DEEP RESEARCH · PJ METAL

PJ Metal 2025 Q4: Aluminum and Recycled Lead Drive a Profit Quantum Jump

A research-style review of the deoxidizer cash cow, PJ E&S recycled-lead ramp, and circular-economy policy tailwinds

0. Bottom line first

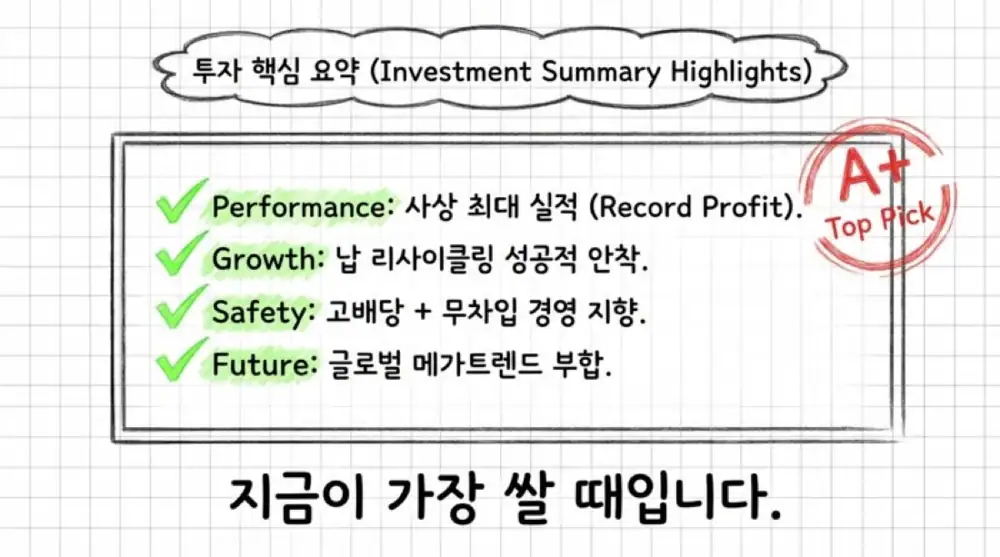

My core read is that PJ Metal is no longer just a POSCO-facing aluminum deoxidizer cash cow. In 2025 it proved, in the numbers, that the recycled-lead business can stabilize yield and utilization while passing through raw-material inflation.

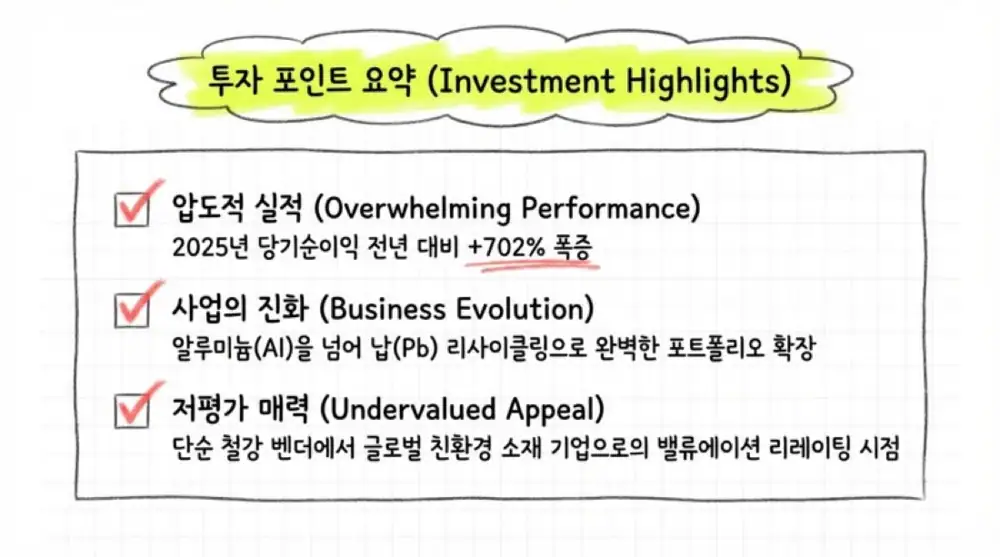

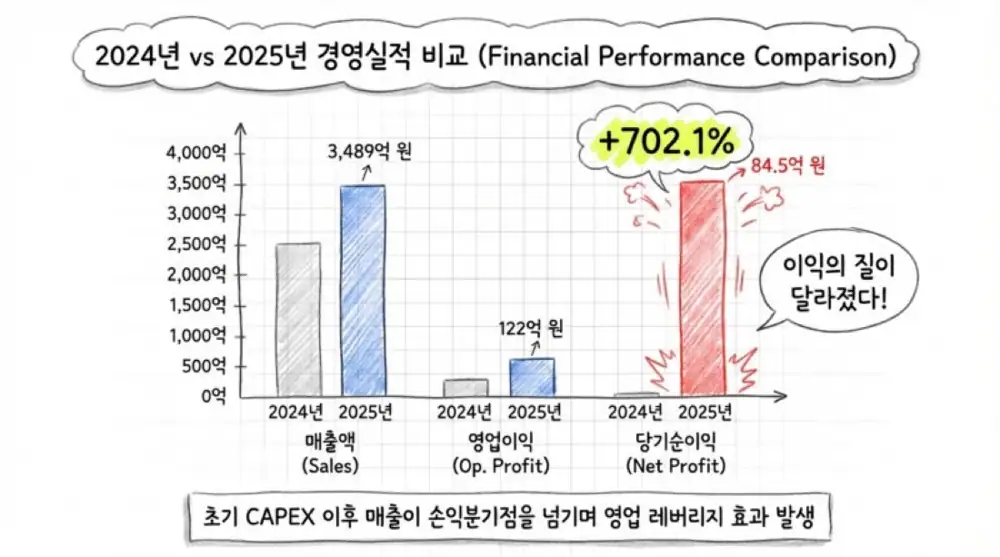

- 2025 consolidated revenue rose 37.1% YoY to KRW 348.96 billion, while operating profit rose 33.3% to KRW 12.23 billion.

- Pre-tax profit increased 561.7% to KRW 10.12 billion, and net income increased 702.1% to KRW 8.46 billion.

