DEEP RESEARCH · DKT / SMT MODULES

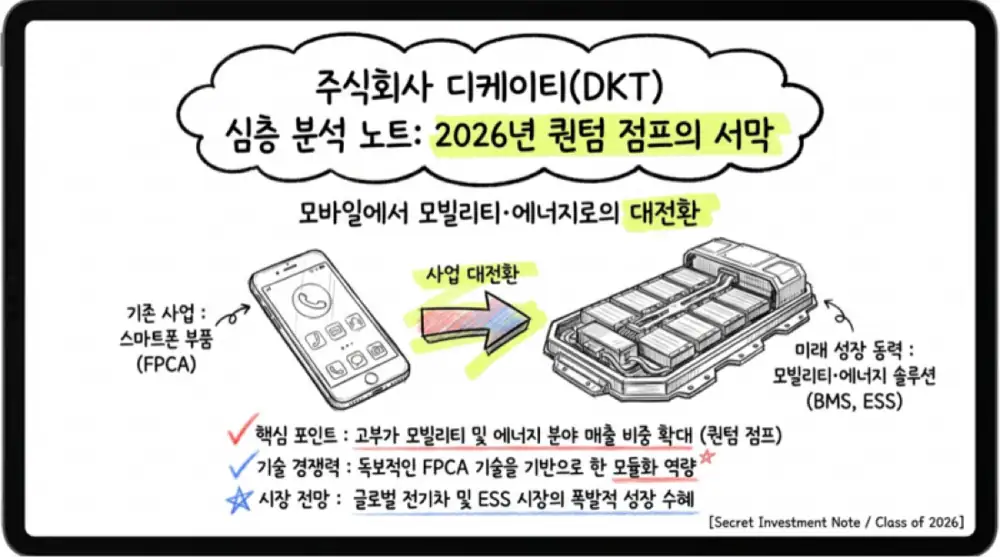

DKT: 4Q25 OP Up 102.5% and the 2026 Mobility & Energy Quantum Jump

A mobile-captive No. 1 in SMT modules pivots to Tesla, ESS BMS and North-American nearshoring

0. Bottom line first

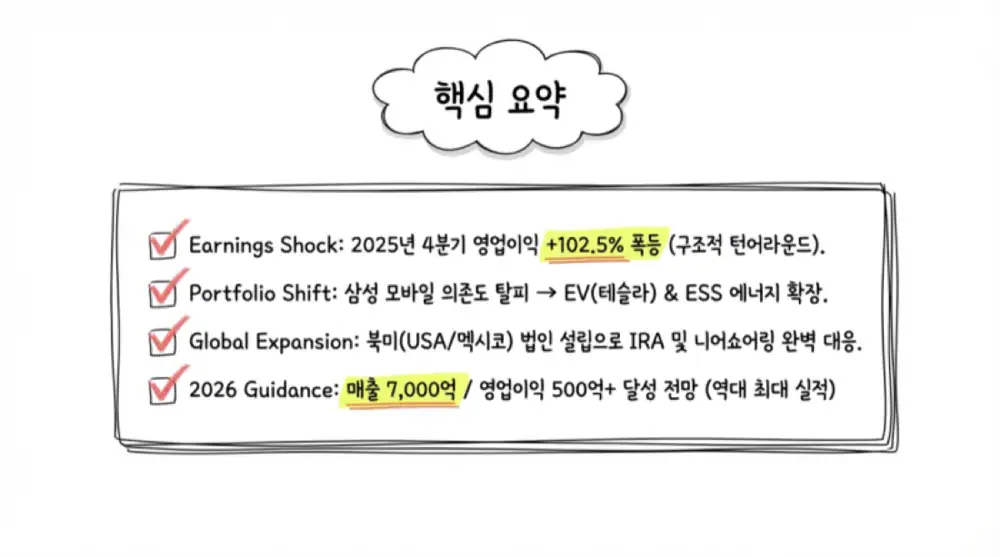

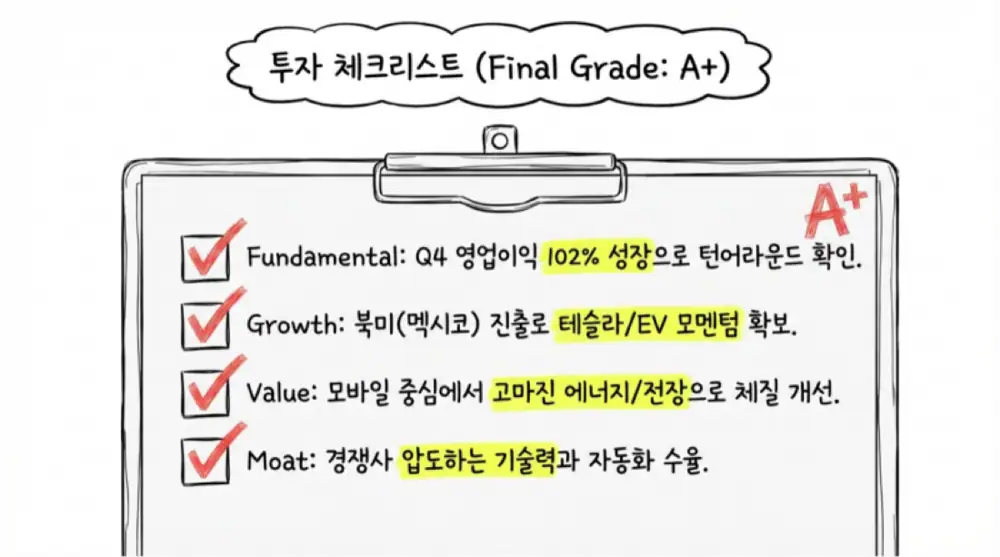

DKT's 4Q25 results are not just a strong quarter — they mark a structural inflection. 4Q revenue KRW 114.8bn (+8.5% QoQ, +16.9% YoY) and operating profit KRW 5.65bn (+102.5% QoQ) showcased the explosive operating leverage of an SMT model. 2026 should be the quantum-jump year as S-PCM, P-LBM, ESS BMS and Tesla orders ignite together, putting KRW 600–700bn revenue and KRW 50–58bn operating profit in sight.

