DEEP RESEARCH · SEOUL VIOSYS

Seoul Viosys: Price Normalization and Technology Leadership Driving a Structural Turnaround

Testing the durability of qualitative growth from Violeds, WICOP, automotive, UV, and micro LED

0. Bottom line first

The core of Seoul Viosys' 2025 story is not just revenue recovery. Price normalization and a shift toward higher-value products are beginning to show up in the numbers. 4Q25 revenue of KRW 221.1 billion and a 2025 EBITDA margin of 10.2% are the first tests of whether automotive, UV, and micro LED can pull the company away from commodity LED price wars.

KRW 221.1B revenue

Up 23.6% YoY and more than 31% above 1Q24 revenue of KRW 168.0B.

KRW 763.8B revenue

Revenue continued rising after KRW 504.0B in 2023 and KRW 699.2B in 2024.

18,000+ patents

The company has built technical barriers around Violeds and WICOP.

Official fact: The source summarizes Seoul Viosys' 4Q25 revenue at KRW 221.1 billion, full-year 2025 revenue at KRW 763.8 billion, EBITDA at KRW 77.7 billion, and EBITDA margin at 10.2%. The company guided 1Q26 revenue at KRW 190.0-200.0 billion.

Interpretation: The quality of the numbers matters. The source's central read is that the company defended double-digit EBITDA margin because it shifted from low-priced commodity LEDs toward higher-value automotive, UV, industrial, and micro LED products.

1. 2025 earnings summary

| Item | 2023 | 2024 | 2025 | 4Q25 | Note |

|---|---|---|---|---|---|

| Revenue | KRW 504.0B | KRW 699.2B | KRW 763.8B | KRW 221.1B | Continued top-line growth |

| EBITDA | KRW 2.3B | KRW 83.0B | KRW 77.7B | - | Cash-generation recovery |

| EBITDA margin | 0.5% | 11.9% | 10.2% | - | Double-digit margin defended |

| R&D investment | KRW 53.3B | KRW 56.9B | KRW 69.8B | - | Future-technology investment rising |

4Q25 revenue rose 23.6% from roughly KRW 179.0 billion in 4Q24 and represented about 29% of full-year revenue. For a quarter that is usually seasonally weak in LEDs, that sales concentration suggests stronger momentum into the second half.

Interpretation: Defending a 10.2% EBITDA margin after the 2024 EBITDA rebound supports the idea that product mix, not just cost cuts, is working. Still, the separate question is how much EBITDA and operating cash flow can reduce balance-sheet stress.

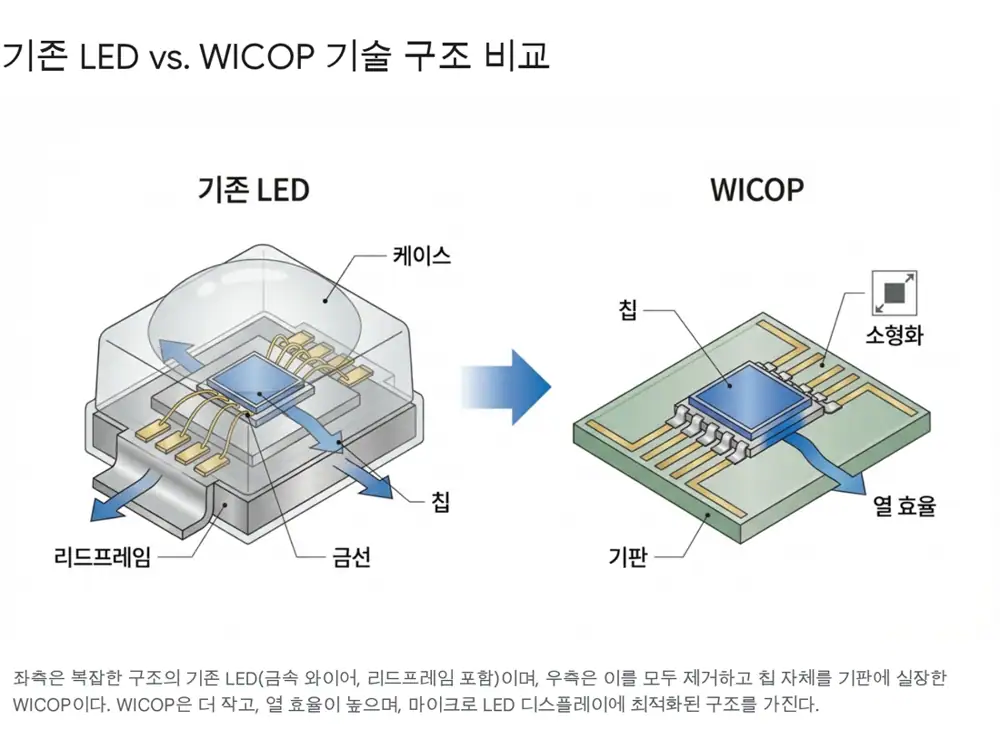

2. Technology moat: Visible to Invisible

Seoul Viosys is framed not as a simple LED chip maker, but as an optical-semiconductor solution company spanning ultraviolet, visible, and infrared/VCSEL wavelengths. If Seoul Semiconductor is stronger in packaging and modules, Seoul Viosys is specialized in the upstream core of epitaxy and chip manufacturing.