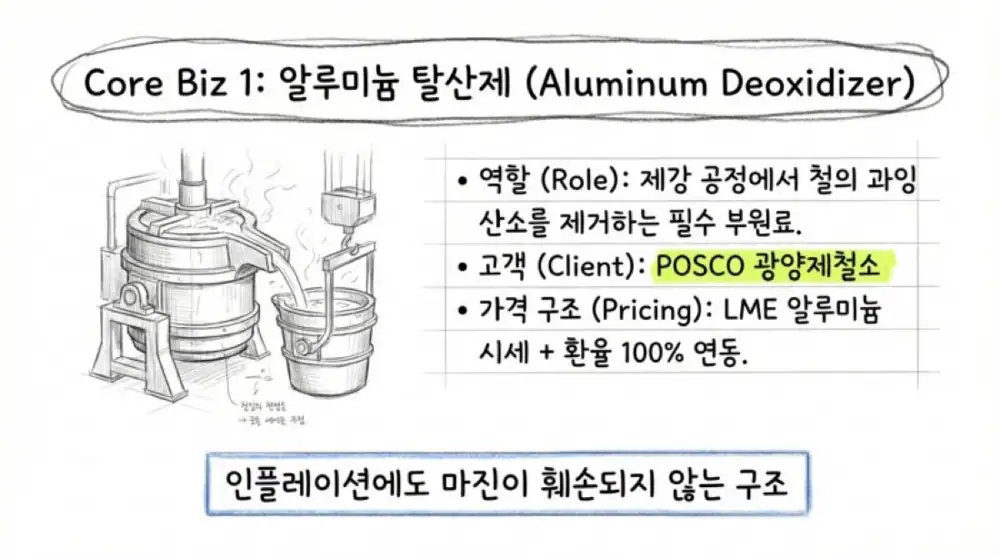

- The aluminum deoxidizer business generates about 42.9% of total revenue from POSCO Gwangyang Steelworks, with pricing linked to LME aluminum and FX.

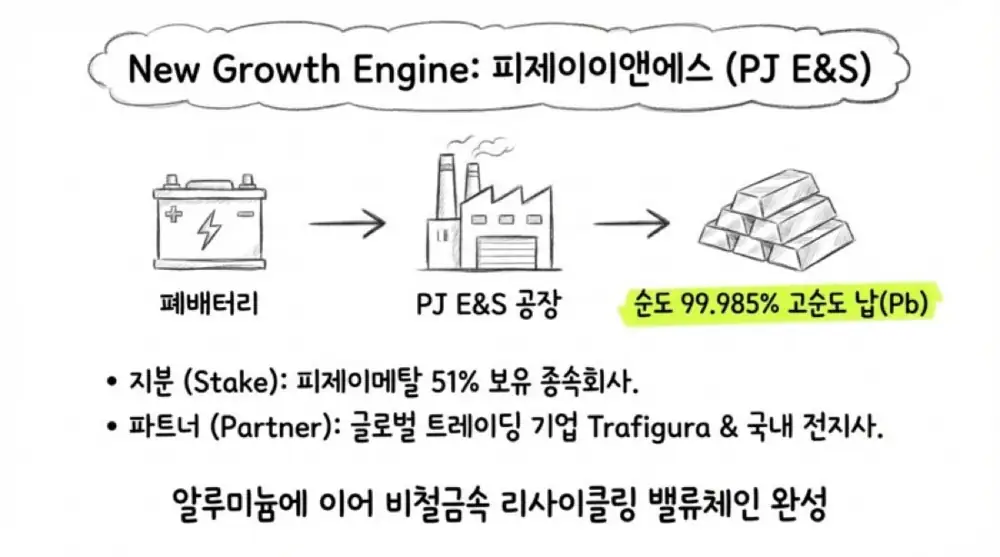

- PJ E&S, established in June 2023 and 51%-owned by PJ Metal, processes and melts used lead-acid batteries to make 3N refined lead ingots with purity above 99.985%.

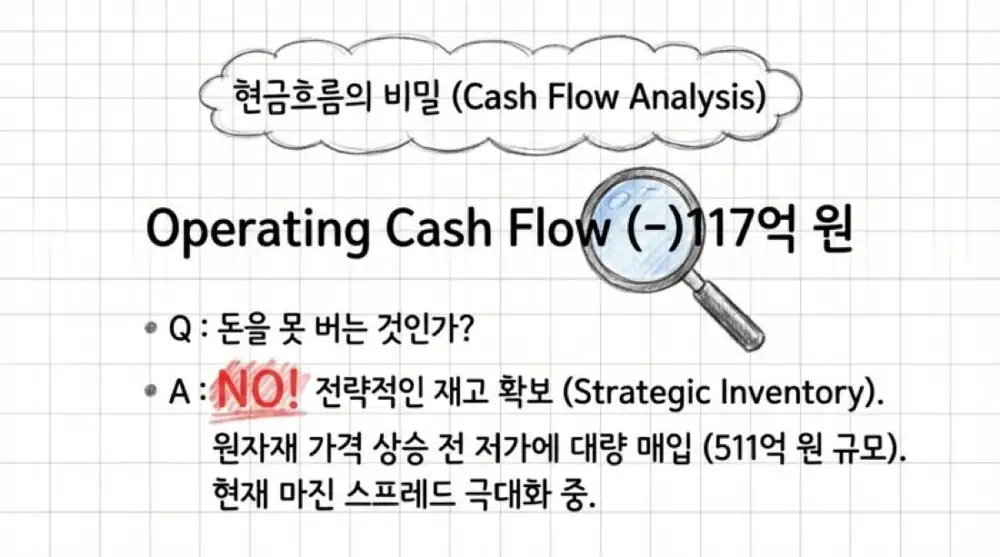

- 2025 3Q cumulative operating cash flow of -KRW 11.7 billion, investing cash flow of -KRW 12.5 billion, and financing cash flow of +KRW 17.4 billion are interpreted as inventory and facility investment ahead of the Q4 ramp.

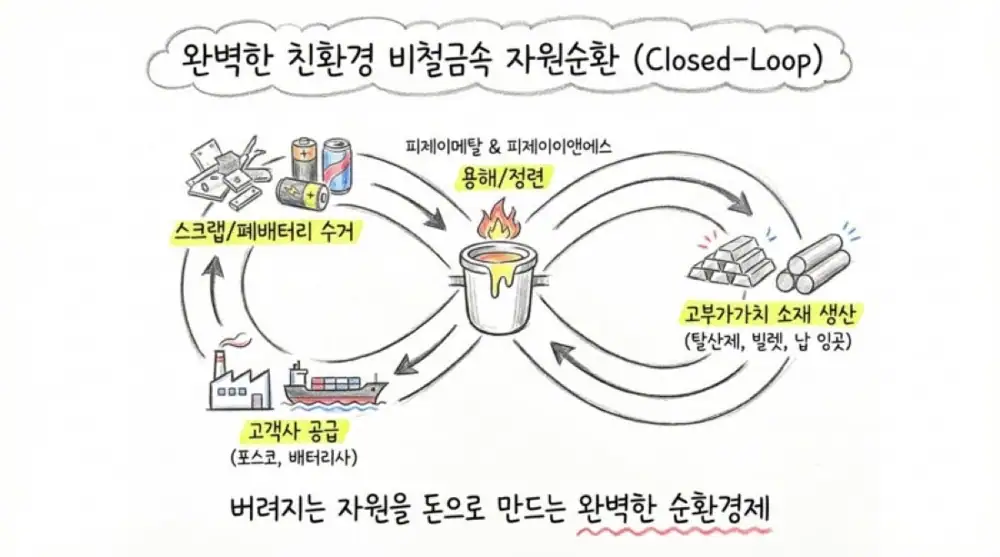

1. Business structure: non-ferrous recycling from aluminum to lead

PJ Metal buys aluminum scrap domestically and abroad, then produces and sells steelmaking deoxidizers and aluminum billets. The source frames this as a closed-loop circular-economy model that turns discarded metal into higher-value industrial material.

