DEEP RESEARCH · BH/4Q25 RESULTS & FPCB

BH 2025 Fourth-Quarter Preliminary Results Analysis

A review of profitability turnaround, capital redeployment, and the foldable, IT OLED, automotive, and robot-charging order cycle

0. Bottom line first

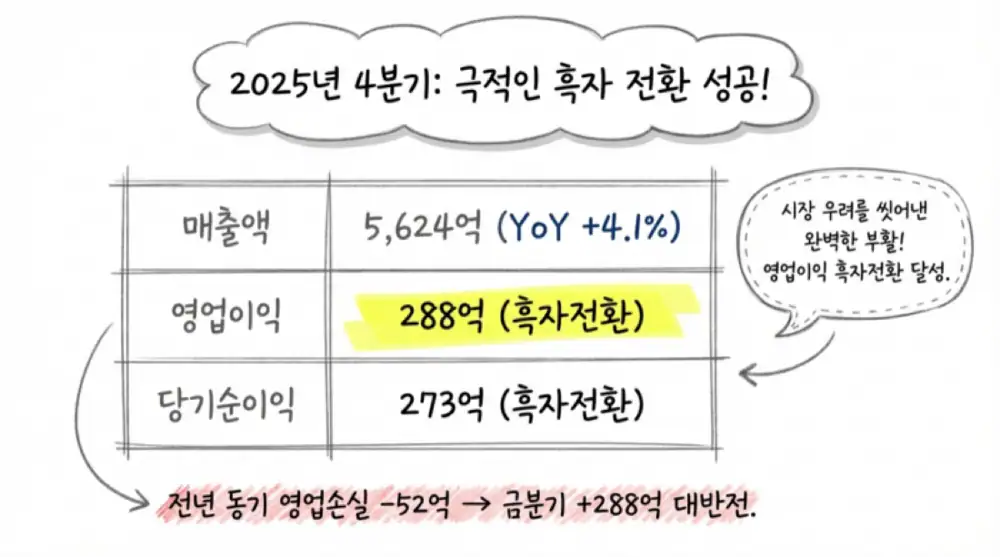

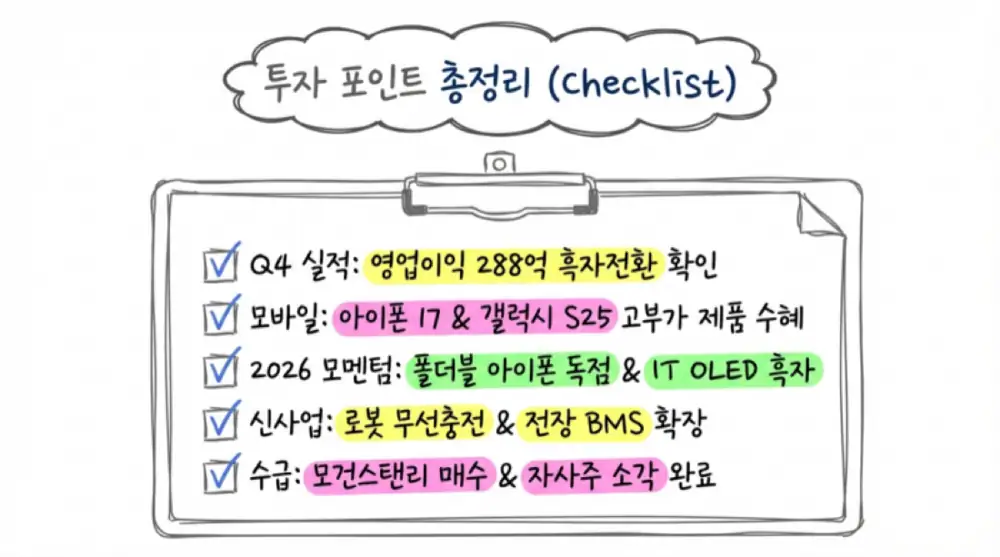

BH's 4Q25 was not just a seasonal rebound. High-value mobile FPCB and automotive subsidiary BH EVS overwhelmed IT OLED upfront costs. Revenue reached KRW 562.466 billion and operating profit KRW 28.822 billion, turning around from an operating loss in the prior year; pre-tax profit was KRW 45.536 billion, up 325.5% YoY.

I see three key points. First, the high-value product mix centered on iPhone 17 Pro Max and Korean OLED panel share near 98% lifted FPCB volume. Second, the company secured about KRW 56.7 billion in growth capital without new-share dilution through EB, PRS, and treasury-stock cancellation in 3Q25. Third, 2026 brings a new order cycle across foldable iPhone, IT OLED, robot wireless charging, and BMS FPCB.

1. 4Q25 results: from operating loss to profit

Official fact: Preliminary 4Q25 consolidated revenue was KRW 562.466 billion, up 4.1% from KRW 487.879 billion a year earlier. Operating profit was KRW 28.822 billion, turning around from an operating loss of KRW 5.293 billion in 4Q24.

| Financial metric | 4Q24 | 3Q25 | 4Q25 preliminary | YoY | QoQ |

|---|---|---|---|---|---|

| Revenue | KRW 487,879mn | KRW 508,037mn | KRW 562,466mn | +4.1% | -9.7% |

| Operating profit | -KRW 5,293mn | KRW 34,483mn | KRW 28,822mn | Turnaround | -16.4% |

| Pre-tax profit | KRW 6,959mn | KRW 29,613mn | KRW 45,536mn | +325.5% | -35.0% |

| Net income | -KRW 2,300mn | KRW 40,005mn | KRW 27,347mn | Turnaround | -31.6% |

| Controlling shareholder net income | -KRW 4,903mn | KRW 37,841mn | KRW 25,217mn | Turnaround | -33.4% |

Full-year 2025 cumulative revenue was KRW 1.79266 trillion, up 2.2% from KRW 1.754442 trillion in 2024. Full-year operating profit was KRW 53.978 billion, down 38.0% from KRW 87.053 billion. The source attributes annual profit pressure to equipment investment and depreciation for the IT OLED lineup during the first half of 2025.