- Violeds: The source says Seoul Viosys ranked No. 1 in the global UV LED market for six consecutive years as of 2024. Violeds is an eco-friendly sterilization, disinfection, and deodorization technology that can replace mercury lamps and chemicals.

- WICOP: Wafer Level Integrated Chip on PCB removes the lead frame and gold wire, mounting the chip directly on the PCB. The benefits are lower cost, lower thermal resistance, smaller size, and greater design freedom.

- No-Wire patents: The source describes WICOP's no-wire technology as a prerequisite for micro LED and the basis for patent-litigation wins in Europe and elsewhere.

3. 4Q25 earnings: the price-normalization strategy

The source treats the fourth-quarter performance as the result of a strategic pivot, not just market recovery. In the past, the company accepted low-priced orders to raise utilization. Now, the source argues that it is using proprietary technology to get paid properly.

10.2% EBITDA margin

Interpreted as the result of lower commodity-lighting LED mix and higher automotive, UV, and industrial mix.

Price normalization

Patented technologies such as WICOP are harder to replace, improving bargaining power.

4Q weakness overcome

More than 20% YoY growth suggests a shift toward steadier B2B automotive and industrial demand.

In automotive, EVs and premium vehicles continued adopting more LEDs, while high-output headlamp LEDs and in-cabin UV sterilization demand supported results. WICOP is described as helping improve EV power efficiency and slim designs, increasing adoption.

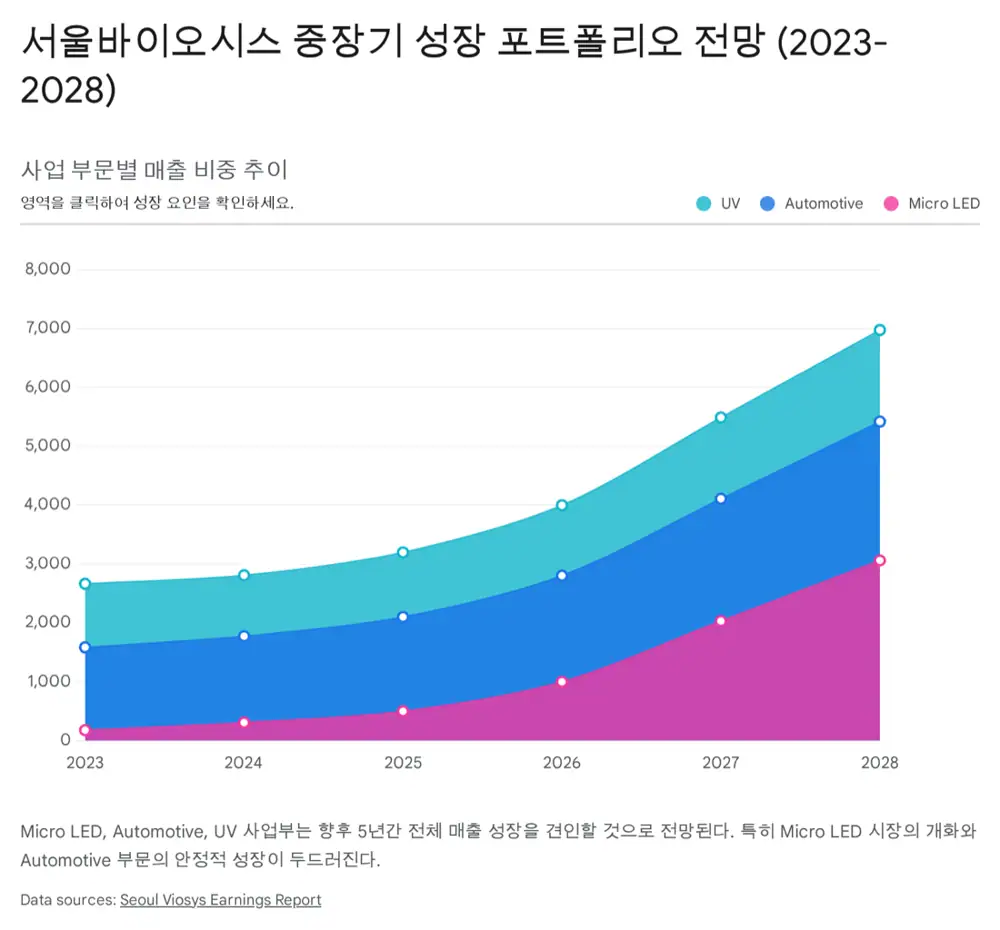

4. Three growth engines

| Engine | Core point | Numbers and evidence |

|---|---|---|

| Automotive | Vehicle lighting is evolving from visibility into design identity and pedestrian communication. WICOP fits the space-efficiency needs of EV design. | The source says many of the global top 10 automotive brands have adopted WICOP and that applied models exceed 100. |

| UV / Bio | Under the Minamata Convention, manufacture and import/export of mercury-containing lamps are phased out from 2026, creating UV LED replacement demand. | Seoul Viosys is described as global No. 1 in UV LEDs for six consecutive years. UV-C is technically difficult, limiting low-cost entry. |

| Micro LED | Micro LED is the next-generation display that can overcome OLED burn-in and brightness limits. WICOP Pixel vertically stacks RGB devices into one chip-like structure. | The source cites Omdia's forecast that the micro LED chip market will grow to USD 2.7 billion in 2026. WICOP Pixel can reduce package area to one-third. |

Interpretation: The common thread is that regulation, vehicle electrification, and difficult process technology are creating demand, not commodity LED price competition. If that holds, Seoul Viosys can deserve a higher multiple than commodity peers.

