DEEP RESEARCH · INTERFLEX

Interflex: Q4 2025 Earnings Surge and Vietnam Production Realignment

An earnings report connecting the FPCB rebound, Youngpoong governance changes, and automotive/Apple-related optionality.

0. Bottom line first

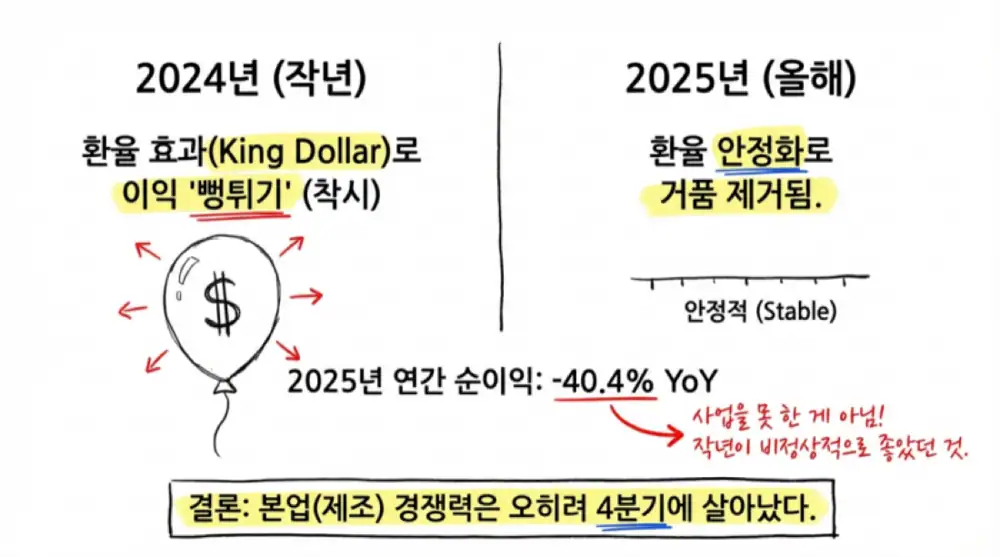

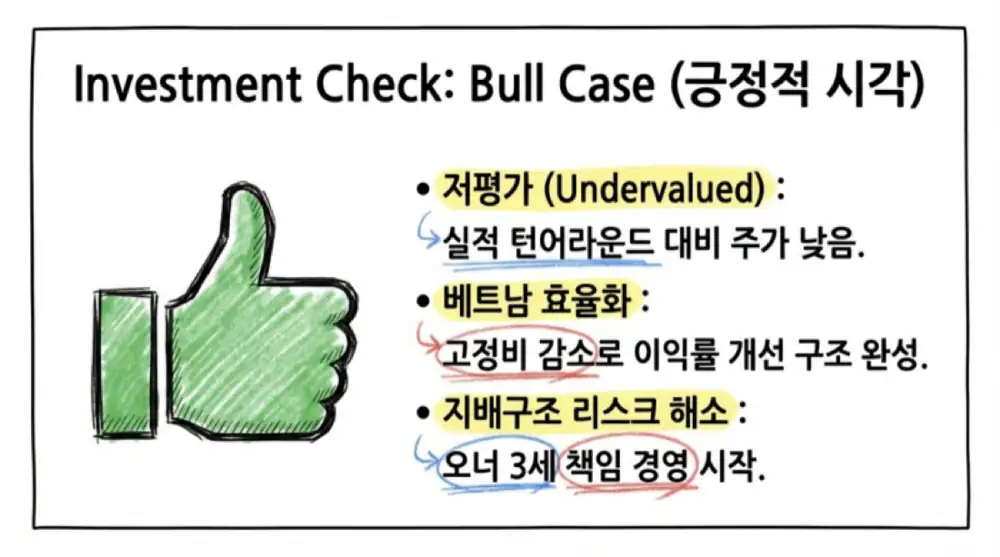

My read is that the annual 2025 numbers look weaker on the surface, but the Q4 core business clearly rebounded. The source interprets the move as a structural shift driven by high-end digitizer supply, Vietnam production consolidation, and stabilized process yields.

