DEEP RESEARCH · OCI Holdings

OCI Holdings: From commodity chemicals to advanced energy materials

PERC → TOPCon → perovskite tandem: what grows, what is new, and what fades

0. Bottom line first

The move to perovskite-silicon tandem is more than a technology step — it is a full BOM rewrite. For OCI Holdings: ① 11N-grade polysilicon premium for N-type, ② new perovskite precursor markets (PbI₂, FAI, MABr), ③ a surge in silane (SiH₄) specialty gas, ④ rising share of indium TCOs and POE encapsulants. The non-China ‘Malaysia → Vietnam → US’ stack is a powerful moat under IRA and UFLPA.

1. The technology inflection

PERC is saturating near its theoretical efficiency limit of 24%. The industry is accelerating into N-type TOPCon/HJT, and ultimately perovskite-silicon tandem with silicon as the bottom cell. The added stack — perovskite, ETL, HTL, TCO on top — drives demand for higher-functionality materials. ETIP PV SRIA Update

2. Polysilicon — quality, not just quantity

2.1 P-type → N-type

PERC used boron-doped P-type with LID and tolerance limits. TOPCon/HJT use phosphorus-doped N-type — high electron mobility but extreme purity sensitivity, requiring electronic-grade ≥11N polysilicon. Solar-grade P-type tolerates 10–50 ppbw of metal impurities; N-type needs ≤1–5 ppbw. Market data: in 2024–25 N-type polysilicon commands an ~USD 1.5–3.0/kg premium over P-type. OCI’s Malaysia base captures both a non-China premium and N-type premium. Coherent Market Insights, SMM, OPIS Solar Weekly

2.2 Material intensity (g/W)

- PERC (P-type): ~2.4–2.6 g/W

- TOPCon (N-type): ~2.0–2.2 g/W

- Perovskite/Si tandem: ~1.6–1.8 g/W

Interpretation: Higher efficiency (22% → 33%) plus wafer thinning (170 → 100–130μm) cuts polysilicon per GW from ~2,400 to ~1,600 tonnes (~33% less). Global demand is shifting to TW scale, however, so OCI’s volumes don’t fall — the mix moves from ‘low-purity high-volume’ to ‘high-purity high-value.’

2.3 CubicPV partnership and ‘direct wafer’

OCI Holdings signed a USD 1B long-term supply contract with US CubicPV. CubicPV’s ‘direct wafer’ technology skips ingot growth and sawing — drastically reducing kerf loss (~30–40% in standard sawing). If this becomes a tandem-scale standard, OCI becomes a tech partner — not just a raw-material supplier. KED Global, Business Wire.

3. New and growing materials — OCI’s opportunity

3.1 Perovskite precursors — the ‘new light-absorbing heart’

- PbI₂ / PbBr₂: central to crystal formation. Today small-volume suppliers like TCI and Greatcell exist, but at GW scale, ton-scale industrial supply will be needed — OCI’s lane.

- Organic cations (FAI, MABr): determine thermal stability; ≥5N purity required. Explosive growth ahead. TMR — FAI

- Functional solvents: DMF/DMSO today, but toxicity drives demand for greener alternatives — an OCI R&D opportunity. TCI — Solar Cell Materials, RSC — bottom cell design, ACS — Titanium silicide recombination layer

3.2 Transparent conductive oxides (TCO) — indium surge

- Tandem requires the top cell to let light through to the bottom cell — metal grids replaced by TCOs.

- Main material: ITO. Indium demand spikes.

- PERC: <1 mg/W indium. HJT / tandem: ~15–20 mg/W (tens of times more). Price risk + accelerates AZO substitution research.

3.3 Specialty gases — silane (SiH₄) returns

Essential for TOPCon poly-Si layers and HJT/tandem a-Si thin films. OCI is expanding its silane gas facility in Gunsan — triple-demand from semiconductors, EV silicon anodes and solar. Inox Air Products, OCI Integrated Report 2024

3.4 Encapsulants — EVA → POE

- EVA hydrolyzes and releases acetic acid — corrodes moisture-sensitive perovskite. Not fit-for-purpose.

- POE (polyolefin elastomer) has low water permeability and no acid — fast becoming the standard for N-type and tandem modules.

- POE/EPE share went from ~30% in 2023 to projected >50% by 2030. OCI’s carbon-chemicals unit can extend into raw materials / films. TERLI, TaiyangNews

4. Shrinking / disappearing materials

- Aluminum paste: used for PERC back BSF. With N-type adoption, top of the ‘sharply declining’ list.

- Commodity P-type polysilicon: 6N–9N grade losing ground — a positive for OCI as low-end Chinese supply demand shrinks while high-purity demand concentrates.

