DEEP RESEARCH · COWEAVER

CoWeaver 2025 Q4: Optical Transport Turnaround and Quantum-Security Upside

A research-style read-through of the 2025 profit swing, fourth-quarter seasonality, and the POTN·ROADM·QKD/PQC technology moat

0. Bottom line first

My core read is that CoWeaver moved from a 2024 loss to a 2025 profit through heavy fourth-quarter revenue recognition, while also holding long-duration options in 16T POTN, OPEN ROADM, and QKD/PQC-secured transport equipment.

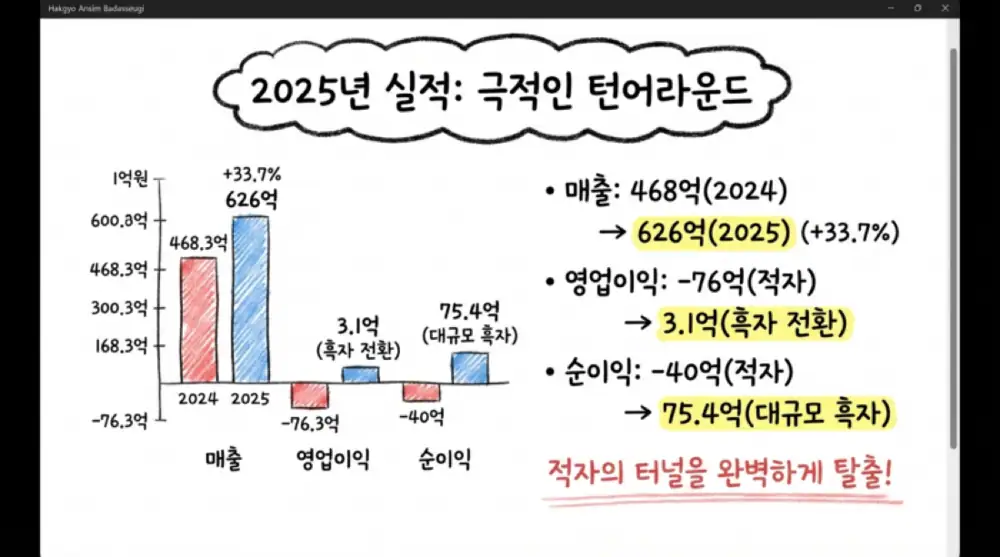

- 2025 consolidated revenue was KRW 62.59 billion, up 33.7% from KRW 46.83 billion in 2024.

- Operating profit turned positive from a KRW 7.63 billion loss in 2024 to KRW 306 million in 2025, while net income swung from a KRW 4.07 billion loss to KRW 7.54 billion.

- The source estimates that roughly KRW 26.36 billion, or about 42% of annual revenue, was recognized in Q4 alone, with Q4 operating profit of about KRW 4.59 billion and net income of about KRW 9.54 billion.

- At year-end 2025, total assets were KRW 184.0 billion, liabilities KRW 25.5 billion, and equity KRW 158.5 billion; the debt-to-equity ratio was about 16.1%.