2. Structural reasons for the earnings rebound

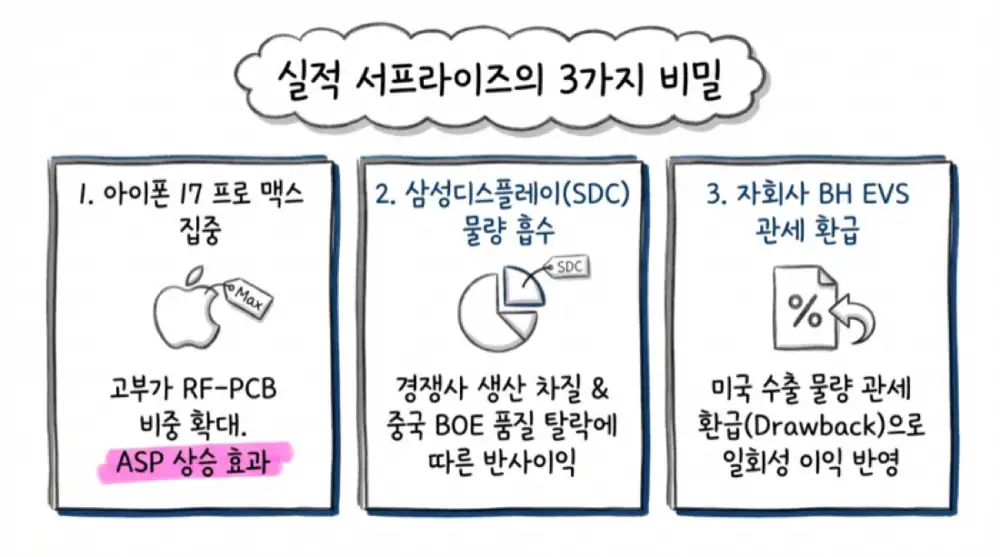

High-value mix

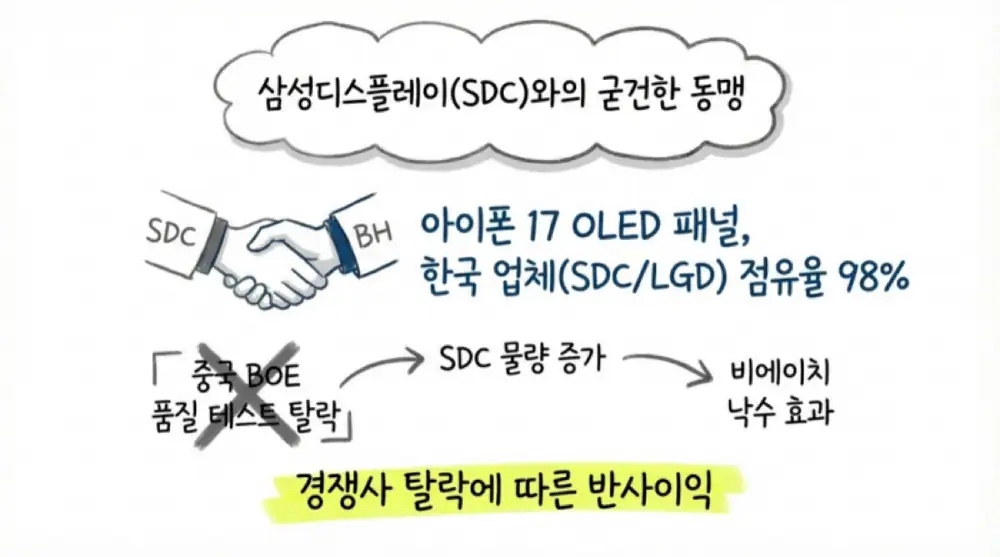

Demand centered on iPhone 17 Pro Max lifted RF-PCB shipments and ASP.

Panel customer share

While China's BOE struggled with quality tests, Korean display makers secured about 98% share of iPhone 17 OLED panels.

BH EVS refund effect

Tariff drawback on U.S.-bound exports acted as a one-off upside factor.

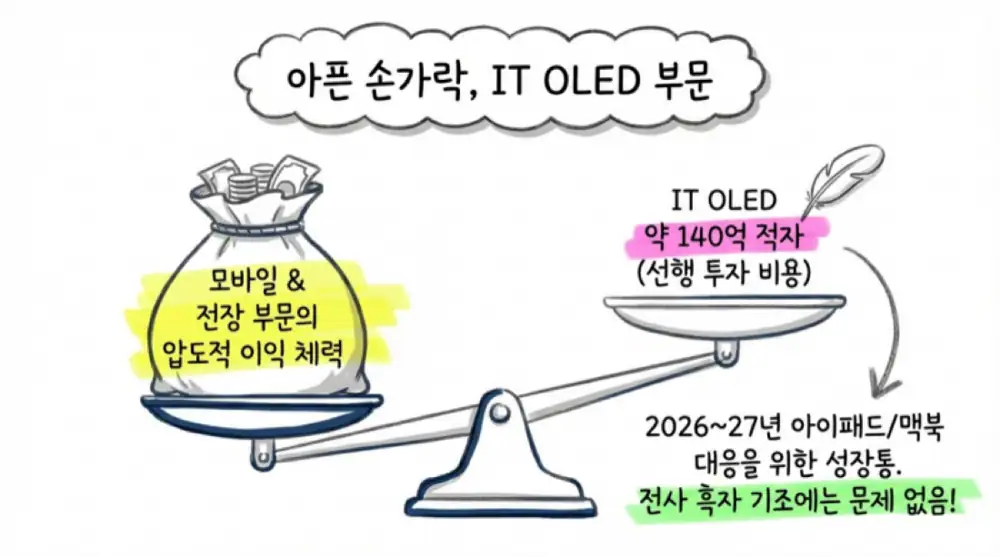

IT OLED loss

New-line fixed costs likely caused about KRW 14.0 billion in 4Q operating loss, but mobile and automotive profits overwhelmed it.

