DEEP RESEARCH · ORIENT PRECISION

Orient Precision: Structural Turnaround Beyond Political Theme Volatility

A review of HEV exposure, SBW and nano-material portfolio shifts, and 2025 earnings improvement

0. Bottom line first

My key takeaway is that Orient Precision still trades like a political theme stock, but its 2025 numbers show a real profitability-focused restructuring. The caution is that the share price already embeds both turnaround expectations and theme premium.

KRW 2,995

The stock hit the daily upper limit on February 12, 2026, up 29.93%.

About KRW 95bn

A level where political-theme demand and turnaround expectations coexist.

9M25 operating profit +71.1%

Consolidated profit improved on mix and cost control.

1. Theme noise versus fundamental signal

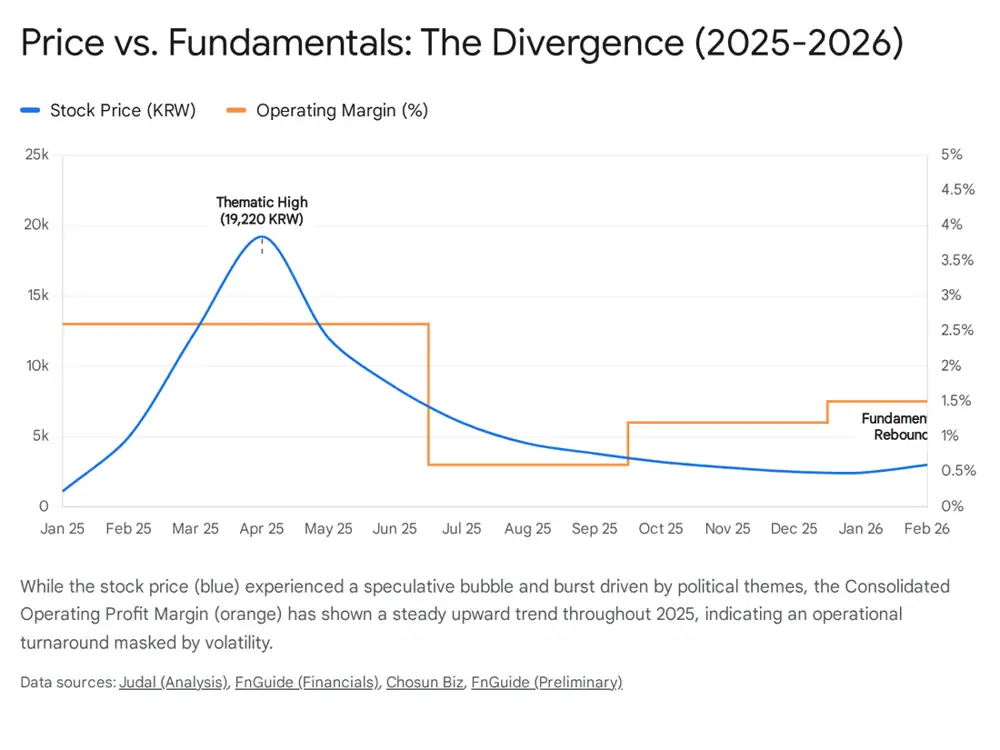

Official fact: The source says Orient Precision closed at KRW 2,995 limit-up on February 12, 2026. It also notes a historical high of KRW 19,220 in April 2025, followed by a decline of more than 80% into the low KRW 2,000 range.

Interpretation: The 2025 boom-bust was theme-driven, but the 71.1% increase in 9M25 consolidated operating profit is a separate fundamental signal. Price volatility and business restructuring should be analyzed separately.

2. The HEV window

As the EV chasm pushes automakers to reinforce hybrid lineups, demand for multi-speed transmissions and DCT precision parts is being defended. Pure BEVs can shrink the TAM for transmission parts, but HEV/PHEV systems combine engines and motors and therefore require more complex powertrains.

3. Technology moat: SBW and nano-composites

Official fact: The source describes Orient Precision as a tier-2 supplier of transmission core parts to Hyundai/Kia through Hyundai Transys, and says it has localized electronic actuators and precision parts for shift-by-wire systems.

Electronic actuators

Safety-critical parts create lock-in once the supplier passes automaker validation.

Nano-composites

The company is expanding lightweight materials into housings and lamp supports.

Legacy to strategic

The portfolio is shifting from manual-transmission forks and brackets to DCT precision parts, SBW, and nano materials.

4. Turnaround through Q/P/C

| Item | Source fact | Read-through |

|---|---|---|

| Q | 9M25 separate revenue KRW 100.9bn, down 5.8% YoY; consolidated revenue down 5.7% | Intentional pruning of low-margin legacy parts |

| P | Operating profit surged despite lower revenue | Hybrid precision and module parts lifted blended ASP |

| C | 9M25 consolidated operating profit +71.1%; separate COGS -6.4% | Raw-material stability, automation, SG&A discipline, and selective R&D |

5. Financials and valuation

Official fact: The source gives a current ratio of about 74.7%, says positive operating cash flow lowers near-term liquidity risk, and cites PER of roughly 240-300x and PBR of about 2.0-2.5x.

Interpretation: The high PER reflects both a small earnings denominator in an early turnaround and a political-theme numerator. The source estimates normalized 2026 revenue of KRW 180bn, operating margin of 4%, operating profit of KRW 7.2bn, and fair market cap of KRW 70-80bn using 10-12x auto-parts PER, implying the current KRW 95bn market cap is 20-30% above that fundamental value.

6. Strategy and risks

- Short term: the February 12, 2026 limit-up move is strong momentum, but it belongs in a disciplined trading framework.

- Long term: fresh entry near KRW 3,000 carries valuation burden; the source prefers waiting for political-theme premium to fade toward PBR 1.0-1.5x.

- Main risks: PER above 200x, political-event sensitivity, and theme-driven swings.

My conclusion is that the fundamental turnaround is real, but the stock sits on the boundary between corporate change and overheated pricing.