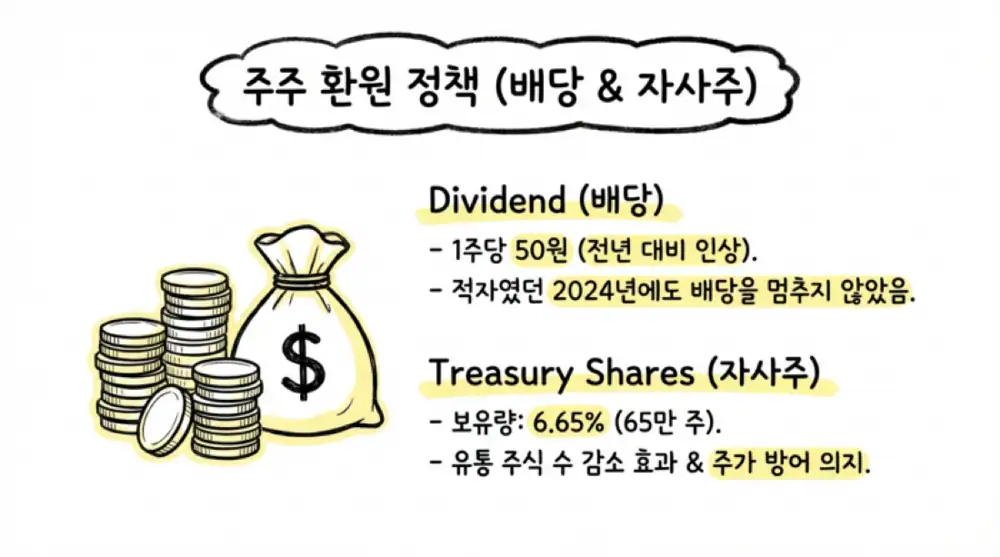

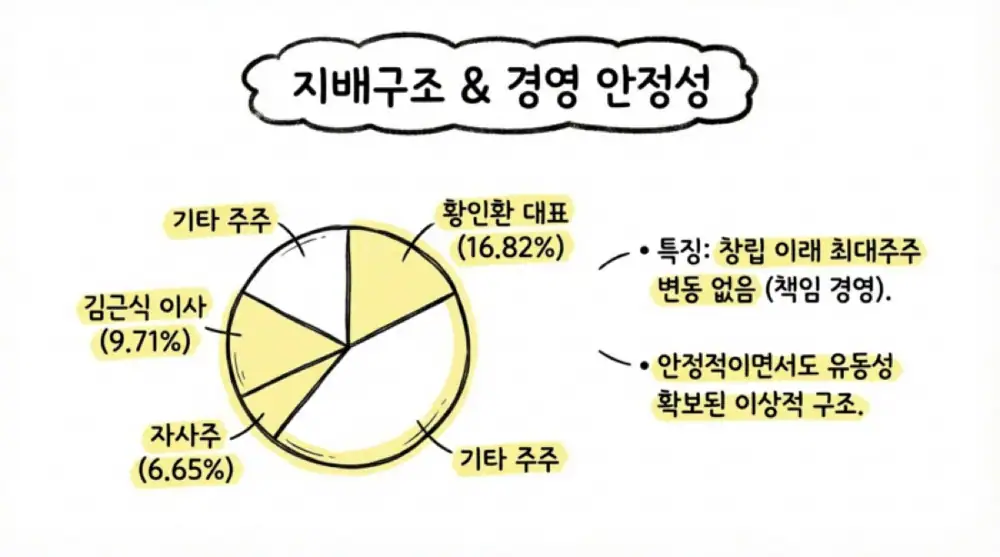

- The KRW 50 per-share cash dividend, 651,866 treasury shares, and insider stakes of 16.82% for CEO In-hwan Hwang and 9.71% for director Geun-sik Kim read as shareholder-return and owner-alignment signals.

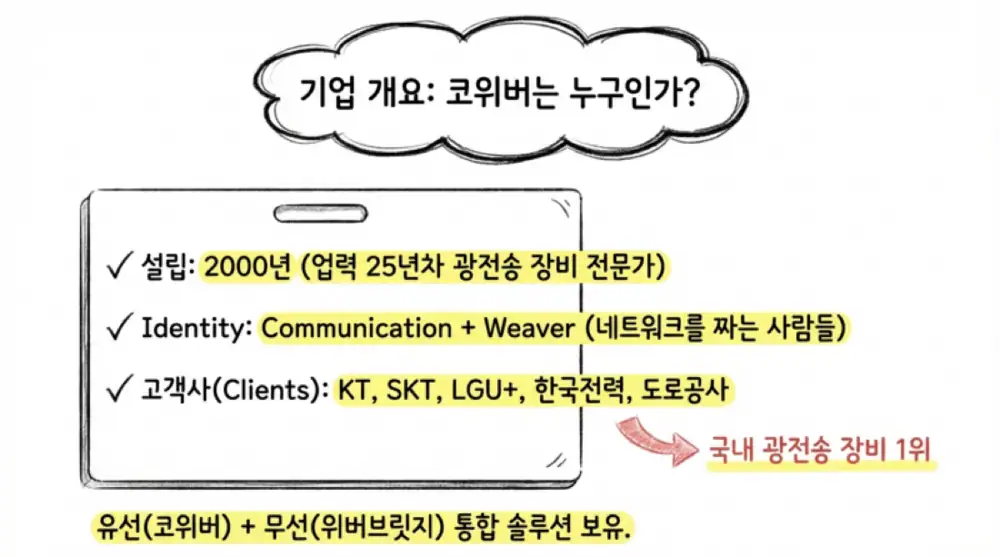

1. Business structure: optical transport across L0, L1, and L2

Official fact: CoWeaver Co., Ltd. was founded on February 19, 2000 and listed on KOSDAQ on December 4, 2001. Its head office is at 45, Magokjungang 8-ro 7-gil, Gangseo-gu, Seoul.

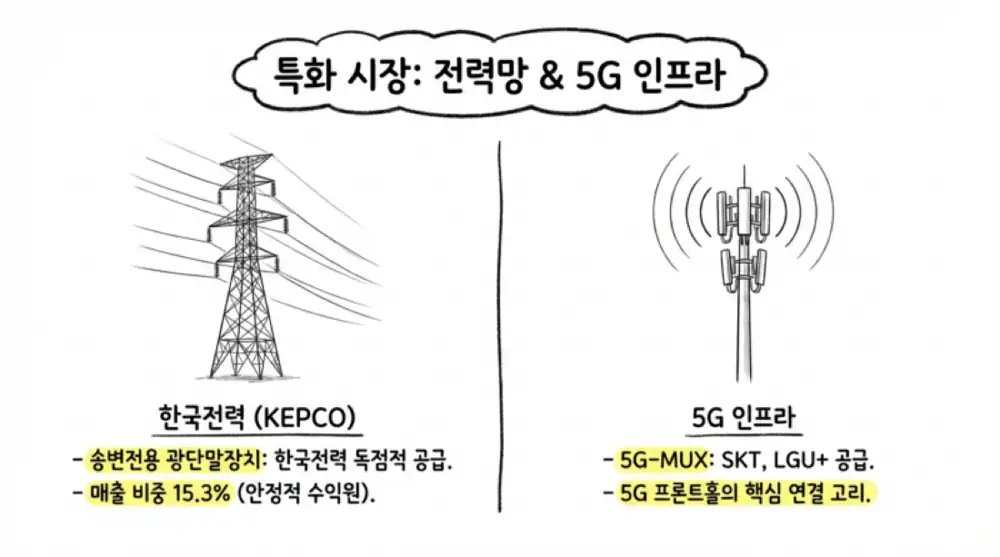

The company serves major Korean telecommunications carriers including KT, LG U+, SK Broadband, and SK Telecom, as well as public infrastructure operators such as Korea Electric Power Corporation, Korea Rail Network Authority, and Korea Expressway Corporation. In 2009 it established WeaverBridge, a wholly owned subsidiary for wireless mobile terminal equipment development and manufacturing.

