DEEP RESEARCH · ICRAFT

iCraft 4Q25 Review: AI Infrastructure Supercycle and the Re-rating Case

Testing whether the company is shifting from network integration to turnkey AI-infrastructure engineering

0. Bottom line first

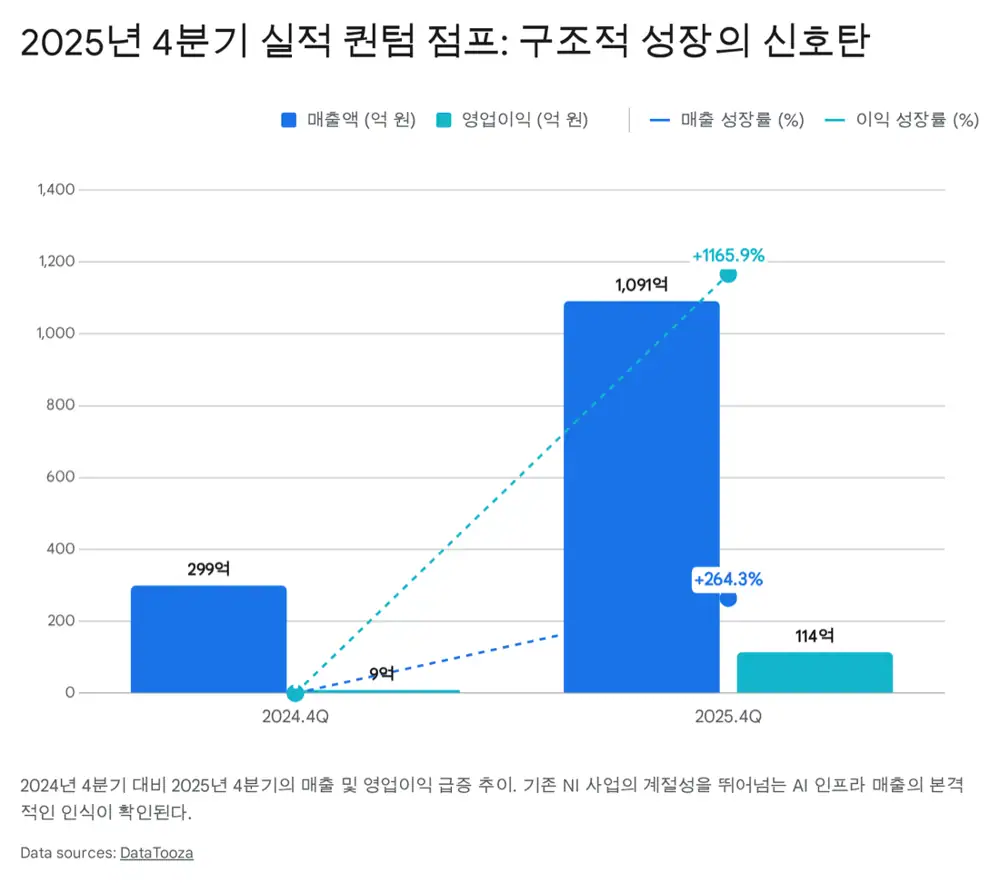

iCraft's preliminary 4Q25 results were KRW 109.0 billion of revenue and KRW 11.4 billion of operating profit, up 264.3% and 1,165.9% YoY, respectively. I read this not as a one-off equipment-resale quarter, but as the first earnings proof that Kakao and Naver Cloud AI-infrastructure contracts plus Nvidia partnership leverage are becoming visible.

KRW 109.0B revenue

Revenue increased 264.3% YoY.

KRW 11.4B OP

Operating profit increased 1,165.9% YoY and operating margin exceeded 10%.

KRW 200B+ sales / KRW 20B+ OP

The source presents this as a conservative possibility considering remaining orders and new Blackwell-related demand.

Official fact: The source summarizes iCraft's February 9, 2026 disclosure of 4Q25 preliminary results as revenue of KRW 109.0 billion and operating profit of KRW 11.4 billion. The Kakao AI-infrastructure contract is presented at KRW 35.5 billion, and the Naver Cloud Infiniband contract at roughly KRW 12.3-12.36 billion.

Interpretation: The key is whether iCraft can move from a low-growth network-integration multiple to an AI-infrastructure solution multiple. But because the business is project-based, revenue recognition can be lumpy; annualizing the fourth quarter mechanically would be risky.

