DEEP RESEARCH · KBI DONGKOOK INDUSTRIAL

KBI Dongkook Industrial: Global Footprint Expansion and the 2025 Turnaround

An auto-parts turnaround report on Mexico, Europe, Shinasan, and interior-module IP.

0. Bottom line first

My read is that 2025 was the first year in which expansion at Mexico, Spain, and the Shinasan domestic plant clearly appeared in the numbers. The source frames KBI Dongkook Industrial as a deep-value auto-parts turnaround.

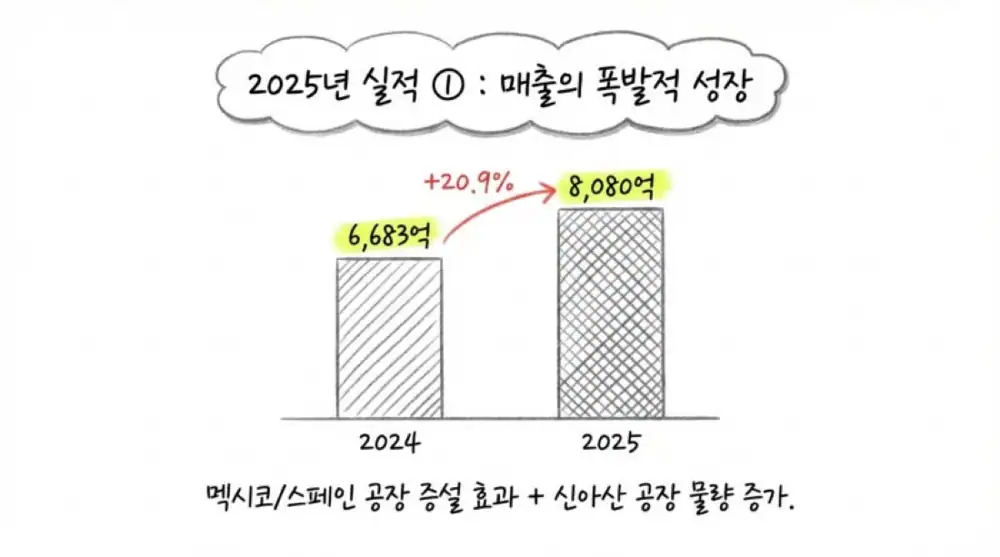

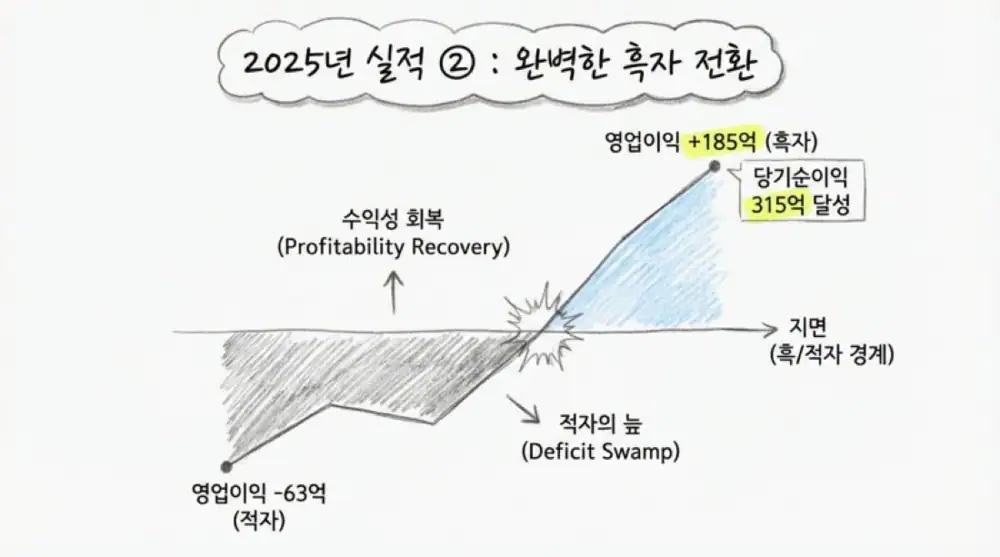

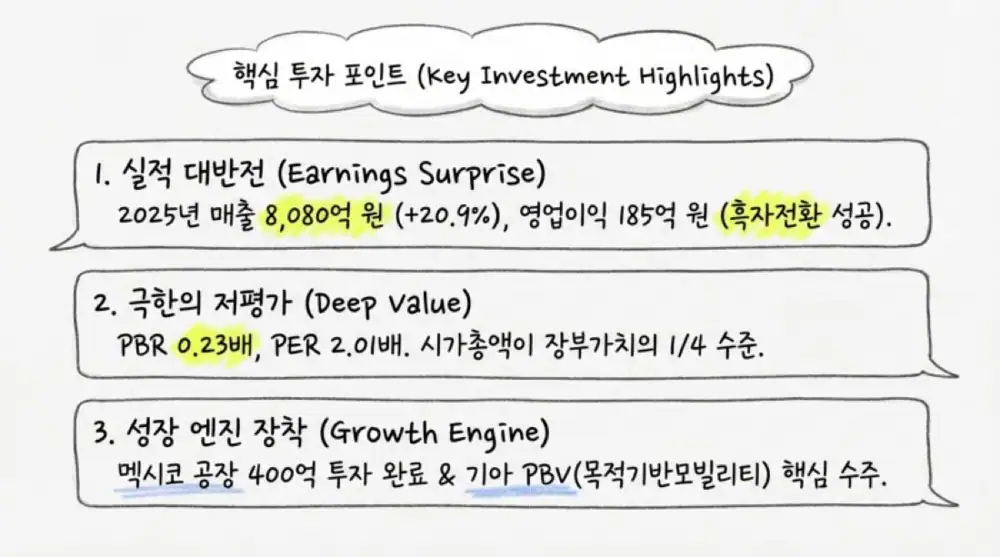

