DEEP RESEARCH · KBI METAL

KBI Metal: Power-Grid Supercycle and Structural Turnaround

A review of the copper and cable value-chain upside reflected in preliminary 4Q25 and full-year results

0. Bottom line first

KBI Metal’s preliminary 2025 results look closer to a structural turnaround than a simple rebound. Copper prices, North American grid investment, LS Cable and Taihan Electric order momentum, and exports from the Vietnam subsidiary are aligning.

KRW 758.5bn

Revenue grew 7.9% year over year.

KRW 24.3bn

Operating profit rose 39.1%, confirming margin improvement.

KRW 2.3bn

Net income increased 42.6%, strengthening the profit trend.

1. Macro: copper and the power-grid supercycle

Official fact: The source says copper prices stayed above USD 10,000 per ton in 2025, near historical highs. Supply is constrained by aging South American mines and long lead times for new mines, while demand is rising from EVs, renewables, and grid investment.

Interpretation: If a copper fabricator such as KBI Metal can pass raw-material increases into selling prices, higher copper prices can bring both top-line growth and inventory valuation gains.

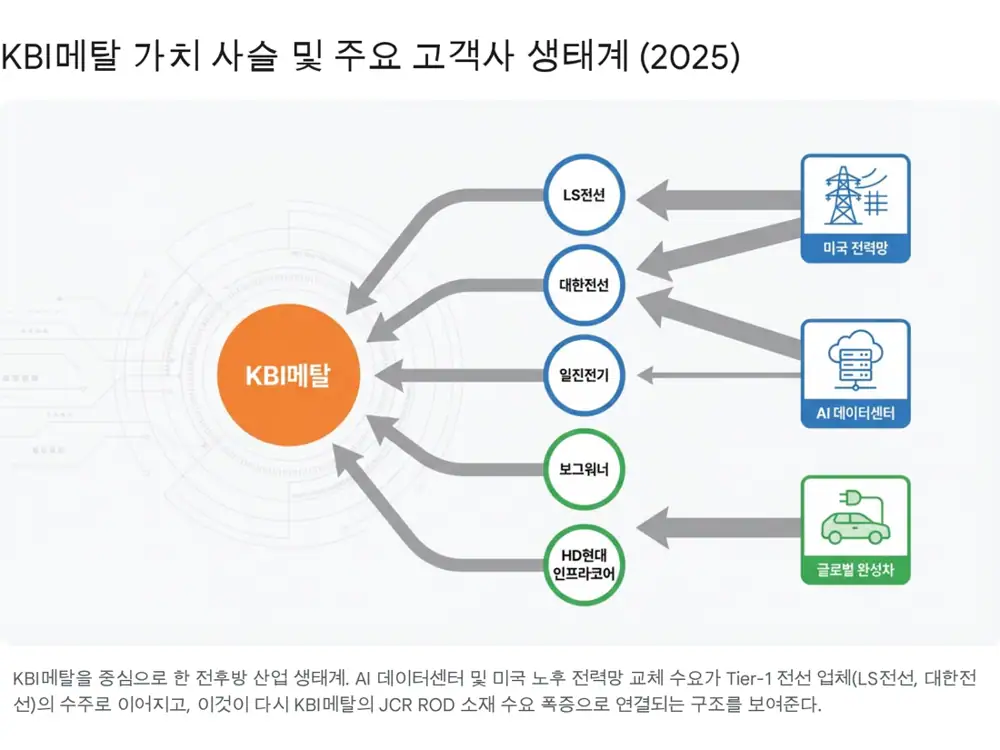

2. AI data centers and the North American grid

- The source cites NERC’s view that U.S. power demand could rise by about 500TWh by 2028 to reach 4,500TWh.

- Hyperscale data centers require large volumes of wires and cables from server-rack connections to substations.

- A large part of the U.S. transmission and distribution grid was built in the 1960s and 1970s and has already exceeded the 40-50 year replacement cycle.

- Insufficient U.S. cable manufacturing capacity creates high-voltage cable opportunities for Korean suppliers such as LS Cable and Taihan Electric, which can flow upstream to KBI Metal.