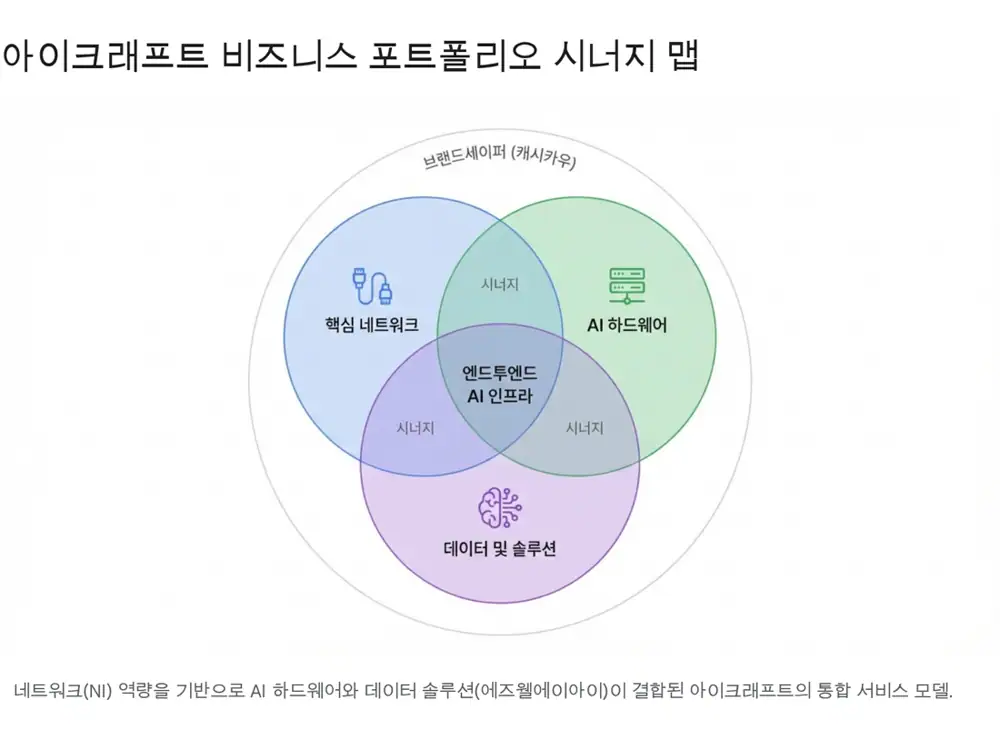

1. Business essence: engineering, not just distribution

The source starts from the idea that iCraft should be viewed not as a simple IT equipment distributor, but as an engineering company that designs and optimizes complex network environments. Its mid-sized enterprise status provides creditworthiness and financing capacity needed to execute large infrastructure projects.

| Business | Description | Investment point |

|---|---|---|

| Core internet network build-out | Supplies and maintains routers, switches, and large data-transfer equipment for telecom backbone networks such as KT and SK Broadband. | High barriers and long customer relationships, but limited growth. |

| AI infrastructure solutions | Provides Nvidia GPU servers such as DGX and ultra-high-speed Infiniband networks on a turnkey basis. | Combines cluster design, thermal management, and software optimization; this is the core driver of the 4Q25 surge. |

| BrandSafer | Anti-counterfeit authentication solution for cosmetics, apparel, and other K-culture consumer goods. | Cash cow that buffers volatility in the AI-infrastructure segment. |