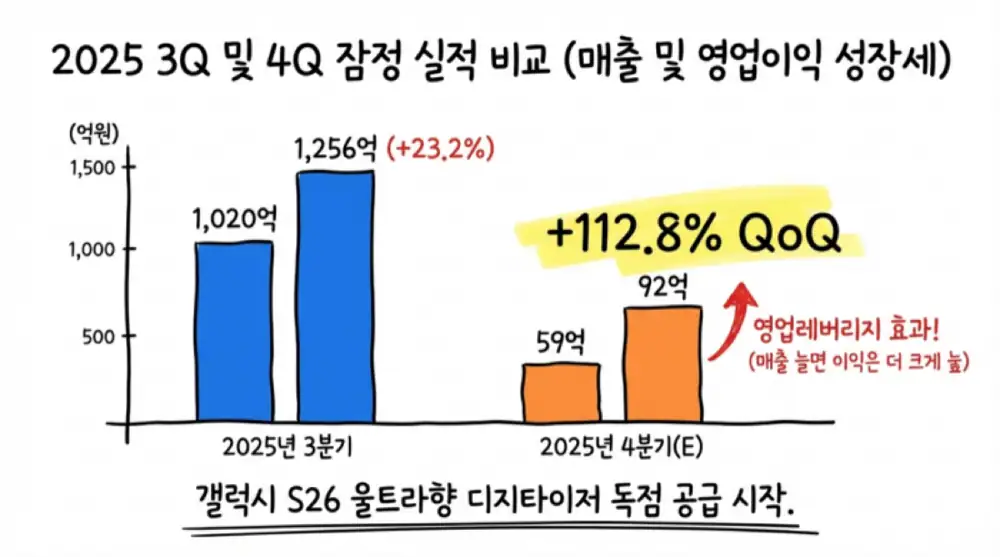

Official fact: The source says Q3 2025 revenue of KRW 102.0 billion and operating profit of KRW 5.9 billion beat earlier estimates of KRW 91.3 billion and KRW 2.0 billion. It presents Q4 2025 revenue of KRW 125.6 billion, up 23.2% QoQ, and operating profit of KRW 9.2 billion, up 57.7% QoQ.

Interpretation: The annual net-profit decline should be read as a base effect from the disappearance of 2024 FX gains, while the real operating signal is the Q4 profit leverage.

1. Source images and earnings snapshot

The source includes many images related to earnings, governance, and production-footprint changes. All source images are preserved below.

| Item | 2024 | 2025 preliminary | Change |

|---|---|---|---|

| Revenue | KRW 497.5 billion | KRW 468.0 billion | -5.9% |

| Operating profit | KRW 34.4 billion | KRW 28.6 billion | -16.7% |

| Pre-tax profit | KRW 50.8 billion | KRW 33.5 billion | -34.0% |

| Net income | KRW 55.1 billion | KRW 32.8 billion | -40.4% |

Official fact: The company’s stated reason for the profit-structure change is lower foreign-exchange gains due to reduced FX volatility versus the prior year. The source says exports were KRW 295.5 billion out of KRW 319.5 billion in 9M 2025 revenue, or about 92.6%.

