DEEP RESEARCH · SOULBRAIN

Soulbrain: The Hidden Process Enabler of the AI Storage Supercycle

Connecting ICMS, 3D NAND layer scaling, HSN etchants, and 2026 earnings leverage

0. Bottom line first

My conclusion is that Soulbrain has been overlooked relative to HBM names, but if the post-Rubin AI bottleneck shifts toward storage and persistent long-context memory, the company could receive direct materials leverage. The key is that 3D NAND layer scaling can raise both HSN etchant volume and price.

KRW 923.4bn revenue

Up 7.0% from KRW 863.4bn in the source.

KRW 42.9bn operating profit

About 24.7% higher than 3Q, indicating a turn.

KRW 1.1tn revenue

18.5% OPM and KRW 204bn operating profit forecast.

1. The AI bottleneck moves to storage

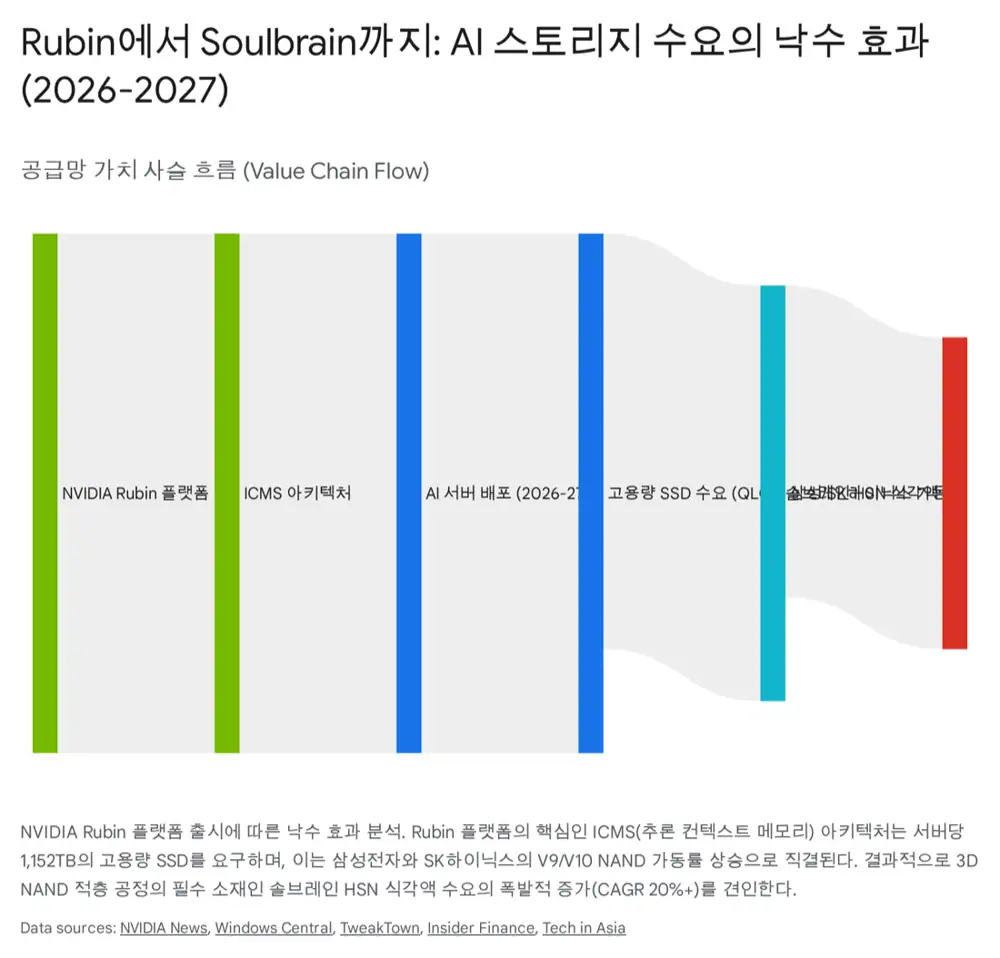

Official fact: The source says NVIDIA Rubin introduces ICMS, or Inference Context Memory Storage, and estimates about 1,152TB of additional SSD NAND per Rubin NVL72 rack. It also cites Citi Research estimates that ICMS could represent about 2.8% of global NAND demand in 2026 and 9.3% in 2027.

