DEEP RESEARCH · COSMAX BTI

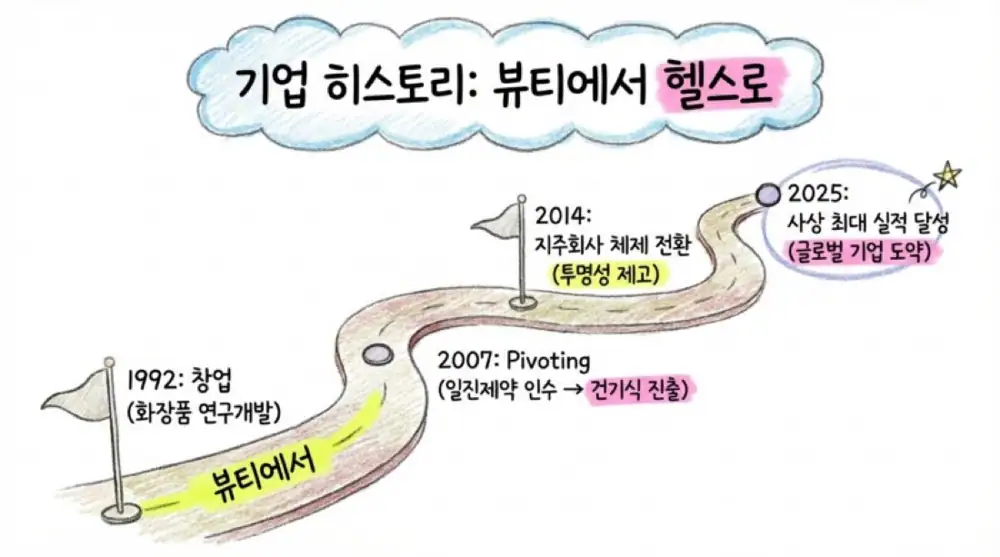

COSMAX BTI: Holding-Company Turnaround Across K-Beauty and K-Health

A review of 2025 record earnings, global ODM expansion and the KRW 150B convertible-bond overhang.