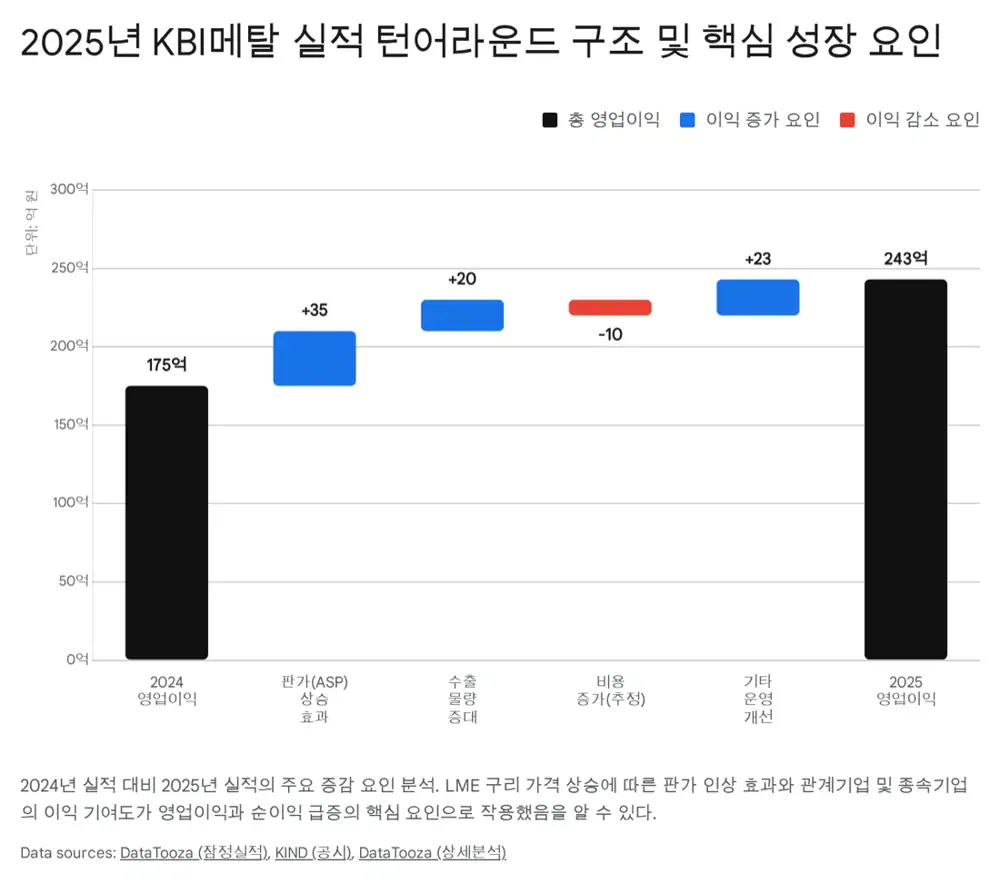

3. Preliminary 2025 results

| Item | Preliminary 2025 | YoY | Meaning |

|---|---|---|---|

| Revenue | KRW 758.5bn | +7.9% | LME copper price and price pass-through |

| Operating profit | KRW 24.3bn | +39.1% | Wider spreads and improved utilization |

| Net income | KRW 2.3bn | +42.6% | Reduced discount from financial costs and affiliate losses |

Interpretation: In the past, net income was often damaged by financial costs or affiliate losses even when operating profit was positive. Stronger net income suggests part of that discount has eased.

4. Vietnam subsidiary and export expansion

Official fact: The source says KBI Group acquired 100% of Vietnam’s SH-VINA in 2017 and launched KBI Cosmolink Vina. It also cites KRW 36bn in 2021 revenue and exceeding the 2022 target of KRW 40bn.

- The Vietnam entity serves both domestic Vietnamese demand and Southeast Asian export markets, supported by ASEAN manufacturing growth and rising power consumption.

- Lower labor and electricity costs than Korea, plus technology transfer from KBI’s cable affiliates, are interpreted as supporting profitability.

- The source says KBI Metal is reviewing and pursuing U.S. market entry based on its domestic No. 1 JCR ROD technology.

- JCR ROD using recycled copper could be preferred in a U.S. market with tighter ESG requirements.

5. Equity-method gains and group synergy

Auto parts

A Hyundai/Kia tier-1 supplier that benefited from stronger 2025 auto conditions.

Copper alloy

Higher copper prices supported inventory gains and product margins.

Cable

A vertically integrated cable affiliate using KBI Metal ROD.

Interpretation: Additional affiliate-share purchases and disposal gains can be read as group-level portfolio optimization. The logic is to monetize non-core stakes and reinvest in higher-growth entities such as overseas subsidiaries, strengthening financial flexibility.

6. Risks and 2026 outlook

- Raw-material volatility: a sharp fall in LME copper could cause inventory losses and lower selling prices.

- FX risk: higher exports increase FX exposure, though simultaneous raw-material imports and product exports provide partial natural hedging.

- End-market visibility: AI data centers and U.S. grid modernization are presented as megatrends that can last at least five years.

- Valuation: the source argues that a 2025 market cap in the KRW 60bn range leaves room for low-PER re-rating if earnings continue improving.

My conclusion is that KBI Metal is a hidden materials beneficiary at the front line of the power-grid supercycle, but copper-price and FX volatility must be tracked alongside the thesis.

Sources

- Naver original post

- DataTooza on KBI Metal 2025 earnings

- Wide Daily on copper price and policy theme

- FerroTimes on KBI Metal operating profit

- Etoday on JCR ROD and U.S. export review

- KRX filing on earnings structure change

- Steel & Metal News on Taihan backlog

- Newswire on Taihan U.S. project

- Dealsite on LS Cable U.S. high-voltage cable order

- KBI Metal quarterly filing

- Seoul Finance on KBI Cosmolink Vina