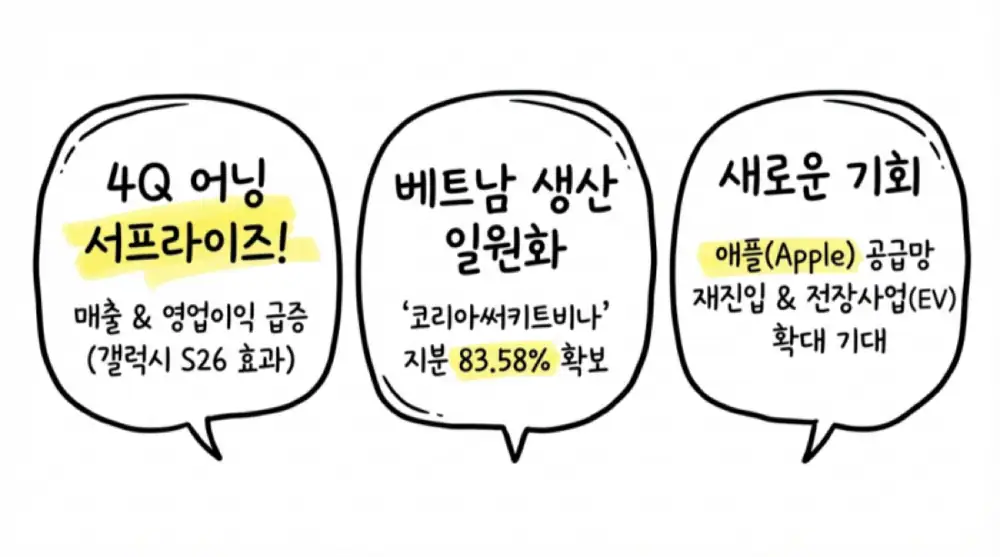

2. Three drivers of the Q4 surge

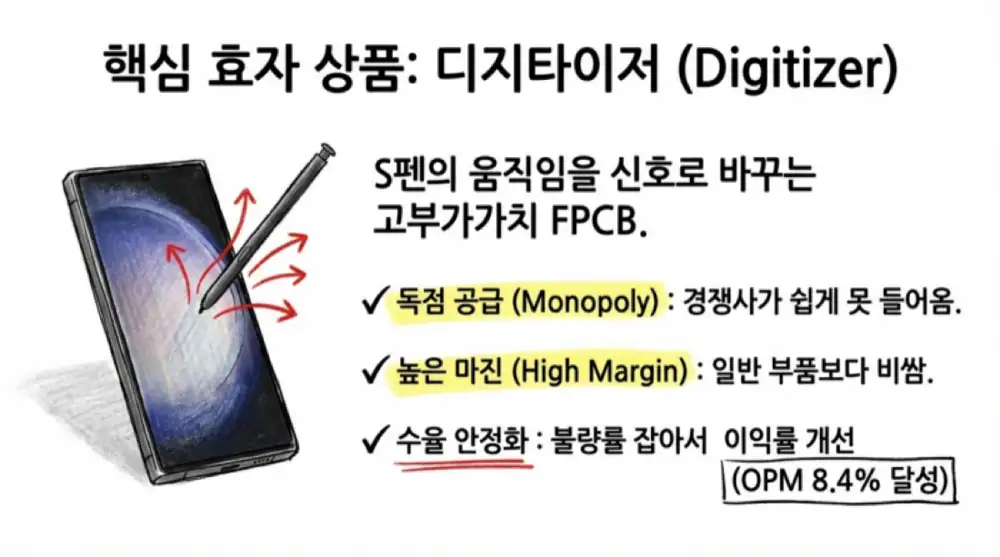

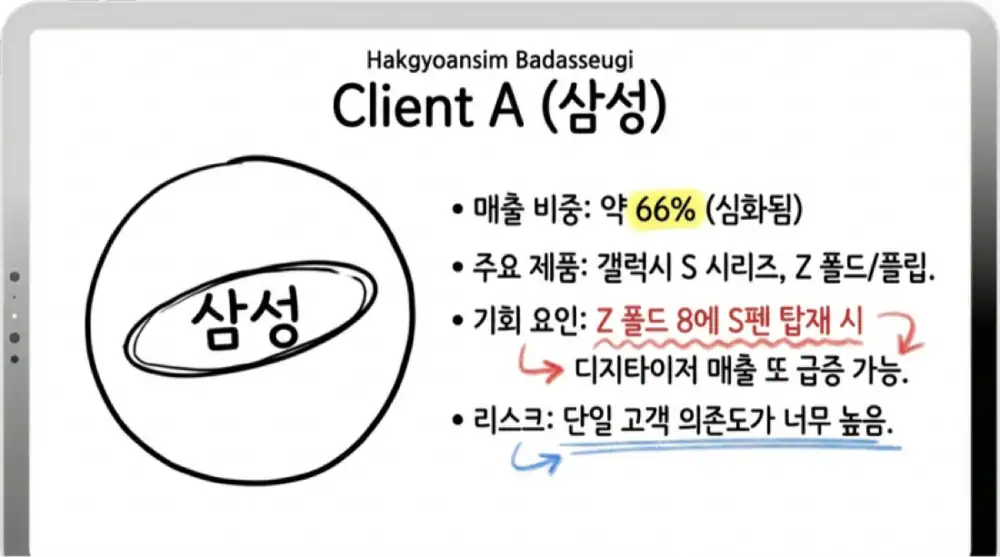

Galaxy S26 Ultra digitizer

The source identifies near-exclusive supply of S Pen digitizers for Samsung’s highest-end line as the main Q4 driver. Digitizers require double-sided FPCB, fine circuit patterning, and EMI shielding, supporting higher ASP and margin than commodity FPCB.

