DEEP RESEARCH · ICRAFT

iCRAFT: From Legacy Networking to AI Infrastructure Backbone

A research note on the InfiniBand moat, 3Q25 growing pains, and working-capital risk

0. Bottom line first

iCRAFT is shifting from network integration into an AI infrastructure partner built around Nvidia/Mellanox InfiniBand. Naver and Kakao references are meaningful, but usance debt, inventory, and FX exposure mean sales growth alone is not enough.

AI cluster networking

InfiniBand links between GPUs can determine AI training ROI.

KRW 74.1bn

Backlog at end-September 2025 is presented as revenue cover for more than two to three quarters.

KRW 5.28bn usance

USD 3.76mn at TERM SOFR + 1.1% creates short-term trade-finance pressure.

1. Corporate evolution: from backbone networks to AI infrastructure

Official fact: The source says iCRAFT was founded on January 21, 2000, built core and access networks for carriers such as KT and SK Broadband, and listed on KOSDAQ in January 2005.

Interpretation: Routing optimization and large-traffic handling experience can transfer into AI cluster network design. The company’s adoption of Nvidia/Mellanox solutions from 2020 marks the start of the transition.

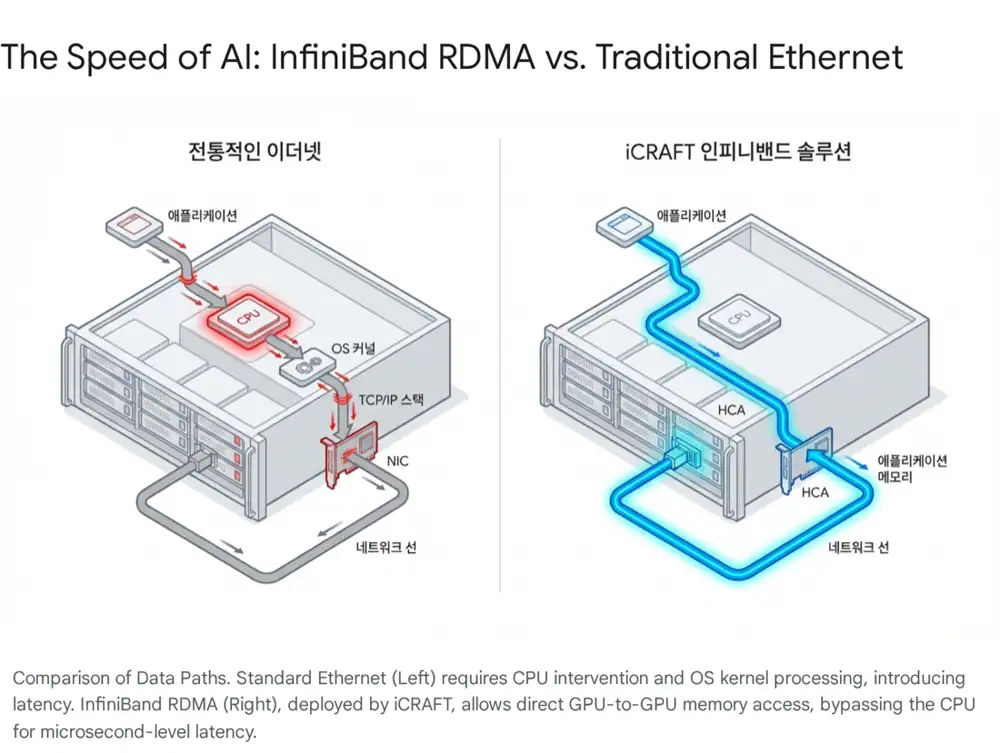

2. Technology moat: InfiniBand versus Ethernet

AI training requires thousands or tens of thousands of GPUs to exchange parameters. If networking lags, GPUs wait idle for data, and network bottlenecks determine the return on the whole infrastructure investment.

- InfiniBand provides a lossless architecture through credit-based flow control.

- RDMA lets the network card access remote server memory directly, bypassing CPU and OS paths.

- The source compares Ethernet latency at 10-50 microseconds with InfiniBand at 0.5-2 microseconds, implying more than a 10x reduction.

- Modern InfiniBand switches can perform in-network computing such as aggregation and reduction through SHARP.

- RoCE v2 Ethernet has cost and compatibility advantages, but PFC, ECN, and other tuning complexity remain risks.