0. Bottom line first

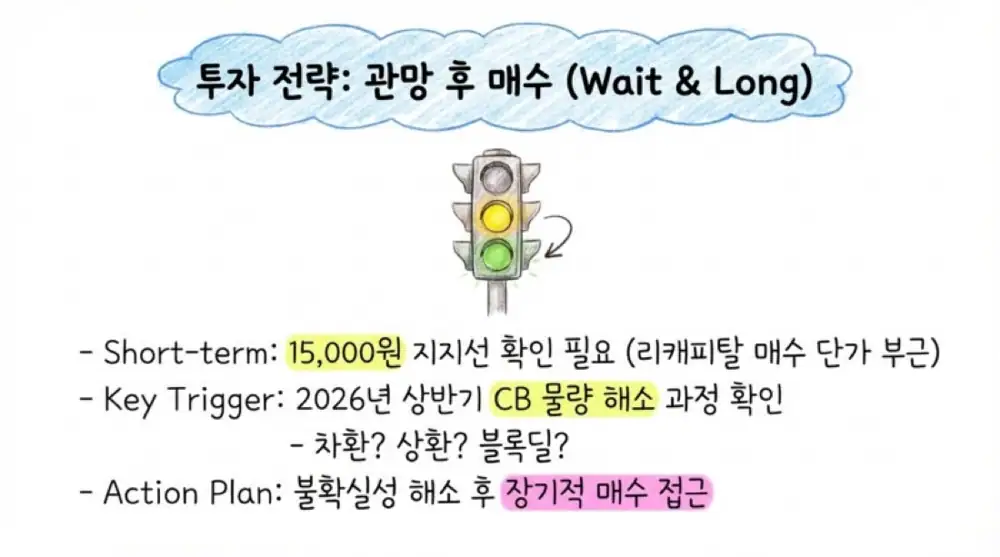

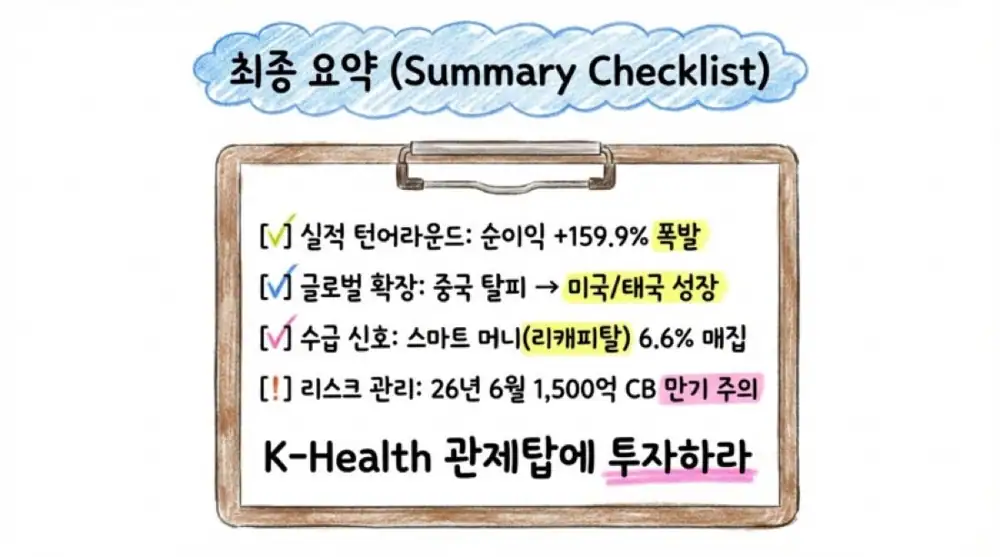

COSMAX BTI is the control tower that can extend the group’s leading K-beauty ODM infrastructure into K-health and supplements. The 2025 turnaround is strong, but the KRW 150 billion CB maturing in June 2026 and its KRW 15,279 conversion price are the key supply risk.

1. Macro and top-pick logic

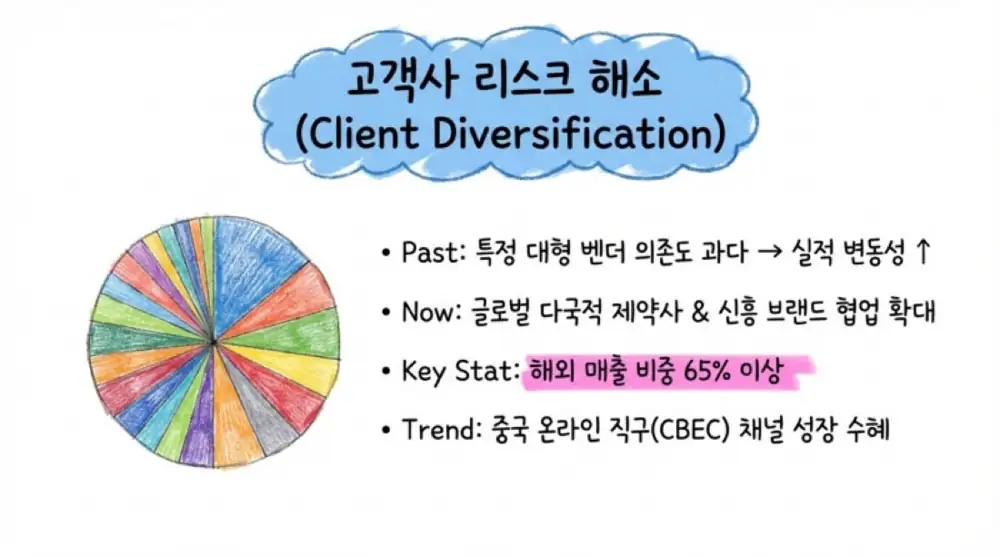

The source frames global aging, longer healthspan demand and self-medication as the demand drivers for supplements. COSMAX uses China, the U.S. and Southeast Asian routes to raise global penetration of K-beauty and K-health.