Interpretation: If HBM solved the compute-bandwidth bottleneck, Rubin shifts the next constraint to high-speed, high-capacity SSDs for long context and persistent memory. This can become alpha demand on top of normal NAND bit growth.

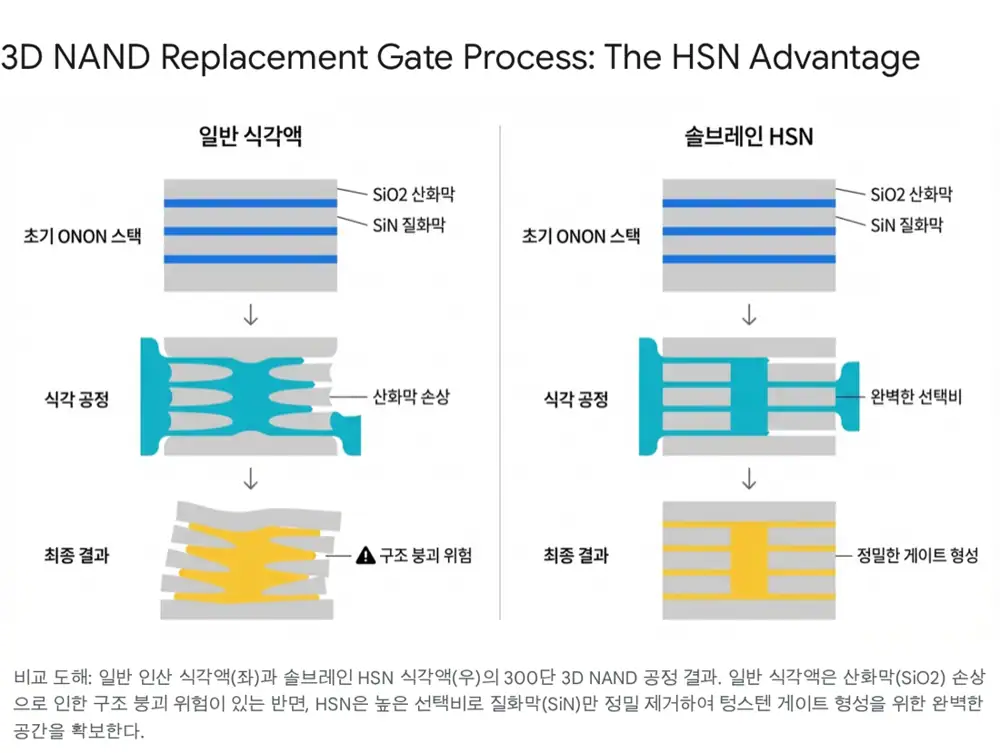

2. HSN: the chemical answer to 3D NAND scaling

3D NAND is moving from 176-layer V7 and late-200-layer V8 toward 300-plus-layer V9 and 400-layer-class V10. The replacement-gate wet etch that removes silicon nitride while preserving oxide is one of the critical bottlenecks.

Official fact: The source says Soulbrain’s HSN uses additive technology and silicon-concentration control to raise oxide selectivity and suppress loading effects in ultra-tall structures.

3. Q and P rise together

| Variable | Source logic | Earnings impact |

|---|---|---|

| Q | Estimated etchant consumption per wafer rises about 37% beyond 200 layers | More layers, longer process time, and shorter recycle life lift shipment volume |

| P | Higher layers require stricter selectivity and impurity control | Premium HSN mix rises versus commodity phosphoric acid |

| Technology fit | Cryogenic etch is channel-hole dry etch; HSN is later wet strip | Cryogenic etch enables taller stacks and expands HSN TAM rather than replacing it |

4. Customers and timeline

- The source describes Soulbrain as a strategic supplier with high share in etchants and CMP slurry at Samsung Electronics and SK hynix.

- 2H25: Samsung Pyeongtaek P4 V9 NAND tool setup and pilot run, with materials pre-orders and inventory build.

- 1Q26 to 1H26: Rubin production and data-center delivery, Samsung V9 QLC NAND mass production, and HSN shipment ramp.

