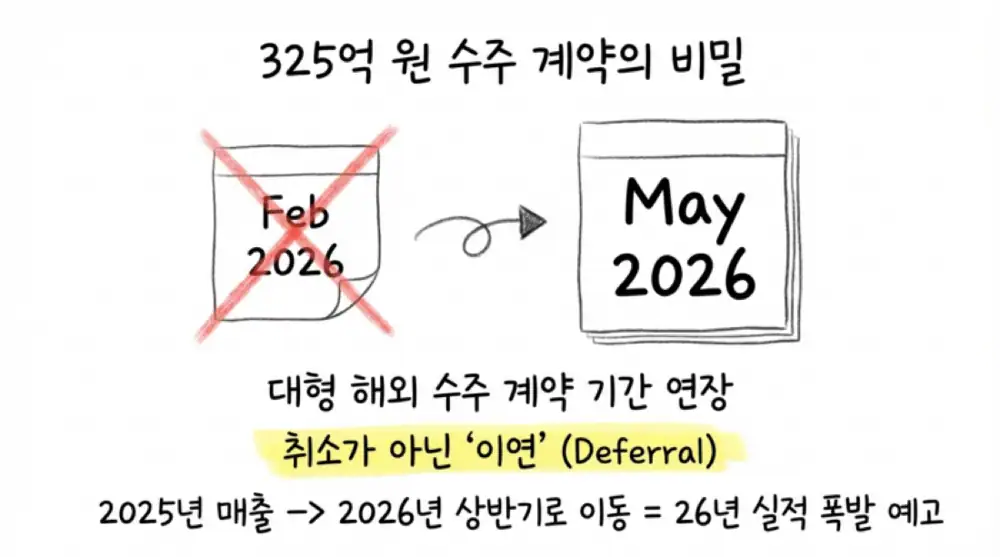

The representative case is an overseas battery-company mixing-system contract worth KRW 32,519,354,400, or USD 24,524,400. It equals 21.86% of recent revenue, and the end date was extended by about three months from February 28, 2026 to May 31, 2026.

| Item | Detail |

|---|---|

| Payment structure | 30% down payment, 40% first progress payment, 20% second progress payment, 10% final payment |

| Cash-flow read | The source says 90% can be collected before or around equipment shipment |

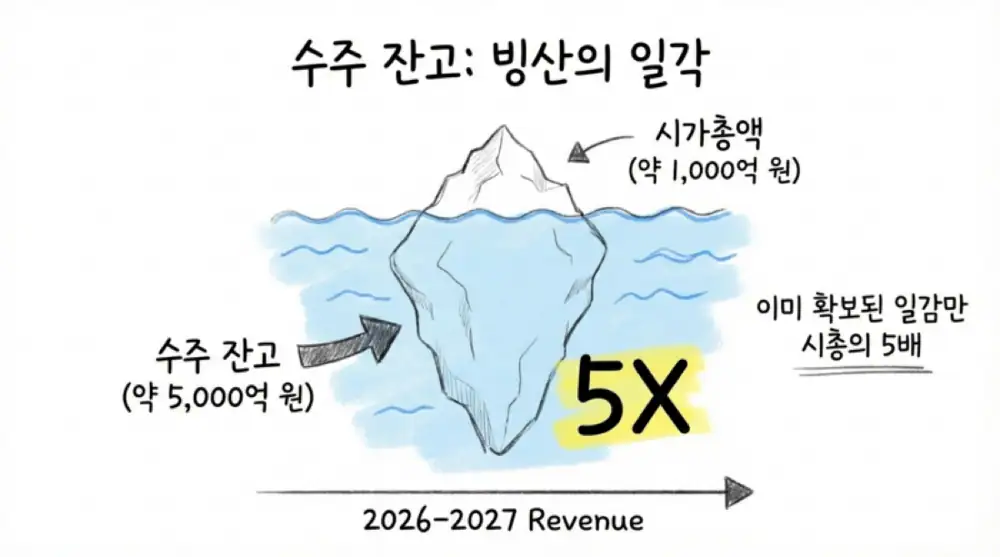

| Backlog | About KRW 500B, roughly five times market cap in the source estimate |

| North America | The source says TSI is known to have secured more than KRW 100B of orders around Arizona and other North American sites |

Interpretation: A contract extension is often caused by customer plant construction, utility connection, and SAT scheduling rather than equipment-vendor fault. The source therefore reads it as 2025 revenue recognition moving into 1H26, with operating leverage to follow.