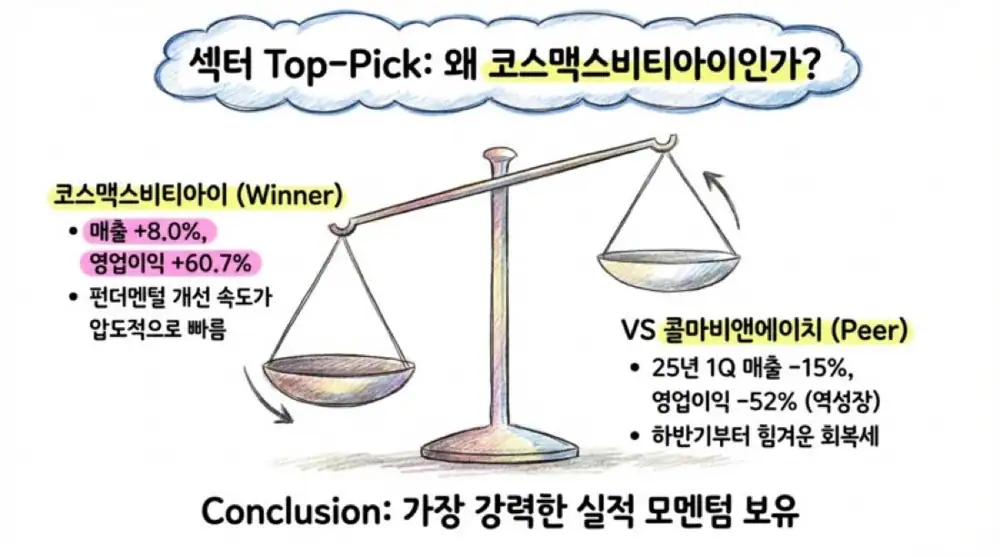

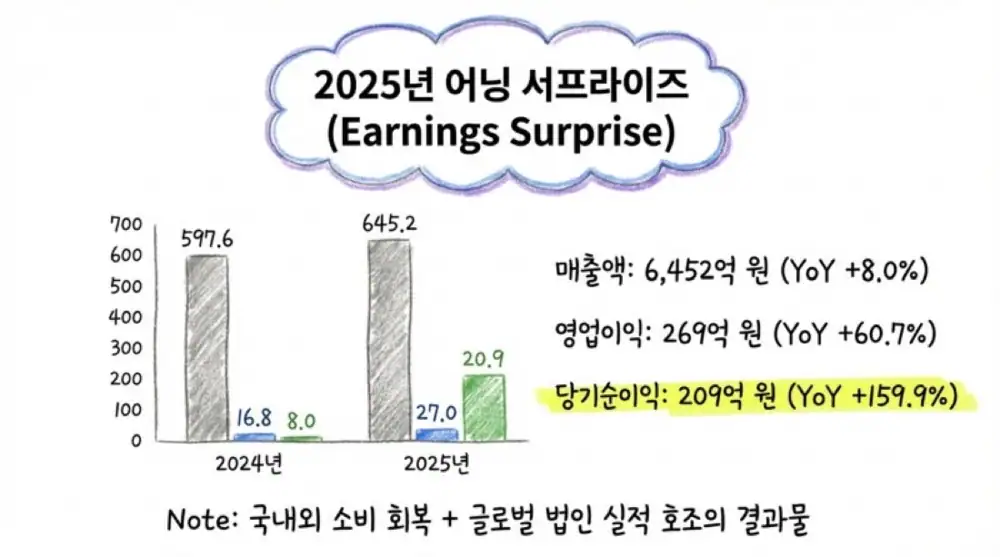

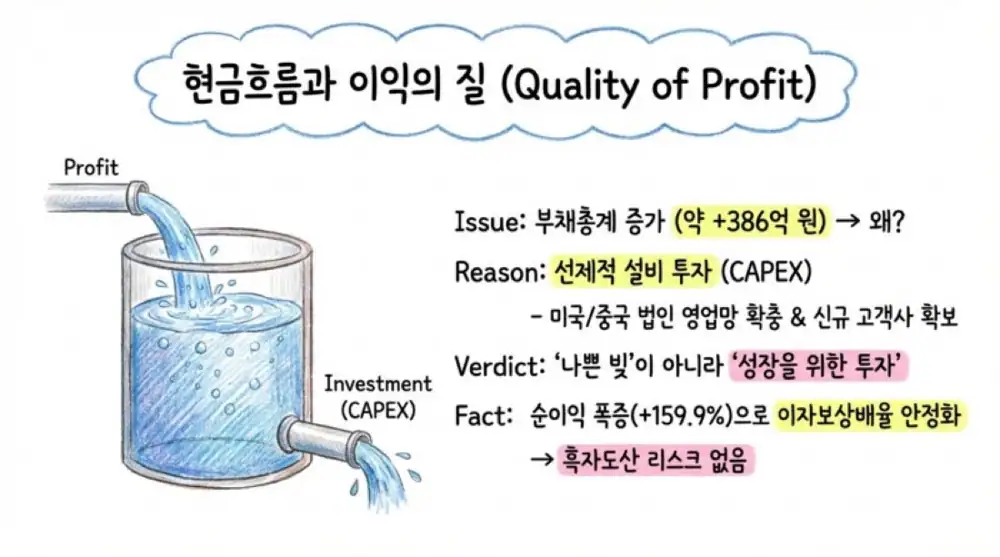

Official fact: The source cites 2025 consolidated revenue of KRW 645.2 billion, up 8.0% YoY, operating profit of KRW 26.9 billion, up 60.7%, and net income of KRW 20.9 billion, up 159.9%.