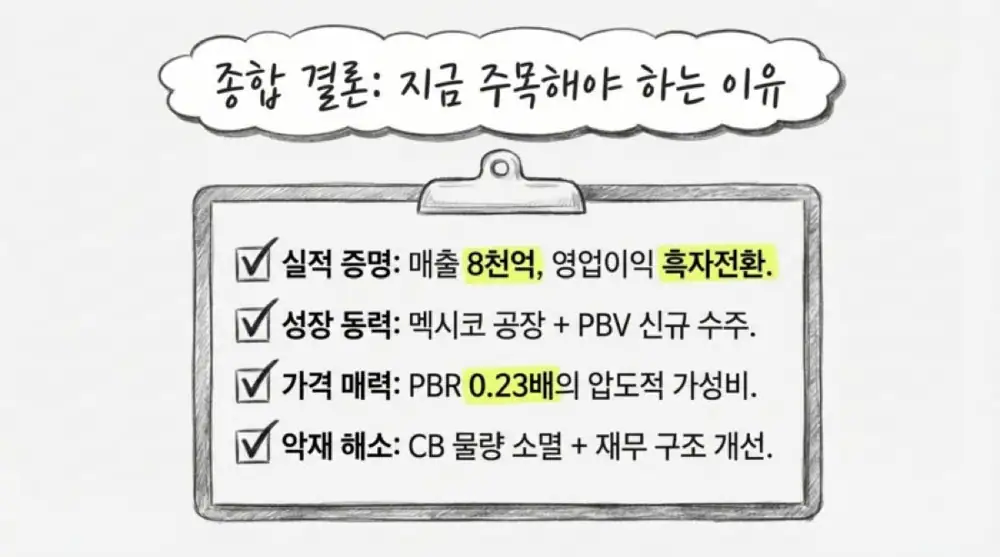

Official fact: 2025 consolidated revenue was KRW 808.00804 billion, up 20.9% YoY. Operating profit was KRW 18.55848 billion, turning around from a KRW 6.32662 billion operating loss in 2024. Net income was KRW 31.56005 billion, up 23.0% YoY.

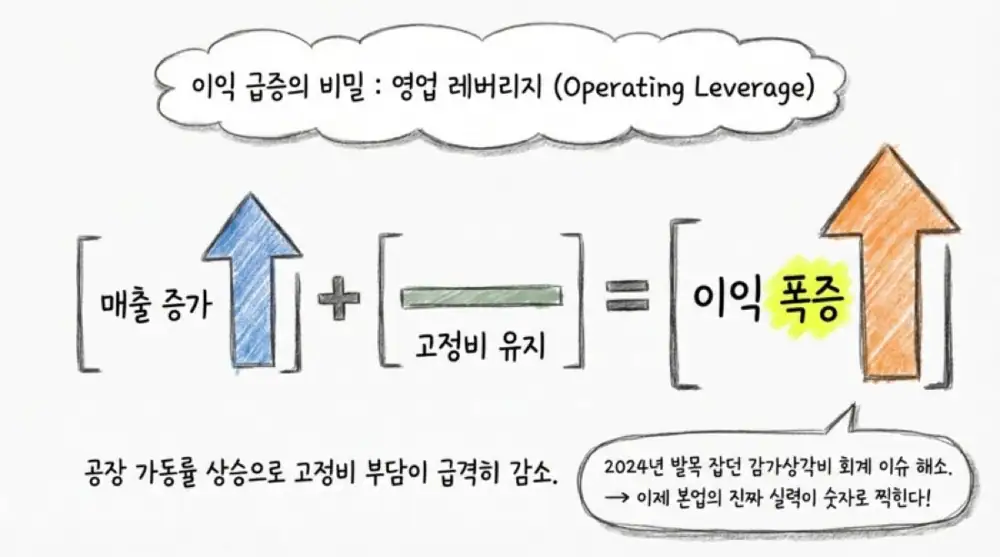

Interpretation: 2024 earnings were pressured by items such as a depreciation useful-life estimate change, while 2025 combined new expansion volume with better working-capital management and improved operating cash flow.