Interpretation: The quarter matters because core competitiveness recovered. Recording large operating profit despite IT OLED losses shows that high-value mobile FPCB and automotive earnings can absorb 2026 upfront investment costs.

3. Shareholders and capital redeployment

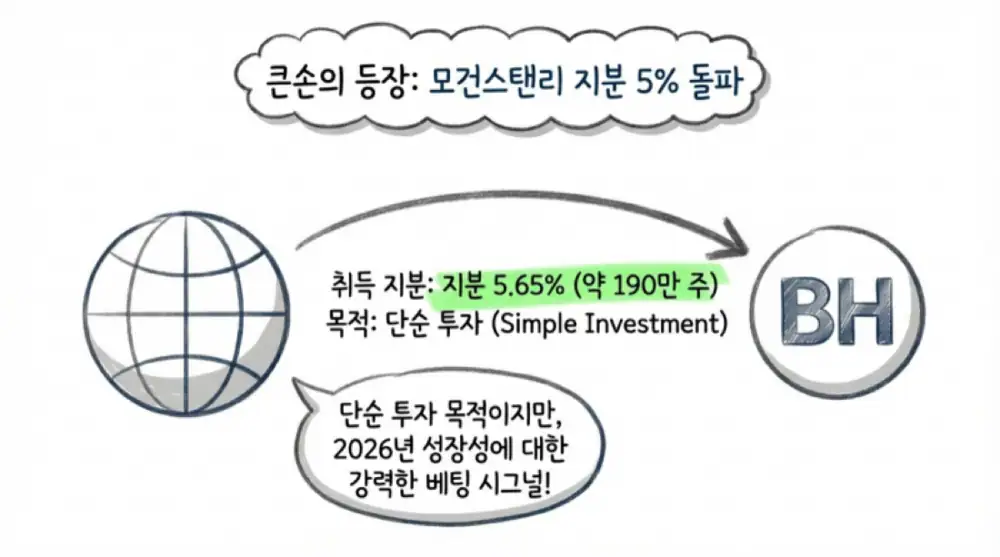

Official fact: In February 2026, Morgan Stanley & Co. International plc newly crossed the 5% ownership threshold in BH. With February 11, 2026 as the reporting-trigger date, it disclosed on February 20 that it held 1,906,186 shares, or 5.65%, for simple investment purposes.

Morgan Stanley moved from 1,562,126 shares, about 4.63%, then bought 312,866 shares and sold 9,088 shares on February 11, reaching 1,865,904 shares and crossing the 5% reporting threshold. Further trading from February 12 to 19 finalized the holding at 1,906,186 shares. The largest shareholder group, including Chairman Lee Kyung-hwan and related parties, holds 7,317,145 shares and 21.71%, maintaining stable control.

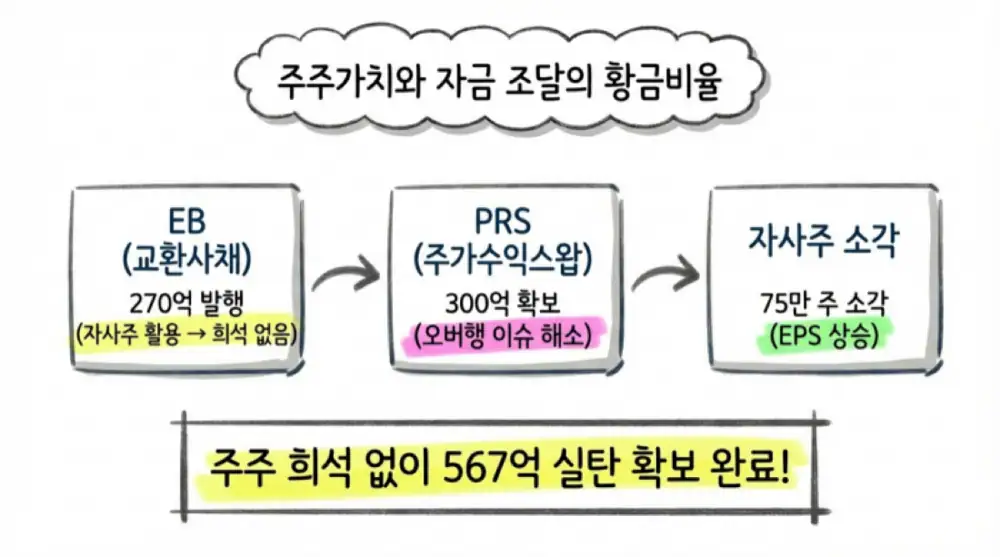

| Capital strategy | Detail | Effect |

|---|---|---|

| Exchangeable bond | KRW 27.0bn privately placed, unsecured, bearer EB issued on September 23, 2025. Exchange asset: 1,250,000 treasury shares. Exchange price: KRW 21,600. Maturity: September 23, 2030 | Secures growth capital using treasury shares rather than new issuance, reducing dilution risk |

| PRS | Price Return Swap using 1,646,054 treasury shares as underlying asset, about KRW 29.7bn, signed on September 16, 2025. Base price: KRW 18,100. Maturity: September 13, 2027 | Secures about KRW 30.0bn of liquidity without a large market overhang; upside settlement possible if the share price rises |

| Treasury-stock cancellation | 752,841 common treasury shares cancelled from distributable earnings on September 18, 2025 | Reduces floating shares and improves EPS, supporting shareholder value |

Interpretation: BH secured about KRW 56.7 billion in growth capital through EB and PRS while offsetting dilution concerns with treasury-share cancellation. I view this as pre-funding for 2026 foldable, IT OLED, and automotive opportunities.