1. 4Q25 preliminary results deep dive

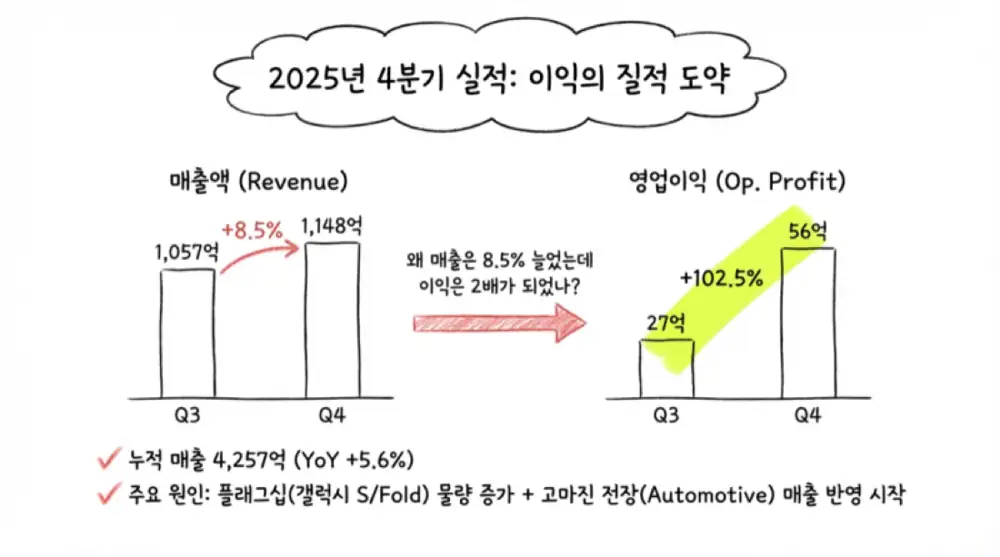

DKT's 4Q25 consolidated preliminary results signal that the company's earnings structure has reached a fundamentally upgraded inflection point. According to the disclosure, 4Q revenue was KRW 114.807bn, up 8.5% from 3Q (KRW 105.771bn) and 16.9% YoY from 4Q24 (KRW 98.183bn).

The strongest signal is operating profit. 4Q OP came in at KRW 5.649bn, up +102.5% from 3Q's KRW 2.789bn. Full-year 2025 cumulative revenue was KRW 425.776bn (+5.6%), but cumulative OP was KRW 21.156bn (-8.4%).

+102.5% QoQ

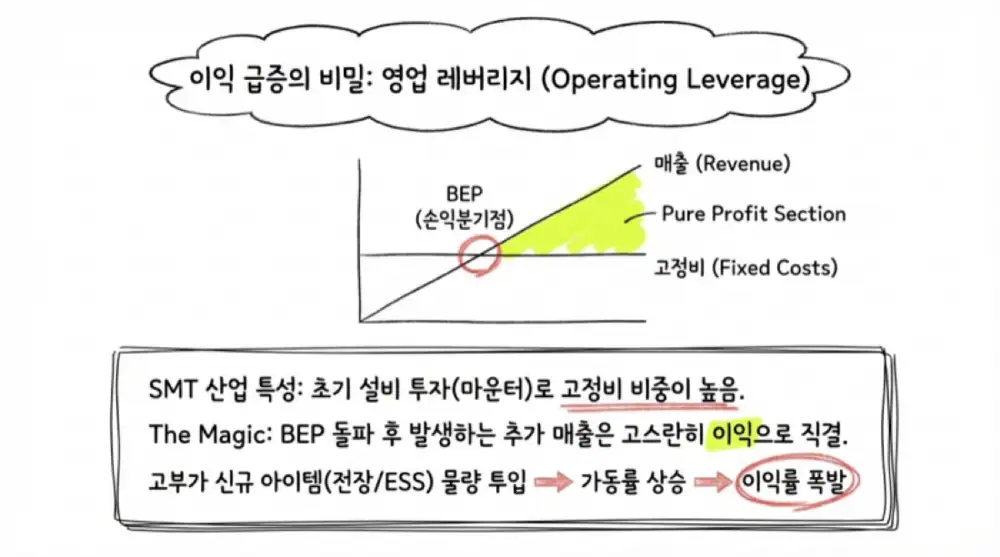

KRW 5.65bn — once an SMT business clears breakeven, incremental revenue flows almost entirely to OP via operating leverage.

On-device AI spec-up

Galaxy S series rising compute and heat raise FPCA circuit integration and ASP at the same time.

P-LBM & ESS BMS land

From 2H25, automotive auxiliary battery modules and ESS BMS volumes hit the books, expanding high-margin mix.

| Financial (KRW mn) | 4Q24 | 3Q25 | 4Q25 | QoQ | YoY |

|---|---|---|---|---|---|

| Revenue | 98,183 | 105,771 | 114,807 | +8.5% | +16.9% |

| Operating profit | - | 2,789 | 5,649 | +102.5% | - |

| FY cumulative revenue | 403,350 | - | 425,776 | - | +5.6% |

| FY cumulative OP | 23,086 | - | 21,156 | - | -8.4% |

Interpretation: The -8.4% full-year OP reflects 1H weakness, but a 102.5% single-quarter rebound proves that high-value-added new items poured into 4Q, converting incremental revenue directly into OP. Even amid the macro slowdown, portfolio diversification has built fundamental resilience.

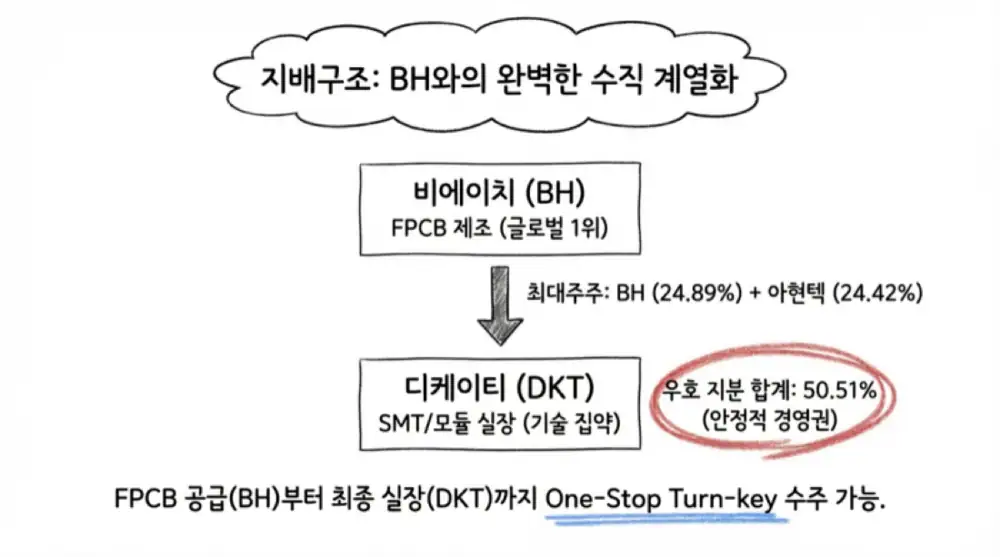

2. Governance and vertical integration along the value chain

To understand DKT's medium-term competitiveness, look at the bond with its largest shareholder and parent BH Co., Ltd. As of end-3Q25, BH owns 4,978,000 shares (24.89%); the second-largest holder Ahyun Tech owns 4,885,000 shares (24.42%). Counting related parties, the friendly stake reaches 50.51% (10,102,780 shares) out of 20,001,230 outstanding — governance is firmly locked.