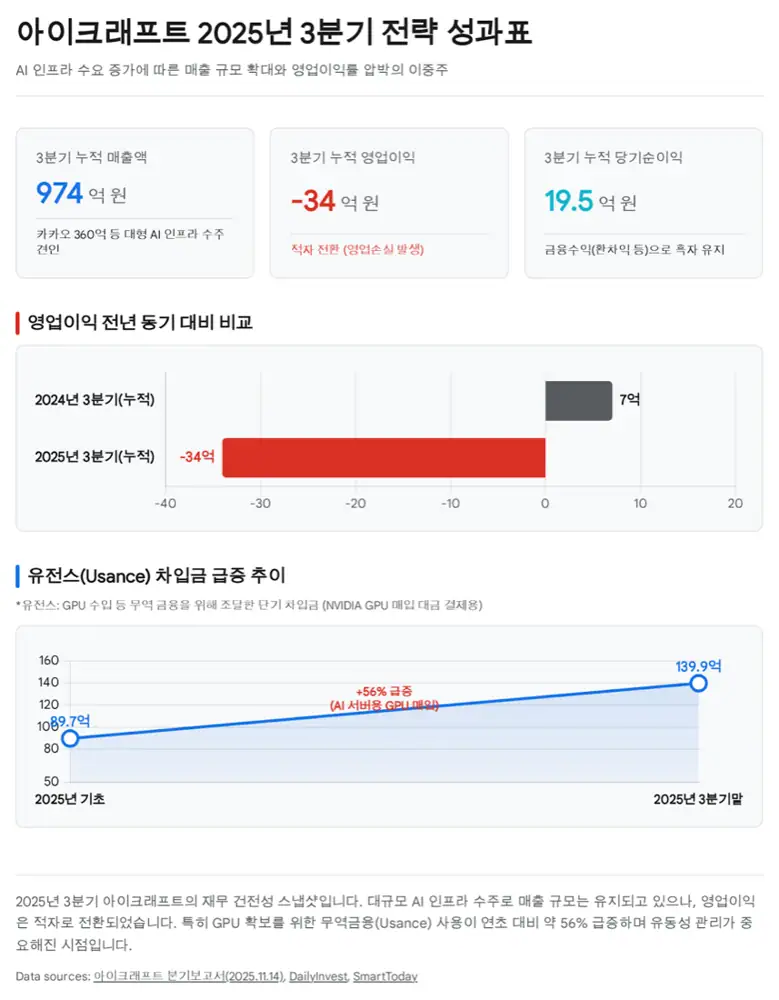

3. 3Q25: growth with margin strain

Official fact: The source summarizes the 3Q25 report as showing both revenue growth and profitability deterioration. Large AI infrastructure contracts with Kakao and Naver Cloud created references, while a high hardware-resale mix can pressure margins.

| Item | Source figure | Meaning |

|---|---|---|

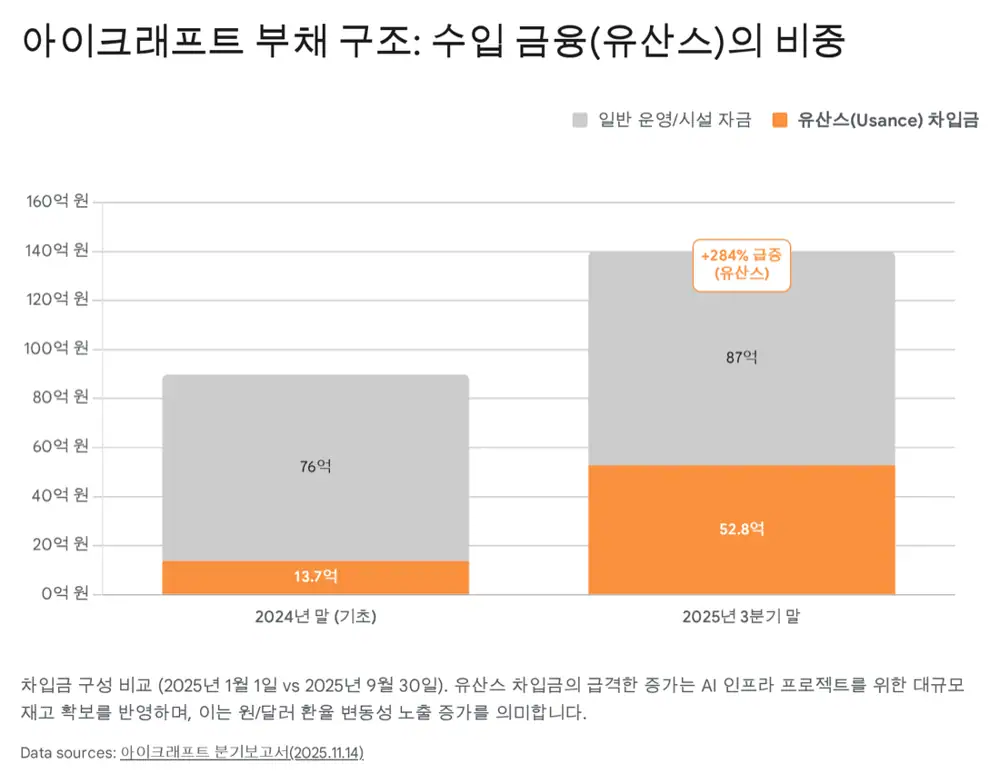

| Usance debt | About KRW 5.28bn, USD 3.76mn | Nearly 4x increase from the beginning balance |