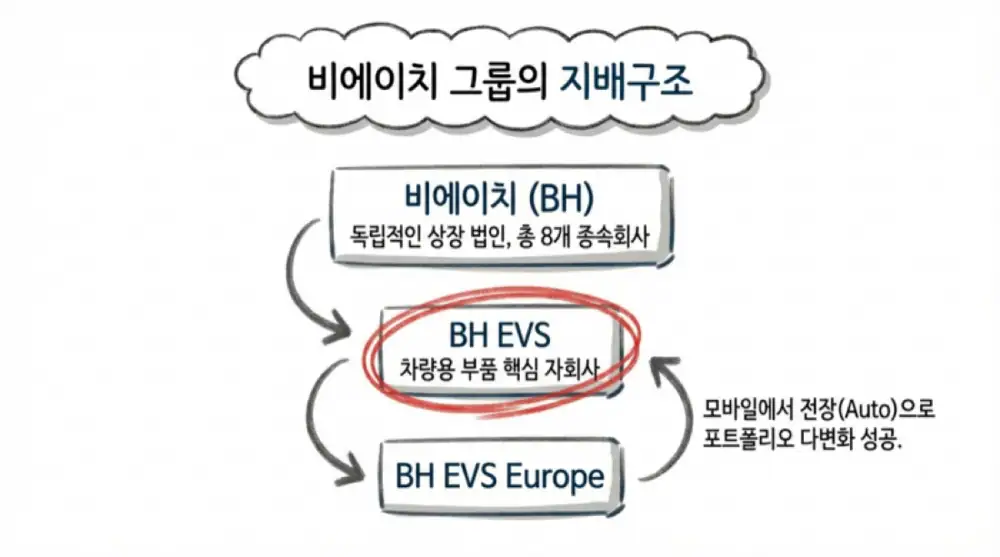

4. Subsidiaries and global automotive expansion

BH is an independent listed company without a controlling parent company. The number of consolidated subsidiaries rose from seven at the beginning of 3Q25 to eight at quarter-end, all unlisted, with three major subsidiaries.

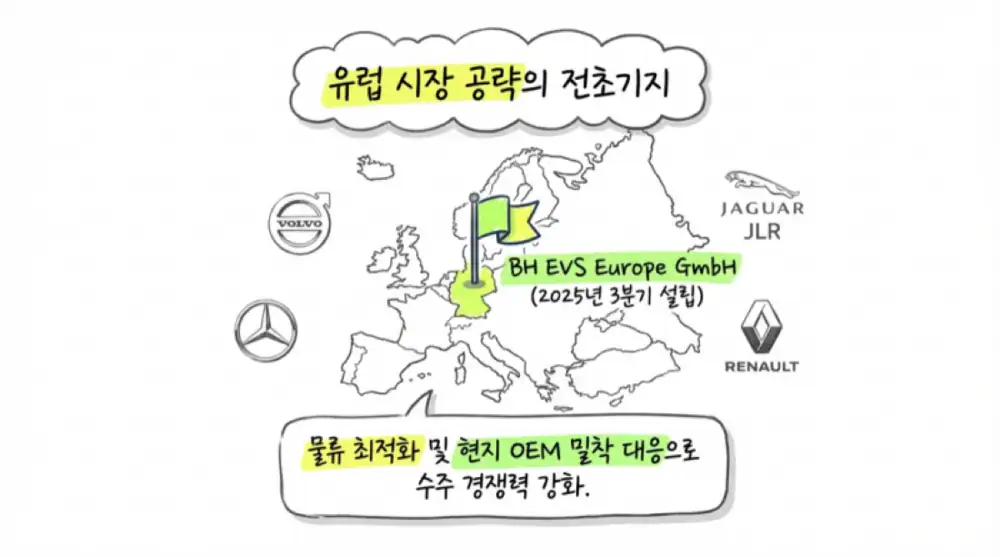

Official fact: BH EVS Europe GmbH was newly included in consolidation during 3Q25. It is a European sales entity established with 100% investment from BH EVS, targeting regions such as Germany. It is intended as a forward base to serve OEMs such as Volvo, Renault, Land Rover, Skoda, and Mercedes-Benz.