The March 30, 2018 change of control from Ahyun Tech to BH was not a mere capital reshuffle; it completed vertical integration of the FPCB value chain: BH (FPCB) → DKT (SMT-mounted MLCC, DDI, touch ICs) → finished FPCA module — a one-stop structure.

| Shareholder | Shares | Stake (%) | Note |

|---|---|---|---|

| BH Co., Ltd. (largest) | 4,978,000 | 24.89 | Parent, FPCB supply base |

| Ahyun Tech | 4,885,000 | 24.42 | Major affiliate |

| Lee Kyung-hwan (related party) | 239,780 | 1.20 | - |

| Others | 9,898,450 | 49.49 | Retail and institutions |

| Total | 20,001,230 | 100.00 | End-3Q25 |

Parent lock-in effects: ① FPCB supply stability, ② shared design-to-mount data lifts yield/quality consistency, ③ Turn-key (board + module) proposals to Samsung Display and set-makers, sharply boosting negotiating power. Joint investment and shared sales networks with the parent are also a strong tailwind in the current expansion into automotive and battery.

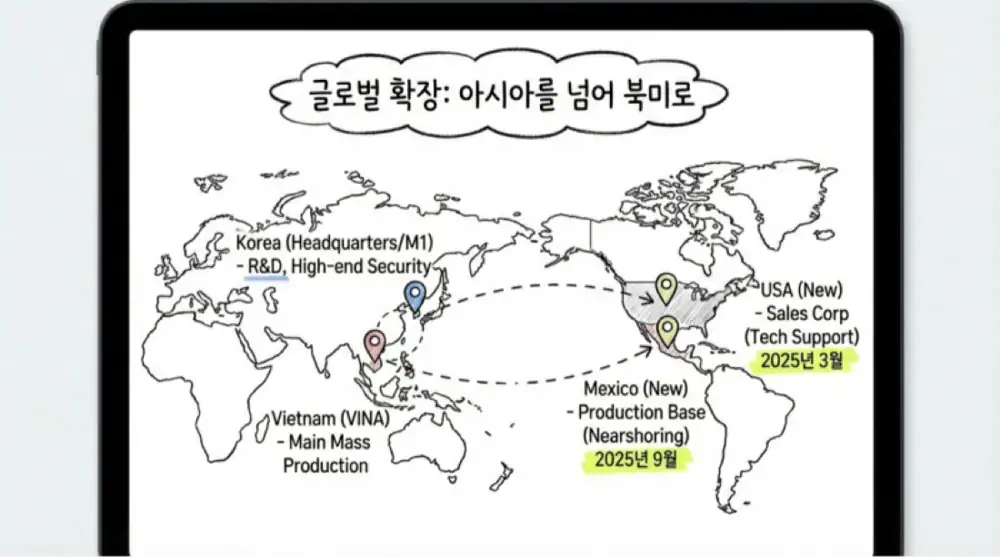

3. Supply-chain restructuring: Vietnam – US – Mexico triad

During 2025, DKT set up two new overseas entities, expanding from a Vietnam-only base to a three-axis structure spanning the Americas.

| Subsidiary | Location | Established / acquired | Control basis | Strategic role |

|---|---|---|---|---|

| DKT VINA CO., LTD. | Vinh Phuc, Vietnam | Sep 2012 (acquired) | 100% voting | Main production base, mobile FPCA SMT mass production |

| DKT USA INC. | USA | Mar 3, 2025 | 100% voting | North-American sales/tech support hub for EV & IT customers |

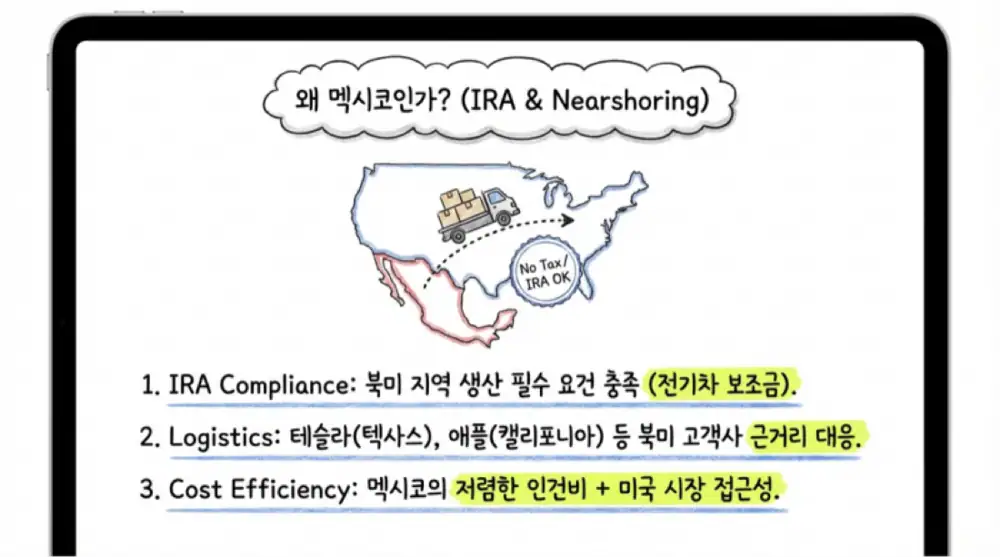

| DKT TECH MEXICO, S.A. DE C.V. | Mexico | Sep 24, 2025 | Majority voting | IRA-compliant nearshoring base, direct OEM (e.g., Tesla) supply |

Strategic meaning: ① Real-time technical support and delivery for Tesla and other North-American OEM/battery customers, ② proactive alignment with USMCA/IRA-driven supply-chain re-shoring, ③ lower labor cost in Mexico (e.g., Nuevo León) close to the US border, minimizing logistics. If Apple and other US set-makers accelerate OLED adoption in IT devices, DKT can supply directly to North-American customers without going through Korean panel makers.