Higher utilization

Orders for display FPCB and high-spec R/F boards for camera modules rose alongside digitizers, turning 23.2% revenue growth into 57.7% operating-profit growth.

Yield stabilization

After the 2017 quality issue with a global customer, the company improved processes and quality systems. Vietnam-centered efficiency, I-Soft, and SAP stabilization are described as supports for lower manufacturing cost.

The source highlights I-Soft, SAP with 15um pitch fine-pattern capability, and Ag Nanowire adoption. It also treats a possible S Pen return in the Galaxy Z Fold 8 in H2 2026 as a medium-term option.

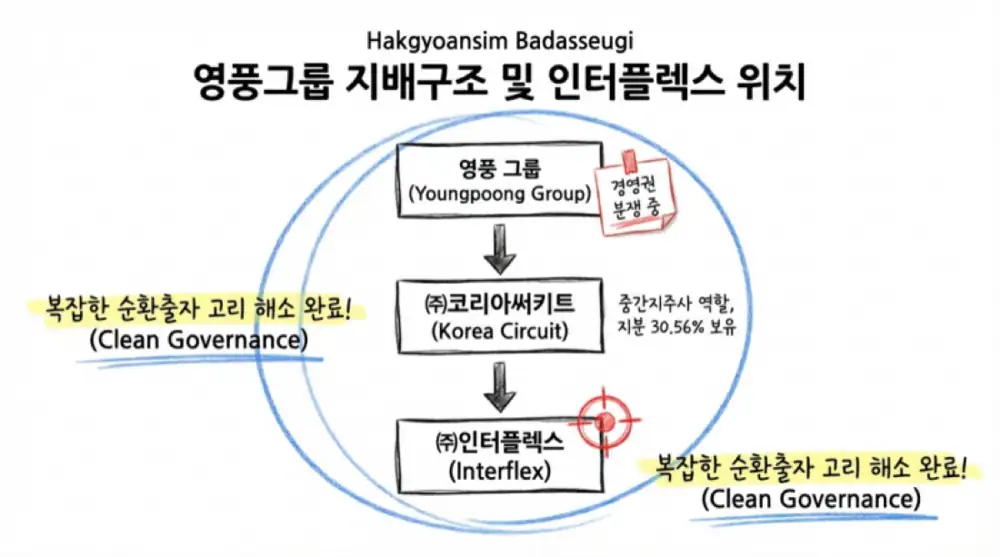

3. Governance and Vietnam footprint redesign

Interflex is an electronics-parts affiliate within the Youngpoong group, with Korea Circuit as its largest shareholder. The source interprets the Youngpoong-Korea Zinc control dispute as a catalyst for faster decision-making across the electronics affiliates.

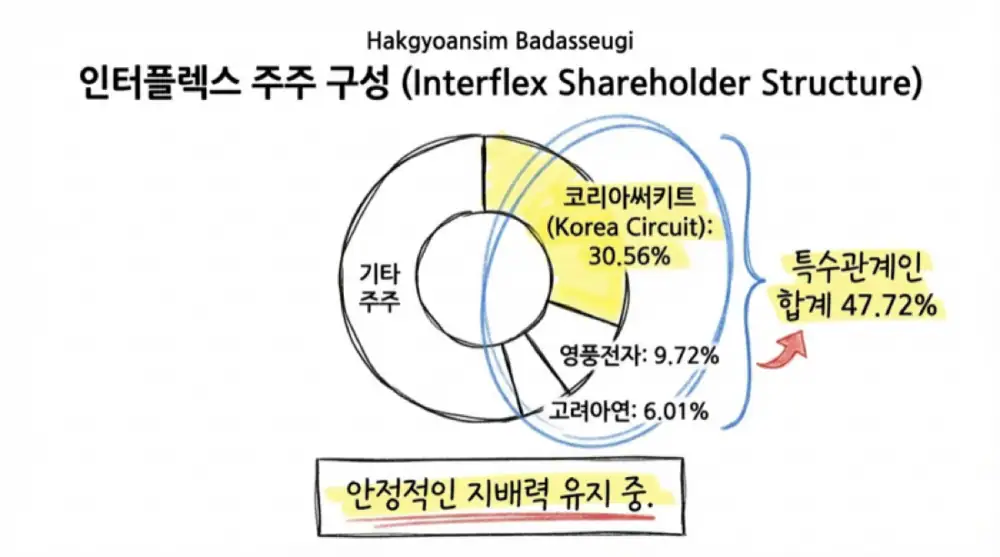

| Shareholder/person | Stake or role | Source interpretation |

|---|---|---|

| Korea Circuit | 30.56% of Interflex | Intermediate holding company for electronics components |