Official fact: Aluminum deoxidizer is an essential steelmaking input used in converter operations to remove excess oxygen from molten iron and refine the iron crystal structure. PJ Metal recycles aluminum cans and compressed chips into pellets and mini-pellets supplied to POSCO Gwangyang Steelworks.

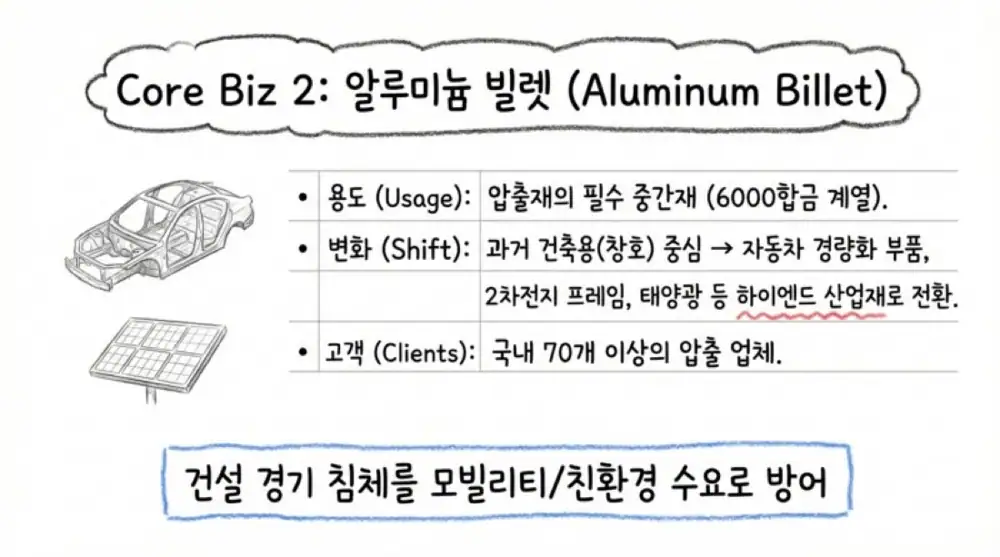

Aluminum billets are intermediate products for extrusion. The company produces 6000-series alloys such as 6063, 6061, and 6N01 for extrusion companies, with demand expanding from construction sash to automotive light-weighting, battery-pack materials, phones, solar structures, and aerospace.

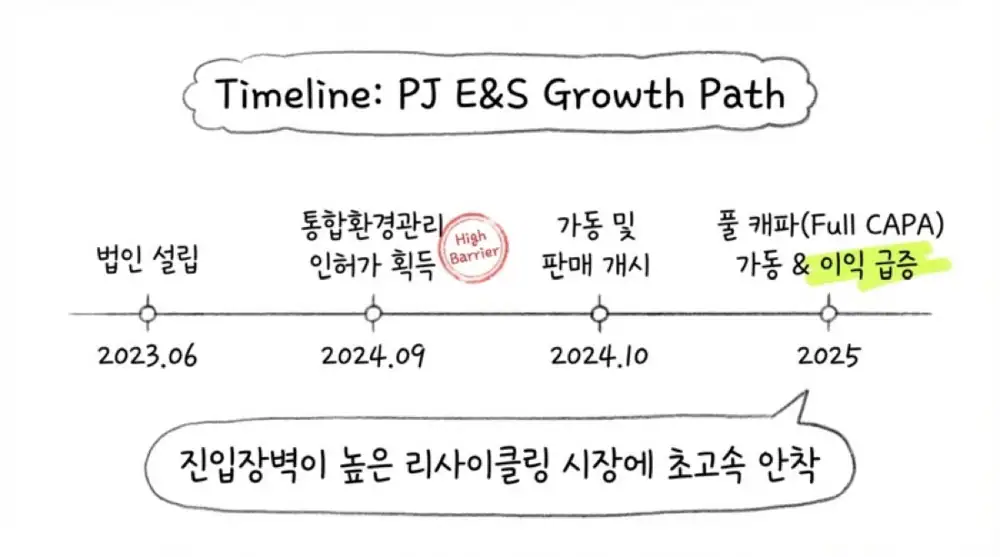

Official fact: PJ E&S was established on June 19, 2023 and is a 51%-owned subsidiary of PJ Metal. It pretreats, crushes, and melts used lead-acid batteries to produce 3N refined lead ingots with purity above 99.985%.

Deoxidizer

Essential input for POSCO. LME aluminum and FX-linked pricing is the margin-defense mechanism.

6000-series billets

Extrusion intermediates expanding into autos, battery packs, solar structures, and aerospace demand.

3N recycled lead

Lead-acid battery recycling is the new business that breaks dependence on aluminum alone.

2. 2025 results: net income moved much more than revenue

Official fact: The 2025 preliminary consolidated results disclosed on February 24, 2026 were revenue of KRW 348,957,303,218, operating profit of KRW 12,226,661,140, pre-tax profit of KRW 10,115,880,779, and net income of KRW 8,456,845,572.

| Metric | 2024 | 2025 | YoY |

|---|---|---|---|

| Revenue | KRW 254,485,502,212 | KRW 348,957,303,218 | +37.1% |

| Operating profit | KRW 9,170,810,482 | KRW 12,226,661,140 | +33.3% |

| Pre-tax continuing profit | KRW 1,528,681,110 | KRW 10,115,880,779 | +561.7% |

| Net income | KRW 1,054,292,151 | KRW 8,456,845,572 | +702.1% |

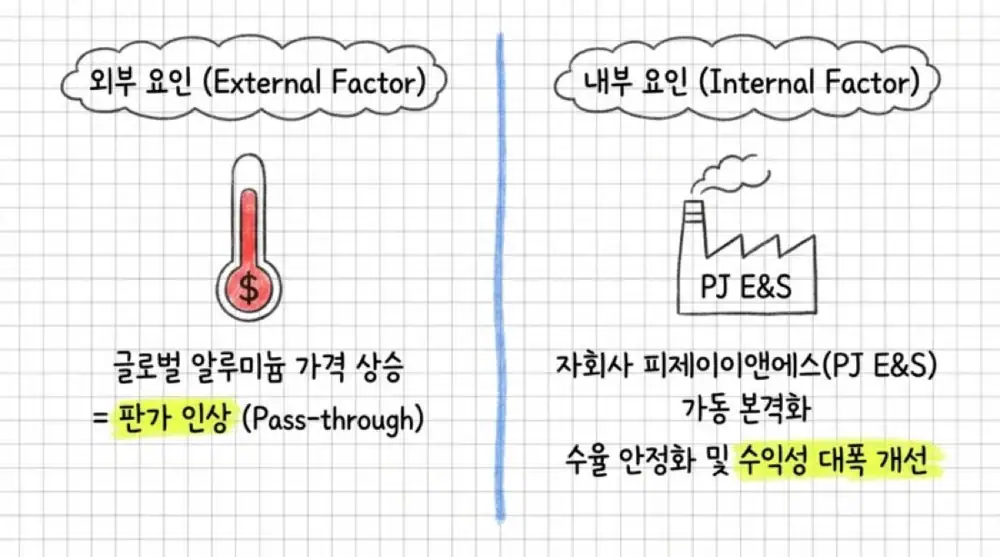

Interpretation: The much larger net-income growth than revenue growth reflects higher selling prices in the legacy business, yield stabilization after PJ E&S mass production, operating leverage after CAPEX crossed breakeven, and FX/commodity futures hedging effects.