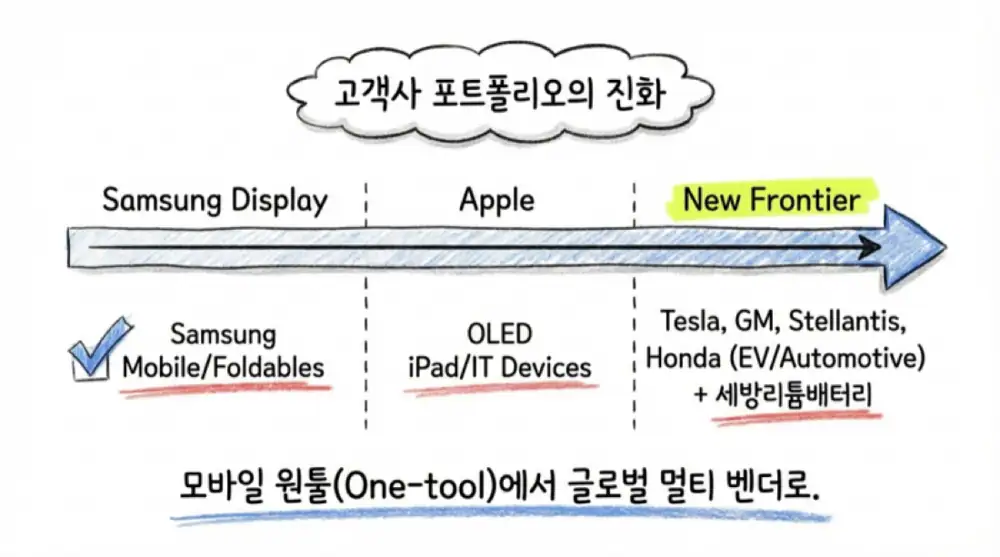

4. Front-end customer changes: from mobile captive to Tesla momentum

4.1. Smartphone & IT devices: an evolving captive market

Core customers are Samsung Display (SDC) and Samsung MX. DKT is the top-tier vendor with near-monopoly supply of FPCAs optimized for the high-difficulty Y-OCTA (Youm On-Cell Touch AMOLED) panel. Y-OCTA patterns the touch sensor directly on top of the OLED encapsulation layer; DKT supplies nearly all FPCAs that integrate main display drive and TSP control for Galaxy S and Z Fold/Flip series.

Official fact: In 2024 a North-American set-maker (strongly presumed to be Apple) first adopted OLED in its premium tablet lineup; DKT secured a new opportunity to supply large-area OLED FPCAs via Samsung Display. IT OLED FPCAs are much larger and contain many more chips than mobile, so ASP is structurally higher.

4.2. Auto electronics entry and global EV leap

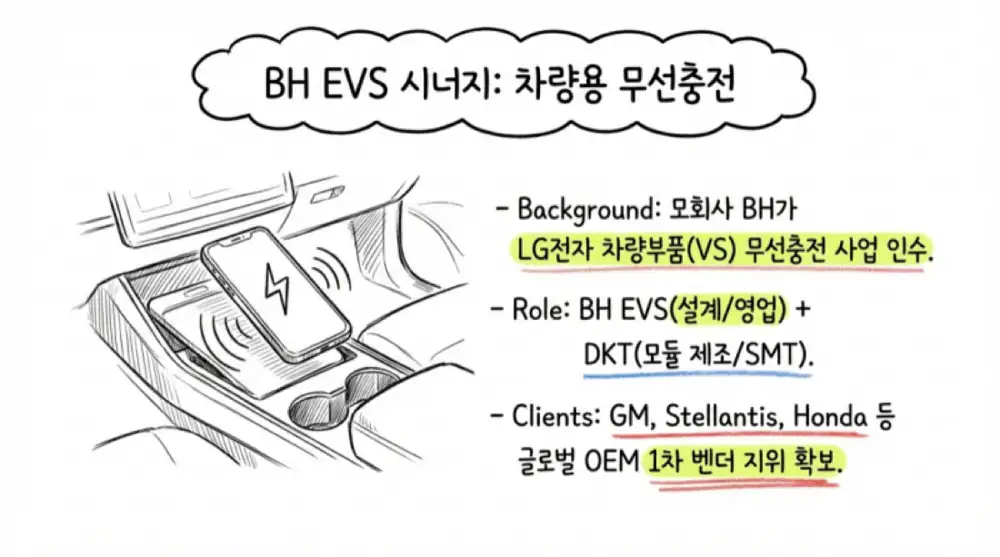

Parent BH acquired LG Electronics' Vehicle Component (VS) wireless mobile-device charging business in October 2022, forming the JV BH EVS (BH 59% / DKT 41%). DKT handles SMT contract manufacturing and module assembly for WMDCs (Wireless Mobile Device Chargers).

- Customers: Through this indirect entry, DKT joined the vendor lists of GM, Stellantis, Honda and other global OEMs faster than usual. Automotive wireless charging revenue grew from KRW 6.1bn (2023) to about KRW 48.0bn (2024).

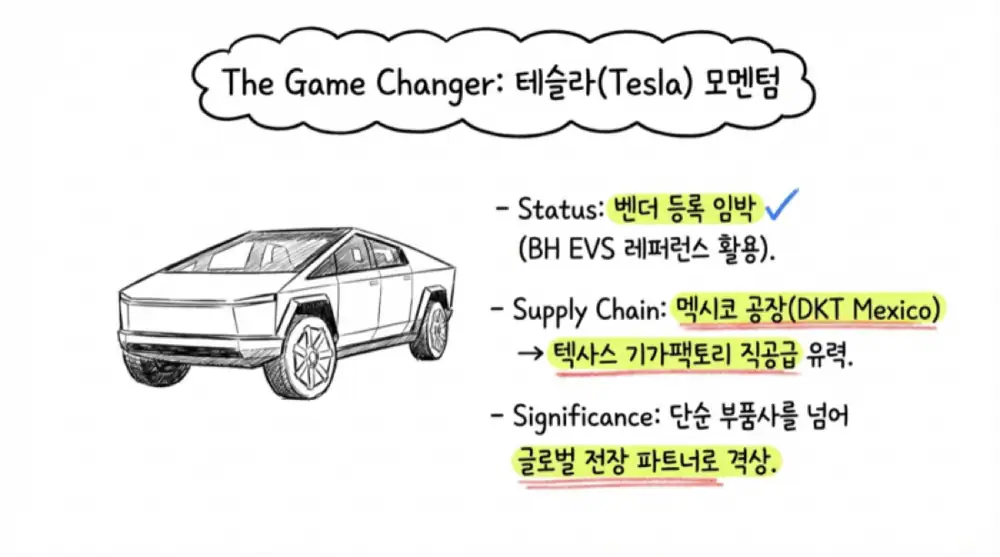

- Tesla momentum: DKT has been going through Tesla's strict supplier qualification since early 2024. The industry treats vendor approval as a near certainty barring surprises. If approved, the Mexico entity will serve as the core logistics hub for Tesla's Texas Gigafactory and future Latin-American plants.