| Youngpoong Electronics | 9.72% | Same-industry FPCB and components affiliate |

| Korea Zinc | 6.01% | Core non-ferrous metals affiliate in dispute |

| Advisor Hyung-jin Jang | Bought 10.4% of Youngpoong shares worth about KRW 133.6 billion, raising his personal stake to 11.5% | Signal of stabilization and electronics-affiliate rebuilding |

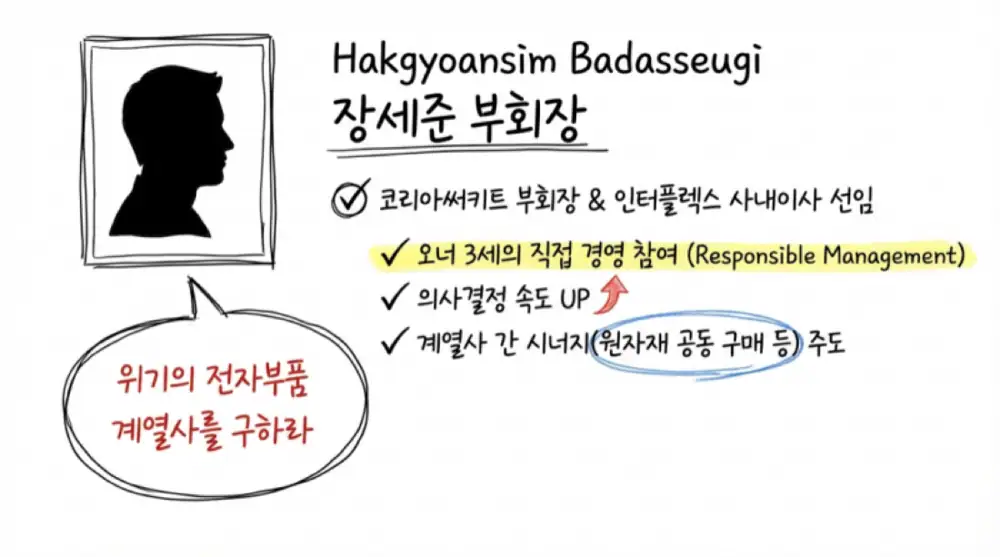

| Vice Chairman Se-jun Jang | Largest individual Youngpoong shareholder at 16.9%; appointed Interflex inside director on March 28, 2025 | Center of a Korea Circuit-Interflex-Youngpoong Electronics “one team” strategy |