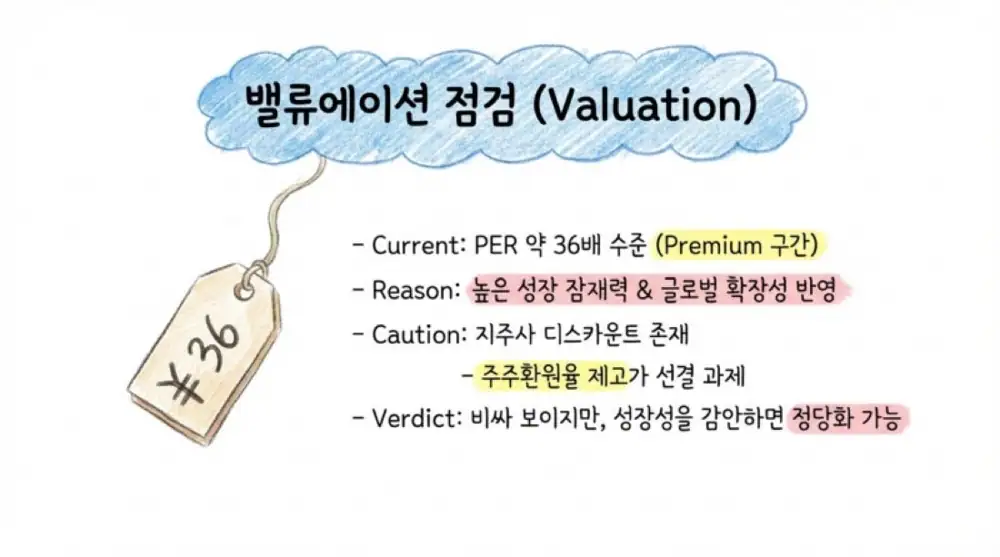

Interpretation: The turnaround looks strong versus Kolmar BNH’s weak Q1 2025 revenue of KRW 136.7 billion, down 15%, and operating profit of KRW 3.6 billion, down 52%. The caveat is valuation risk after the stock reached around 36x PER.