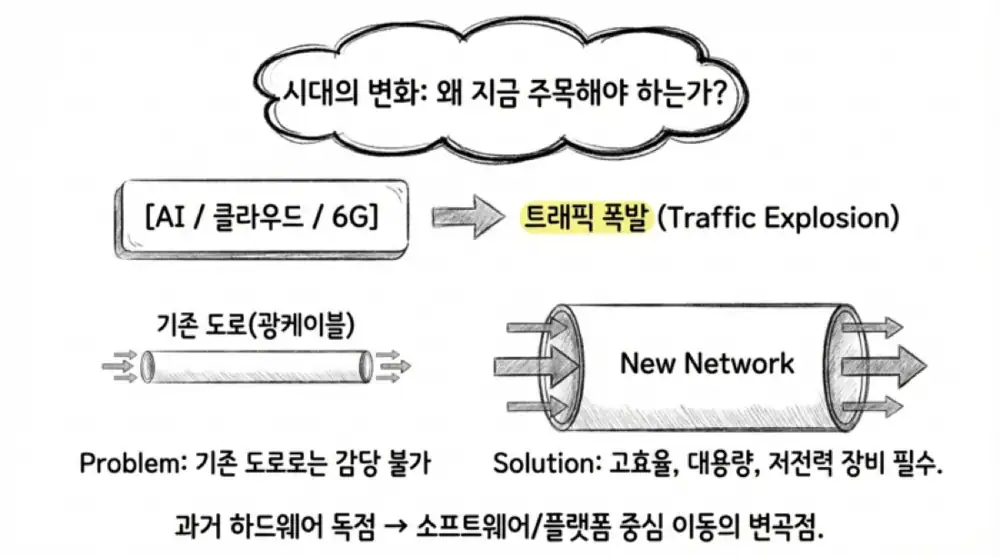

My read is that CoWeaver is not just a hardware supplier. It is an optical-network infrastructure vendor positioned around the need to make networks more efficient, higher capacity, lower power, and lower cost as AI, cloud, IoT, and immersive-media traffic grows.

| Item | 2025 3Q cumulative revenue | Share | Role |

|---|---|---|---|

| PTN | KRW 9,021 million | 24.9% | Transports voice and data services on one network |

| Power transmission terminal | KRW 5,531 million | 15.3% | Accepts power-communication signals and multiplexes them into optical signals |

| WDM | KRW 3,991 million | 11.0% | Optical transport based on wavelength division multiplexing |

| MSPP | KRW 3,585 million | 9.9% | Multiservice platform for leased lines and Ethernet |

| 5G-MUX | KRW 2,628 million | 7.3% | Link between 5G DU and RU |

| Other products | KRW 10,640 million | 29.4% | Other optical-communication and network equipment |

| Merchandise | KRW 841 million | 2.3% | Purchase and resale of raw materials and other goods |