- ESS battery: Sebang Lithium Battery joined as a new customer, accounting for 27.19% of revenue as a single customer. EV-related cumulative backlog reaches about KRW 3tn.

5. 2026 new items in the pipeline

DKT has positioned 2026 as a quantum-jump year, with the commercialization of new product groups in front.

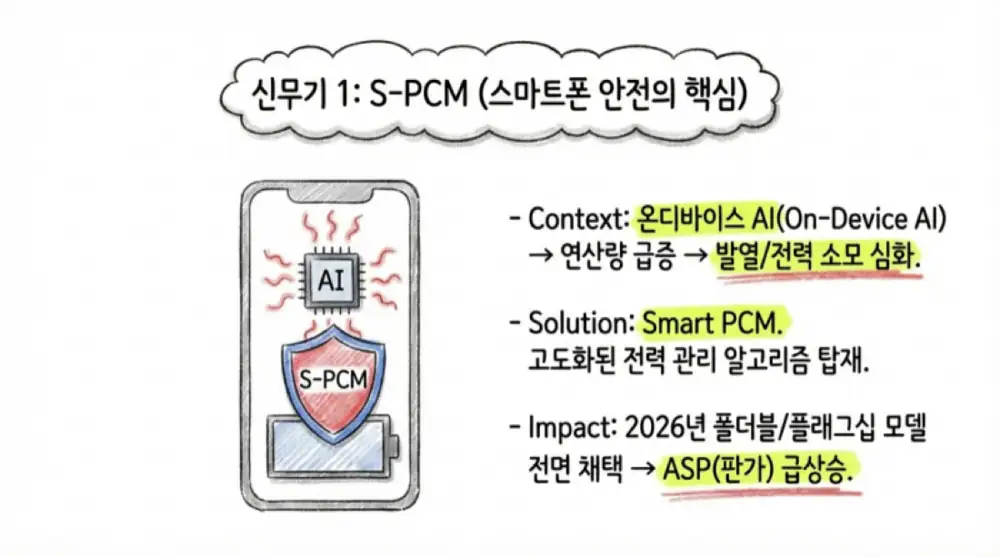

5.1. S-PCM (Smart Protection Circuit Module)

As on-device AI smartphone compute and heat surge, legacy PCM's limits are exposed. DKT completed in-house development of S-PCM, an upgraded module with advanced power management algorithms, and is ready for mass production. It will be rolled out first to next-generation foldable and flagship models in 2026. Initial mass adoption in foldables drives a quantum jump in ASP per part.

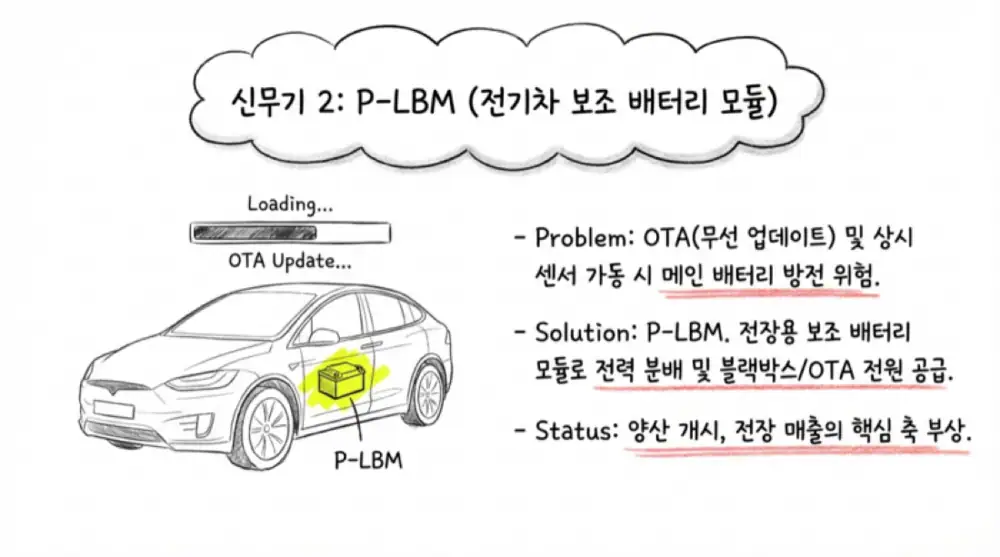

5.2. P-LBM (Automotive Auxiliary Battery Module)

As OTA stays continuously active and sensors run 24/7, main battery drain becomes severe. DKT developed and started mass production of P-LBM, a high-value module that communicates with the vehicle's ECU and intelligently distributes power.

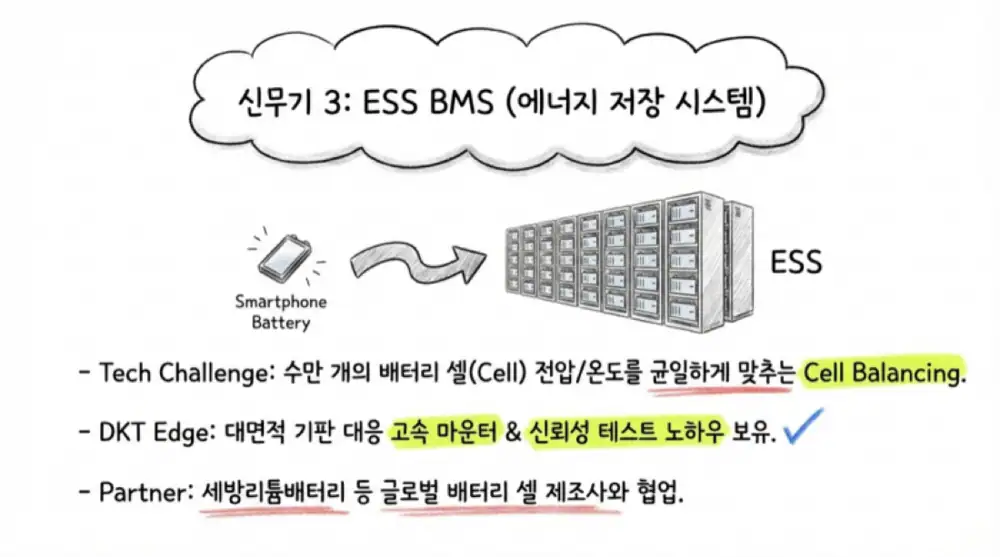

5.3. ESS BMS (Battery Management System)

Large ESS systems are hundreds of times bigger than automotive packs and consist of tens of thousands of cells, where cell balancing is critical for system life. DKT preemptively built high-speed chip mounters and reliability test environments for large boards, and has been jointly developing ESS BMS modules with global top-tier battery makers. This is the most explosive 2026 order pipeline item.