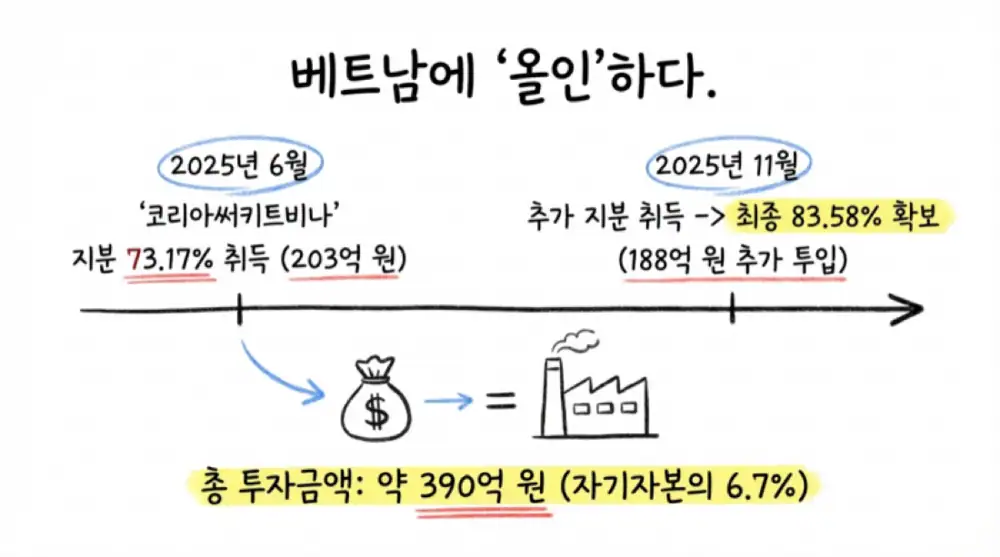

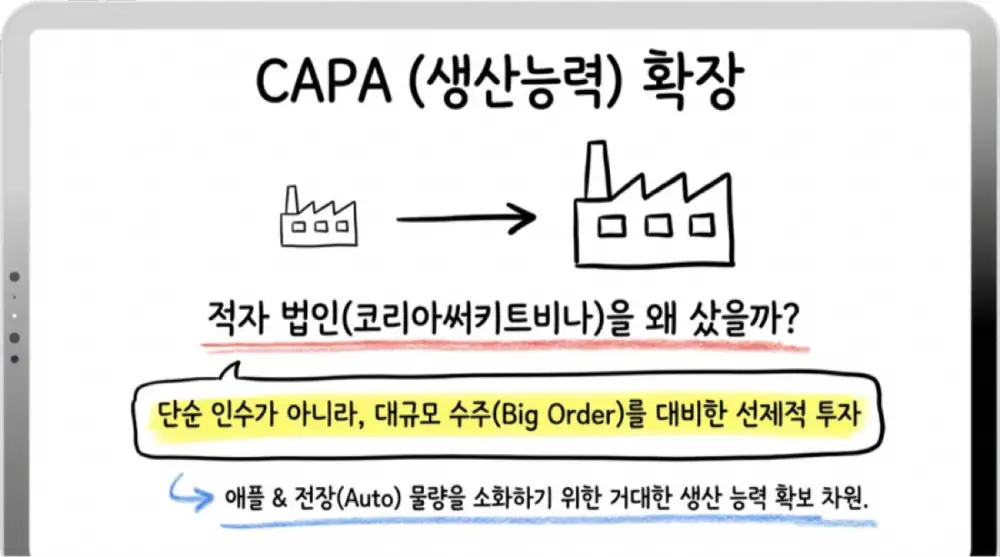

The biggest footprint change is the consolidation of KOREA CIRCUIT VINA. Interflex invested KRW 20.364 billion, or USD 15 million, on June 27, 2025 to acquire 73.17%, then invested another KRW 18.811 billion, or USD 13 million, on November 14, 2025 to lift ownership to 83.58%.

| Date | Amount | Ownership after deal | Meaning |

|---|---|---|---|

| 2025-06-27 | KRW 20.364 billion | 73.17% | Changed from Korea Circuit’s wholly owned subsidiary into Interflex’s consolidated subsidiary |

| 2025-11-14 | KRW 18.811 billion | 83.58% | Additional cash investment equal to 6.68% of KRW 281.7 billion equity |

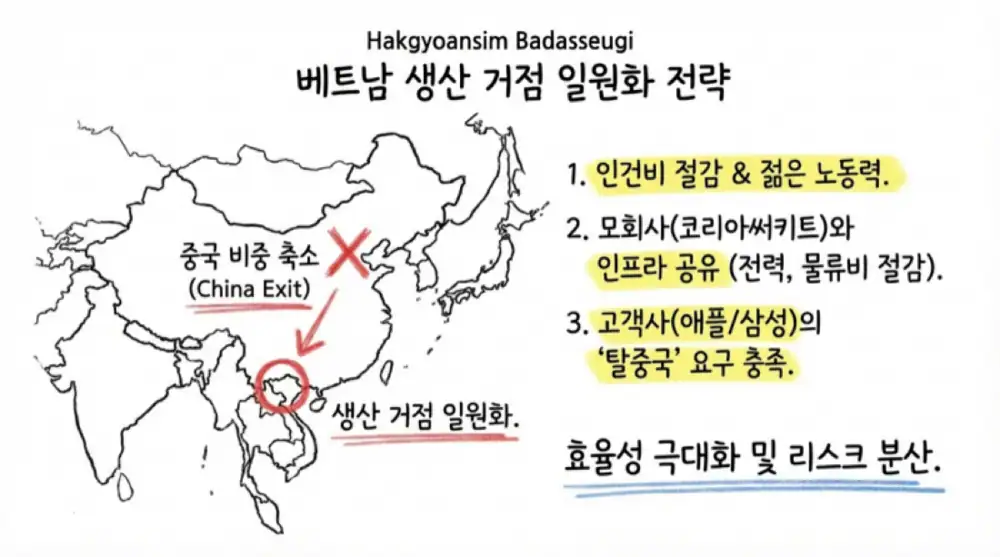

Interpretation: The source reads this investment as China-risk avoidance, shared Vietnam utilities, and pre-built capacity for Apple and automotive electronics demand. KOREA CIRCUIT VINA had KRW 6.138 billion in assets and a KRW 471 million net loss at end-2024, but the roughly KRW 39 billion rapid investment is treated as a signal of expected large-scale demand.