| Total | KRW 36,237 million | 100.0% | 2025 3Q cumulative consolidated basis |

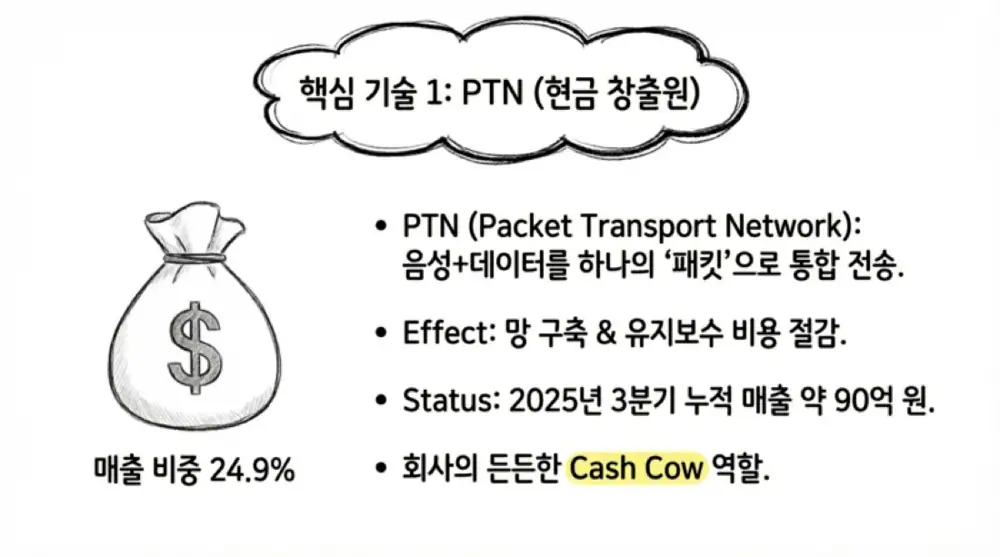

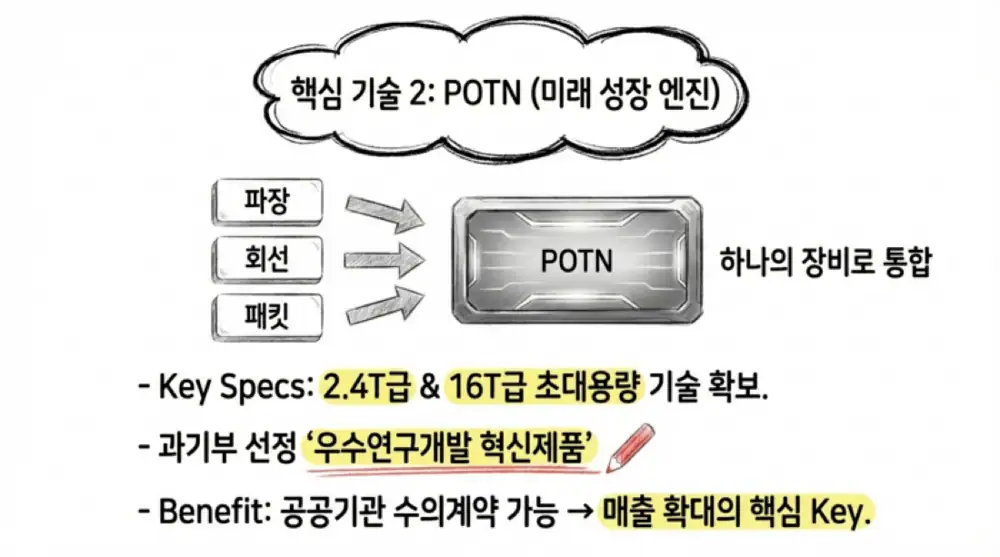

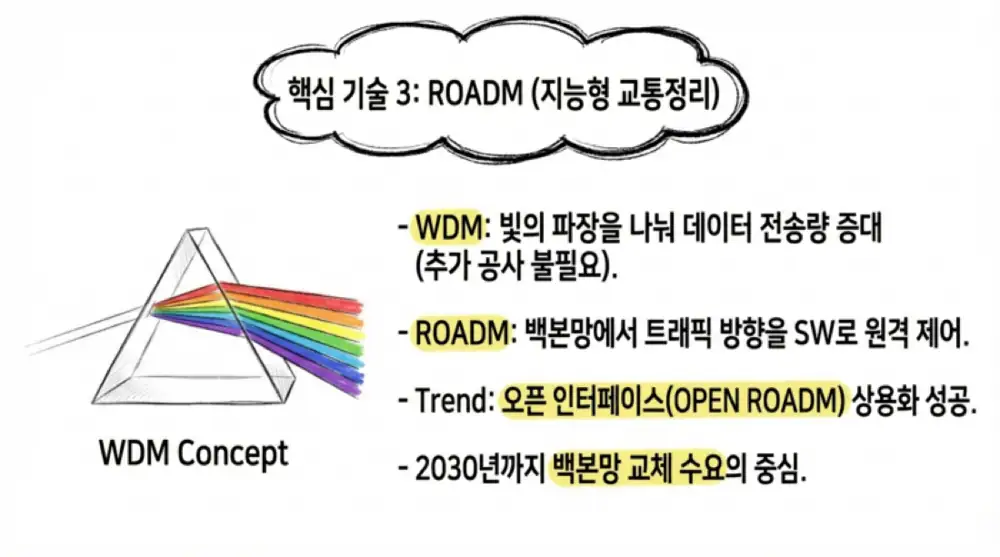

2. Product portfolio: POTN and ROADM anchor the replacement cycle

Official fact: PTN is carrier Ethernet equipment based on MPLS-TP. It generated KRW 9.02 billion of cumulative revenue through 2025 Q3, or 24.9% of total revenue of KRW 36.23 billion.

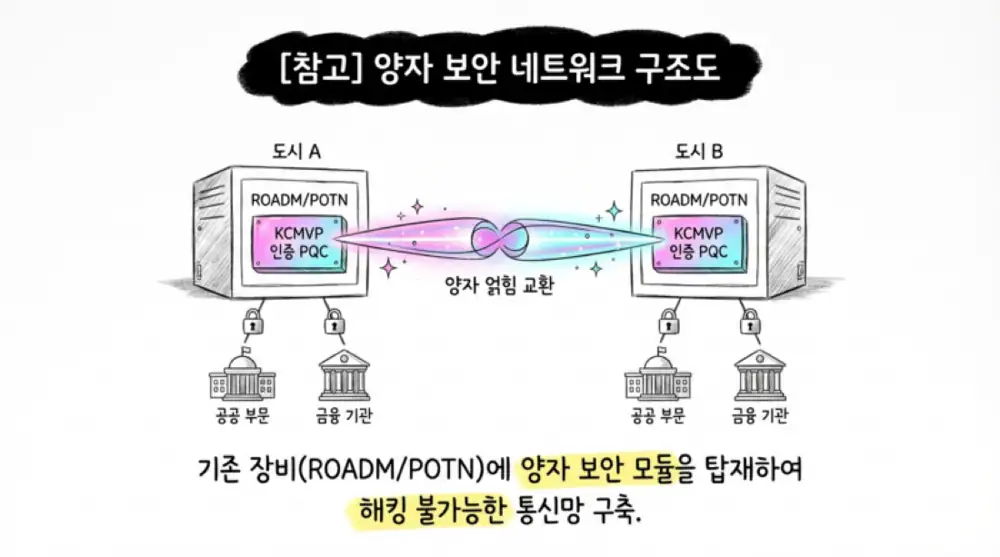

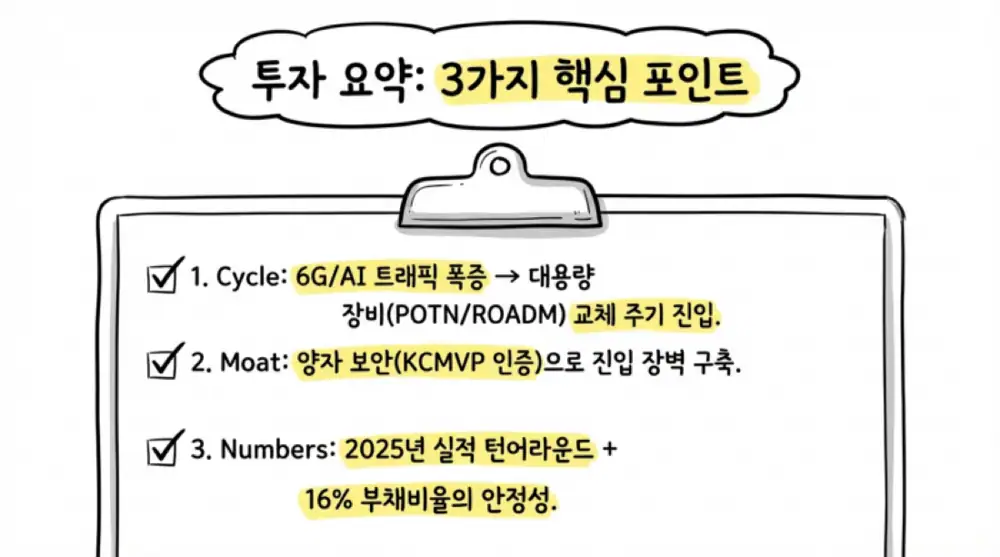

POTN integrates wavelength, circuit, and packet-layer signals into one switching and transport platform. CoWeaver commercialized the 2.4T UTRANS-8400 and received the Ministry of Science and ICT’s “excellent R&D innovative product” designation; it also completed development of a 16T ultra-large-capacity POTN device.