Through 2025 Q3, operating cash flow was -KRW 11.7 billion, investing cash flow -KRW 12.5 billion, and financing cash flow +KRW 17.4 billion. The source interprets the apparent cash outflow as working-capital build from preemptive purchases of used-battery links and rails ahead of the Q4 recycled-lead ramp. Inventory at the end of 2025 Q3 was KRW 51.1 billion.

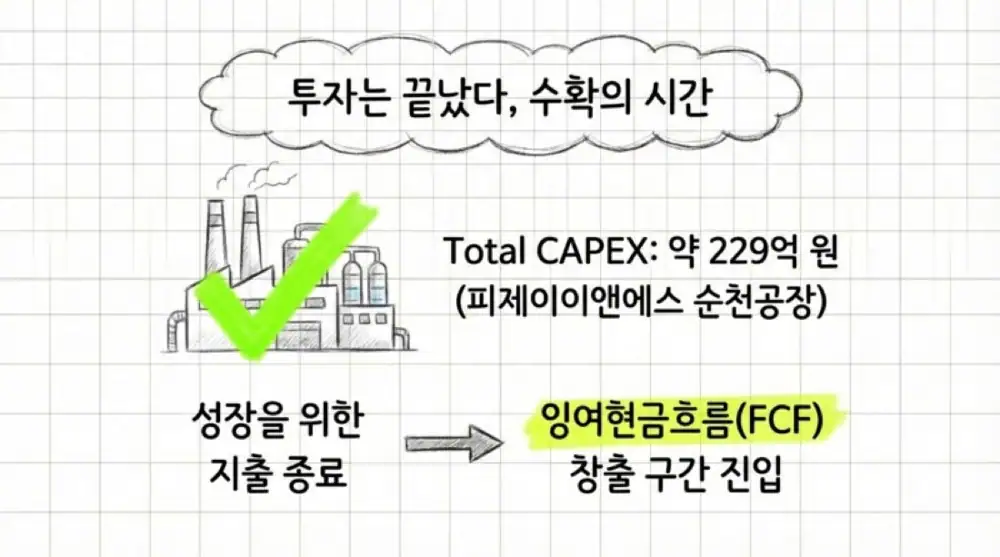

The investing outflow funded productive CAPEX at PJ E&S’s Suncheon plant, which has annual capacity of 27,000 tons, including fixed assets, machinery expansion, and integrated environmental permits. The source’s view is that the cash-generation cycle completed in Q4 as inventory was processed into 3N refined lead and raw-material inflation was passed through to selling prices.

3. Customers and moat: POSCO, Trafigura, and Poongjeon sourcing

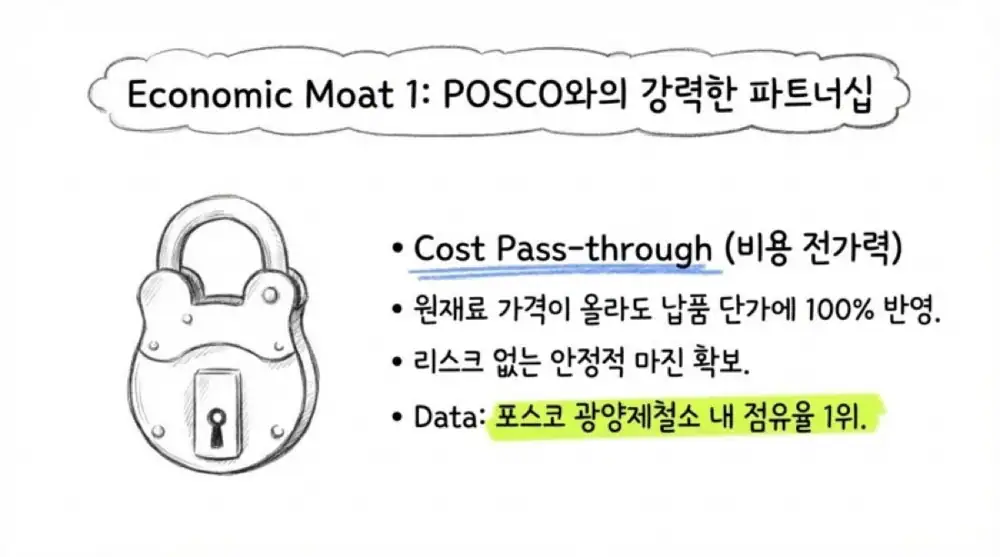

Official fact: The anchor customer in deoxidizers is POSCO, and about 42.9% of total revenue comes from POSCO Gwangyang Steelworks. The selling price is calculated monthly with 100% linkage to LME aluminum prices and exchange rates.

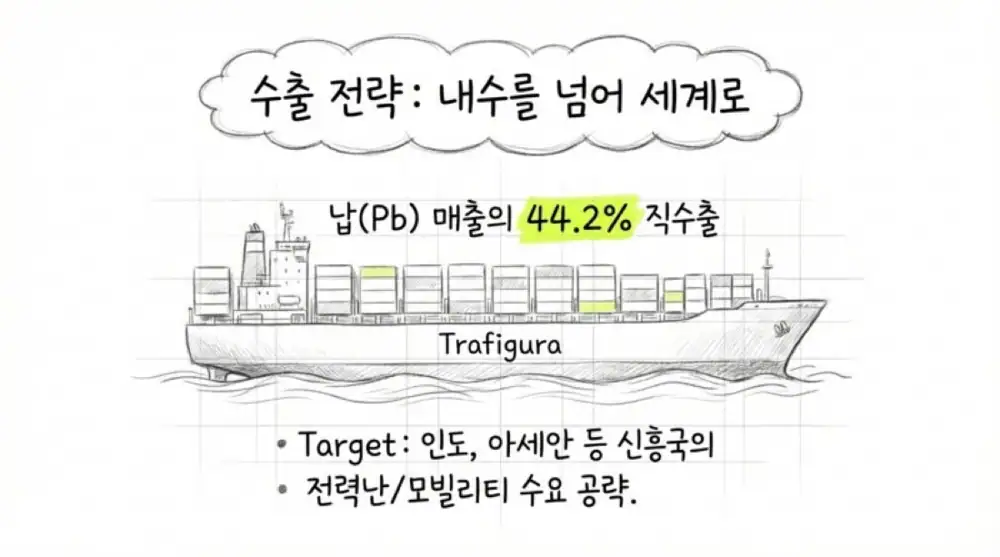

The billet segment serves more than 70 domestic aluminum extrusion companies with KS-certified extrusion profiles. For PJ E&S’s recycled-lead products, direct exports under FCA terms through partnership with global commodity trader Trafigura account for 44.2% of sales.