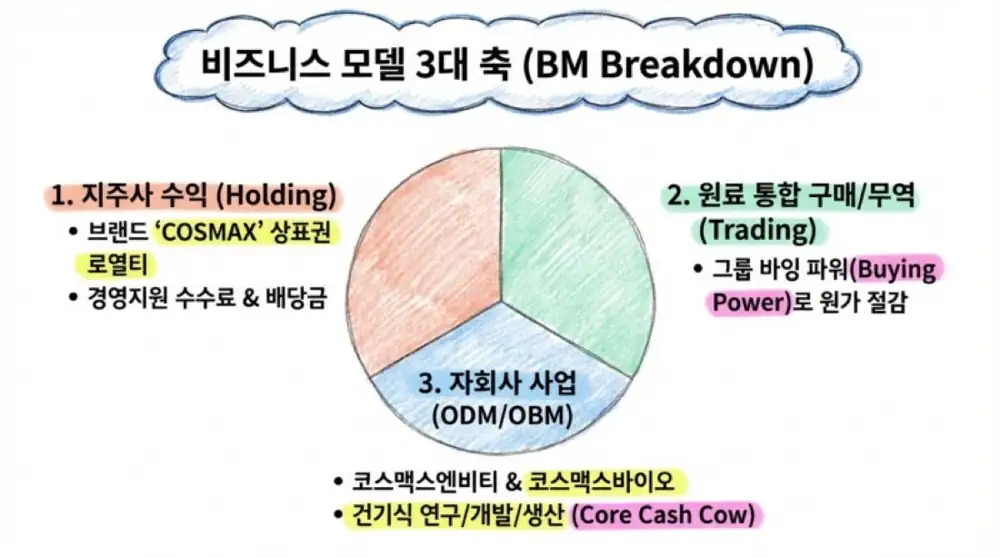

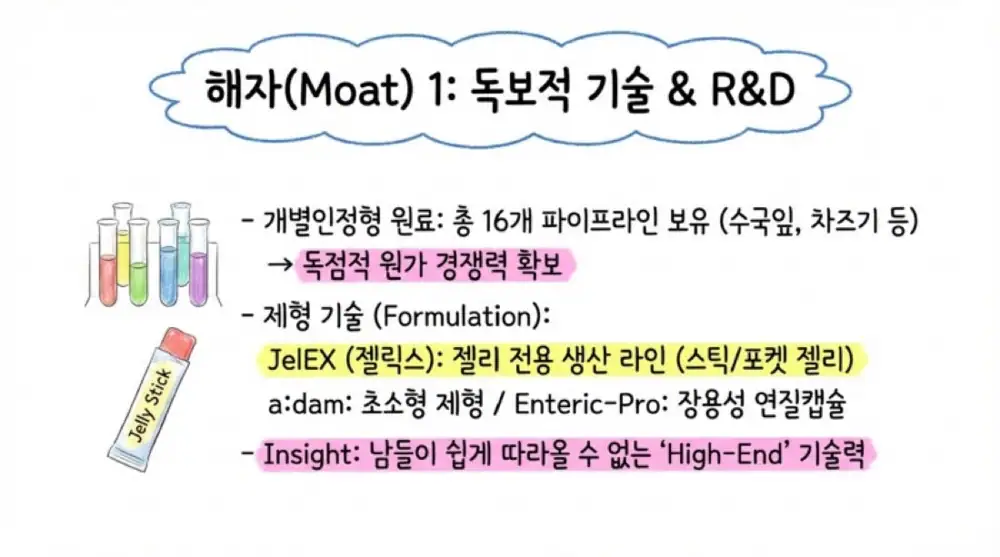

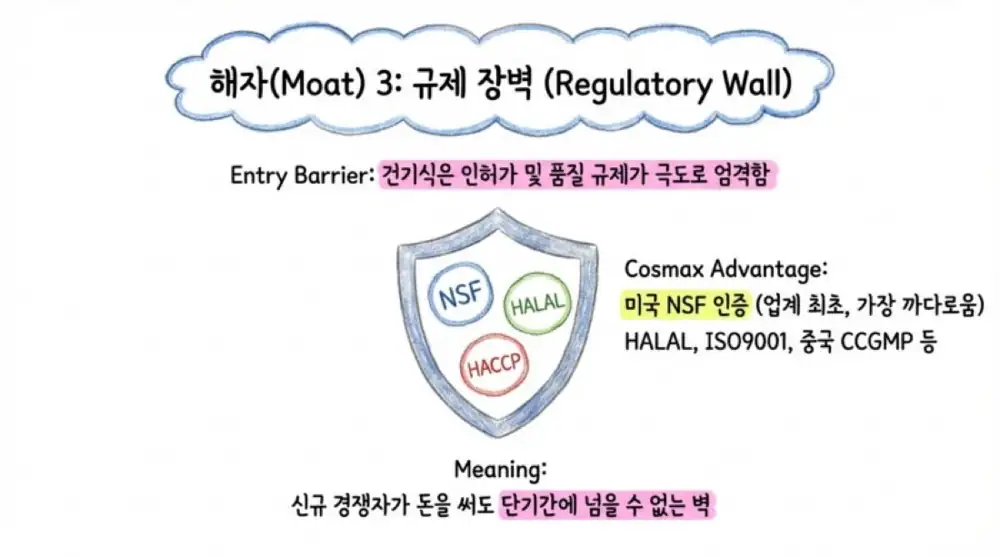

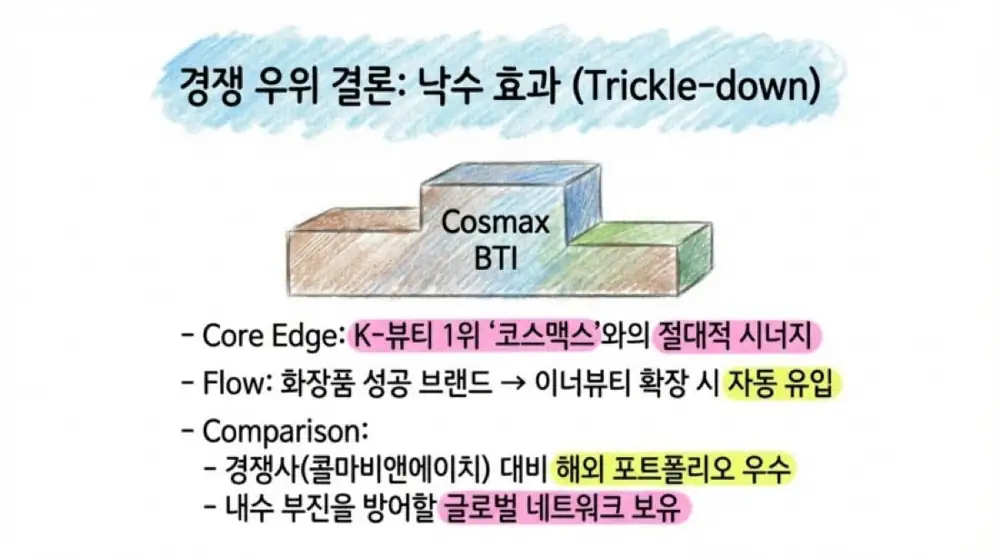

2. Business structure and moat

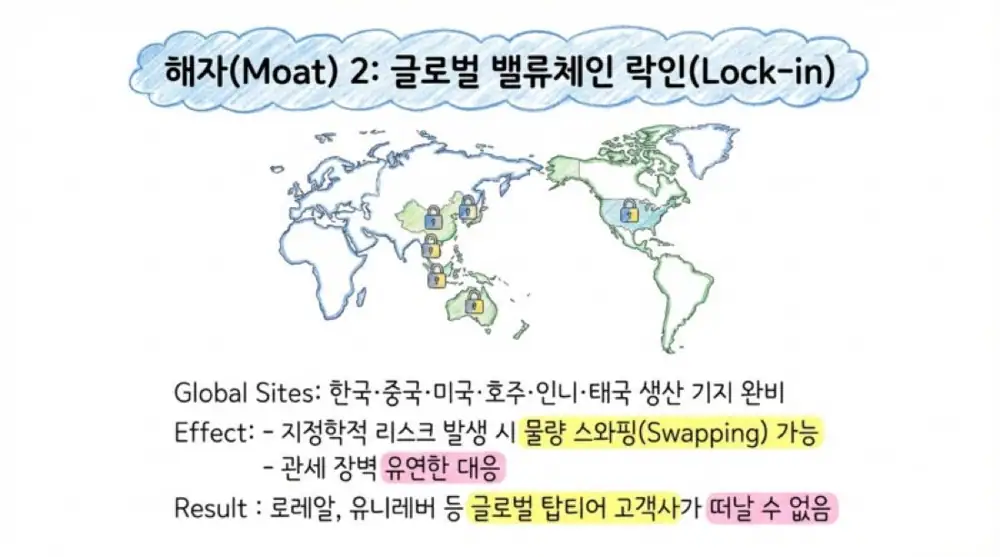

Global value-chain lock-in

The production network across Korea, China, the U.S., Australia, Indonesia and Thailand makes vendor switching harder.

COSMAX spillover

K-beauty indie brands can use group supplement infrastructure when expanding into inner beauty.

Green bio

The Seungju green-bio knowledge industrial center, targeted for completion by end-2027, is a policy catalyst.