WDM increases capacity by carrying multiple wavelengths on one fiber, while ROADM remotely routes optical signals in backbone networks without O-E-O conversion. The source expects ROADM and POTN to become core replacement-demand drivers for next-generation backbone networks through 2030.

Current cash cow

KRW 9.02 billion in 2025 3Q cumulative revenue. This is the base equipment for carrying voice and data on one network.

Large-capacity convergence

The 2.4T commercialization and 16T development are the core options for public and telco CAPEX cycles.

Software-defined backbone

400G/1T OPEN ROADM commercialization supports the open-interface upgrade thesis.

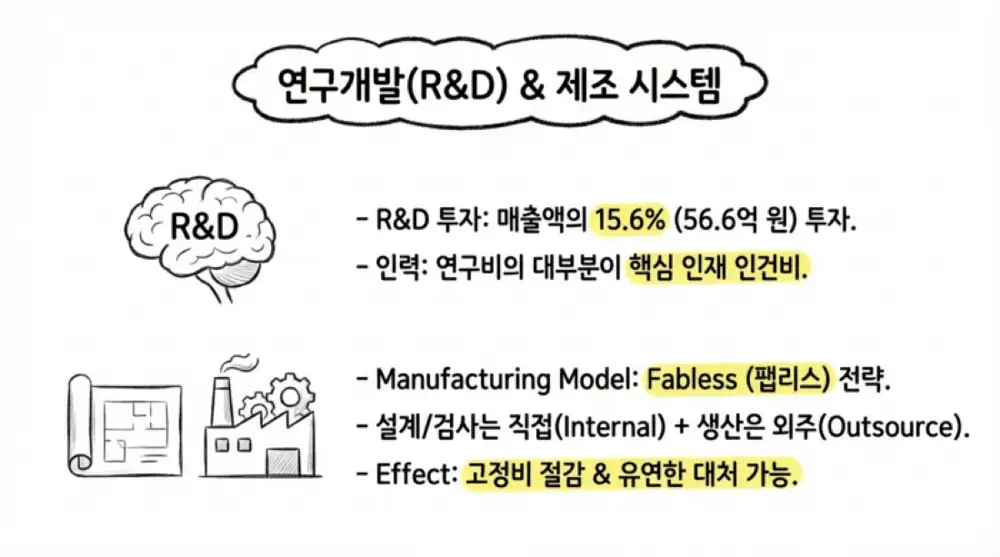

3. R&D and cost structure: 15.6% of revenue reinvested

Official fact: Cumulative R&D expense through 2025 Q3 was KRW 5.66 billion, equal to 15.6% of revenue. KRW 4.44 billion of that was invested in key engineering personnel.

The research organization is segmented under the CTO into Research Group 1, Research Group 2, research operations, technology foundation, new business, systems, PTN/POTN, ROADM, QENC, and QKD functions. Production is close to a fabless model: CoWeaver performs high-value development, design, testing, and final inspection in-house while using external facilities for physical assembly.

| Raw material | 2025 3Q cumulative purchase amount | Share | Read-through |

|---|---|---|---|

| Optic Module | KRW 3,985,289 thousand | 18.3% | Core optical-transport part, around USD 18 unit price |

| PCB | KRW 1,045,125 thousand | 4.8% | Demand for multilayer high-precision boards |

| Broadcom | KRW 524,947 thousand | 2.4% | Network switching core chipset |

| Altera | KRW 389,650 thousand | 1.8% | FPGA, around USD 20 unit price |

| PMC | KRW 254,608 thousand | 1.2% | Communication control and signal-processing chipset |

| Shelf & Panel | KRW 545,342 thousand | 2.5% | Equipment enclosures and structural panels |

| Other parts | KRW 14,580,910 thousand | 66.8% | PSUs, relays, fans, and many other parts |

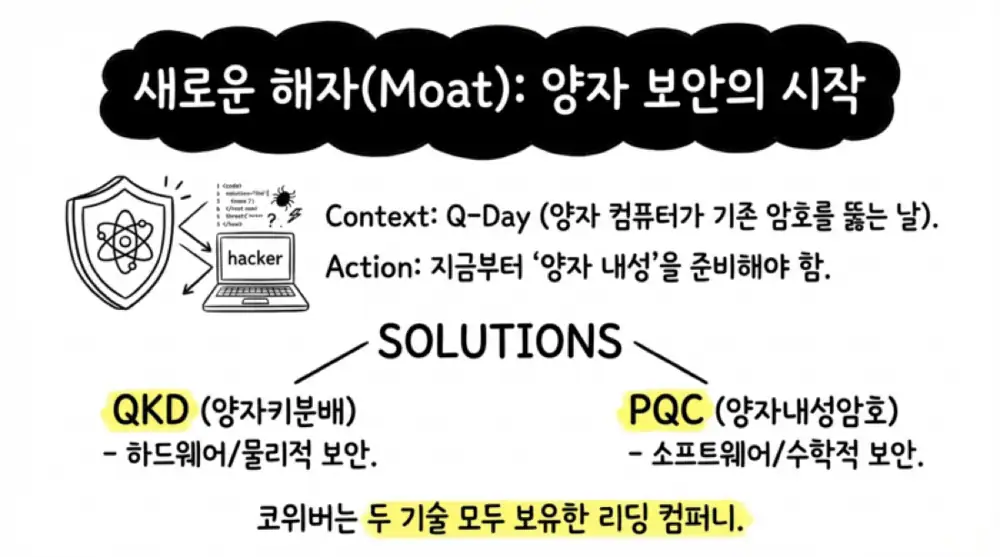

4. Quantum security: QKD and PQC create a regulatory moat

The source argues that cybersecurity is shifting from conventional RSA-style cryptography toward architectures that can withstand quantum-computer threats. CoWeaver’s differentiation is that it addresses both physical-layer quantum key distribution and algorithm-layer post-quantum cryptography.