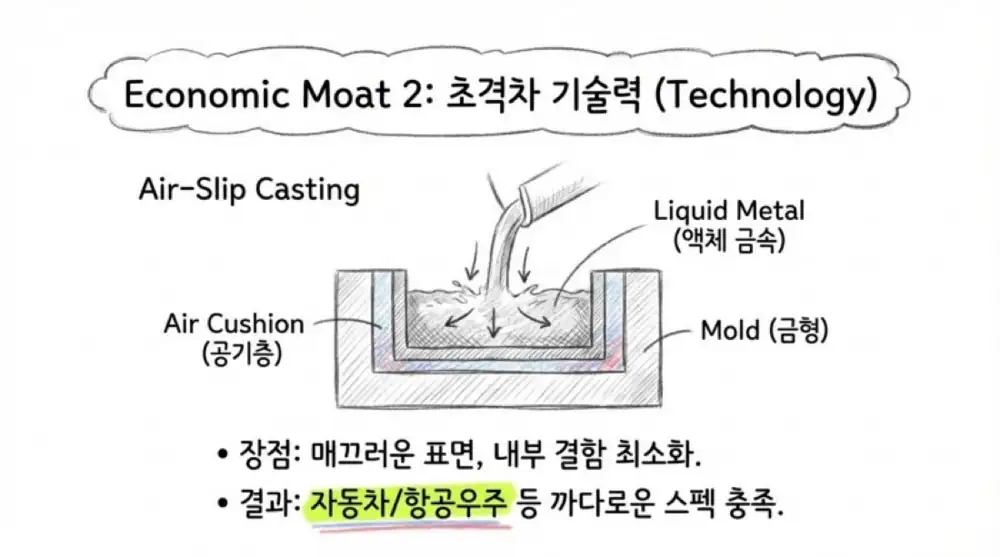

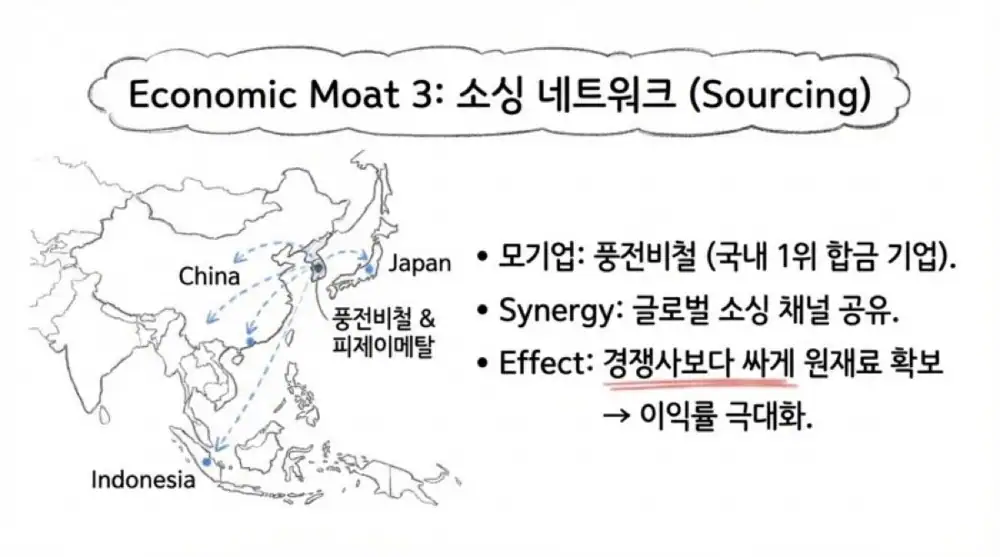

The moats are threefold: Air-Slip continuous casting for internal and surface quality, the Gwangyang plant’s proximity to POSCO Gwangyang Steelworks and JIT supply, and the global sourcing network of parent company Poongjeon Nonferrous across China, Indonesia, Japan, Sweden, and other regions.

| Moat | Content | Investment read-through |

|---|---|---|

| Process technology | Air-Slip continuous casting and strict quality control | Barrier to late entrants |

| Location | Gwangyang plant near POSCO Gwangyang Steelworks | Logistics-cost and response-speed advantage |

| Sourcing | Shared global scrap procurement network from Poongjeon | Cost defense |

| Pricing | LME/FX pass-through; lead ingots priced at LME plus premium | Pricing power |

4. History and investment: CAPEX led into recycled lead

| Year | Event | Strategic meaning |

|---|---|---|

| 2010.06 | PJ Metal established through split-off of Aldex deoxidizer business | Standalone non-ferrous identity |

| 2010.12 | Relisted on KOSDAQ; largest shareholder changed from Taihan Electric Wire to Poongjeon | Poongjeon recycling DNA and sourcing network transplanted |

| 2012.11 | New deoxidizer plant completed | Capacity expansion for POSCO volumes |

| 2016.01 | Aluminum billet plant completed | Diversification into extrusion intermediates |

| 2023.06 | PJ E&S established | Entry into lead-acid battery recycling |

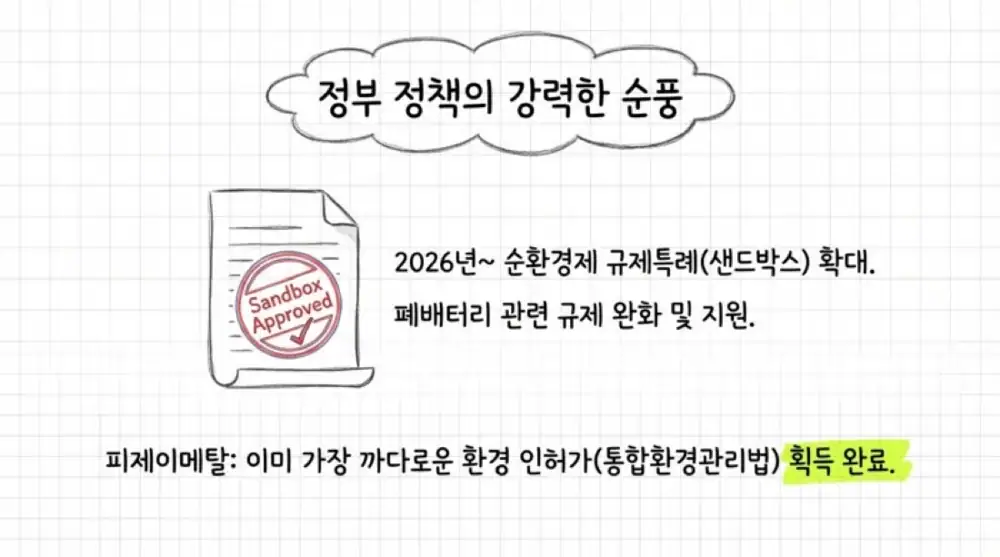

| 2024.09 | PJ E&S integrated environmental operation start report obtained | Environmental permitting barrier cleared |

| 2024.10 | 3N refined-lead melting and sales started | First year of the export-oriented recycling ramp |

Official fact: The 2023 capital contribution to PJ E&S was KRW 5.1 billion for a 51% stake. During 2024-2025, roughly KRW 22.9 billion was invested, on carrying-value basis, in the Suncheon plant’s two modern furnaces, pretreatment crushing facilities, and pollution-control equipment.