5. Governance and Shareholder Return

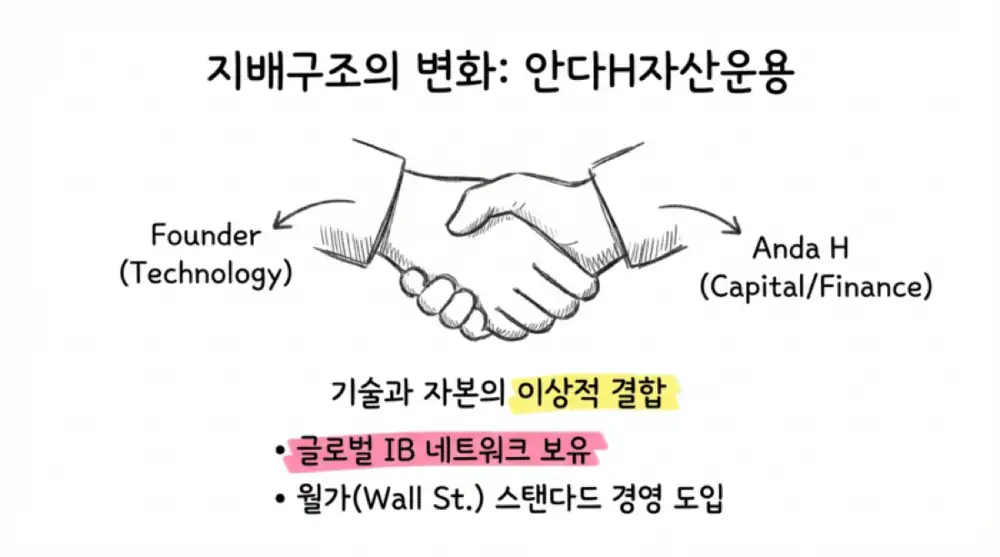

- In 2023, control shifted from founder and CEO Pyo In-sik's owner-led structure to AndaH Private Investment Trust No. 6, managed by AndaH Asset Management.

- The source interprets Chairman Choi Kwon-wook's Hong Kong network, Samjong KPMG financial due diligence, GLG business due diligence, and global IB network as sales and capital-efficiency catalysts.

- The AndaH structure keeps Pyo In-sik's engineering and customer relationships while capital-market professionals oversee allocation and risk.

- At the October 2025 extraordinary shareholders' meeting, AndaH executive Sohn Byung-joon was appointed as a non-executive director and audit committee member.