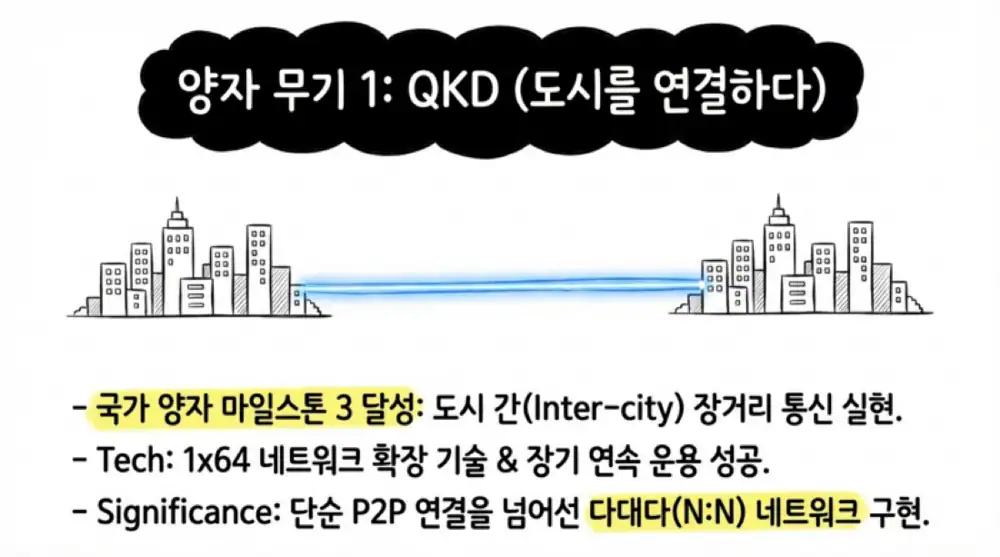

Official fact: The source defines Milestone 3 as intercity quantum communication using entanglement swapping, Milestone 4 as intrastate quantum-entanglement distribution using quantum repeaters, and Milestone 5 as the transition from demonstration research to operating infrastructure across institutions.

CoWeaver has conducted joint research with KIST and KT. It applied time, wavelength, and polarization multiplexing to QKD systems, expanded to a 1x64 network, and presented a field-fiber demonstration of stable 1x4 network operation for more than a week.

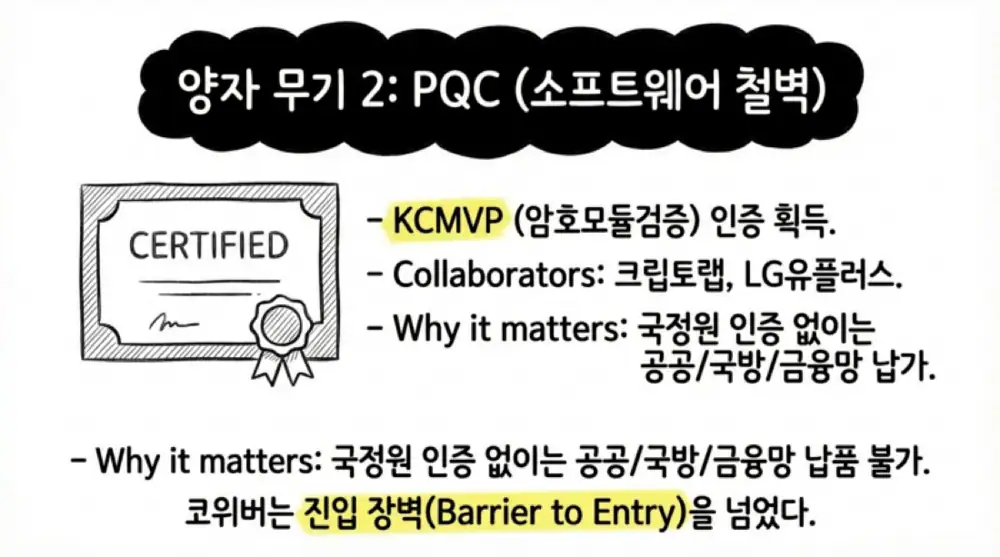

Official fact: CoWeaver jointly developed a PQC encryption module mounted in ROADM equipment with CryptoLab and LG U+. Since 2022 it has participated in the LG U+-led national pilot project for quantum cryptography communication infrastructure, with examples including Jeollanam-do office video conferencing and Kakao Mobility parking/payment unmanned gates.

Interpretation: KCMVP certification matters because it clears a regulatory threshold for supplying encrypted communication equipment to public agencies, local governments, national defense data centers, and financial private networks. The key point is that CoWeaver’s equipment can move from transport gear to a security gateway.

5. 2025 results: Q4 concentration drove the profit swing

Official fact: Based on the February 23, 2026 board resolution, estimated 2025 consolidated revenue was KRW 62,599,540,297, up KRW 15,763,324,688 or 33.7% from KRW 46,836,215,609 in 2024.

| Metric | 2024 | 2025 estimate | Change | Status |

|---|---|---|---|---|

| Revenue | KRW 46,836,215,609 | KRW 62,599,540,297 | +KRW 15,763,324,688 | +33.7% |

| Operating profit | -KRW 7,634,892,172 | KRW 306,265,207 | +KRW 7,941,157,379 | Turned profitable |

| Pre-tax profit | -KRW 4,995,801,945 | KRW 1,848,374,293 | +KRW 6,844,176,238 | Turned profitable |

| Net income | -KRW 4,074,396,606 | KRW 7,544,637,263 | +KRW 11,619,033,869 | Turned profitable |

| Total assets | KRW 151,090,414,660 | KRW 184,022,424,070 | +KRW 32,932,009,410 | +21.8% |

| Total liabilities | KRW 24,442,609,577 | KRW 25,523,102,724 | +KRW 1,080,493,147 | +4.4% |

| Total equity | KRW 126,647,805,083 | KRW 158,499,321,346 | +KRW 31,851,516,263 | +25.1% |