1. Source images and business structure

All company and earnings-related source images are preserved below.

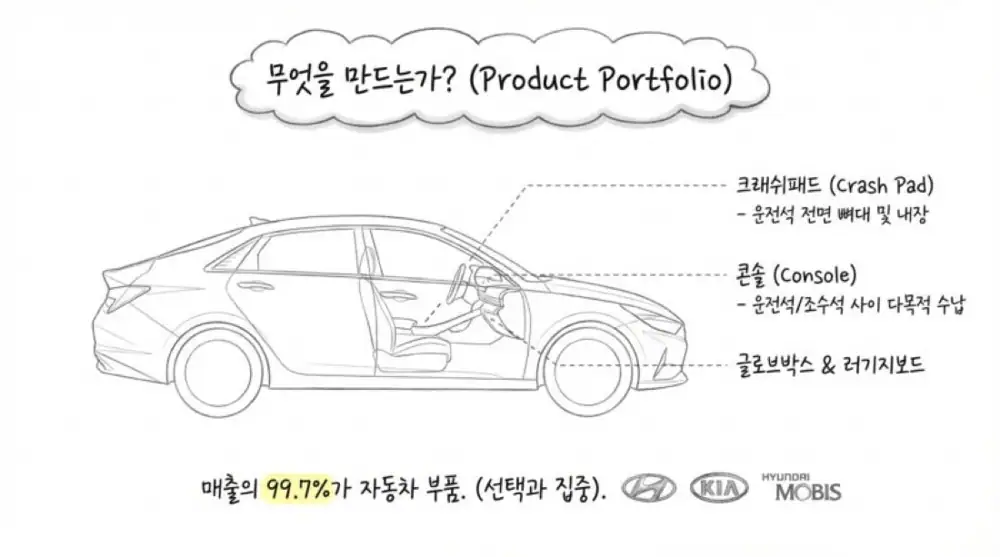

KBI Dongkook Industrial began in textiles in 1955 and pivoted to auto parts after acquiring Hanjin Plastic Industrial in 1996. In 9M 2025, 99.67% of revenue came from auto-parts manufacturing.

| Segment | 9M 2025 revenue | Share | Products/customers |

|---|---|---|---|

| Auto-parts manufacturing | KRW 643,180,339 thousand | 99.67% | Crash pads, consoles, glove boxes, luggage boards, lamps; Hyundai Motor, Kia, Hyundai Mobis, Volkswagen, Audi, BMW, Jiangsu Mobis, Mexico Mobis and others |

| Civil construction | KRW 1,961,049 thousand | 0.33% | Public/private development and civil/building works |

