DEEP RESEARCH · JINKOSOLAR

JinkoSolar: Pragmatism Built on TOPCon Plus Perovskite

A 2035 strategy view across 34.76% tandem efficiency, AI-driven R&D, and the Saudi 10GW base

0. Bottom line first

JinkoSolar’s strategy is not a reckless technology leap. It is a capital-efficient path that stacks perovskite tandem technology on top of proven N-type TOPCon capacity. Weak 2025 profitability is a real burden, but the 34.76% efficiency record and the Saudi 10GW project make the long-term option clear.

34.76%

A NPVM-verified N-type TOPCon-based perovskite tandem-cell result.

TOPCon reuse

Existing large-scale TOPCon lines become a bridge into tandem production.

Saudi 10GW

A USD 1bn high-efficiency cell and module plant with RELC and Vision Industries.

1. Technology inflection: tandem after silicon limits

Official fact: The source cites the Shockley-Queisser limit for single-junction silicon cells at about 29.4% and describes perovskite-silicon tandem cells as having theoretical efficiency above 43%.

Interpretation: JinkoSolar is insisting on TOPCon rather than HJT as the bottom cell. That looks like a strategic choice to reuse existing assets and supply chains, not just a pure efficiency bet.

2. Efficiency record and competitive map

| Company | Technology route | Best efficiency | Date | Strategic feature |

|---|---|---|---|---|

| JinkoSolar | N-type TOPCon | 34.76% (NPVM) | 2025.12 | TOPCon-line reuse and AI-based materials development |

| LONGi | Silicon-perovskite, estimated HJT | 34.85% (NREL) | 2025.04 | Efficiency maximization and diversified technology portfolio |

| Hanwha Qcells | Q.ANTUM-based | 28.6%, commercial area | 2025.01 | Focus on commercial-area manufacturability |

Interpretation: LONGi’s small-area record and Hanwha Qcells’ commercial-area result mean different things. JinkoSolar’s point is that TOPCon can still support world-class tandem efficiency.

3. Value-chain integration: AI R&D and equipment ecosystem

The source reads JinkoSolar’s XtalPi collaboration as a way to reduce uncertainty in perovskite materials development. If Hanwha Qcells is closer to open innovation with specialist tool makers such as YAS, JinkoSolar appears closer to internalizing process recipes through AI collaboration and China’s domestic equipment ecosystem.

- No direct JinkoSolar-YAS equipment contract is confirmed in the source.

- Maxwell is discussed as both a potential supplier and a competitive axis in HJT and tandem equipment.

- JinkoSolar appears to be combining Chinese equipment supply chains with customized process development to maximize cost competitiveness.

4. Saudi 10GW project and global manufacturing 2.0

Official fact: The source says JinkoSolar is building a 10GW high-efficiency cell and module plant worth USD 1bn with RELC, a subsidiary of Saudi Arabia’s PIF, and Vision Industries. The ownership structure is JinkoSolar 40%, RELC 40%, and VI 20%.

Interpretation: Initial production may focus on N-type TOPCon, but Saudi Arabia’s high-irradiance, high-temperature environment is a strong testbed for tandem modules and a platform for MENA expansion.