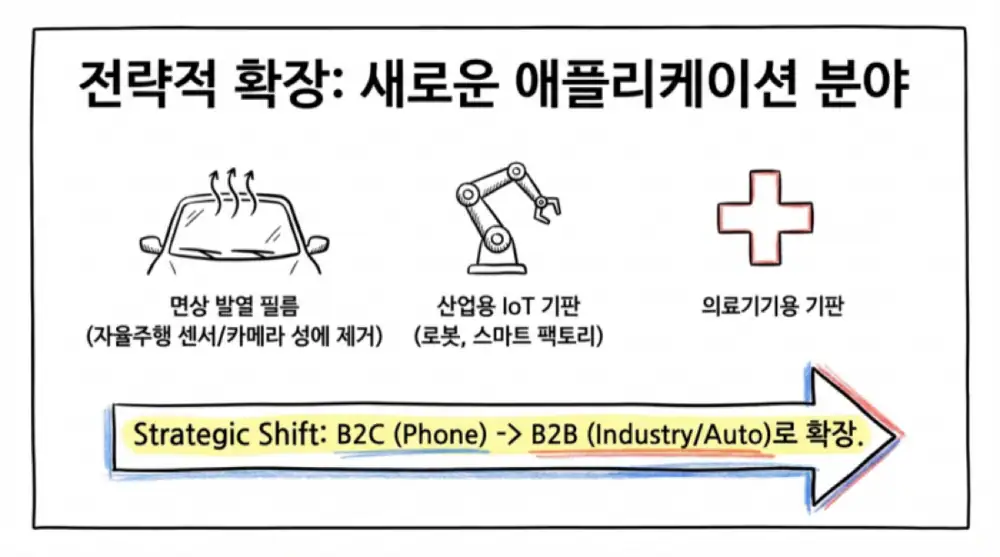

4. New-business pipeline

| New item | Application | Expected effect |

|---|---|---|

| EV BMS FPCB | Replacing bulky copper wire harnesses with thin, light FPCB | EV weight reduction and higher battery-cell density |

| Autonomous-driving ADAS board | High-reliability R/F board connecting cameras/lidar sensors to ECUs | Lossless data transfer under vibration and humidity |

| Planar heating film/lighting | Temperature sensors, heating structures, heating units, LED FPCB for vehicles | Seats, sensor-lens defrosting, and flexible rear-lighting modules |

| Industrial IoT circuits | Waterproof and dustproof FPCB for industrial devices | Longer B2B product cycles than mobile components |

| G-FAST printed substrate | Printed circuit process replacing etching/deposition | EMI shielding plus cost competitiveness |