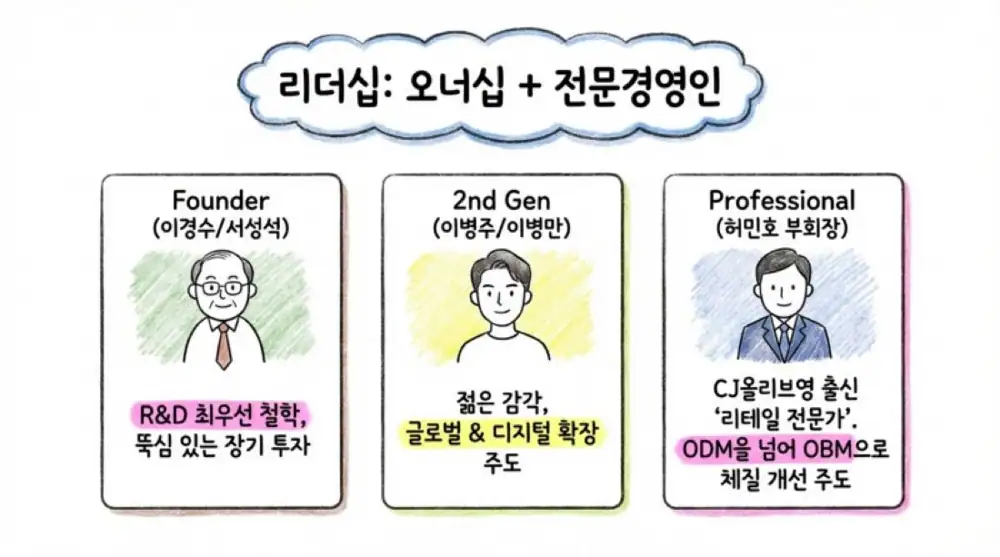

3. Governance and financing

| Item | Detail |

|---|---|

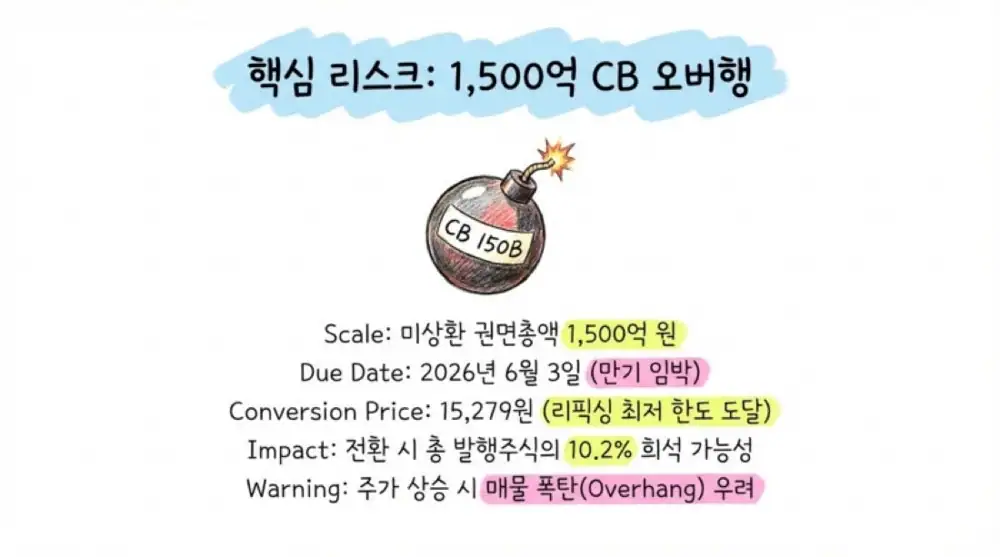

| CB | 1st unsecured private convertible bond, issued 2021-06-03, maturing 2026-06-03 |

| Amount | KRW 150,000,000,000 |

| Conversion price | KRW 15,279 |

| Investors | Mirae Asset Securities and six other institutions |

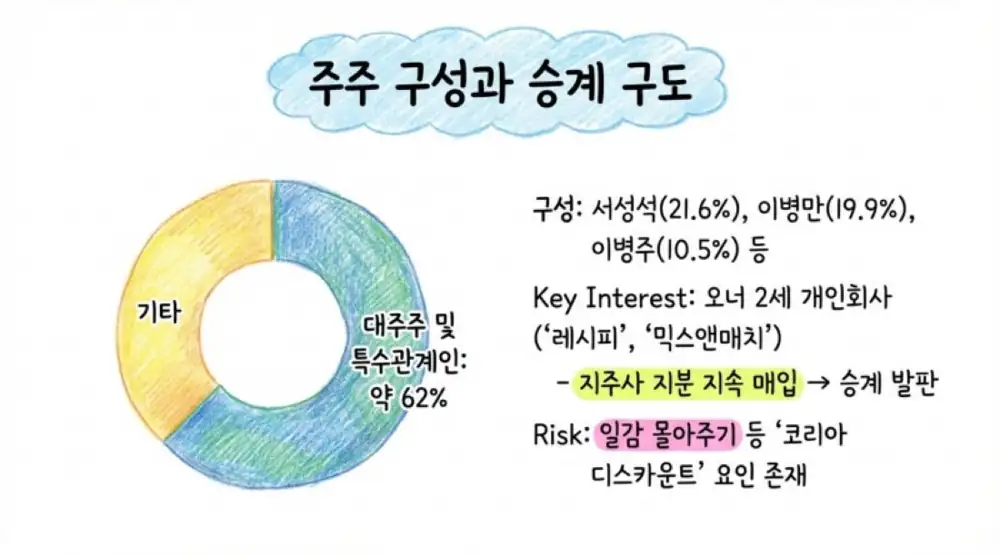

| Shareholder | Stake | Note |

|---|---|---|

| Suh Sung-suk | 21.62% | Effective largest shareholder |

| Lee Byung-man | 19.95% | Second generation owner |

| Lee Byung-joo | 10.52% | CEO/president |

| COSM&M | 9.43% | Family company |

| ReCapital and others | 6.61% | Financial investors |

Interpretation: With related-party ownership near 62%, control risk is low, but a thin float plus conversion of roughly 980,000 CB shares could create an overhang wall.

4. Risks and strategy

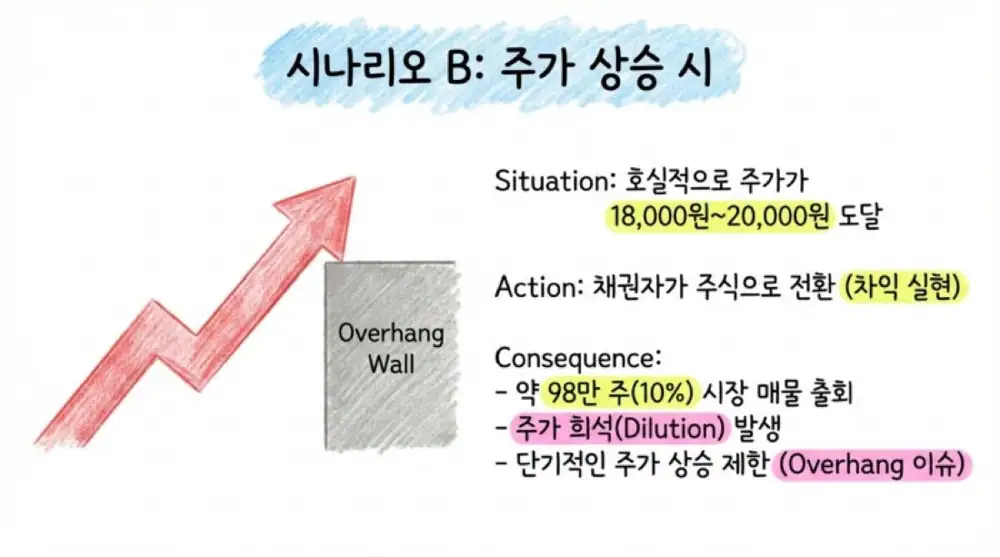

- If the stock moves strongly above KRW 15,279 toward KRW 18,000-20,000, CB conversion and profit-taking become more likely.