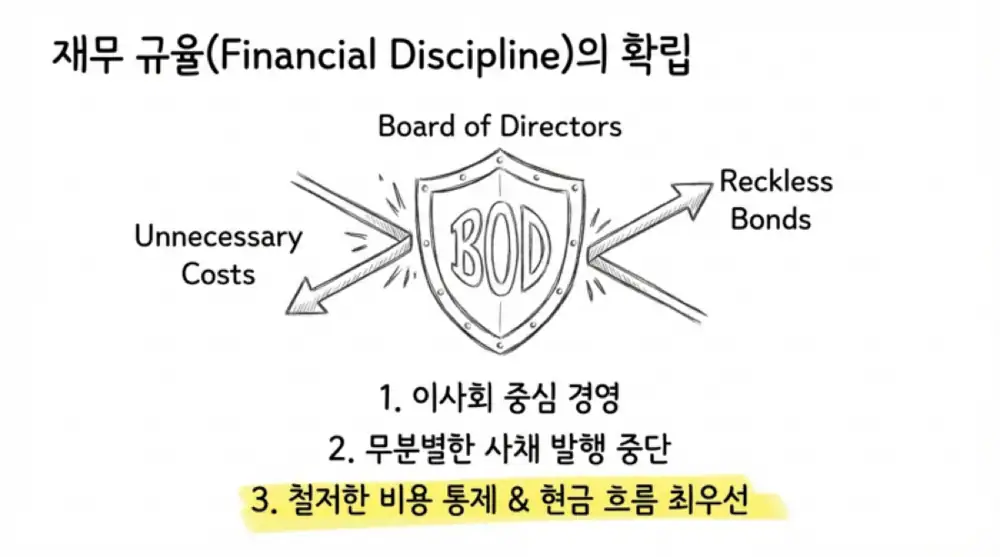

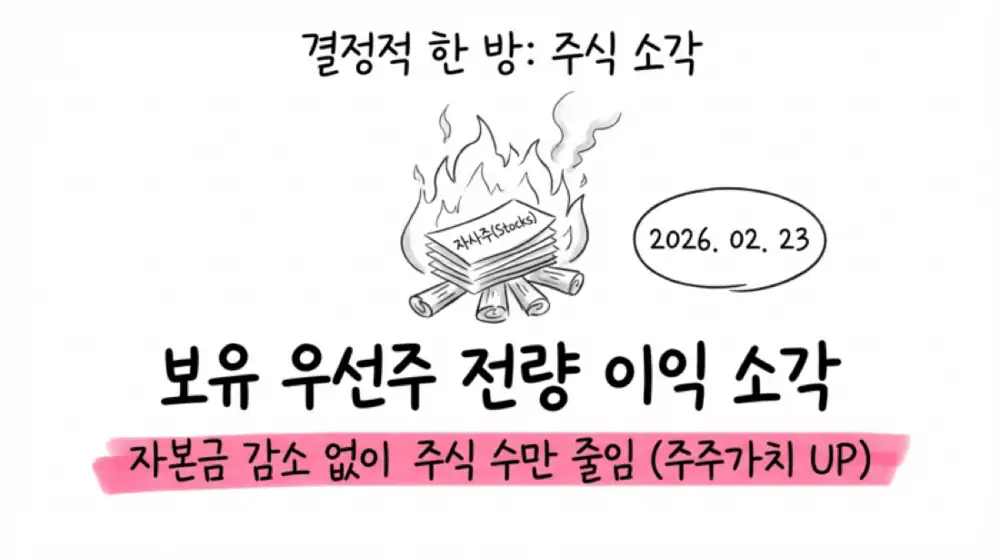

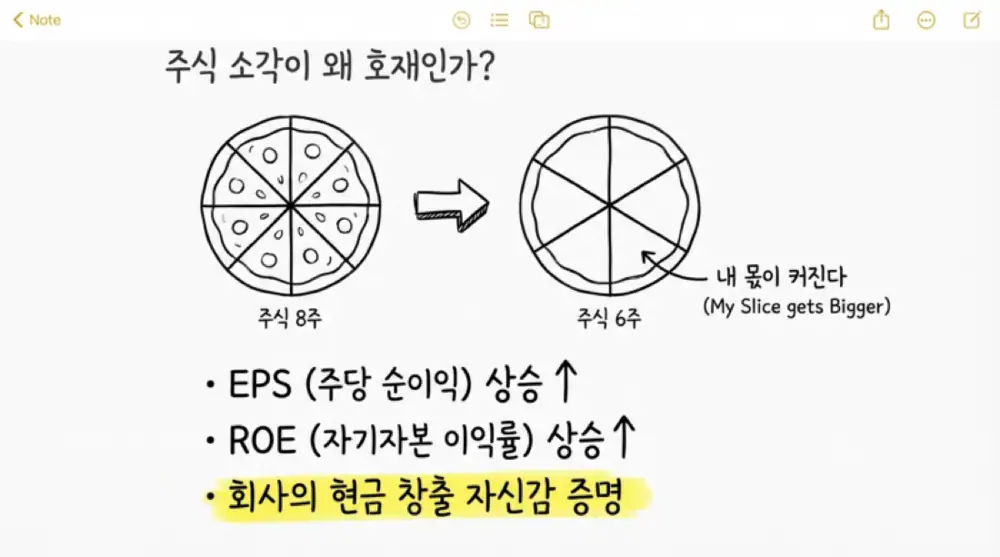

- The source also includes the February 2, 2026 share-cancellation decision, the February 23 cancellation of all preferred treasury shares, SK Securities as broker, and Commercial Act Article 343 paragraph 1 as the legal basis.