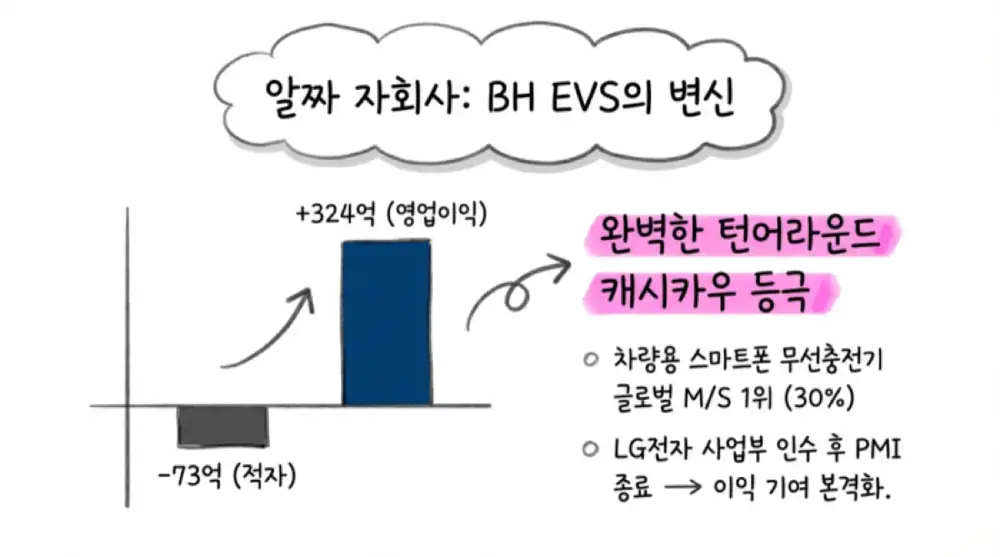

Official fact: BH EVS is an automotive electronics subsidiary established in October 2022 when BH acquired LG Electronics' vehicle wireless charging business from the VS division for KRW 136.7 billion. It recorded an operating loss of KRW 7.3 billion in 2023, then turned around to KRW 348.9 billion in revenue and KRW 32.4 billion in operating profit in 2024.

The source says BH EVS has a 30% share of the in-vehicle smartphone wireless charger market and is global No. 1. As of late 2025, BH owned about 41% to 49% of BH EVS, while second-largest shareholder DKT held 36.1%, creating SMT module assembly cost and quality synergies.

5. Customer diversification and 2026 new-order pipeline

BH's traditional revenue was concentrated in FPCB attached to smartphone OLED panels. Since 2025, the end-market and customer ecosystem has expanded across mobile, IT devices such as tablets and notebooks, automotive electronics, and robotics.

| Pipeline | Source detail | Investment read |

|---|---|---|

| Display and mobile | Samsung Display is the key tier-1 customer, and final products go into Apple iPhones and Samsung Galaxy models. Korean companies are cited as having about 98% iPhone 17 OLED panel share. | BH's No. 1 FPCB share within SDC connects directly to high-value model demand. |

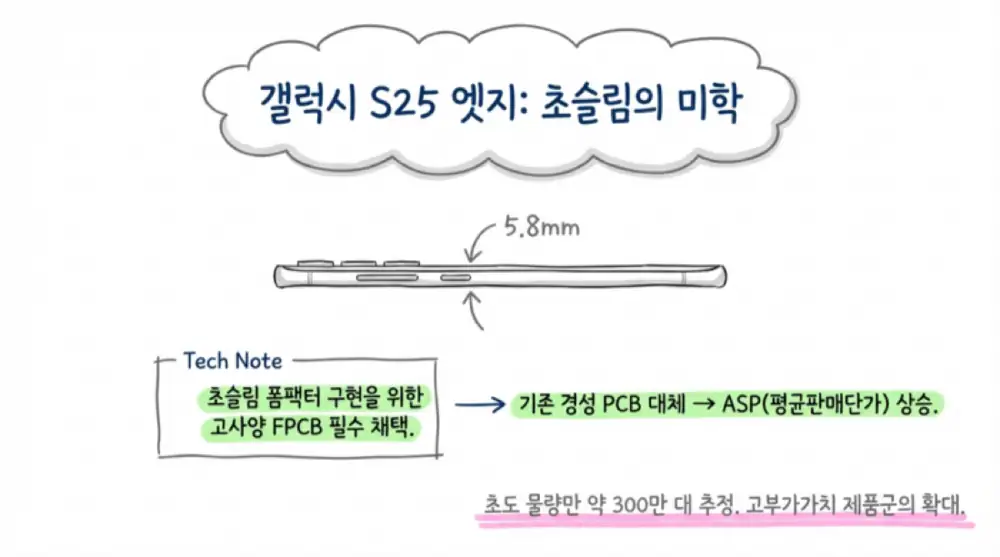

| Galaxy S25 Edge | BH's ultra-thin FPCB was adopted, with initial volume estimated at about 3 million units. A sub-5.8mm ultra-slim form factor requires high-spec FPCB. | Fine-pattern and space-efficiency capability can support ASP increases. |

| Automotive customers | Customers diversify to GM, Ford, Stellantis, Tesla, Volvo, Mercedes-Benz, Renault, Land Rover, Nissan, and Honda. | Reduces company-level risk from a single smartphone customer or region. |