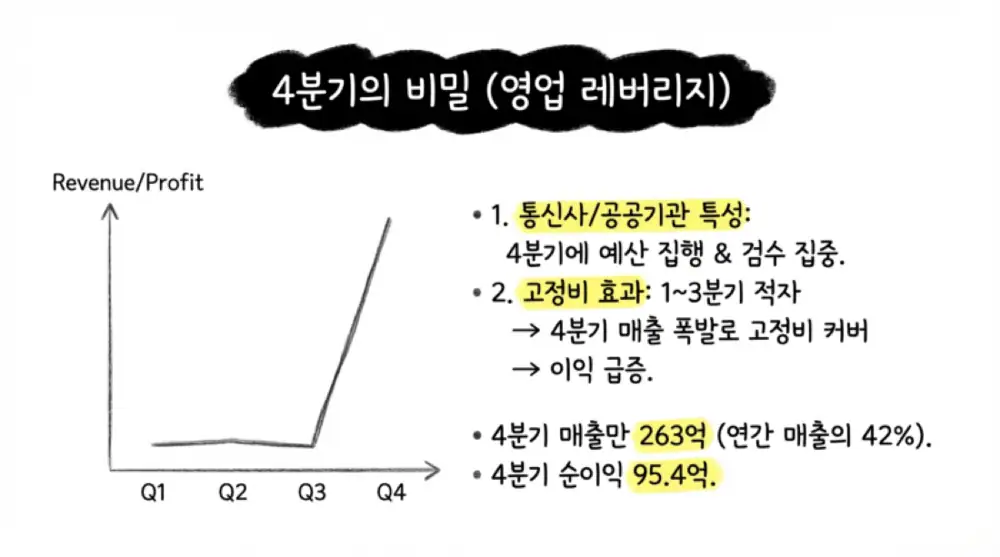

Interpretation: The move from 2025 Q3 cumulative revenue of KRW 36.23 billion, operating loss of KRW 4.28 billion, and net loss of KRW 2.00 billion to a full-year profit implies a very large Q4. The source estimates Q4 revenue of about KRW 26.36 billion, operating profit of about KRW 4.59 billion, and net income of about KRW 9.54 billion.

This pattern fits the seasonality of B2B/B2G telecom-equipment revenue. Telecom carriers and public agencies tend to concentrate budget execution, infrastructure completion, and final acceptance in Q4. In a cost base with more than KRW 6 billion of annual labor expense and more than KRW 7 billion of recurring R&D expense, crossing breakeven in Q4 creates operating leverage.

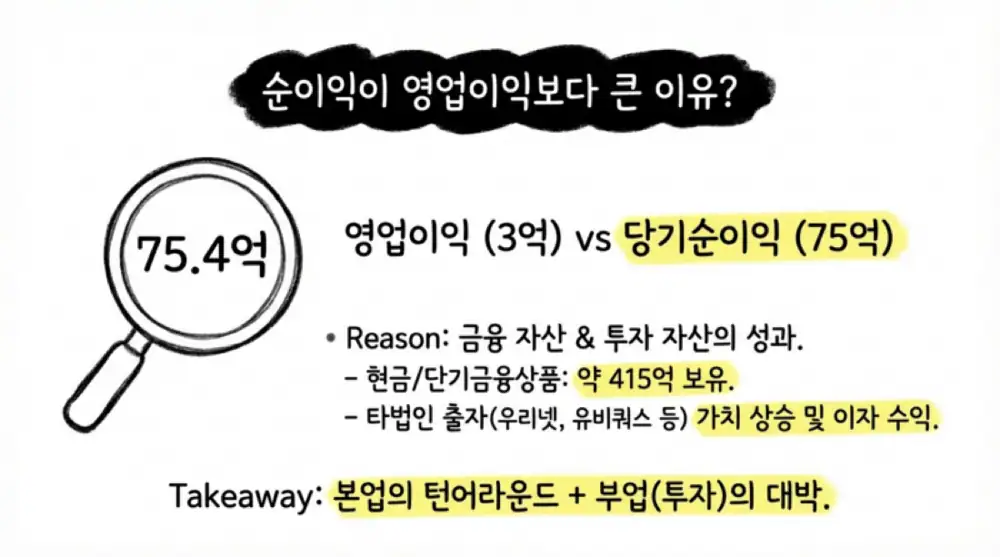

The roughly KRW 7.24 billion gap between operating profit of KRW 306 million and net income of KRW 7.54 billion is interpreted as potential financial/non-operating income, valuation gains on investment assets, interest income, non-core asset sales, or deferred tax-asset realization from loss carryforwards. Because the specific disclosure details are not in the source, this needs follow-up.