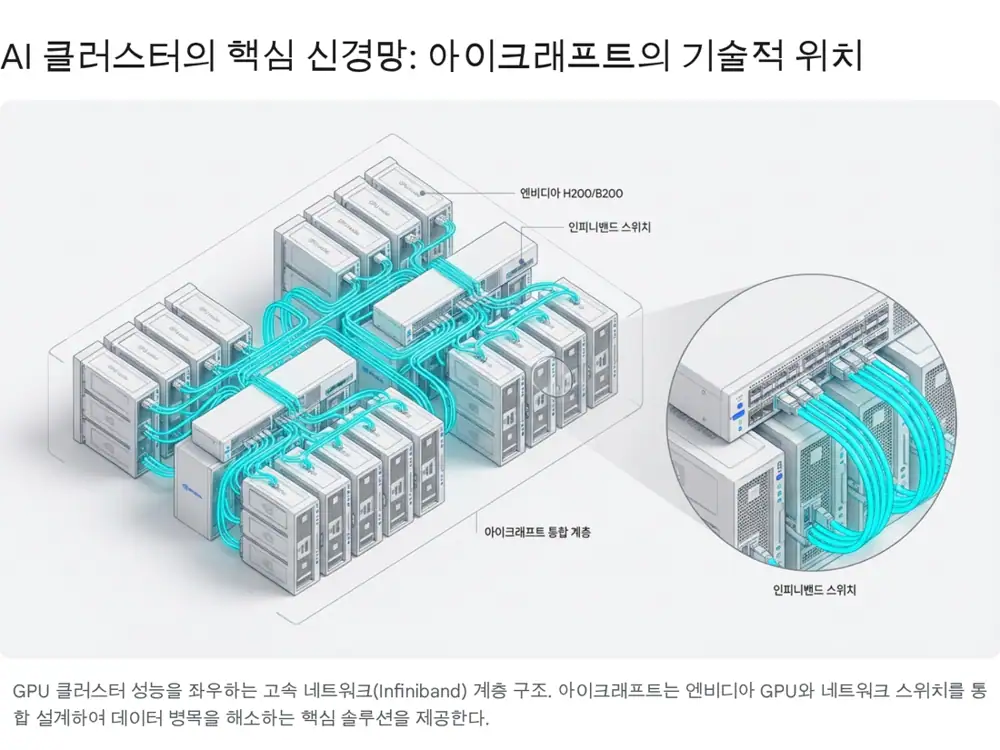

2. Moat: Nvidia Elite Partner and Infiniband design capability

- Nvidia Elite Partner: The source states that iCraft holds the top-tier Elite Partner status in Nvidia's partner program. In an AI-chip shortage, this status has strategic value because it can support allocation priority and delivery reliability.

- Infiniband capability: AI data-center performance depends heavily on GPU-to-GPU communication speed, not just individual GPU compute. Based on more than 20 years of telecom network work, iCraft is described as one of the few Korean companies able to design and optimize complex Infiniband architectures.

- Value-chain position: Nvidia's dominance can limit purchase-price negotiation, but Elite Partner status helps secure volume, while customers prioritize technical reliability and delivery over price.

3. Direct drivers of the fourth-quarter surge

The 4Q earnings surprise is interpreted as the result of large contracts concentrated in the second half of 2025, with equipment delivery and revenue recognition falling into the fourth quarter.

| Project | Size and period | Source interpretation |

|---|---|---|

| Kakao AI infrastructure build-out | KRW 35.5B, signed August 20, 2025, contract term through 2030 | AI infrastructure often has heavy initial hardware supply. The 70% advance-payment condition likely improved cash flow and enabled large equipment purchases. |

| Naver Cloud Infiniband supply | Roughly KRW 12.3-12.36B, December 8, 2025 to March 2, 2026 | The short contract window suggests equipment was ready and could be delivered quickly, with a meaningful portion likely recognized in 4Q. |

| Aswel AI consolidation | Stake acquisition in September 2025, then consolidated subsidiary | AI-training data processing and software solutions added higher-margin capability to the hardware-centered portfolio. |

Interpretation: Aswel AI matters strategically, not just for size. It extends iCraft from GPU hardware and Infiniband networks into data and solutions, creating a fuller AI-infrastructure value chain.

4. 2026 end market: Sovereign AI and Blackwell

260,000 GPUs

The source says the Korean government aims to secure about 260,000 GPUs by 2026 to become a top-three AI country.

B200 / GB200

Next-generation AI-chip supply is expected to ramp, with more than 2.5x training performance versus Hopper H100 and better energy efficiency.

Korean big tech

Naver's B200 cluster and SK Group / Hyundai Motor Group plans for 50,000 Nvidia GPUs are cited as demand drivers.

Sovereign AI is the push to build AI infrastructure reflecting a country's language, culture, regulations, and data sovereignty. The source expects both the national AI computing center and private data-center expansion to increase GPU server and network equipment demand across public and private customers.

Blackwell systems require liquid cooling and more complex interconnect technology. That increases the value of system-integration partners that can design, install, optimize, and maintain systems, rather than merely reselling equipment.