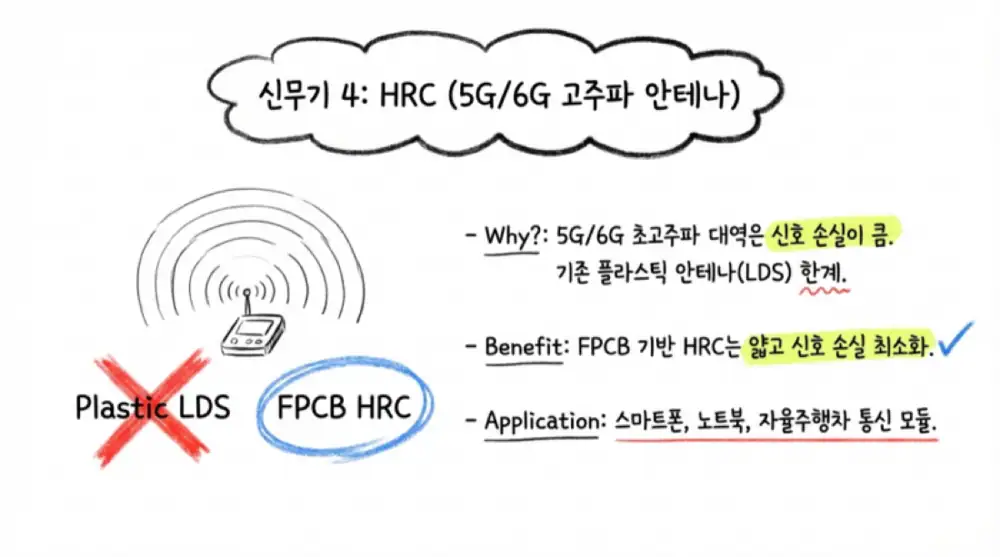

5.4. 5G/6G antenna HRC

Legacy LDS (Laser Direct Structuring) antennas show steep RF loss at high frequencies. DKT entered the HRC (High Retention Connector / High Frequency RF Cable) business, patterning antennas directly on FPCB surfaces and mounting chips to minimize insertion/return loss. Optimized for MIMO and expandable beyond smartphones into laptops, tablets, autonomous-driving communication modules — anywhere RF connectivity matters.

6. Market competition and a decisive tech moat

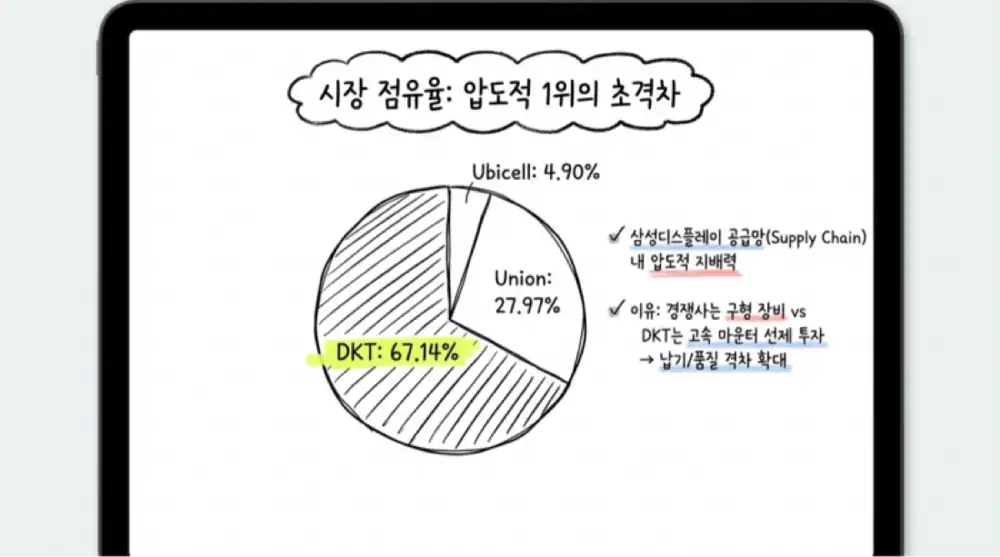

6.1. Dominant market-share gap

Within Samsung Display's smartphone FPCA value chain, DKT is No. 1, Union No. 2, and Ubicell No. 3 — a tight oligopoly. Based on Vietnam subsidiary (DKT VINA, UNION VINA, U.I.T. Vietnam) revenue, estimated 2024 shares:

| 2024 | DKT | Union | Ubicell | Total |

|---|---|---|---|---|

| Estimated revenue | KRW 403.35bn | KRW 168.03bn | KRW 29.411bn | - |

| Market share | 67.14% | 27.97% | 4.90% | 100.00% |

DKT's share moved from 57.95% (2022) to 50.72% (2023) to 67.14% (2024), opening an irreversible gap. The key is large-scale adoption of high-speed chip mounters, which shortened mounting cycle time and gave DKT decisive lead-time advantage.