| Rate | TERM SOFR + 1.1% | U.S. high-rate and dollar-liability burden |

| Inventory | KRW 18.08bn | Up about 17% from KRW 15.44bn |

| FX sensitivity | 10% move affects pretax profit by about KRW 1.25bn | Risk from buying in USD and selling in KRW |

| Backlog | KRW 74.1bn | Revenue visibility as of end-September 2025 |

| PBR | Around 0.84x | Undervaluation thesis versus technical assets |

Interpretation: Rising usance debt may indicate imported equipment from overseas vendors such as Nvidia has not yet been fully converted into customer cash receipts. The larger revenue gets, the more working-capital control matters.

4. Subsidiaries and portfolio

Maintenance cash cow

A wholly owned subsidiary handling network maintenance and system implementation.

Questionable fit

E-commerce and content production sit away from the infrastructure core.

High-margin option

An anti-counterfeit solution that the source says once had operating margin above 30%.

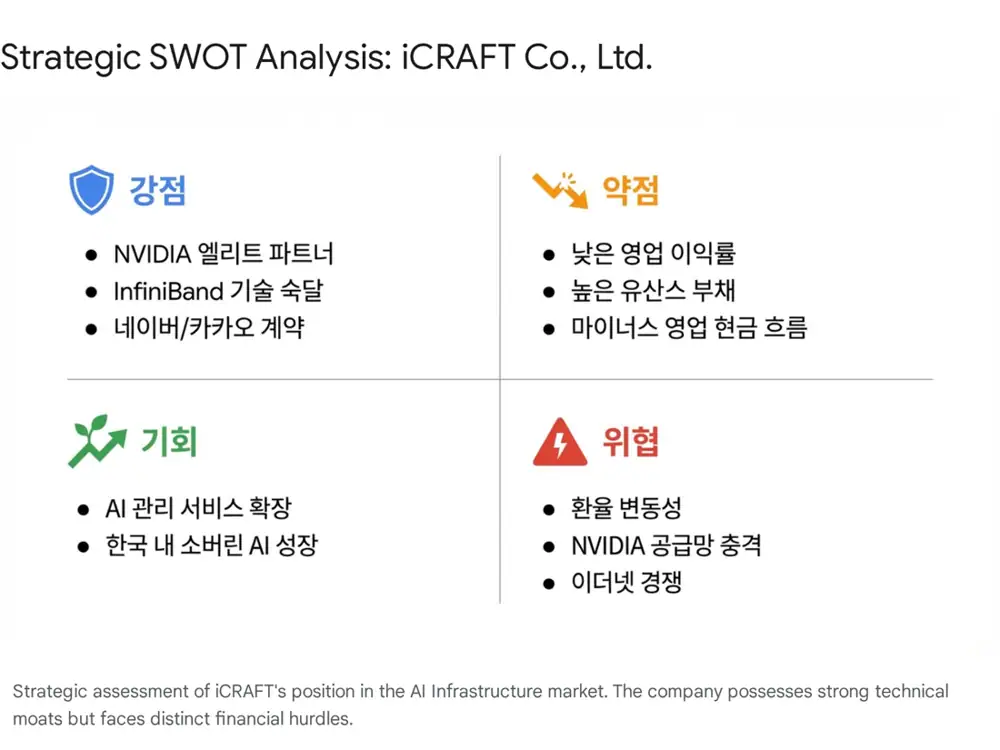

5. Investment points and risks

- Essential AI infrastructure: in the race for Nvidia GPUs, InfiniBand networking is close to mandatory.

- Clear references: large customers such as Kakao and Naver support credibility.

- Cash-flow check: usance repayment, inventory monetization, and positive operating cash flow matter.

- Margin defense: the company needs more technical support and consulting revenue, not just hardware resale.

- FX: a stronger USD raises procurement costs and dollar-debt repayment burden.

My conclusion is that the growth story is valid, but the stock trigger is not revenue alone. It is operating cash flow and margin recovery.

Sources

- Naver original post

- iNews24 interview

- Naver company research PDF

- UfiSpace InfiniBand vs Ethernet

- Juniper AI data center white paper

- WWT AI networking blog

- Medium InfiniBand analysis

- Lightyear Ethernet vs InfiniBand

- Bloter on Mellanox intelligent interconnect

- FiberMall Mellanox InfiniBand guide

- Vitex InfiniBand vs Ethernet for AI clusters

- DailyInvest Kakao KRW 36bn contract

- Bloter Kakao KRW 35.6bn contract

- DailyInvest Naver Cloud KRW 11bn contract

- The Report on Nvidia GPU supply contract

- Chosun Biz on iCRAFT share move

- iCRAFT research PDF

- Judal iCRAFT analysis