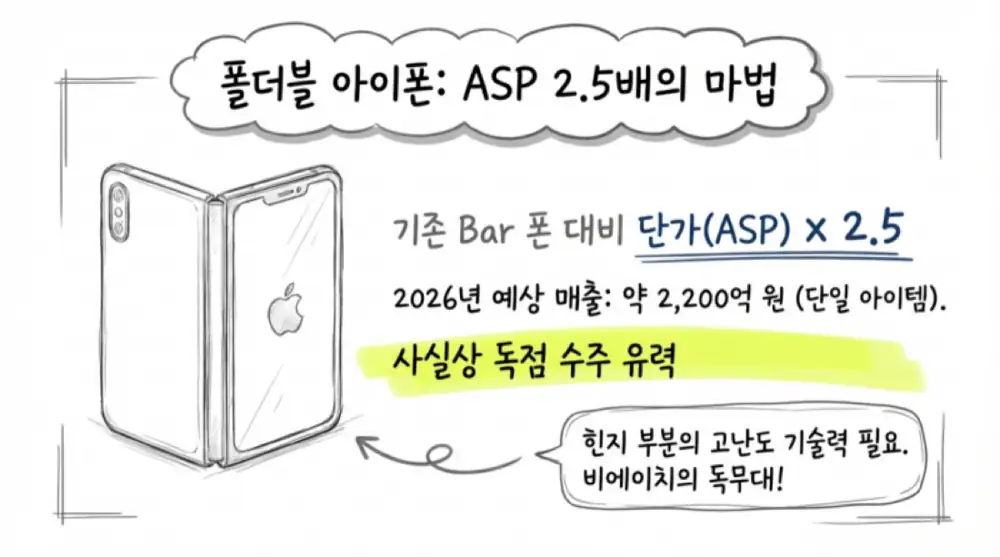

Foldable iPhone FPCB

Apple's first foldable smartphone, expected in the second half of 2026, is presented as the biggest growth engine. Foldable display FPCB must handle hinge durability and complex signal processing, so board layer count and specifications rise versus bar-type smartphones, and the supply ASP is said to be about 2.5 times higher.

Official fact: The source says BH is likely to secure Samsung Display's foldable iPhone FPCB volume at a near-exclusive level. Foldable iPhone FPCB shipments are estimated at 8.5 million units in 2026 and 21.9 million units in 2027. Assuming 100% internal-display share and 50% external-display share, the source forecasts KRW 220.0 billion in new 2026 revenue and KRW 556.0 billion in 2027 from foldable alone.

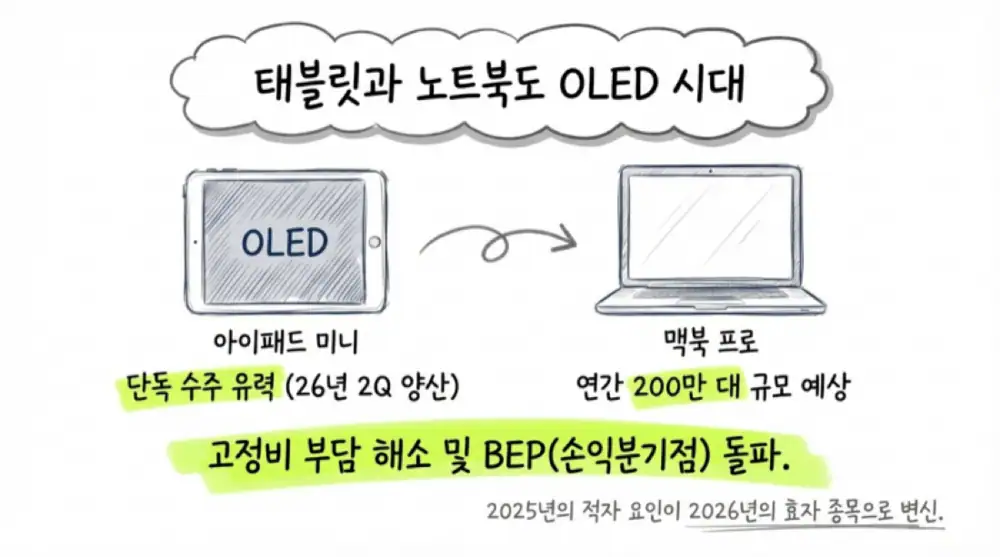

IT OLED substrates

Apple is described as planning to release OLED iPad mini and OLED MacBook Pro models in 2026. Tablet and notebook OLED substrates have much larger area than smartphone substrates, so revenue contribution per device is higher. BH is said to have sole-sourced IT OLED FPCB volume for iPad mini and to begin mass production from late 2Q26.

The source expects 2026 orders of 5 million iPads and 2 million MacBooks to support KRW 59.2 billion in IT OLED-related revenue, allowing the business to pass breakeven and enter an earnings-leverage phase.

Robot wireless charging and BMS FPCB

BH EVS unveiled an autonomous-robot charger at CES 2026. The vertical charging station has a confirmed supply contract with a major Korean company and enters mass production in 1H26; the horizontal model has also been awarded for a next-generation robot to be released the following year, according to the source.

The robot charger has automotive-level reliability testing, more than 5,000 contact durability cycles, and 1kW output, with plans to raise specifications above 1.7kW according to customer requirements. BMS FPCB connects to the automotive trend of replacing heavy copper wire harnesses with thin, light FPCB. BH EVS plans to begin BMS FPCB mass production for major OEMs and new customers from late 2026 and expand applications to ESS. EV wireless charging targets commercialization in 4Q27 and is in vehicle evaluation.