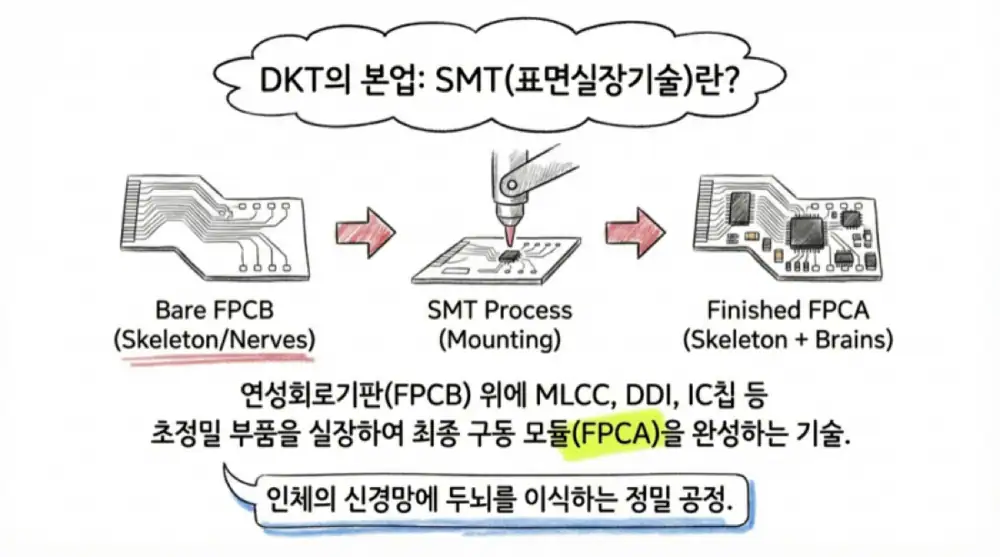

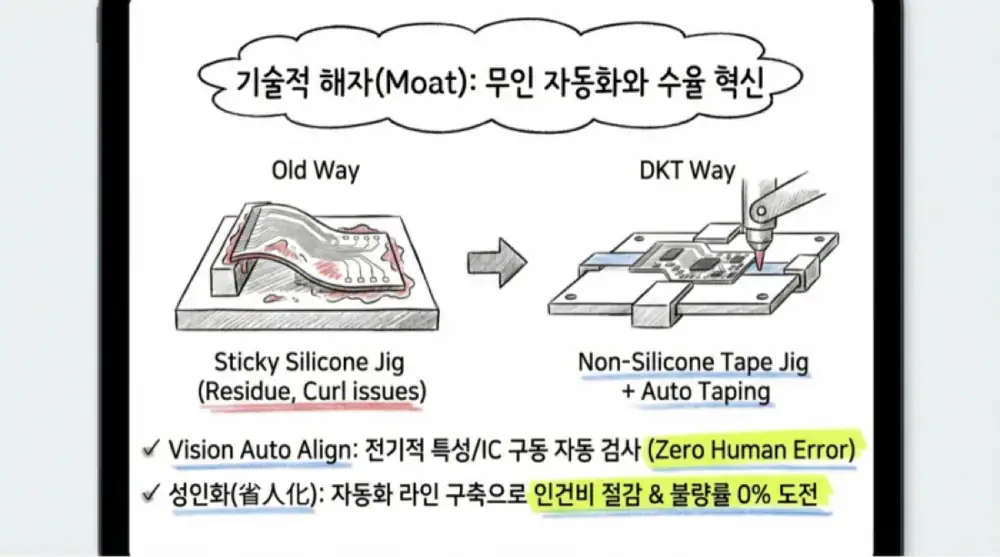

6.2. Yield- and cost-driven automation moat

In contract manufacturing, OP margin is decided by yield. DKT built a giant moat that competitors can't match with capital alone:

- Non-Silicone Tape Jig: Fixes boards without silicone, eliminating residue contamination and curl; uniform SPI solder volume and minimal print shift.

- Vision-recognition TAPE attach line (industry first): Replaces ~16 operators per 2,000K/month production (省人化), cuts handling defects by 50%+.

- Vision auto-align + ET auto inspector + FPCA appearance inspector + CO2 cleaner: Human error effectively eliminated, lot-pass yield up sharply.

7. Production utilization (CAPA) and earnings at full run

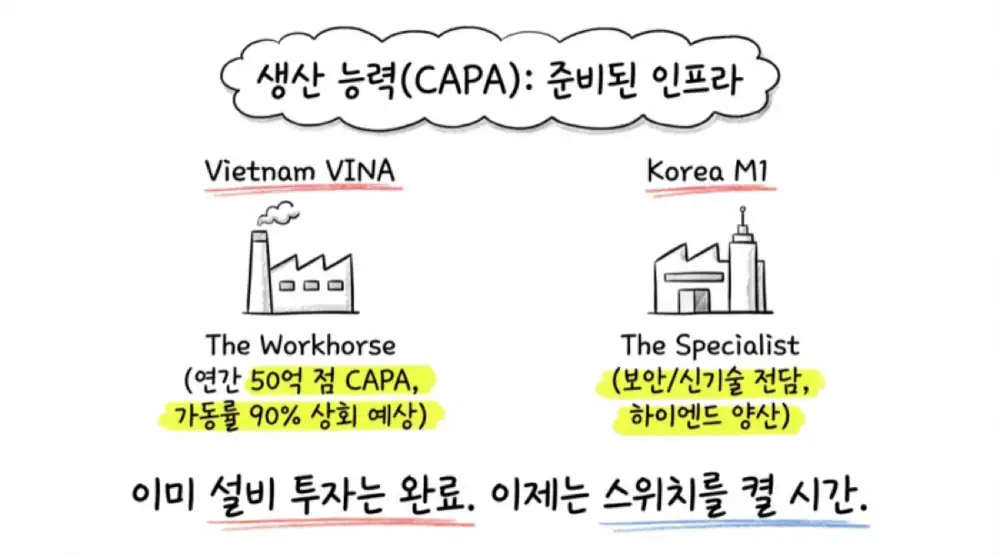

7.1. Vietnam and Korea infrastructure

DKT VINA (Vinh Phuc, Vietnam): 4 high-speed and 91 mid/low-speed mounters (95 total). Three-shift full operation, 26 days/month × 20 hr/day, 6,240 hr/year. 3Q25 total possible production points (CAPA): about 5.01946 billion points, actual: 3.3585 billion, cumulative utilization 66.91% (vs. 69.73% YoY). Given seasonality, 4Q end utilization likely rebounded to 85%+.

Korea (DKT M-One plant): Capacity expanded from 4Q24, mass production started. 5 ultra-high-speed mounters processing 68 points/cycle, 10 hr/day × 2,640 hr/year, total CAPA 175.5 million points. 3Q25 utilization 28.35% (49.76 million points) — still warming up — but if S-PCM, North-American EV parts and Tesla initial volumes are concentrated there, 2026 utilization should climb steeply.