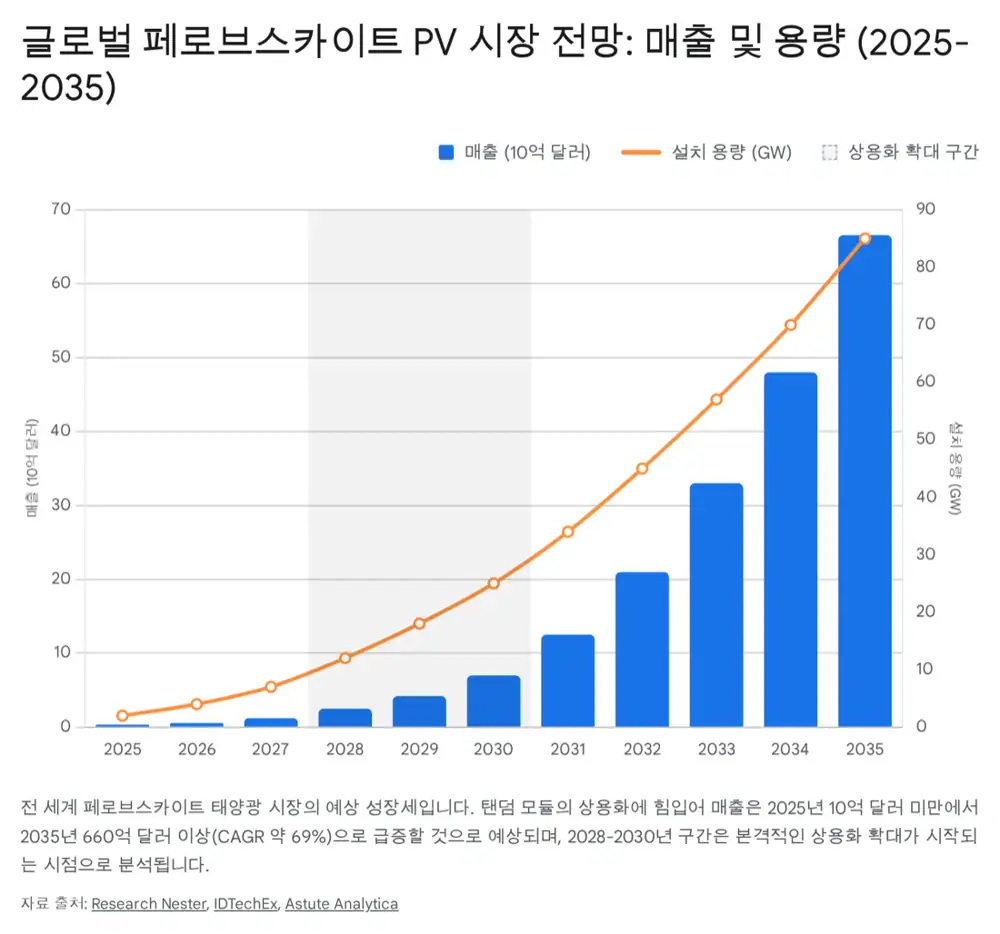

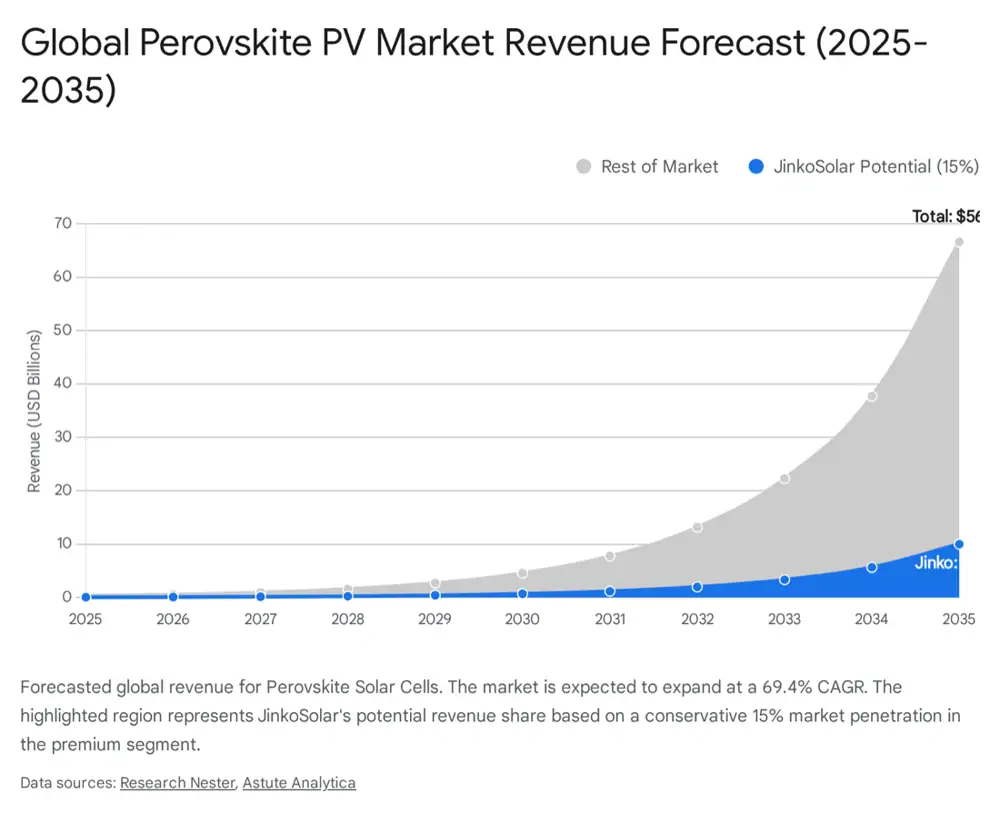

5. Market size and financial frame

- The source cites perovskite market estimates of about USD 342mn in 2025, USD 7bn in 2030, and USD 66.58bn in 2035.

- Annual installations are presented at about 85GW by 2035, with a CAGR near 69.4%.

- If JinkoSolar keeps 15% share in 2035, the source estimates about 12.75GW of shipments and USD 3bn-5bn in additional revenue.

- 2025 is framed as “profitless prosperity”: shipments near 100GW but potential net losses from severe price competition.

- The source projects net income of about RMB 1.14bn in 2026 and RMB 3.38bn in 2027.

- The current 0.1x P/S ratio is read as deeply discounted versus an industry average of 1.7x.

My key monitoring items are XtalPi pilot-line yield stabilization, Saudi utilization and profitability, and IEC/UL certification for tandem modules.

Sources

- Naver original post

- PV Magazine on JinkoSolar 34.76% tandem efficiency

- Perovskite-info on JinkoSolar 34.76%

- LONGi 34.85% release

- KED on Hanwha Q Cells tandem mass production

- JinkoSolar 33.24% release

- JinkoSolar 34.76% company release

- ECS on titanium lead-free perovskites

- Perovskite-info on titanium-based lead-free PV

- PV Magazine Australia on JinkoSolar partnership

- PV Magazine on JinkoSolar partnership

- Perovskite solar market analysis, Google Drive

- Etoday on YAS and Hanwha patent

- PV Tech on JinkoSolar ITC case

- Perovskite-info on Maxwell order

- EnergyTrend survey reports

- JinkoSolar Saudi joint venture release

- Research Nester market forecast

- IDTechEx perovskite PV report

- Astute Analytica market report

- JinkoSolar investor file

- JinkoSolar 2Q and 3Q 2025 results

- Seeking Alpha JKS estimates

- Simply Wall St JinkoSolar valuation

- Simply Wall St JinkoSolar future growth

- Morningstar preliminary 2025 results notice