6. Competitive environment: BH and Interflex

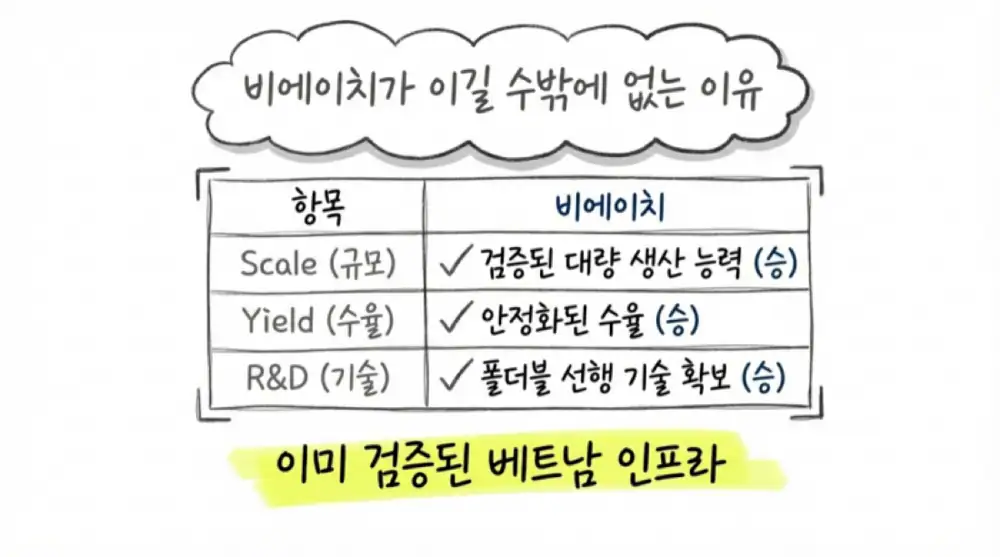

The FPCB industry is a capital-intensive equipment industry and also a technology- and labor-intensive industry requiring fine-pitch control, skilled processes, and quality certification. Becoming a vendor for top-tier customers such as Apple requires proof of strict quality and yield stabilization.

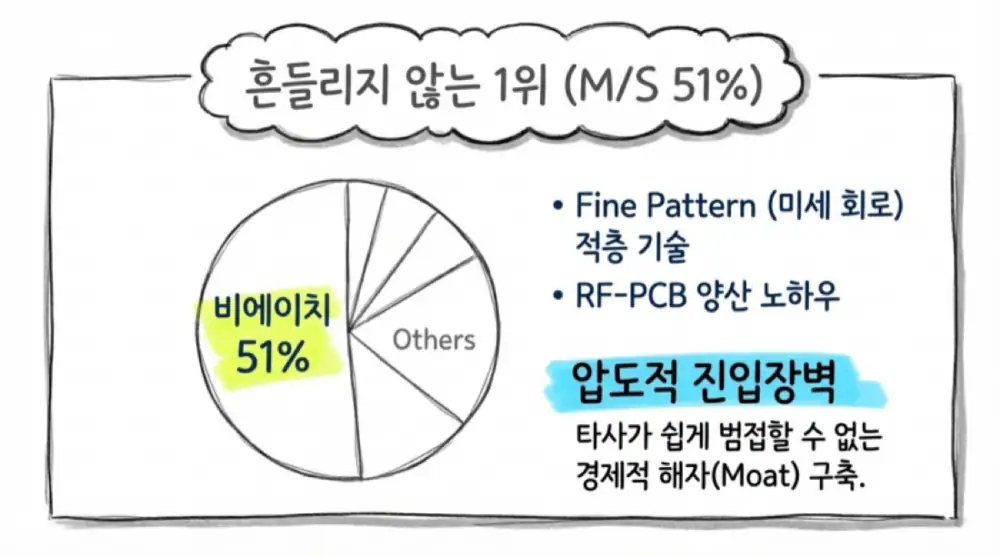

Official fact: The source says Korean FPCB competitors include BH, Interflex, Young Poong Electronics, SI-Flex, and Newflex, with BH holding the No. 1 position at 51% market share. In high-function, high-density build-up and RF PCB, BH also competes with Taiwanese players such as ZDT and Flexium.

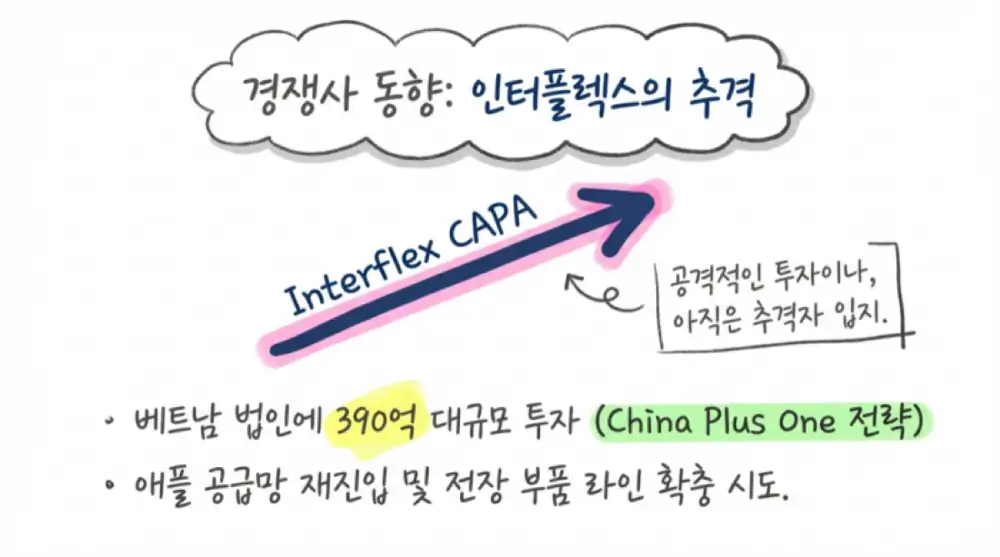

Interflex participated twice, in June and November 2025, in capital increases for parent Korea Circuit's Vietnam entity, KOREA CIRCUIT VINA, investing a total of KRW 39.0 billion and raising its stake to 83.58%. The strategy is to reduce geopolitical risk from the Tianjin, China plant, consolidate Vietnam production under the China Plus One trend, share Korea Circuit's HDI infrastructure, resume Apple component orders, and pre-expand automotive FPCB and ADAS lines.

Interpretation: Competition will intensify, but BH already has a front-end process line at BH Flex VINA and has secured logistics, labor-cost efficiency, and maximum-CAPA operating experience. I believe BH retains a cost and yield-stability advantage even as share competition increases in foldable and automotive markets after 2026.

7. Final take

BH's 4Q25 preliminary results indicate that high-value FPCB and automotive electronics have crossed an earnings threshold. The combined EB, PRS, and treasury-share cancellation strategy was a financial move to prepare for the 2026 mega order cycle while defending existing shareholders from dilution.