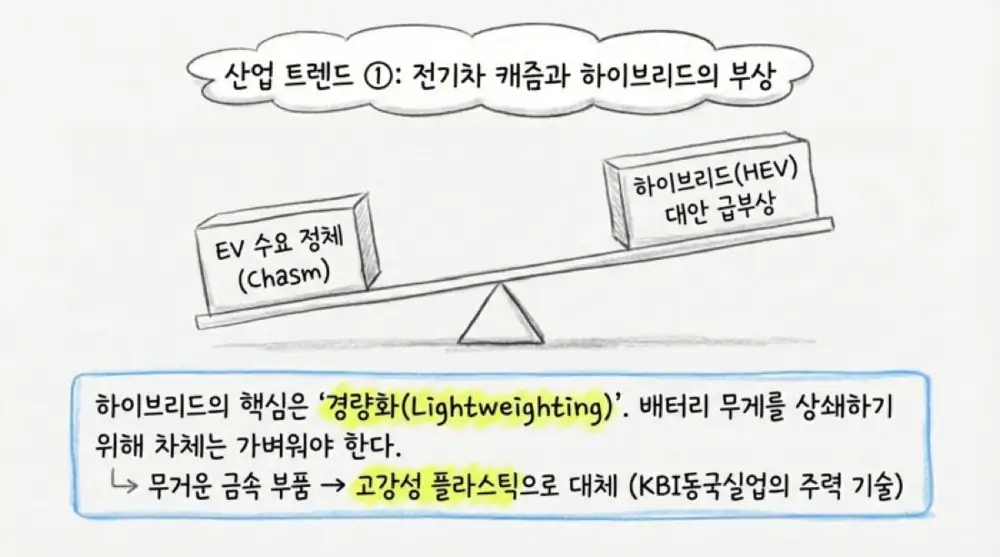

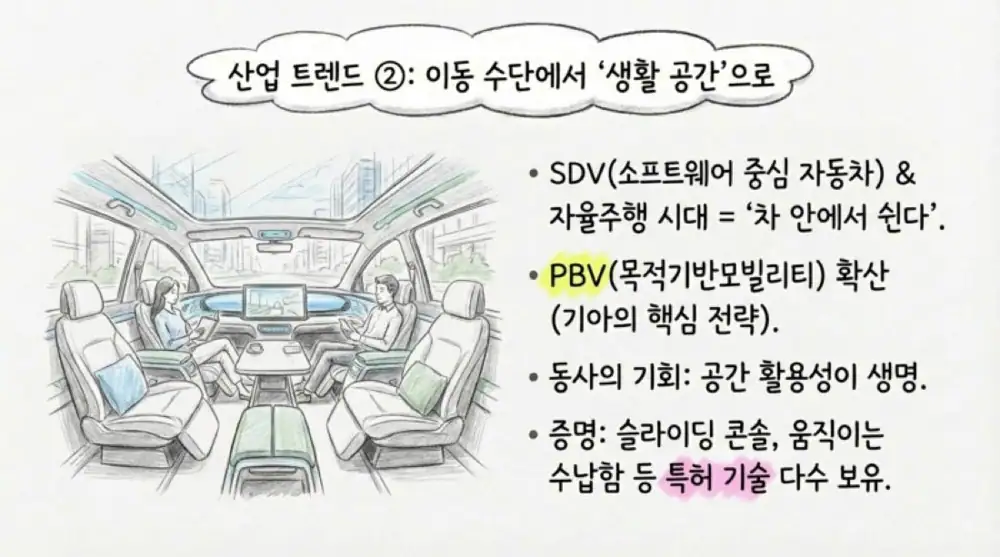

2. Auto megatrends and product position

The source focuses on the EV chasm, hybrid growth, and SDV/autonomous-driving redesign of interior space. It cites research that a Kona Electric with a 64kWh battery can lose about 27.5km of maximum range for every additional 100kg of vehicle weight.

Plastic injection and blow molding

High-strength lightweight plastics and recycled polymer materials replace metal parts in crash pads, consoles, glove boxes, and other interior modules.

Interior UX redesign

Sliding glove boxes, sliding armrest-console mechanisms, and display-integrated crash pads target PBV and autonomous-vehicle interior flexibility.

Design-stage collaboration

The company wins part-level orders through Tier-1 collaboration with automakers from new-model planning and design.

