DEEP RESEARCH · HWASHIN

Hwashin: 4Q Earnings Surprise and BPC-Led Re-Rating

A review of Hyundai/Kia HEV strength, U.S./India new plants, and eM-platform BPC orders

0. Bottom line first

Hwashin’s 4Q25 result does not look like a simple FX benefit. HEV chassis volume, Georgia/Pune ramp-up, and high-value BPC mix appear to have worked together. If the market is focused only on the EV chasm and tariff risk, the key point is that those risks may strengthen Hwashin’s local-production moat.

KRW 1.9625tn revenue

Preliminary revenue rose 14.6% YoY.

KRW 102.7bn operating profit

Up 57.2% YoY, with margin improvement.

KRW 939.9bn order

Hyundai Mobis eM-platform battery-pack case supply contract.

1. Business structure and moat

Official fact: The source describes Hwashin as a chassis and body parts supplier to Hyundai and Kia. Chassis parts account for more than about 65% of consolidated revenue, while body parts contribute around 11-13%.

Interpretation: Hwashin’s strength is not simple contract manufacturing. It participates from early vehicle development as a guest engineer across design, DMU, structural/dynamic analysis, and prototype evaluation, creating locked-in revenue over a five-to-seven-year model lifecycle.

2. Hyundai/Kia and HEV exposure

Official fact: The source says Hyundai recorded 4,138,389 global wholesale units, KRW 186.2545tn revenue, and KRW 11.4679tn operating profit in 2025. It also cites global hybrid sales of 3.63mn units, up 20.8% YoY.

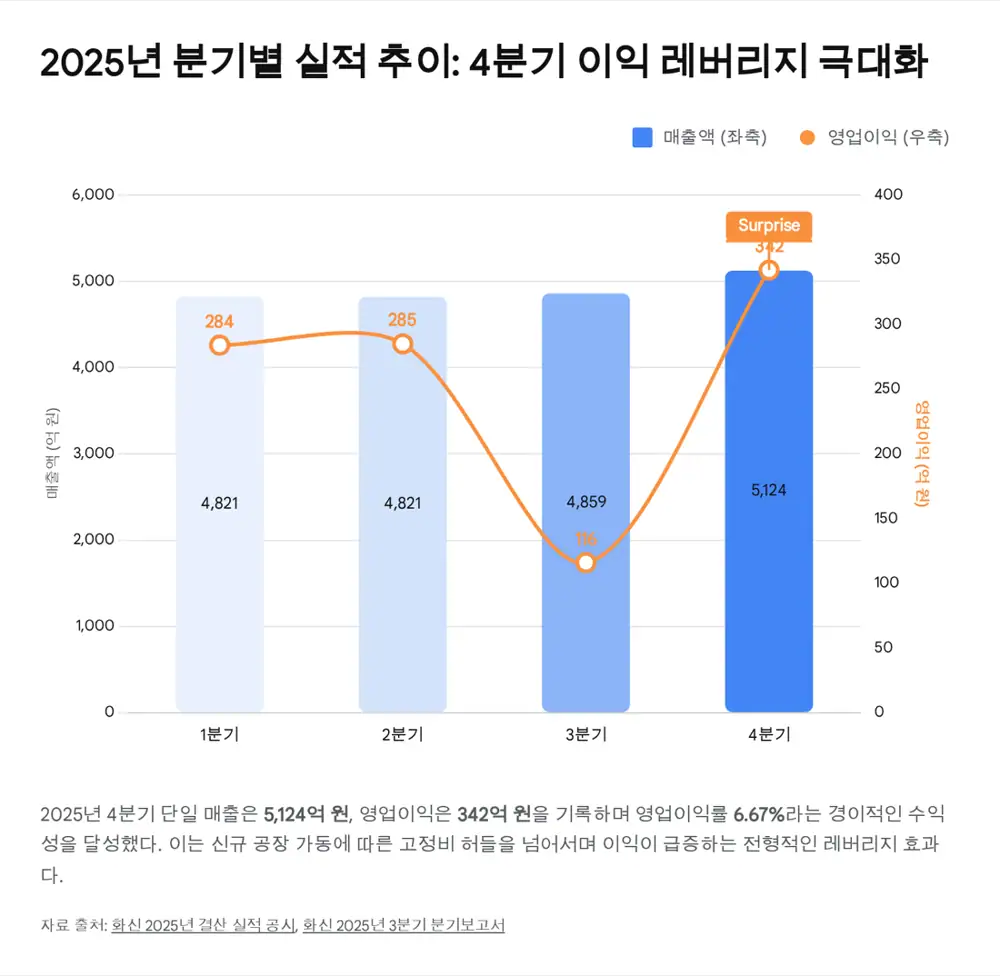

3. 4Q preliminary result breakdown

| Item | Figure | Meaning |

|---|---|---|

| 2025 revenue | KRW 1.9625tn | +14.6% YoY |

| 2025 operating profit | KRW 102.7bn | +57.2% YoY |

| 2025 net income | KRW 82.4bn | +53.8% YoY |

| Implied 4Q25 revenue | About KRW 512.4bn | After subtracting 9M revenue of KRW 1.4501tn |

| Implied 4Q25 operating profit | About KRW 34.2bn | OPM about 6.67% |

4. Q/P/C: why profit jumped

HEV and new plants

Orders rose for high-strength chassis parts for mid-large HEVs, while Georgia HGA and Pune entered yield stabilization in 2H25.