- 2H26 to 2027: V10 400-layer-class investment and HBM4 hybrid-bonding CMP slurry contribution.

5. Earnings and valuation

| Item | 2024 | 2025E | 4Q25E | 2026E | 2027E |

|---|---|---|---|---|---|

| Revenue | KRW 863bn | KRW 923bn | KRW 244bn | KRW 1.1tn | KRW 1.35tn |

| Operating profit | KRW 168bn | KRW 134bn | KRW 43bn | KRW 204bn | KRW 285bn |

| OPM | 19.5% | 14.5% | 17.6% | 18.5% | 21.1% |

| Controlling net income | KRW 118bn | KRW 83bn | - | KRW 165bn | KRW 230bn |

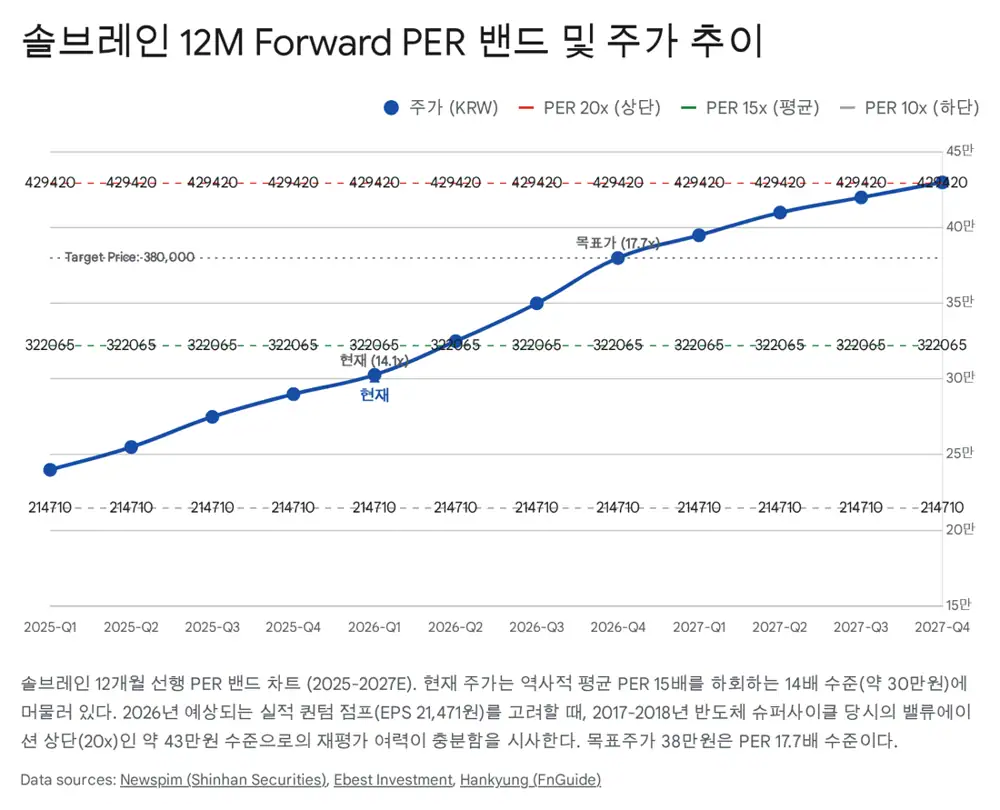

Interpretation: 2025 was an investment and cost year, but the 4Q margin recovery suggests HSN mix and cost structure are already improving. The source sees 12M forward PER of 12-14x on 2026E EPS of KRW 21,471, below the 15-20x multiple seen in prior NAND upcycles.

6. Risks and trading plan

- Delayed Samsung V9 QLC NAND yield stabilization is the main near-term risk.

- HBM4 hybrid-bonding CMP slurry could face pricing pressure from competitors such as Dongjin Semichem.

- The source target price is KRW 380,000, applying 18x target PER to 2026E EPS of KRW 21,471.

- Monitoring indicators are P4/P5 etch-tool move-ins, NAND contract prices, and precision-chemical export data from Sejong/Gongju.

I view Soulbrain as a hidden leader in the AI storage supercycle, but the Samsung V9 QLC schedule and materials shipment ramp must be verified quarter by quarter.