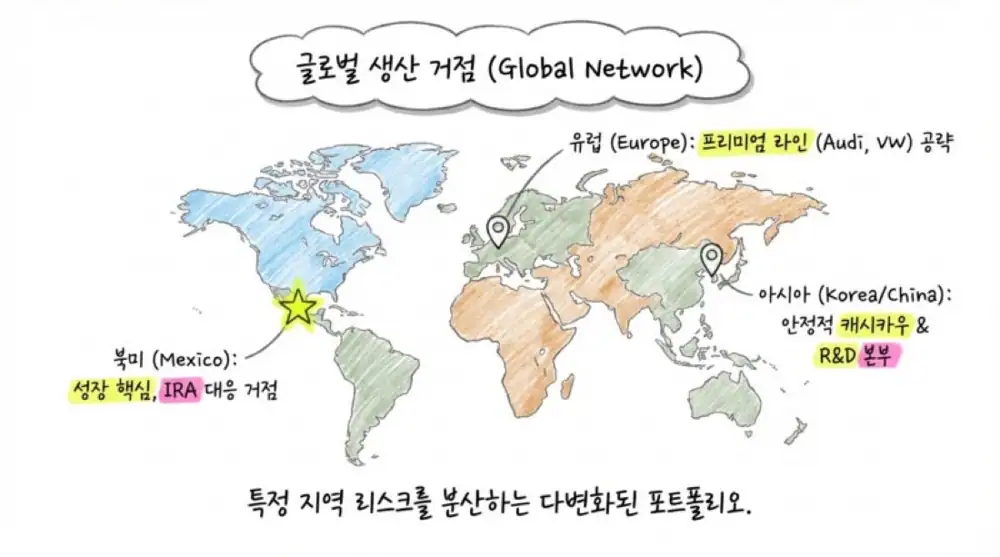

3. Global production footprint

| Footprint | Source facts | Strategic meaning |

|---|---|---|

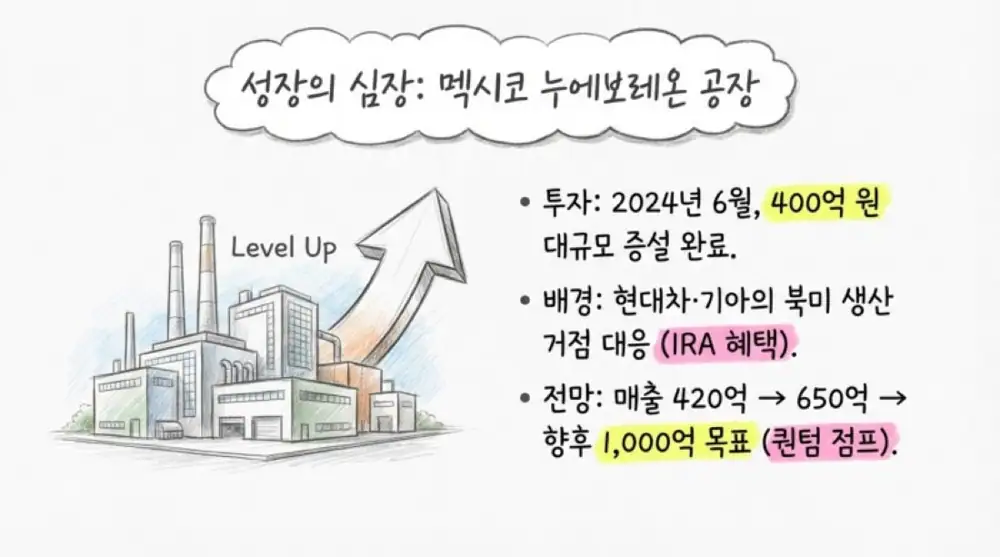

| Mexico | Founded in Pesqueria, Nuevo León in 2017 on 50,000㎡; KRW 40 billion CAPEX from June 2023 for about one year; 14,720㎡ expansion completed in June 2024 | IRA and North America production realignment. Parts for seven new Hyundai/Kia models, revenue expected to rise from KRW 42 billion to KRW 65 billion, with a long-term KRW 100 billion plant goal |

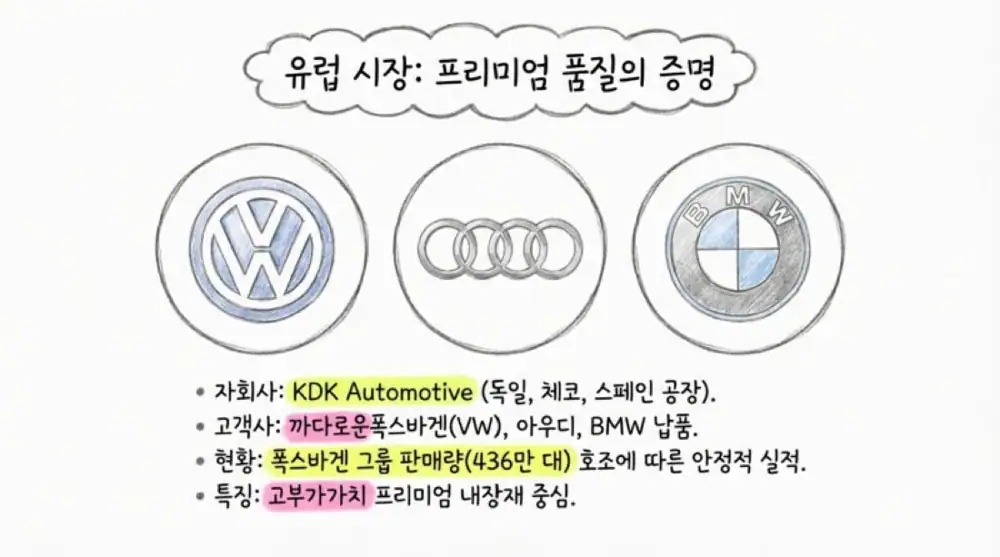

| Europe KDK Automotive | Launched through acquisition of Germany’s ICT in 2013; four plants across Germany, Czechia, and Spain | Premium interior trim supply to Volkswagen, Audi, and BMW |

| China and Korea | Yancheng Dongkook Auto Parts in China; domestic plants in Asan, Shinasan, Ulsan, Gyeongju, and Gunpo | Dongfeng Yueda Kia and Jiangsu Mobis support; Shinasan Plant 2 Building B produces core parts for five new EVs including electric PBV platform models |

4. R&D and patent moat

Official fact: 9M 2025 R&D spending was about KRW 9.8 billion, equal to about 1.7% of consolidated revenue and 2.7% of standalone revenue. The company has 108 patents, and its eco-friendly crash pad developed in 2022 won the IR52 Jang Young-sil Award.