The source notes that 2025 Q3 cumulative R&D expense of KRW 490 million, or 0.23% of revenue, may look low. But in a capital-equipment and network industry, the true barrier is mass-production facilities, high-quality feedstock access, and environmental permits rather than the absolute R&D line.

5. Shareholders and competition

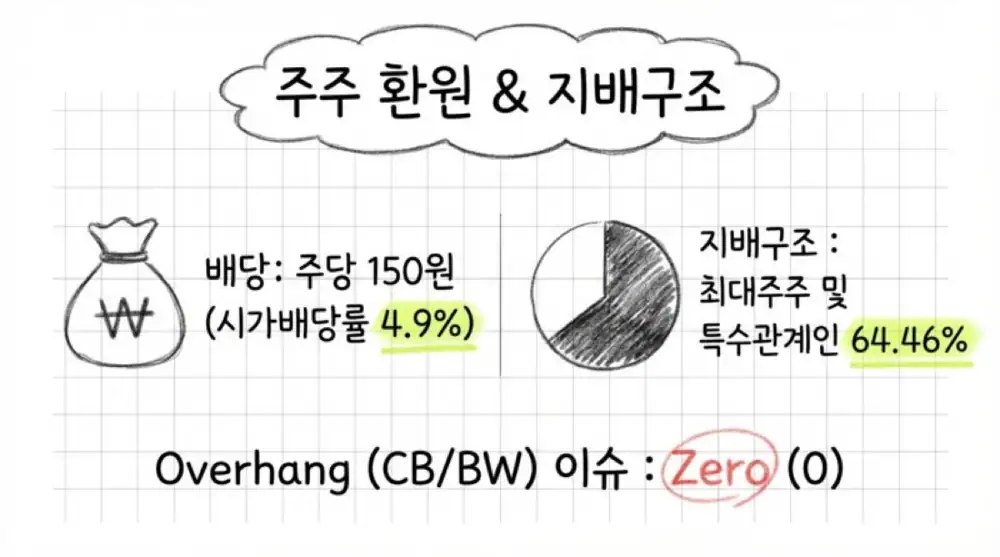

Official fact: As of September 30, 2025, Poongjeon Nonferrous held 45.00% or 11,162,444 shares, Chairman Dong-chun Song held 15.07% or 3,738,272 shares, and PJ Chemtech held 3.93% or 974,303 shares. The largest shareholder and related parties held 64.46% in total.

Poongjeon is an unlisted holding-company-like entity controlled by Chairman Song, who owns 80.44%. It controls a group of non-ferrous companies including PJ Altec, PJ Chemtech, Hwachang, and Dawon Alloy. The source interprets PJ Metal as the group’s only KOSDAQ-listed company and its capital-market window/new-growth testbed.

Official fact: The quarterly report showed no outstanding mezzanine securities such as BW, CB, or EB that could dilute shareholders. Of 24,803,369 shares outstanding, minority shareholders held 31.84%, or about 7.89 million shares.

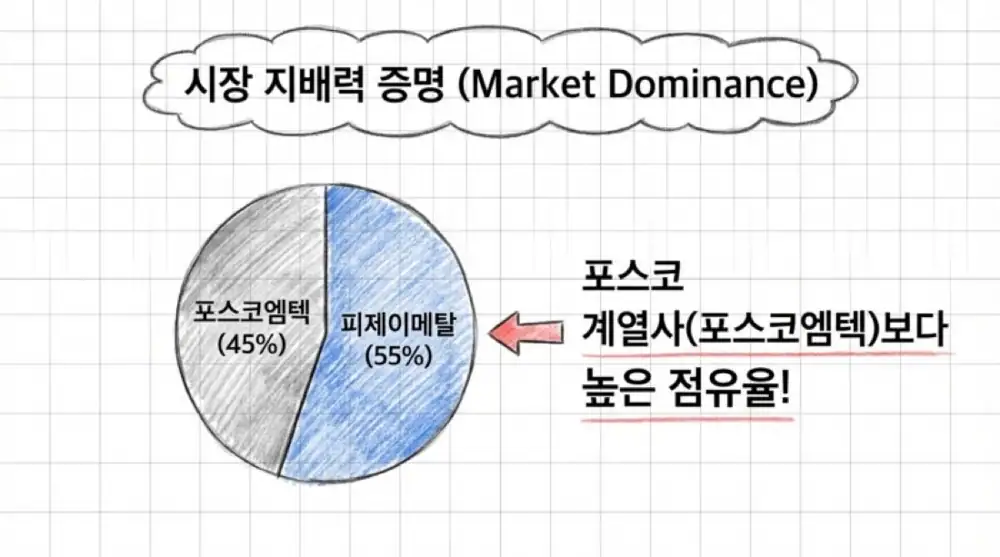

The 2024 dividend, paid in April 2025, was KRW 150 per share, with total dividends of about KRW 3.72 billion and dividend yield of about 4.9%. In POSCO-facing aluminum deoxidizers, PJ Metal held 55% or 7,815 tons of supply volume versus POSCO M-Tech’s 45% or 6,285 tons.

In billets, the company is moving from low-margin construction products to soft-alloy 6000-series products for automotive light-weighting chassis, battery frames, and solar supports, plus hard alloys for machining. 2025 Q3 billet revenue was KRW 68.4 billion, or 32.48% of total revenue.

In recycled lead, competition includes Young Poong, Korea Zinc, and small domestic recyclers. PJ E&S’s strategy is to avoid pure domestic competition through global partnerships such as Trafigura and a 44.2% direct-export share.