6. Balance sheet, dividend, and governance

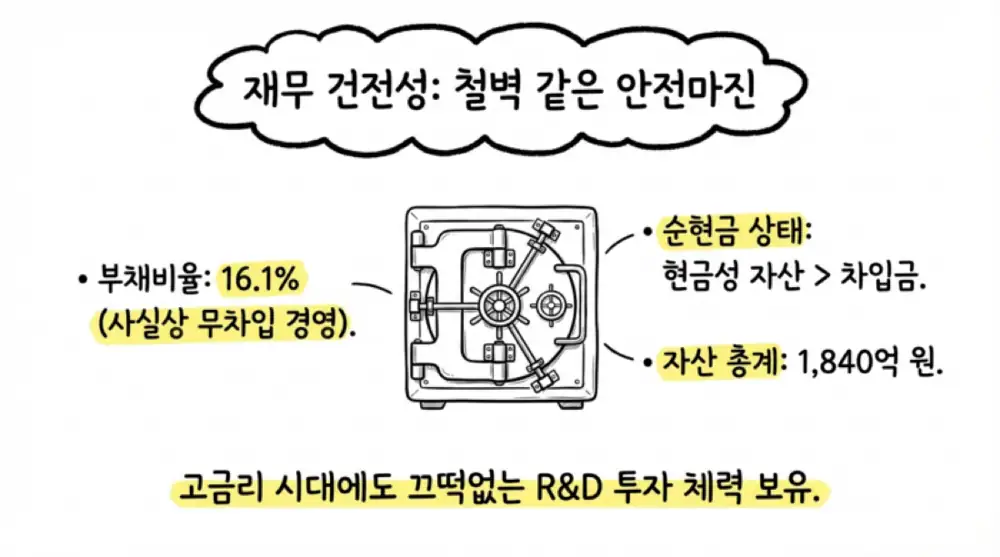

Official fact: At the end of 2025, total assets were KRW 184.0 billion, total liabilities KRW 25.5 billion, and equity KRW 158.5 billion. The debt-to-equity ratio was about 16.1%.

At 2025 Q3, CoWeaver held about KRW 41.5 billion in cash and short-term financial products, about KRW 26.5 billion in financial assets measured at fair value through profit or loss, and investment property of about KRW 3.9 billion with fair value of KRW 5.76 billion. Even with KRW 12.5 billion of total borrowings, cash equivalents of KRW 3.65 billion plus KRW 25.0 billion of short-term financial products point to a net-cash profile.

FX and interest-rate sensitivities were also limited in the source: a 10% FX move would affect profit or loss by about KRW 5.5 million, while a 1% rate increase on KRW 10.5 billion of floating-rate debt would reduce pre-tax profit by only KRW 78.75 million.

Official fact: The company decided a KRW 50 cash dividend per common share for the 2025 fiscal year. The total dividend is KRW 457,246,700, the dividend yield is 0.9%, the record date is December 31, 2025, and the scheduled payment date is April 15, 2026.

The company paid KRW 30 per share even in the loss-making 2024 year and raised the payout to KRW 50 after the 2025 turnaround. At 2025 Q3 it held 651,866 treasury shares, equal to about 6.65% of 9,796,800 shares outstanding. Dividends are paid on 9,144,934 shares excluding treasury stock.

Governance is summarized as CEO In-hwan Hwang holding 16.82% or 1,647,362 shares, director Geun-sik Kim holding 9.71% or 951,697 shares, and other retail/institutional investors holding about 66.8%. The source interprets the absence of any founder-to-date controlling-shareholder change as a stable ownership structure.

7. Risks and follow-up points

- Q4 concentration: Because acceptance and budget execution are year-end-heavy, 2026 orders and revenue recognition timing need quarterly tracking.

- Parts procurement: Costs and lead times for optic modules, PCBs, Broadcom chips, Altera FPGAs, and other key parts can affect gross margin.

- Non-operating income durability: Part of the 2025 net-income expansion appears to include non-operating factors, so recurring operating profit should be separated from one-time gains.

- Quantum-security commercialization: QKD/PQC technology and KCMVP certification are moats, but actual defense, finance, and municipal closed-network wins are the proof point.

8. Final read

My summary is that CoWeaver is an optical-transport equipment company with exposure to both next-generation backbone replacement and quantum-security demand. The 2025 turnaround to KRW 62.6 billion revenue and KRW 7.54 billion net income shows that Q4 revenue concentration and higher-value equipment mix can overcome the fixed-cost base.

Interpretation: The most important 2026 test is whether 16T POTN, OPEN ROADM, and QKD/PQC-secured equipment translate into actual orders and margin improvement. If that happens, CoWeaver can be revalued from a telecom-equipment subcontractor into a network-security infrastructure company for the 6G and quantum era.

Sources

- Original Naver blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224192940028

- Quantum Information Technology white paper: https://www.researchgate.net/profile/Jihyun-Kim-74/publication/366494257_Quantum_Information_Technology_white_paper/links/63c526dbd7e5841e0bd1c1f3/Quantum-Information-Technology-white-paper.pdf

- Quantum Technology white paper PDF - Scribd: https://www.scribd.com/document/630861389/%EC%96%91%EC%9E%90%EA%B8%B0%EC%88%A0%EB%B0%B1%EC%84%9C-pdf

- Mobile carriers advance in quantum market - iNews24: https://www.inews24.com/view/1446764

- LG U+ quantum cryptography infrastructure project - Smart Economy: http://www.dailysmart.co.kr/news/articleView.html?idxno=61457

- LG U+ quantum cryptography infrastructure project - SME Daily: https://www.smedaily.co.kr/news/articleView.html?idxno=234042

- CoWeaver obtains domestic certification for quantum-safe communication - MarketIn: https://marketin.edaily.co.kr/News/ReadE?newsId=02646966639055544

- CoWeaver decides KRW 50 year-end cash dividend - DigitalToday: https://www.digitaltoday.co.kr/news/articleView.html?idxno=633181

- Source external image 1: https://lh7-rt.googleusercontent.com/docsz/AD_4nXc0rkJHwOPElQ_X3Edj8-HS-i5fHDmGL2LfWPB8IILfDOfXROQKb8odpM7Nwg41_7qFE53qWqVoReodnlwVEQ_swGiTuWgeGsDC-tGVeoKdcahHezWgCcZg2HKkRDSxv57OQgdmHgVtkw6N20D5NELjxEaohKk?key=3Pj3CauD6-OEVTRstYpl7Q

- Source external image 2: https://lh7-rt.googleusercontent.com/docsz/AD_4nXdPFaXpchkvu_Ch-vl1hbSBt-UJG0ZwfSWASZ-3ARhbTRW4CPba7QALFs1vA3Oxk6nZgYvDsYy8G4dbsB8CVLnV0tNnYng-2qHNXiJU77zLync8yE9QAZAiaUVbhPZXySH17Cxn3Gd8Nl2mIOcLCm0DzBg42UM?key=3Pj3CauD6-OEVTRstYpl7Q