DEEP RESEARCH · ILJIN ELECTRIC

Iljin Electric: EHV Power-Equipment Supercycle and 2025 Earnings Surprise

A view across AI data centers, aging-grid replacement, Hongseong capacity expansion, and the HVDC option

0. Bottom line first

Iljin Electric’s preliminary 2025 results directly challenge peak-out fears. Revenue above KRW 2tn, operating profit up 89.6%, and net income up 132.3% look like the result of EHV transformer/cable mix improvement combined with a power-grid supercycle.

KRW 2.0445tn

Preliminary 2025 revenue grew 29.6% YoY, passing KRW 2tn for the first time.

KRW 151.2bn

Up 89.6% YoY, far faster than revenue.

KRW 107.2bn

Up 132.3%, showing higher-quality earnings.

1. Business model and moat

Official fact: The source describes Iljin Electric as a heavy-electrical and cable manufacturer focused on EHV cable, EHV transformers, and breakers. It says the company has shifted from low-margin copper wire and generic power cable toward EHV cable and transformers.

Interpretation: EHV power equipment depends on decades-long operating records and utility vendor approval, not simple manufacturing capability. The source argues that Hongseong expansion and track record have lifted Iljin into a fourth major EHV competitor alongside HD Hyundai Electric, Hyosung Heavy Industries, and LS Electric.

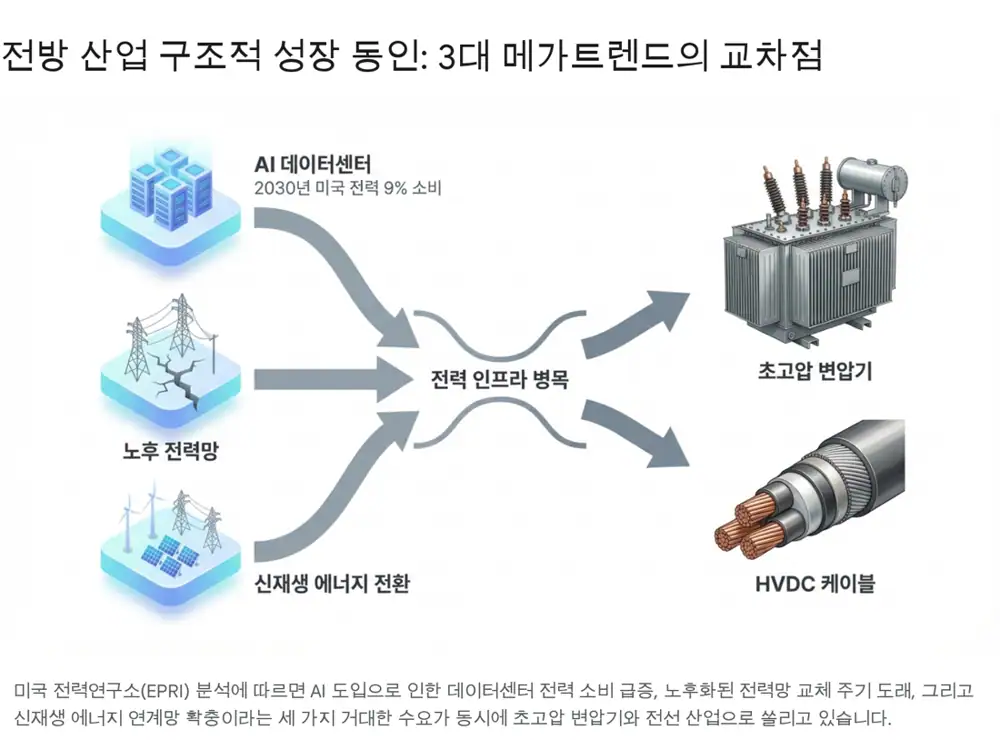

2. End market: AI power demand and aging-grid replacement

Official fact: The source cites EPRI analysis that generative-AI search can use more than 10 times the power of conventional search, and that data centers could consume about 9% of total U.S. power generation by 2030.

3. Preliminary 2025 results

| Item | 2024 | 2025 consensus | 2025 preliminary | YoY |

|---|---|---|---|---|

| Revenue | KRW 1.5772tn | KRW 1.9859tn | KRW 2.0445tn | +29.6% |

| Operating profit | KRW 79.7bn | KRW 148.7bn | KRW 151.2bn | +89.6% |

| Net income | KRW 46.1bn | KRW 92.8bn | KRW 107.2bn | +132.3% |

Interpretation: Profit rose much faster than revenue because high-value EHV transformers and underground EHV cable were recognized heavily in 4Q. The source highlights a KRW 198bn contract for 24 transformers and a first U.K. order of about KRW 10bn.

4. Q/P/C impact

Hongseong Plant 2

KRW 68.2bn invested in 30,000MVA annual EHV transformer capacity eased the bottleneck.

High-margin mix

U.S. grid shortages and EHV product mix support price and margin.

Pass-through

Escalation clauses hedge copper and other input costs, with room to pass tariffs and logistics costs to customers.

5. 2026 leverage: capacity and HVDC

- The source says EHV transformer annual revenue capacity rises from around KRW 300bn in 2024 to KRW 433bn in 2026.

- The cable segment is expanding high-power cable capacity from KRW 540bn to about KRW 620bn by 2026 through KRW 17.6bn of additional capex.

- The thesis depends on an USD 1.8bn backlog and USD 350-400mn U.S. long-term supply contract converting into 2026 revenue.

- HVDC 525kV underground cable is presented as a catalyst for projects such as Korea’s East Coast-to-Seoul grid and West Coast energy highway.

6. Financials, returns, and valuation

Official fact: The source gives end-2025 consolidated assets of KRW 1.5266tn, liabilities of KRW 934.7bn, and equity of KRW 591.9bn. Equity rose more than 18.3% from KRW 500.3bn in 2024.

Interpretation: The source values management’s reinvestment of surplus cash into core capacity, including KRW 68.2bn for Hongseong and KRW 17.6bn for high-power cable capacity. Shareholder returns remain underdeveloped beyond dividends, so a clearer return policy could become a value-up catalyst.

On valuation, the source argues that peak-out fears are creating mispricing. It references peer PER around 19x or higher and domestic target-price increases up to KRW 70,000 as evidence of re-rating potential.

7. Risks and strategy

- Global infrastructure-investment delay is the largest macro risk, though grid modernization may be delayed rather than cancelled.

- Extreme LME copper volatility can cause temporary book losses or margin squeeze.

- Yield issues or delivery delays at Hongseong Plant 2 would hurt the 2026 full-year contribution scenario.

- The source conclusion is Strong Buy, with a long horizon into late 2026 or early 2027 as backlog converts and HVDC orders emerge.