6. Growth strategy and risks

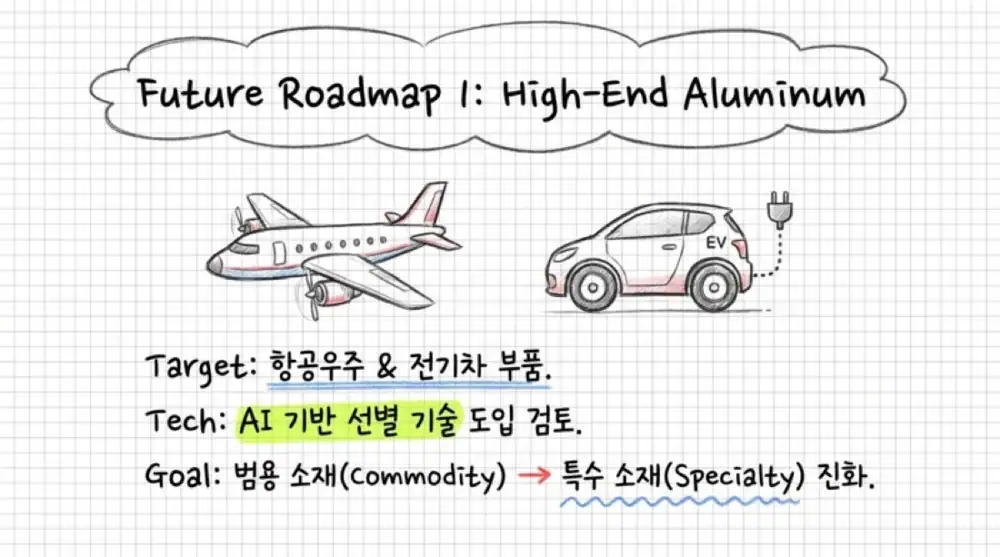

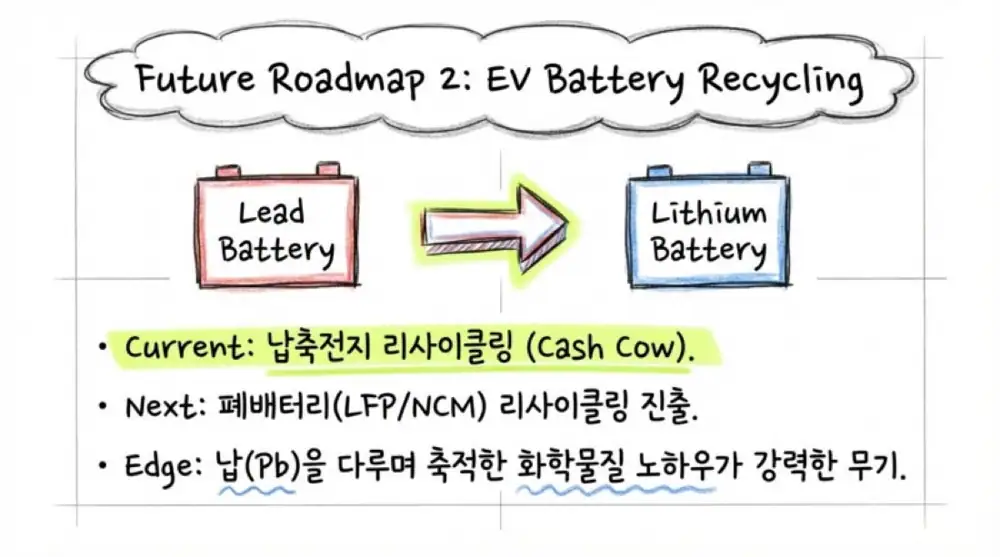

Full recycled-lead utilization

The source believes PJ E&S comfortably met the 2025 target of 21,000 tons of 3N refined lead after Q4 2024 initial mass production.

4N refined-lead option

Future upgrade to 99.995% 4N refined lead is presented as a higher-margin lineup strategy.

EV battery recycling

The know-how in chemical handling and environmental permits from lead-acid recycling could extend into EV battery recycling.

For high-end aluminum, the source cites an external forecast that the aerospace aluminum market will reach USD 1.04 billion by 2035, growing at 3.86% CAGR. Air-Slip casting and AI-based high-precision color sorting are positioned as ways to maximize high-purity scrap recovery.

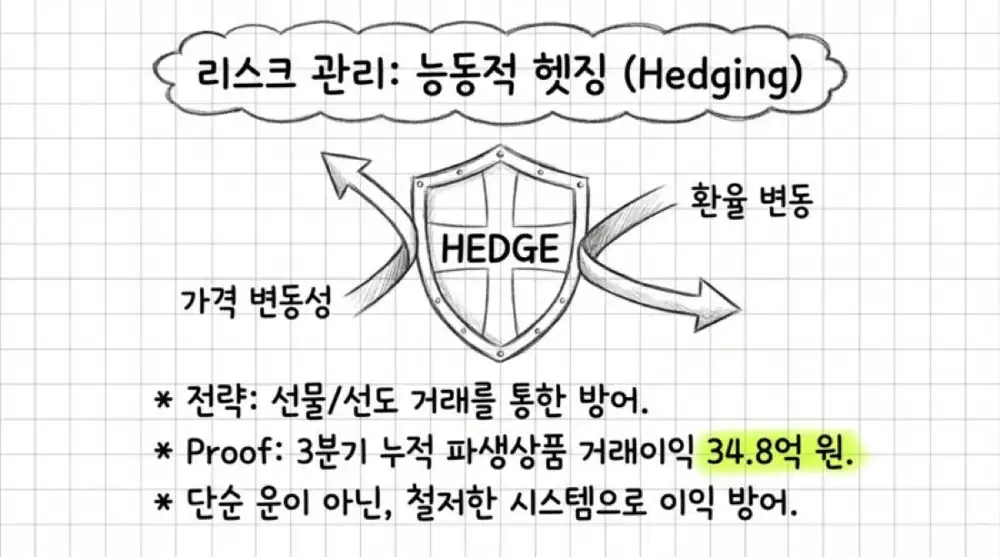

Official fact: As of 2025 Q3, the company held currency futures short positions of USD 30 million and aluminum commodity futures short positions of USD 2.63 million. It realized KRW 3.48 billion of derivative transaction gains from forwards.

- LME and FX risk: Metal-price declines and currency swings can cause inventory write-downs and lower selling prices.

- Scrap sourcing competition: Decarbonization increases competition for quality aluminum scrap and used lead-acid batteries.

- Customer concentration: POSCO-related revenue of about 43% is a risk, although proven inputs in steelmaking carry high switching costs.

- New-business execution: Utilization, yield, and export premiums for 3N recycled lead need continued confirmation.

7. Policy and mega trend: circular economy and carbon rules

The source frames the 2026-2028 keywords as circular economy and carbon-emission reduction. Korea’s Ministry of Environment and Korea Environment Corporation are expanding resource-circulation and carbon-response policies, including regulatory sandboxes for recycling technologies and services.

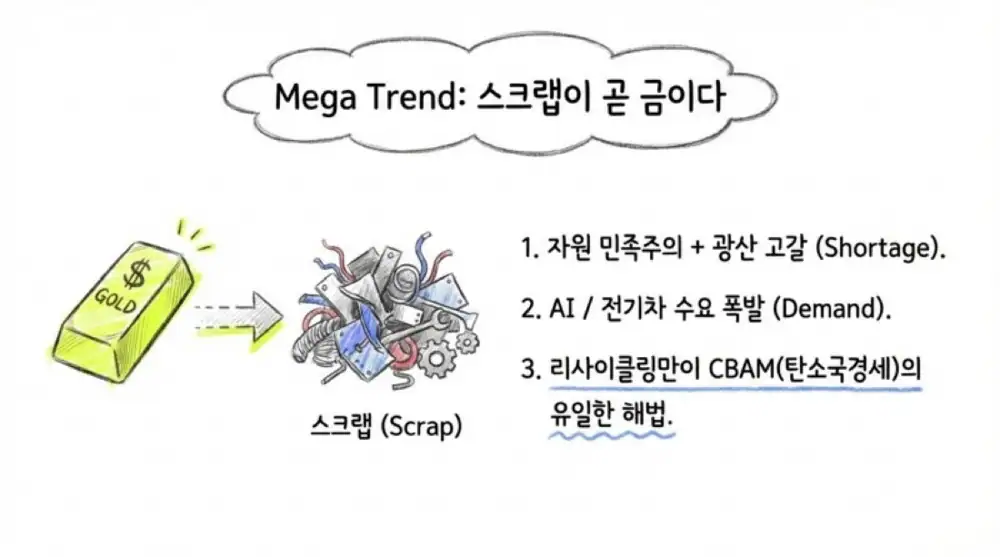

The global non-ferrous scrap recycling market is presented as growing at 6.7% CAGR and exceeding USD 104.9 billion. The source also notes that the World Bank’s metals and minerals price index rose 9% month over month in May 2024.