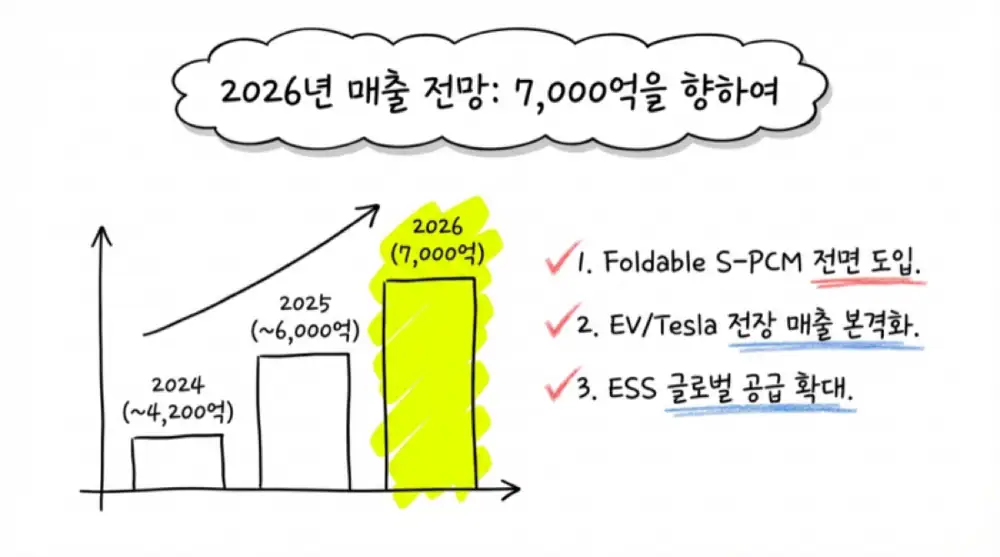

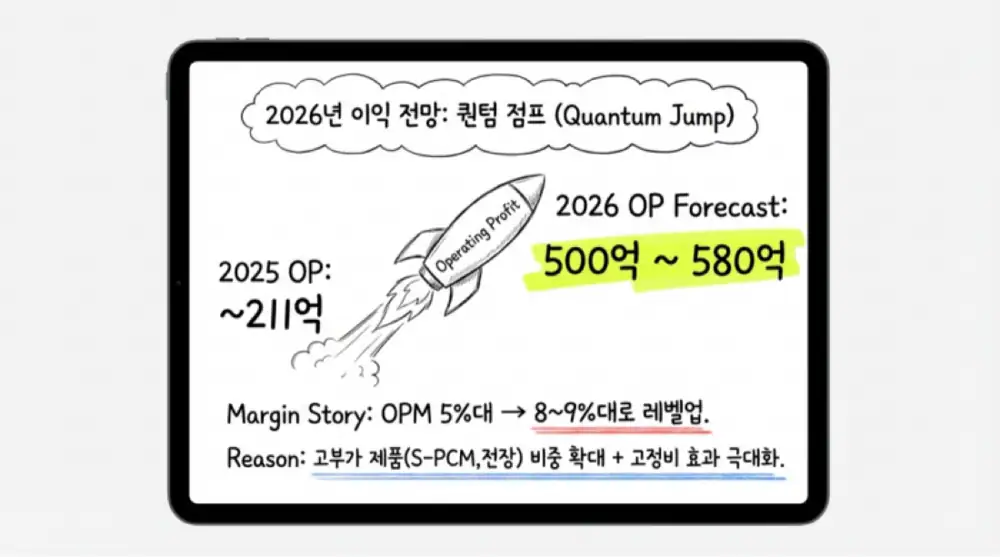

7.2. 2026 full-CAPA earnings scenario

Brokerage consensus suggests 2026 revenue of KRW 600–700bn (all-time high), driven by ① rising Samsung foldable shipments, ② full adoption of S-PCM and other high-value mobile items, ③ global supply ramp of P-LBM and large-scale ESS BMS.

KRW 600–700bn

Mobile + auto + ESS growing together.

7.5–9.0%

Up from 5.5–6.1% (2024–25) on high-value mix + fixed-cost dilution.

KRW 50–58bn

Midpoint KRW 650bn × OPM 8.5% — +130%+ vs. 2025 preliminary KRW 21.1bn.

This is the data that proves the SMT model's explosive operating leverage will finally bloom in 2026 and feed enterprise value.

8. Conclusion

DKT is passing a structural inflection — from a contract assembler of smartphone display parts into a global player leading mobility and clean-energy control modules.

- Qualitative fundamentals leap: The 102.5% 4Q25 OP surge isn't one-off; it combines new-item ramp with rising SMT utilization.

- Strategic Americas quantum jump: The USA and Mexico entities counter IRA-style protectionism and open a direct Tesla supply route, removing geopolitical risk → valuation re-rating catalyst.

- Portfolio innovation + order visibility: S-PCM lifts mobile ASP; a roughly KRW 3tn EV/ESS backlog makes 2026 revenue of KRW 600–700bn plausible.

- Automation-driven margin maximization: Dominant 67%+ FPCA share + Non-Silicone Tape Jig and unmanned inspection underpin a margin spread that supports KRW 50bn+ OP at full CAPA.

Anchored by a steady mobile-captive cash cow and now grafted with EV battery control (BMS, WMDC) and high-frequency communication (HRC), DKT enters 2026 — a historic quantum-jump year for enterprise value.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224190725099

- DKT preliminary consolidated operating results disclosure (Feb 12, 2026), DART/FSS filings

- DKT 4Q again 'good' — diversification did it (DKT official board): https://dkttech.co.kr/bbs/board.php?tbl=bbs43&mode=VIEW&num=12&category=&findType=&findWord=&sort1=&sort2=&it_id=&shop_flag=&mobile_flag=&page=1

- Brokerage report 2025.02.18: https://files-scs.pstatic.net/2025/02/18/C3yQcC3wzD/250218(%ED%99%94)%20%EC%A6%9D%EA%B6%8C%EC%82%AC%EB%A6%AC%ED%8F%AC%ED%8A%B8.pdf

- DKT expected to register as Tesla partner vendor - Global Epic: https://www.globalepic.co.kr/view.php?ud=202406281027331197abe7dc9896_29

- DKT 2026 revenue to reach KRW 600–700bn — Naver Premium Content: https://contents.premium.naver.com/rvs/tbw/contents/250112172444096od

- DKT investment analysis 2026.02.08 - Judal: https://www.judal.co.kr/?view=stockAI&shareToken=G8luG8giCKFKbRc8

- DKT 4Q OP KRW 5.6bn (+102%) - Data Tooza: https://www.datatooza.com/article/2026021209595132852ef3fddee_80

- DKT investment analysis 2026.02.17 - Judal: https://www.judal.co.kr/?view=stockAI&shareToken=0sTttDvLv62FO4NA