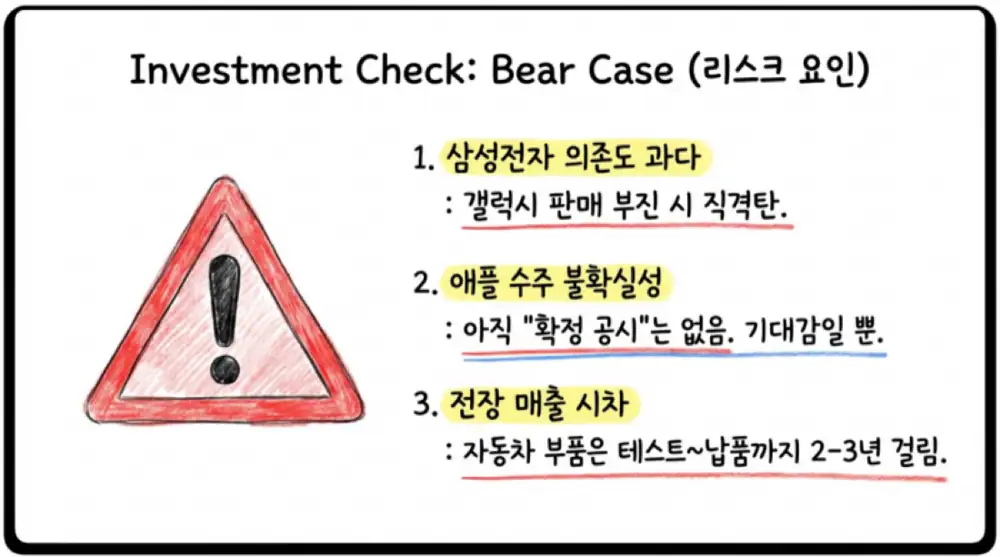

Automotive electronics can provide long revenue duration after qualification, but the source flags the usual 2-3 year lag from design-in to mass-production revenue as a short-term risk.

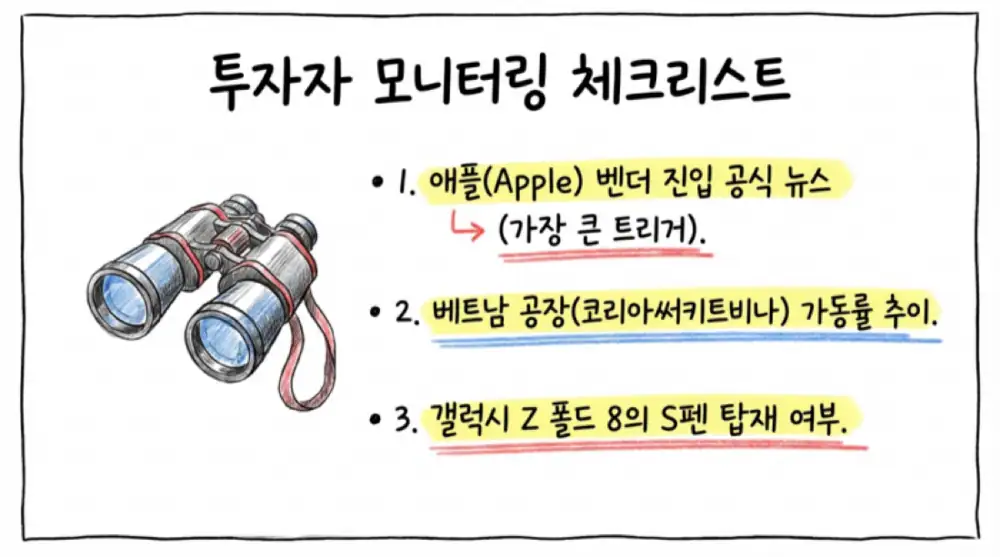

5. Monitoring points

- Whether Apple-related FPCB expectations become an official order and vendor-entry announcement.

- Whether KOREA CIRCUIT VINA can begin automotive/industrial large-volume supply with stable yield and meaningful revenue.

- Whether Korea Circuit and Interflex’s shared Vietnam utilities, joint purchasing, and shared R&D infrastructure appear in margins.

Interpretation: The Q4 2025 earnings jump is easier to read as the first number from a combined customer-mix, footprint, and yield transition than as a simple seasonal spike.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224190347252

- 원문 외부 이미지: https://lh7-rt.googleusercontent.com/docsz/AD_4nXfarlls6CUKxuK_qorC9HzHopgF8sky3ArF4ymMpvG4MOhEj40ucDxY97YdhAkAofHFcNd2oEBpPNPHHvAinxYrAQ8OKXgdhE9TKZrYb3XsdRlP4kj77Zf95S5TCwZ4om1Ktl5s2Che_ZIrJIErWotzExdvw6M?key=JrzN94MWd7F7IGUv4UPwRA

- 인터플렉스 실적 정상화 기사 - 뉴스핌: https://m.newspim.com/news/view/20251117000120

- 인터플렉스 애플향·전장 기대감 - 모바일한경: https://plus.hankyung.com/apps/newsinside.view?aid=202511253540a&category=&sns=y

- 고려아연 vs MBK·영풍 배경 - 중앙일보: https://www.joongang.co.kr/article/25277901

- [지배구조 리포트] 영풍 - 딜사이트: https://dealsite.co.kr/articles/51096/025076

- 고려아연 경영권 분쟁 1년 - YouTube: https://www.youtube.com/watch?v=FOCgVZouzXE

- 엠씨넥스 갤럭시S26 울트라 공급 기사 - 전자신문: https://www.etnews.com/20250929000227