| Category | Patent/technology | Partner | Meaning |

|---|---|---|---|

| Space flexibility | Sliding glove box and sliding transfer device for vehicle storage units | KBI Dongkook Industrial, Hyundai Mobis, or in-house | Higher interior flexibility for autonomous and PBV use cases |

| Lightweight/eco-friendly | Polypropylene resin with excellent melt tension | In-house | High-strength plastic material to replace metal |

| Safety/aesthetics | Crash pad with airbag-door deployment part | KBI Dongkook Industrial, Hyundai Motor, Kia, Hyundai Mobis | Combines seamless interior appearance with safe airbag deployment |

5. Financials and valuation

| Metric | 2024 | 2025 | Change |

|---|---|---|---|

| Revenue | KRW 668.39968 billion | KRW 808.00804 billion | +20.9% |

| Operating profit | KRW -6.32662 billion | KRW 18.55848 billion | Turnaround |

| Pre-tax continuing profit | KRW 31.76815 billion | KRW 37.86030 billion | +19.2% |

| Net income | KRW 25.66035 billion | KRW 31.56005 billion | +23.0% |

| Equity | KRW 225.92796 billion | KRW 268.04707 billion | +18.6% |

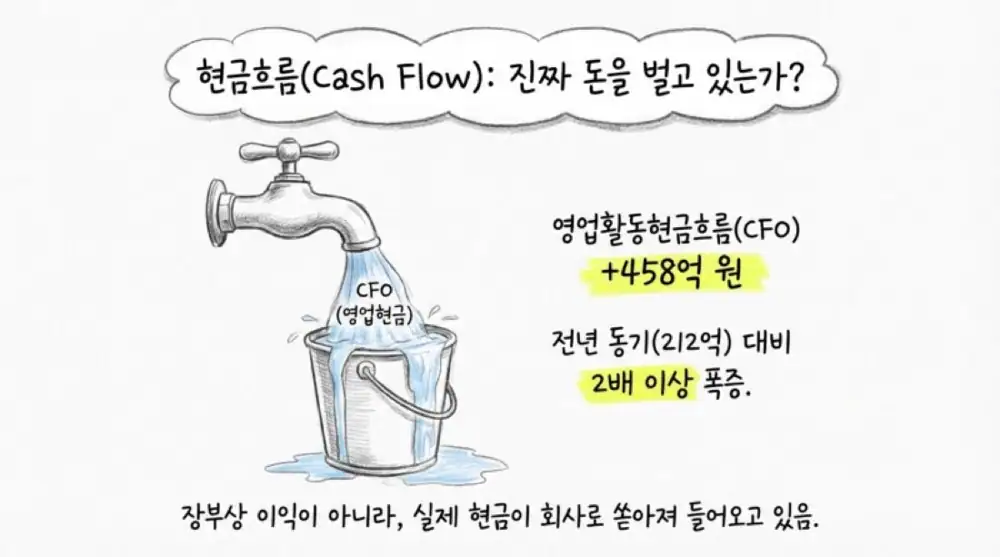

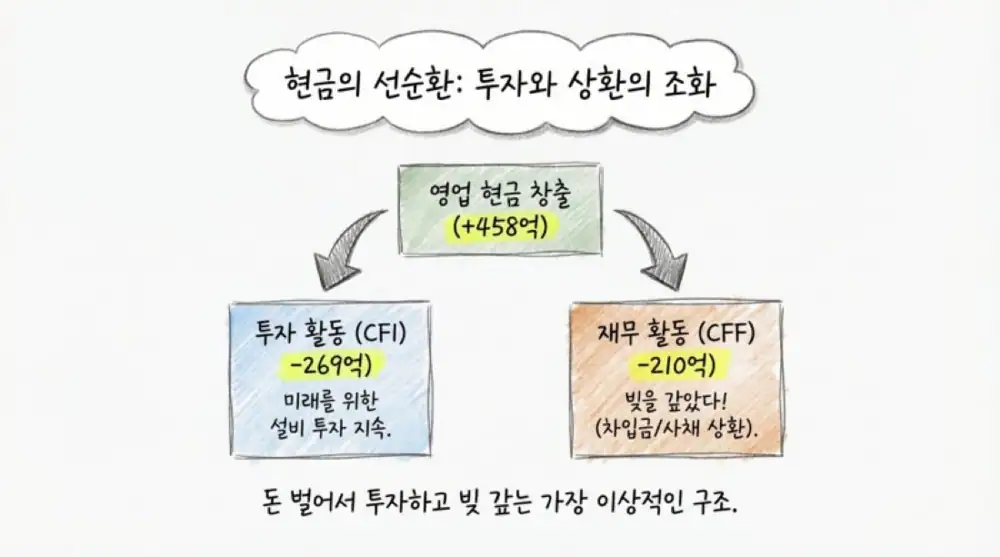

| Cash flow | 9M 2025 | 9M 2024 | Source interpretation |

|---|---|---|---|

| CFO | KRW 45,810,059 thousand | KRW 21,282,777 thousand | +115% on profitability improvement and working-capital optimization |

| CFI | KRW -26,970,447 thousand | KRW -66,518,949 thousand | CAPEX spending became more efficient after large expansions |

| CFF | KRW -21,004,413 thousand | KRW 36,218,330 thousand | Shift to net repayment of bonds and short-term borrowings |