- From 2024 to 2025, TSI used call options to acquire and cancel outstanding CBs from the 2nd through 6th tranches before maturity; the preferred-share cancellation is framed as the final action in removing overhang.

6. My Conclusion

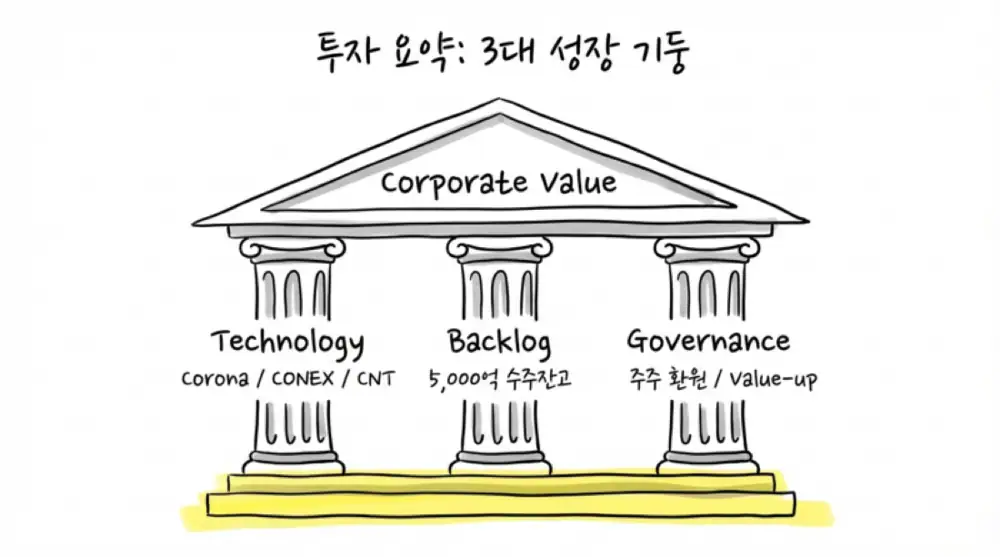

In 2025, TSI absorbed higher SG&A, FX movement, and the loss of accounting valuation gains. But the technology path is moving from PD mixers to Corona Mix, CONEX, dry electrodes, and CNT dispersions, while the KRW 32.5B contract and roughly KRW 500B backlog can support 2026 revenue recognition.

Interpretation: The real question is not the 80.3% decline in 2025 net income alone. It is whether backlog, technology transition, and capital-structure cleanup are all moving together behind that number.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224195822841

- Source 2: https://www.edaily.co.kr/News/Read?newsId=02706006642072816&mediaCodeNo=257

- Source 3: https://www.researchandmarkets.com/reports/5939084/secondary-batteries-market-report

- Source 4: https://www.technavio.com/report/secondary-battery-market-industry-analysis

- Source 5: https://contents.premium.naver.com/thebell/stock/contents/230220182920225ij

- Source 6: https://economychosun.com/site/data/html_dir/2016/04/04/2016040400007.html

- Source 7: https://kr.investing.com/news/stock-market-news/article-861102

- Source 8: https://cm.asiae.co.kr/article/2021011411324194875

- Source 9: https://plus.hankyung.com/apps/newsinside.view?aid=202303213206a&category=&sns=y

- Source 10: https://www.judal.co.kr/?view=stockAI&shareToken=wbMf62P6eEo0ZLDP

- Source 11: https://www.globalepic.co.kr/view.php?ud=202502210943207858abe7dc9896_29

- Source 12: http://www.andaasset.com/child/sub/member/team-view.php?idx=23

- Source 13: https://www.forbeskorea.co.kr/news/articleView.html?idxno=300733

- Source 14: https://v.daum.net/v/xFkhPmNdIA?f=p