In 2026, foldable iPhone, OLED iPad mini and MacBook, robot wireless charging, and BMS FPCB all become major catalysts. The checkpoints I would watch are actual foldable iPhone shipments, IT OLED breakeven, BH EVS expansion with Europe, Tesla, and robot customers, and market-share changes after Interflex's Vietnam expansion.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224190725696

- BH consolidated preliminary operating results fair-disclosure PDF dated 2026.02.09

- [리포트 브리핑]비에이치, 4Q 실적 컨센서스 상회 전망 - 뉴스핌: https://m.newspim.com/news/view/20260128000113

- 비에이치, 2026년 폴더블·OLED 수혜로 매출 2조원 도약 기대 - 글로벌에픽: https://www.globalepic.co.kr/view.php?ud=2025061317460952975ebfd494dd_29

- 비에이치 (090460) 리포트 PDF - AlphaSquare: https://file.alphasquare.co.kr/media/pdfs/company-report/_10072818-090460.pdf

- 비에이치(090460) 리포트 - Bondweb: https://www.bondweb.co.kr/_research/downloadPage.asp?number=887356&gn=1

- 아이폰17 OLED 패널, 韓 디스플레이 점유율 '98%' 압승 - 조선비즈: https://biz.chosun.com/it-science/ict/2025/10/28/G5CFALA3GRA4TFIUHUDF2HCQCA/

- [버핏 리포트]비에이치, 2026년 폴더블 아이폰·IT OLED·갤럭시가 견인 - 메리츠: https://buffettlab.co.kr/news/view.php?idx=51121

- [비에이치] 분기보고서(일반법인) - KRX KIND: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20251114000444

- 신사업 'BMS' 2026년 말 제품 양산, 고객사 공급 확정 - 비에이치: https://www.bhflex.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=48&category=&findType=&findWord=&sort1=&sort2=&it_id=&shop_flag=&mobile_flag=&page=2

- [CES 2026]BH EVS, '로봇 충전기' 상반기 내놓는다 - BHE: https://www.bhe.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=58&category=&findType=&findWord=&sort1=&sort2=&page=&mobile_flag=

- [CES 2026]BH EVS, '로봇 충전기' 상반기 내놓는다 - BHFlex: https://www.bhflex.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=58&category=&findType=&findWord=&sort1=&sort2=&page=2&mobile_flag=

- 신사업 'BMS' 2026년 말 제품 양산, 고객사 공급 확정 - BHE: https://www.bhe.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=48&category=&findType=&findWord=&sort1=&sort2=&it_id=&shop_flag=&mobile_flag=&page=2

- 비에이치 EVS “로봇 충전 시장 진출…차세대 로봇도 수주” - BHE page 2: https://www.bhe.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=59&category=&findType=&findWord=&sort1=&sort2=&page=2&mobile_flag=

- 비에이치 EVS “로봇 충전 시장 진출…차세대 로봇도 수주” - BHE: https://www.bhe.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=59&category=&findType=&findWord=&sort1=&sort2=&page=&mobile_flag=

- 비에이치 EVS “로봇 충전 시장 진출…차세대 로봇도 수주” - Daum: https://v.daum.net/v/0tSsz5YCr0

- 비에이치 EVS “로봇 충전 시장 진출…차세대 로봇도 수주” - BHFlex page 1: https://www.bhflex.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=59&category=&findType=&findWord=&sort1=&sort2=&page=1&mobile_flag=

- [CES 2026]BH EVS, '로봇 충전기' 상반기 내놓는다 - BHE page 1: https://www.bhe.co.kr/bbs/board.php?tbl=bbs54&mode=VIEW&num=58&category=&findType=&findWord=&sort1=&sort2=&it_id=&shop_flag=&mobile_flag=&page=1

- 비에이치, 부진한 실적 터널의 끝, 2026년 아이폰 혁신에 베팅 - 네이버 프리미엄콘텐츠: https://contents.premium.naver.com/crioppstock/stockplus/contents/250815080201854pf

- 비에이치 핵심 기업분석 - 2026년 상반기 - 자소설닷컴: https://jasoseol.com/companies/6215/insights

- 폴더블폰 경쟁에 FPCB 재조명 - BHFlex: http://www.bhflex.com/bbs/board.php?tbl=bbs54&mode=VIEW&num=53&category=&findType=&findWord=&sort1=&sort2=&it_id=&shop_flag=&mobile_flag=&page=1

- 비에이치, 테슬라 고객사로 확보 - 디일렉: https://www.thelec.kr/news/articleView.html?idxno=31116

- 비에이치, 2026년 폴더블·OLED 수혜로 매출 2조원 도약 기대 - BHFlex: http://www.bhflex.com/bbs/board.php?tbl=bbs54&mode=VIEW&num=54&category=&findType=&findWord=&sort1=&sort2=&page=1&mobile_flag=

- [특징주] 비에이치, 폴더블 아이폰 FPCB 사실상 독점 전망 - 와이드경제: https://www.widedaily.com/news/articleView.html?idxno=273084

- 분석가, OLED 장착 맥북 프로 2026년 이후 출시 전망 - 케이벤치: https://kbench.com/?q=node/242430

- 애플, 2026년에 20인치 폴더블 및 OLED 맥북 잇달아 출시한다 - AVING: https://kr.aving.net/news/articleView.html?idxno=1790864

- 인터플렉스 실적, 주주, 고객사 분석 - Google Drive: https://drive.google.com/open?id=1h-lnKYQ1VH2--0avvOFKoPPlOfD8D21Mr7pOg7VE9_8