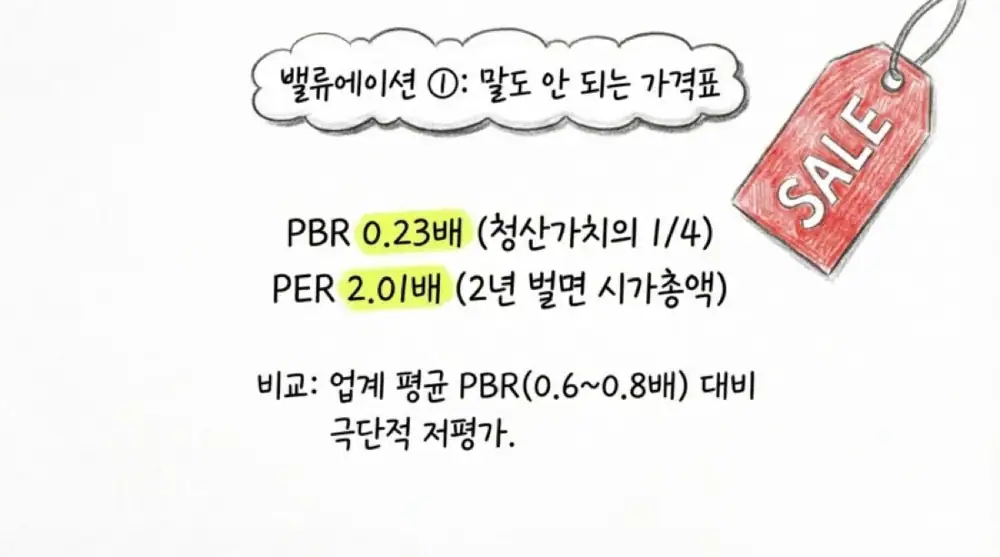

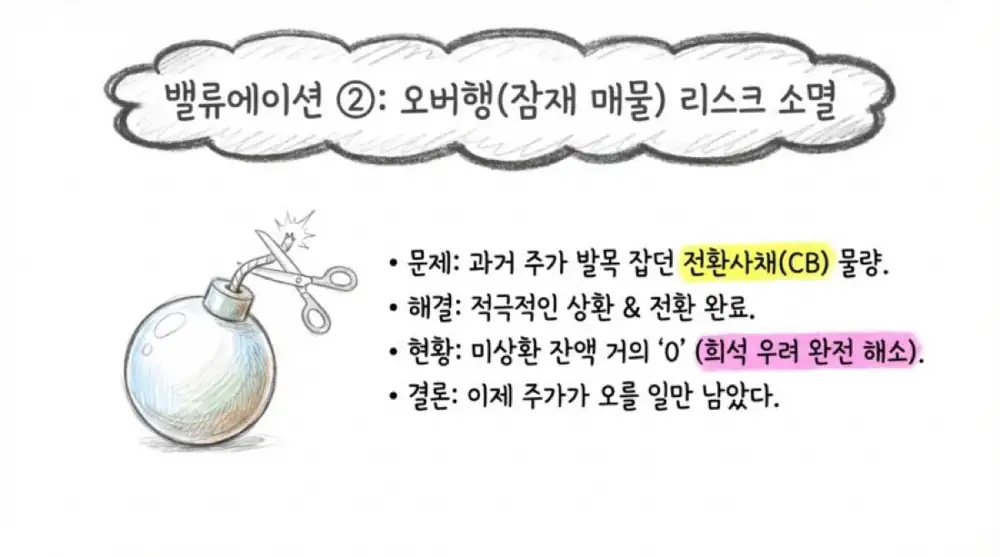

The source presents the early-2026 stock price as stuck in the KRW 400-500 range, with PBR of 0.23x and PER of 2.01x. The 9th privately placed CB issued in March 2021 totaled KRW 16.5 billion with a KRW 649 conversion price; by end-Q3 2025, the remaining balance was only KRW 330 million, or about 2% of face value. With maturity in March 2026, the source views additional dilution risk as largely gone.