BPC ASP

EV battery-pack cases using aluminum extrusions and FSW carry higher ASP than legacy steel chassis parts.

Operating leverage

4Q revenue above KRW 510bn diluted depreciation burden, while yield stabilization and cost cuts improved COGS.

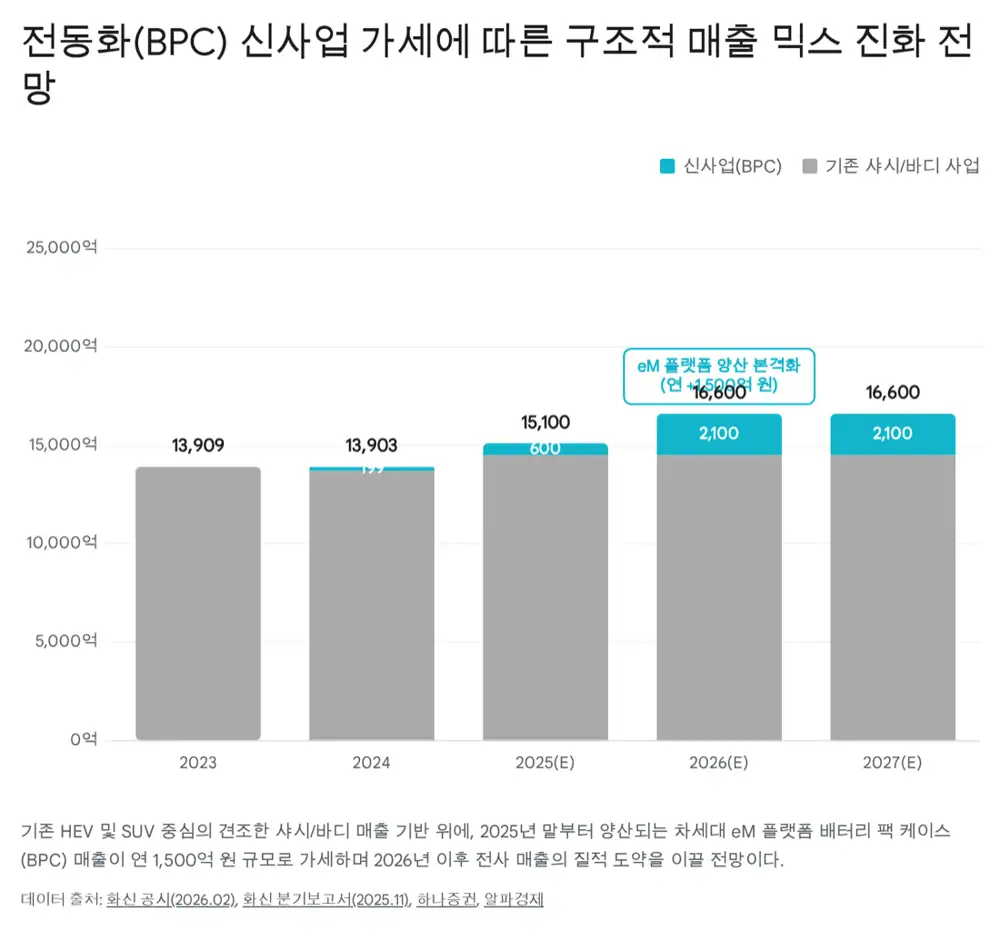

5. BPC and the eM platform

Official fact: On October 21, 2024, Hwashin signed a KRW 939.9bn eM-platform battery-pack case supply contract with Hyundai Mobis. The supply period runs six years, from November 15, 2025 to November 14, 2031.

Interpretation: The source sees this as KRW 100-150bn of average annual high-margin revenue. The eM platform is framed as a second-generation premium EV architecture for Genesis GV90, next K8, G70, and others; winning main-vendor status validates Hwashin’s aluminum processing and FSW capability.

6. Financials and shareholder returns

Official fact: As of 3Q25, the source cites consolidated assets of about KRW 1.5007tn, liabilities of KRW 957.0bn, equity of KRW 543.7bn, debt ratio of about 176%, interest-bearing debt of about KRW 571.6bn, and 9M operating cash flow of KRW 85.2bn.

Interpretation: The source views this debt as productive debt for Georgia, Pune, and Yeongcheon BPC capacity. From 2026, post-capex-peak EBITDA and FCF could support debt repayment and lower interest expense.

| Dividend policy | Content | Meaning |

|---|---|---|

| Base | Annual consolidated net income | Includes overseas subsidiaries |

| Payout | Around 7% | Balance between growth investment and returns |

| Period | 2024-2026 | Provides dividend visibility |

7. Valuation and risks

The source calculates EPS of about KRW 2,359 using preliminary 2025 net income of KRW 82.38bn and 34,920,410 shares. Applying a conservative 7.0x target P/E gives a minimum fair value of KRW 16,500.

- Misunderstanding 1: the EV chasm is also a hedge because it boosts HEV high-strength chassis demand.

- Misunderstanding 2: tariff risk can become a local-share opportunity for Hwashin, which already has U.S. capacity.

- Misunderstanding 3: the legacy steel-parts frame is being broken by the eM-platform BPC order.

- Main risks are a sharp Hyundai/Kia global-sales collapse, eM schedule delay, and U.S. tariff policy.

The source conclusion is Strong Buy. I would track Hyundai/Kia monthly U.S. and India sales, HEV/EV mix, tariff decisions, and eM platform launch timing.