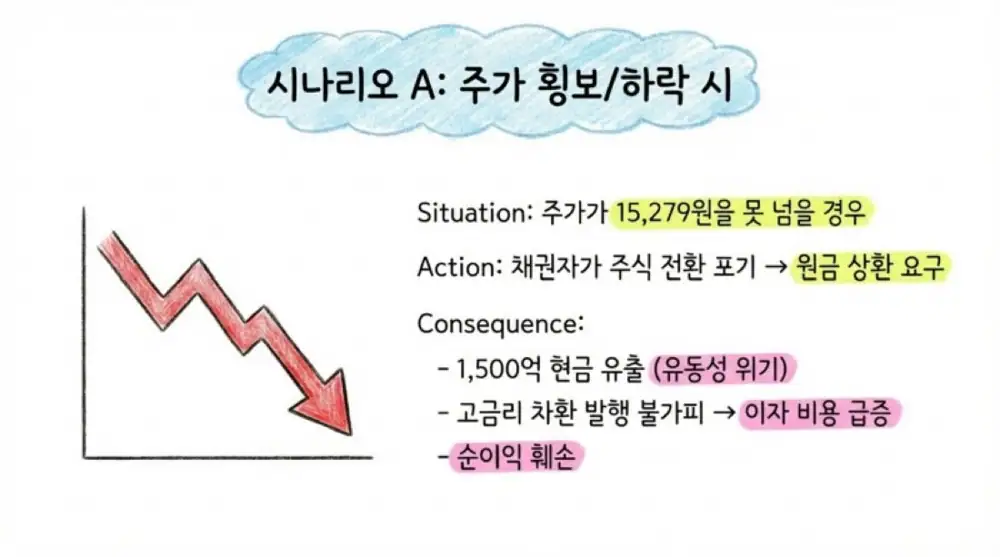

- If the stock remains below the conversion price, maturity repayment can become a liquidity issue.

- The source mentions strategic long entry after confirming support; this is the author’s scenario, not advice.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224194569510

- Reference 2: https://lh7-rt.googleusercontent.com/docsz/AD_4nXedClWPJYv5wOrnsgc9zXWvuwm6CBDxhokcWtMVu9_fc7ypWxLaK4QccNJEmg7QxWYHUDbYQTmzxKRXo6s6GHV1jkATZB_rJUWJyYDbzc4gLGfEh7mVtpb_QIfiP1rjPDor79FSghCdG_XOq4MiIQw_CJ4oMlY?key=36Btp9W4GD33zgvC5U8ifA"/

- Reference 3: https://www.kyosu.net/news/articleView.html?idxno=155091

- Reference 4: https://www.fetv.co.kr/news/article.html?no=213285

- Reference 5: https://www.mstoday.co.kr/news/articleView.html?idxno=100649

- Reference 6: https://m.finance.daum.net/quotes/A044820/news/stock/20251120112311470

- Reference 7: https://m.irgo.co.kr/IR%EC%9E%90%EB%A3%8C/71667/TB/%EC%BD%94%EC%8A%A4%EB%A7%A5%EC%8A%A4-%EC%BD%94%EC%8A%A4%EB%A7%A5%EC%8A%A4-%EA%B8%B0%EC%97%85%EA%B0%80%EC%B9%98%EC%A0%9C%EA%B3%A0%EA%B3%84%ED%9A%8D

- Reference 8: https://www.globalepic.co.kr/view.php?ud=202506021506385805ebfd494dd_29

- Reference 9: https://www.judal.co.kr/?view=stockAI&shareToken=9q7kcn4PO0fcigTp

- Reference 10: https://cm.asiae.co.kr/en/article/2024082010223582036

- Reference 11: https://temp.cosmax.com/new/en/good/sub_good_02_history.asp

- Reference 12: https://a.storyblok.com/f/288782/x/2ca8968346/2025a0006.pdf

- Reference 13: https://www.ntoday.co.kr/news/articleView.html?idxno=54657

- Reference 14: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240516001740&docno=&viewerhost=&

- Reference 15: https://marketbz.com/companyDetail/1208747751