5. Q/P/C view of earnings sensitivity

| Variable | Source view | Impact on iCraft |

|---|---|---|

| Q: Quantity | Government-led sovereign AI and enterprise adoption of generative AI raise absolute GPU server demand. As GPU clusters grow, the number of Infiniband switches and cables rises rapidly. | Customer expansion beyond Naver and Kakao into finance and manufacturing supports structural unit growth. |

| P: Price | B200 is expected to be priced above H100, and related network equipment such as Spectrum-X is high-end. Greater system complexity can raise design, optimization, and technical-service fees. | Premium product mix and higher service fees can lift ASP. |

| C: Cost | Larger revenue scale reduces fixed-cost burden from labor and SG&A. FX remains a cost variable, but hedging and contract pass-through are discussed. | Fourth-quarter operating margin above 10% is interpreted as scale economy plus better software mix. |

6. Financial health and shareholder returns

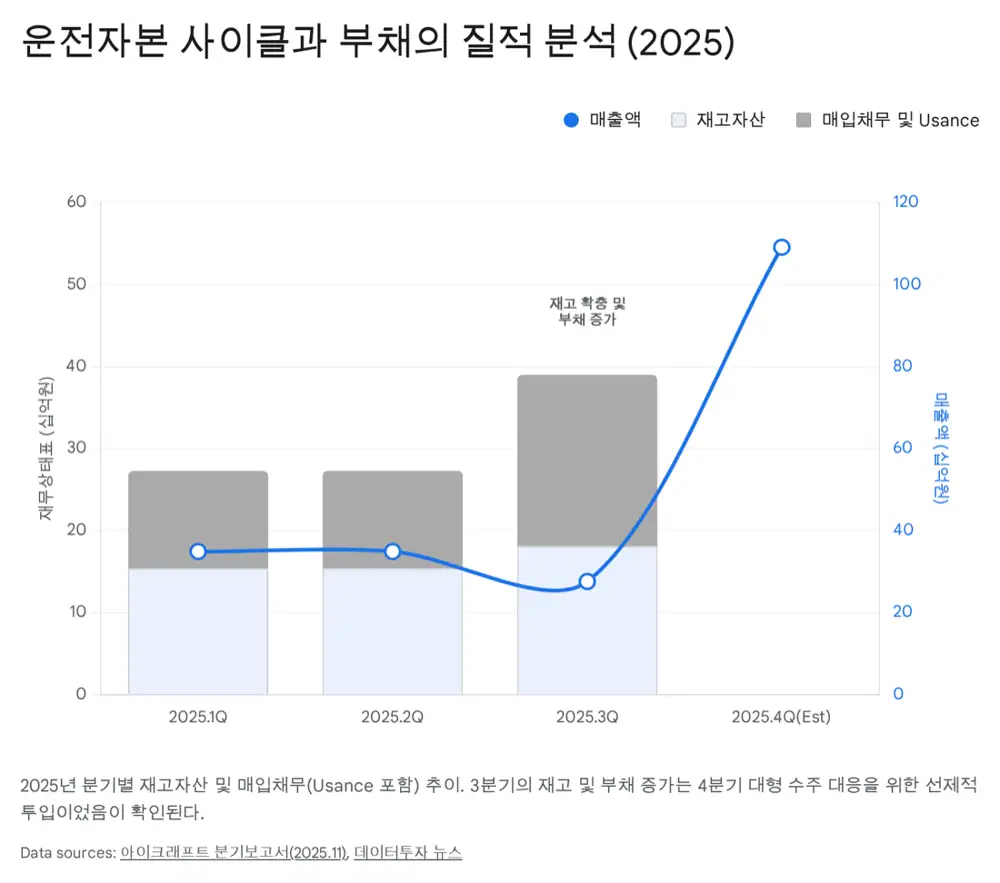

Debt ratios had increased as of the 3Q25 report, but the source views the quality of the debt as preparation for growth rather than a warning sign. Inventory of about KRW 18.0 billion at the end of 3Q was equipment secured for large 4Q revenue recognition, while payables and short-term borrowings were working capital for contracted revenue.

In 4Q, revenue recognition and large advance payments from customers such as Kakao likely improved cash flow. iCraft decided a KRW 100 per share cash dividend for 2025, with a 3.6% dividend yield and total dividend amount of roughly KRW 1.2 billion according to the source.