6. Risks and checklist

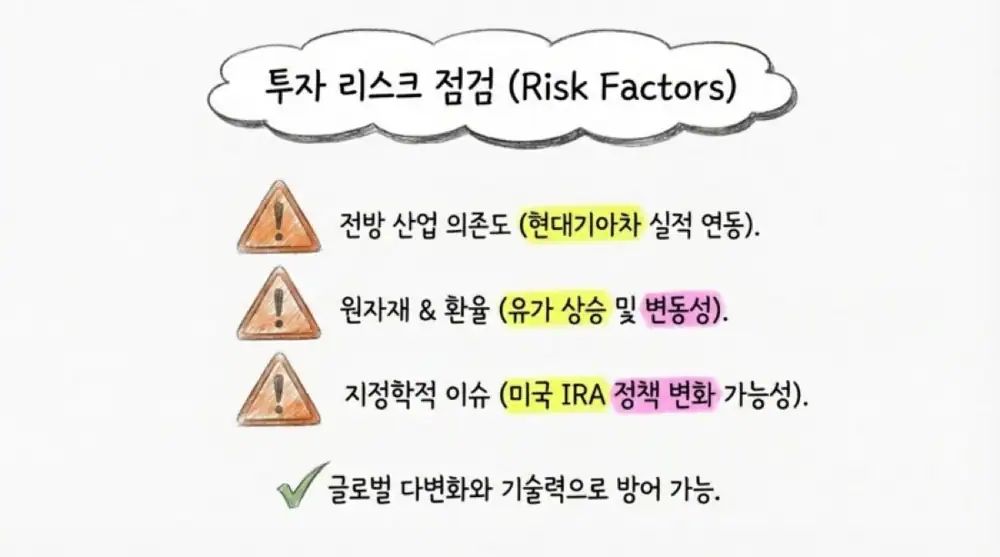

- End-customer dependence: more than 99% of revenue comes from auto parts, heavily tied to large OEMs including Hyundai Motor, Kia, Hyundai Mobis, and Volkswagen.

- Raw materials and FX: PP, PPF, PC+ABS, Nylon and currencies such as USD, EUR, MXN, and CNY can affect margins and reported income.

- Protectionism: the KRW 40 billion Mexico expansion assumes IRA and North American tariff advantages, so US policy changes could extend the payback period.

- Trading confirmation: after the KRW 440 low on December 9, 2024, the source highlights the February 4, 2026 move to KRW 591 on 1,148,796 shares of volume.

Interpretation: I read this less as a “cheap stock” case and more as a turnaround checklist: post-expansion earnings must keep improving, CB pressure must stay contained, and cash flow must keep funding debt reduction.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224194560519

- 2026년 글로벌 자동차 산업 전망 - 기계신문: https://www.mtnews.net/news/articleView.html?idxno=23928

- 자동차 경량화 소재 경쟁 - 한국자동차연구원: https://www.katech.re.kr/download/11d8ce68-2ea6-4728-bff5-6790fcb3840b;jsessionid=67887FC9CDB199824334A71D99B4C275

- KBI동국실업 멕시코 공장 증설 - 글로벌이코노믹: https://www.g-enews.com/article/Industry/2024/07/202407080947142601a67d2c7d5a_1

- KBI동국실업 멕시코 공장 증설 - 서울경제: https://m.sedaily.com/article/13916588

- KBI동국실업 멕시코 공장 증설 - 아산투데이: http://www.asantoday.com/118737

- 케이비아이동국실업 투자분석 2025.12.28 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=21bCW9anCDFrR0EY

- 케이비아이동국실업 투자분석 2026.02.15 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=QfWFHBUii7VHUrLo

- 케이비아이동국실업 투자 보고서 - Goover: https://seo.goover.ai/report/202602/go-public-report-ko-1f087adc-ef38-46e4-b405-e22332ed0d95-0-0.html

- 사출 성형 시장 보고서: https://www.businessresearchinsights.com/ko/market-reports/injection-molding-market-118719

- KBI동국실업 멕시코 400억 투자 - 뉴스웨이브: https://www.newswave.kr/news/articleView.html?idxno=513425

- KBI동국실업 멕시코 증설 완료 - 페로타임즈: https://www.ferrotimes.com/news/articleView.html?idxno=35359

- 폭스바겐그룹 2025년 상반기 실적: https://www.carmgz.kr/news/articleView.html?idxno=15166

- KBI메탈 지분현황 - WiseReport: https://comp.wisereport.co.kr/company/c1070001.aspx?cmp_cd=024840&cn=

- 박효상 KBI그룹 회장 매출 기사 - 스페셜경제: https://www.speconomy.com/news/articleView.html?idxno=325403

- 대표이사 변경 안내공시 - 한국거래소: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240401000246&docno=&viewerhost=&

- 현대모비스 파트너스데이 대상 - 중앙일보: https://www.joongang.co.kr/article/25145384

- 현대모비스 최우수 협력사 선정 - 이코노미스트: https://economist.co.kr/article/view/ecn202303070080