5. 2026 guidance and qualitative growth

Seoul Viosys guided 1Q26 revenue at KRW 190.0-200.0 billion. The source frames this as about 13-19% growth versus the estimated 1Q25 level, and because first quarter is usually a trough for IT-product demand, it implies backlog and utilization remain high.

- Profitability first: Avoiding low-priced orders may moderate revenue growth, but should improve margins. The source expects EBITDA margin could move from the 2025 10% range toward a mid-term target around 15%.

- CAPEX efficiency: With large investment mostly completed, focus can shift to process efficiency and micro LED yield improvement, which may improve free cash flow.

- Process efficiency and yield stabilization: These are framed as core 2026 management strategies and catalysts for micro LED commercialization.

6. Financial risk and the path to relief

The largest risk is financial health. As of 3Q25, debt-to-equity was 274.4%, up sharply from 170.2% in 2022. The source links this to pandemic-era operating losses and expanded R&D for future technologies such as micro LED. The current ratio was also below 100% at 88.4%, so short-term repayment capacity needs monitoring.

The positive is that 2025 EBITDA of KRW 77.7 billion improves interest coverage directionally. The source's solution path is for cash generated through price normalization to be prioritized for debt repayment, gradually reducing leverage if 2026 revenue growth and margin improvement proceed as planned.

7. Valuation and my view

The source compares Seoul Viosys with global optical-semiconductor peers such as ams-OSRAM and Nichia. ams-OSRAM is described as selling non-core assets and restructuring, with earnings volatility and financial risk, while Seoul Viosys is closing the market-share gap with ams-OSRAM to within 1 percentage point. The source argues that being among the global top three while sustaining both revenue growth and market-share gains supports a valuation premium.

EBITDA profit and 4Q surprise

The shift from loss-making to profitable is the strongest re-rating catalyst.

WICOP and Violeds

The question is whether patents and proprietary technologies can neutralize low-cost competition from China.

Minamata Convention

Mercury-lamp phase-out can create policy-driven demand stronger than company-level execution alone.

My conclusion is positive. Rather than focusing on short-term quarterly swings, I would track four structural variables: patented technology exclusivity, environmental regulation plus vehicle electrification, price normalization with profitability-first management, and the pace of debt and liquidity improvement. Financial risk is real, but if turnaround earnings convert into cash flow, the re-rating case can hold.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224181815368

- SeoulViosys: 1Q guidance and WICOP growth: https://www.seoulviosys.com/kr/media/news/178

- SeoulViosys: No. 1 in UV LEDs for six consecutive years: https://www.seoulviosys.com/en/media/news/188

- Semiconductor Today: Seoul Semiconductor closes in on ams OSRAM: https://www.semiconductor-today.com/news_items/2025/may/seoul-semi-120525.shtml

- Seoul Semiconductor: UV LED global No. 1: https://www.seoulsemicon.com/kr/media/newsroom/227

- SeoulViosys: UV LED global No. 1 for six consecutive years: https://www.seoulviosys.com/kr/media/news/188

- HelloT: one-chip micro LED at ISE: https://www.hellot.net/news/article.html?no=74738

- Marketin: 4Q revenue KRW 221.1B: https://marketin.edaily.co.kr/News/ReadE?newsId=04264006645317720

- Electimes: 2024 revenue growth: https://www.electimes.com/news/articleView.html?idxno=349115

- EdisonReport: Seoul Semiconductor Q2 2025 earnings: https://edisonreport.com/2025/08/14/seoul-semiconductor-q2-2025-earnings-growth/

- SeoulViosys Vietnam: third-quarter revenue and operating profit: https://www.seoulviosys.com/vn/media/news/65

- Korea Economic Daily: Violeds replacing mercury lamps: https://www.hankyung.com/article/202206230632i

- The Elec: 2026 micro LED chip market USD 2.7B: https://www.thelec.kr/news/articleView.html?idxno=17775

- English DART: CammSys registration statement: https://englishdart.fss.or.kr/dsbh001/main.do?rcpNo=20260113000671

- Bloter: Cost ratio and loss discussion: https://www.bloter.net/news/articleView.html?idxno=612220

- ams OSRAM: 2026 ad hoc: https://ams-osram.com/documents/d/ams-osram/ad-hoc_2026_en_ams-osram-creating-the-leader-in-digital-photonics

- ams OSRAM: Q3 2025 results ad hoc: https://ams-osram.com/documents/d/ams-osram/ad-hoc_2025_eng-q3-2025-results