7. Valuation, risks, and my view

The source argues that iCraft should be valued not as a legacy NI company but as an AI-infrastructure solutions company. It cites domestic AI infrastructure and GPU-related peers such as XiiLab and MDS Tech at average PERs of 30-50x, and sees iCraft as undervalued at a market cap of roughly KRW 54.5 billion. Annualizing 4Q25 operating profit of KRW 11.4 billion implies nearly KRW 40 billion of operating-profit capacity, and even a conservative 2026 net-income assumption of KRW 15-20 billion would make the current share price difficult to explain, in the source's view.

- Revenue lumpiness: Large project-based orders can create major quarterly swings. The fourth quarter should not be assumed to repeat every quarter.

- Supply-chain risk: Blackwell yield problems or global supply delays could delay delivery and revenue recognition even when orders are secured.

- Overhang check: The source says no special issue is evident in the report, but CB, BW, or other potential selling supply should be monitored.

The source lands close to a Strong Buy conclusion. I am positive as well, but the sequence to verify is quarterly order disclosures, Blackwell supply schedule, Kakao and Naver Cloud remaining revenue recognition, Aswel AI consolidated margin, and inventory/payables turnover. The re-rating case depends on those five items continuing.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224177718390

- Data Tooza: 4Q consolidated operating profit KRW 11.4B: https://www.datatooza.com/article/20260209152203361752ef34a82f_80

- Etoday: Nvidia top-tier partner article: https://www.etoday.co.kr/news/view/2435542

- Data Tooza: Kakao KRW 35.5B supply contract: https://www.datatooza.com/article/20250820145406206352ef33541e_80

- DigitalToday: Naver Cloud KRW 12.36B network equipment supply: https://www.digitaltoday.co.kr/news/articleView.html?idxno=612401

- DigitalToday AI disclosure: Kakao AI computing resources project: https://www.digitaltoday.co.kr/aigongsi/1804/icraft-kakao-ai-computing-resource-contract

- Data Tooza: Naver Cloud KRW 12.3B supply contract: https://www.datatooza.com/article/20251211180310908152ef3e33c3_80

- KRX KIND: iCraft quarterly report: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20251114002744

- Korea Economic Daily: Brand authentication service: https://www.hankyung.com/article/2015102084856

- Korea Investment Securities PDF: iCraft research: https://file.truefriend.com/servlet/Download?file_path=/research/research10/&file_name=iCraft_NR_K_Final.pdf

- NVIDIA IR: South Korea AI infrastructure and ecosystem: https://investor.nvidia.com/news/press-release-details/2025/NVIDIA-South-Korea-Government-and-Industrial-Giants-Build-AI-Infrastructure-and-Ecosystem-to-Fuel-Korea-Innovation-Industries-and-Jobs/default.aspx

- ICN: Nvidia Blackwell and AI infrastructure market: https://icnweb.kr/2026/78905/%EB%B6%84%EC%84%9D-%EC%97%94%EB%B9%84%EB%94%94%EC%95%84-%EB%B8%94%EB%9E%99%EC%9B%B0-2026%EB%85%84-1-3%EC%A1%B0-%EB%8B%AC%EB%9F%AC-ai-%EC%9D%B8%ED%94%84%EB%9D%BC-%EC%8B%9C%EC%9E%A5/

- Korea JoongAng Daily: Naver 4,000 Blackwell GPU cluster: https://koreajoongangdaily.joins.com/news/2026-01-08/business/industry/Naver-builds-Koreas-largest-AI-cluster-using-4000-Nvidia-Blackwell-GPUs/2495755

- NVIDIA Newsroom: South Korea AI infrastructure: https://nvidianews.nvidia.com/news/south-korea-ai-infrastructure

- NVIDIA Newsroom: SK Group AI Factory: https://nvidianews.nvidia.com/news/sk-group-ai-factory

- DigitalToday: KRW 100 per common share cash dividend: https://www.digitaltoday.co.kr/news/articleView.html?idxno=628845

- Gukje News: MDS Tech and XiiLab Nvidia-related stocks: https://www.gukjenews.com/news/articleView.html?idxno=3115966

- Constellation Research: Nvidia Q3 and Blackwell constraints: https://www.constellationr.com/insights/news/nvidia-strong-q3-sees-hopper-blackwell-shipping-q4-some-supply-constraints