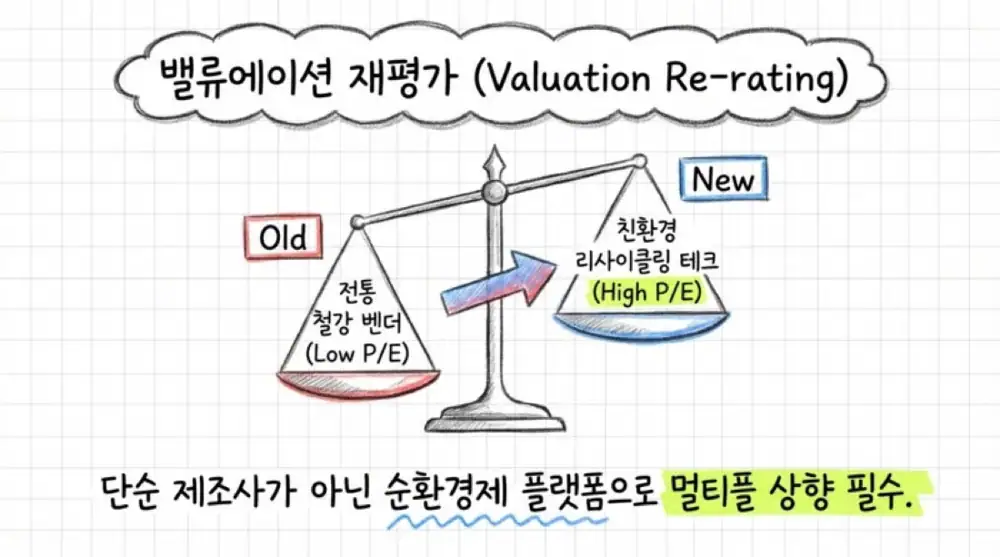

Interpretation: Aluminum recycling saves about 95% of energy compared with new bauxite mining and smelting, making it a practical response to green trade rules such as CBAM. That is the logic for reframing PJ Metal from a steelmaking-input supplier to a bottleneck supplier of green materials.

One-line conclusion: the 702.1% increase in 2025 net income is not just a raw-material-price effect. I read it as a business-quality upgrade where the POSCO cash cow, recycled-lead ramp, Poongjeon sourcing network, and circular-economy policies overlap.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224194564949

- PJ Metal corrected annual report: https://kind.krx.co.kr/common/disclsviewer.do?method=searchInitInfo&acptNo=20230317000305&docno=

- PJ Metal research PDF - Naver Finance: https://ssl.pstatic.net/imgstock/upload/research/company/1713481209150.pdf

- Poong Jeon Nonferrous Metal company information: https://poongjeon.tradekorea.com/company.do

- Poongjeon group KRW 1 trillion revenue - Korea Nonferrous Metals Association: https://nonferrous.or.kr/bbs/?act=bbs&subAct=view&bid=trend&page=5&order_type=desc&seq=4175

- Poongjeon Nonferrous Metal - Wikipedia: https://ko.wikipedia.org/wiki/%ED%92%8D%EC%A0%84%EB%B9%84%EC%B2%A0

- Poongjeon Nonferrous Metal profile - EMIS: https://www.emis.com/php/company-profile/KR/Poongjeon_Nonferrous_Metal_CoLtd__Incheon__en_3519562.html

- Poongjeon official site: http://poongjeon.net/en/

- Poong Jeon Nonferrous Metal profile - Credence Data: https://www.credencedata.com/company-profile/kr/poong-jeon-nonferrous-metal-co-ltd-cab2a022

- Non-ferrous scrap recycling market report - GII: https://m.giikorea.co.kr/report/tbrc1889521-non-ferrous-scrap-recycling-global-market-report.html

- Ministry release on critical-mineral extraction regulatory sandbox: https://mcee.go.kr/home/web/board/read.do;jsessionid=uAiflNfpNDIh5s5XlJwMfjAQ69JSExQ3PVlqoMaz.mehome2?pagerOffset=0&maxPageItems=10&maxIndexPages=10&searchKey=&searchValue=&menuId=10525&orgCd=&boardId=1821830&boardMasterId=1&boardCategoryId=&decorator=

- Aerospace aluminum market outlook - Market Research Future: https://www.marketresearchfuture.com/ko/reports/aluminum-for-aerospace-market-31577

- 2026 resource-circulation and carbon-response policy - Polinews: https://www.polinews.co.kr/news/articleView.html?idxno=720011

- Whole-life decarbonization policy - Net Zero News: https://www.netzeronews.kr/news/articleView.html?idxno=4635

- Alcoa 2025 Q4 results - Investing.com: https://kr.investing.com/news/company-news/article-93CH-1795502

- Source external image 1: https://lh7-rt.googleusercontent.com/docsz/AD_4nXcB12iu03ZNTIGy1PaY5Ya2q6Qg-ofas6TDyPHr8iAvaw4e1FRvnJdKiS7I3sSKT0AYrZEqBXo4WmmgViqCscEfYBKrGHUINgf9kFHalQX-cu9Mz73hqi1dg5_zttLNM4BPtxntFbsaQdMETzB838WLgx7C9hw?key=m8eCcWIJdDpfm2-FH2-t2A

- Source external image 2: https://lh7-rt.googleusercontent.com/docsz/AD_4nXfE_WN_88x9Qu8VTrQEu-Nxzfx7-zLWq5Y9hhJT5xl6BoYd47qj1biHIiLfTTWrpXSql9gKZ6eq21XsOWDfi9QlocNtPR8ccHRekjH_PcEvOBlWR62uY9IuSqcMGtmlkr8eRWeU0sTwiHy_L31eZgpoiEm55Kw?key=m8eCcWIJdDpfm2-FH2-t2A

- Source external image 3: https://lh7-rt.googleusercontent.com/docsz/AD_4nXev0he2_Rh5owWkbHdH8u94vi_L7Xb9c8Ixg01hL8r2PMG7SE3Q4AGWdgYRn92AFTg-9s46vcvqOiDdbrw6Qatf8Kwv5taMN3c_VPYTKEw_6emoEl02-kC5V56bixiGz1aqm7kqNINslj_ZRb6bHz1aUyNs6A?key=m8eCcWIJdDpfm2-FH2-t2A