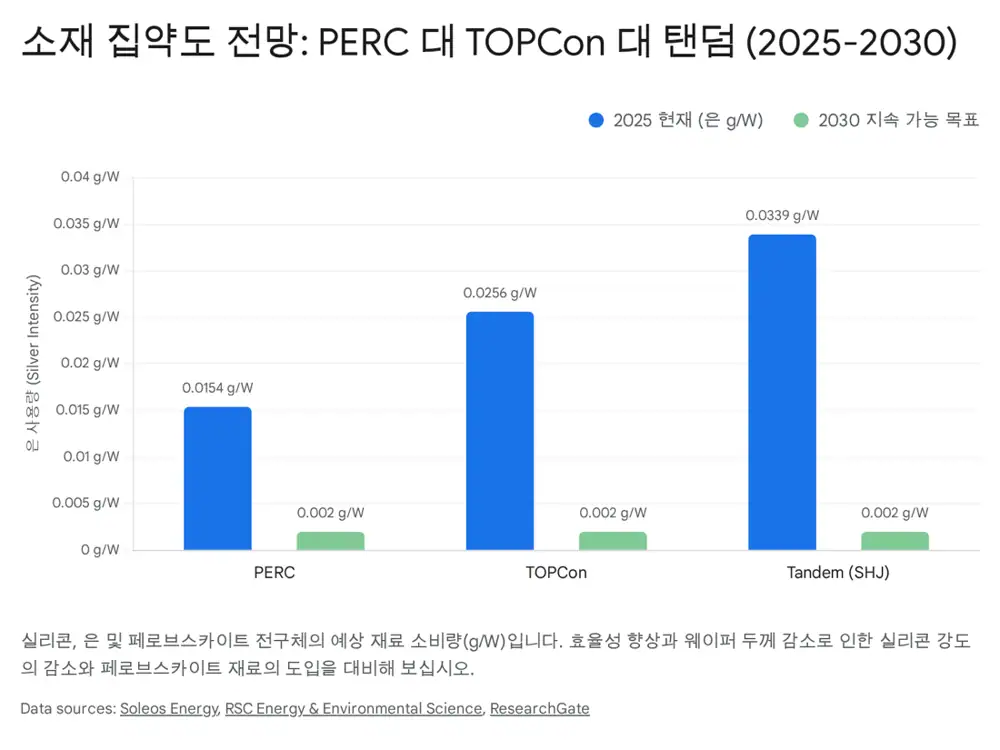

5. Bottleneck — the silver dilemma

- PERC used silver only on the front (~10 mg/W). TOPCon uses both sides; low-temperature paste needs more silver — early tandem/HJT cells hit 20–25 mg/W.

- Response: SMBB (super multi-busbar) thin-electrodes and copper plating as silver substitutes. TaiyangNews — Silver savings

- Outlook: near-term rise, mid-/long-term flat-to-down. OCI doesn’t make silver, but silver spikes raise module prices and choke market growth — critical for OCI’s downstream.

6. OCI strategic response

6.1 Semiconductor-solar convergence

OCI is shifting weight toward semiconductor materials. It can look like solar retrenchment, but tandem manufacturing increasingly resembles semiconductor processes (thin-film deposition, precision cleans, etching). Capabilities developed for semi-grade HCDS, phosphoric acid and hydrogen peroxide directly translate into tandem material competitiveness. OCI R&D, OCI IR deck

6.2 Non-China supply-chain moat

The US IRA and UFLPA exclude Xinjiang polysilicon — OCI’s hydro-powered Malaysian polysilicon enjoys a near-‘free pass’ in the US market. Add the Vietnamese wafer JV and Texas Mission Solar module expansion, and OCI completes a Malaysia (polysilicon) → Vietnam (wafer) → US (cells/modules) non-China vertical chain. PV Tech — Vietnam wafer, PV Magazine — 2.7GW factory

6.3 R&D and new businesses

The CubicPV partnership upgrades OCI from supplier to innovation partner. Existing chemistry strengths give OCI optionality to extend into tandem precursors and encapsulant raw materials/films.

7. Summary — material-by-material outlook

| Category | Material | Direction | 2025 → 2030 | OCI impact |

|---|---|---|---|---|

| Core | Polysilicon (N-type) | g/W down, price up | 2.2 g/W → 1.8 g/W (9N → 11N required) | Positive. High-purity premium + non-China moat. |

| Metal electrode | Silver paste | Spike then decline | 13–16 mg/W → 8–10 mg/W | Neutral. Cost risk; monitor copper plating. |

| New | Perovskite precursors (PbI₂, FAI, …) | New market | 0 → 10–50 t/GW (est.) | Opportunity. OCI specialty chemicals can enter. |

| Encapsulant | POE (polyolefin) | Share expansion | 30% → >55% share | Opportunity. OCI carbon-chemicals into raw materials / films. |

| TCO | Indium / ITO | Sharp rise | <1 mg/W → 15–20 mg/W | Watch. Raw-material supply risk. |

| Specialty gas | Silane (SiH₄) | Demand up | Persistent growth | Positive. Triple-demand from semi, battery, solar. |

| Exit | Aluminum paste | Sharp decline | Phases out with PERC | No impact. Not a core OCI product. |

The tandem transition is not just a technology shift — it is a qualitative supercycle for OCI Holdings. With semi-grade process capability and a geopolitical position aligned with US policy, OCI is entering its leap from commodity chemicals to a global advanced energy-materials company.

Sources

- Naver blog source: m.blog.naver.com/.../224176190000

- Coherent Market Insights — polysilicon role: coherentmarketinsights.com

- Shanghai Metals Market — N-type prices: news.metal.com

- OPIS Solar Weekly: opis.com PDF

- TaiyangNews — Silver savings: taiyangnews.info

- ETIP PV — SRIA Update 2024: etip-pv.eu

- KED Global — OCI / CubicPV $1B: kedglobal.com

- Business Wire — CubicPV / OCI: businesswire.com

- TCI — Solar Cell Materials brochure: tcichemicals.com

- Transparency Market Research — FAI: transparencymarketresearch.com

- RSC — bottom cell design (terawatt): pubs.rsc.org

- ACS — titanium silicide recombination layer: pubs.acs.org

- OCI Integrated Report 2024: PDF

- Inox Air Products — Solar gases: inoxairproducts.com

- TERLI — EVA vs POE vs Silicone: terli.net

- TaiyangNews — EVA → EPE: taiyangnews.info

- OCI R&D page: oci.co.kr

- OCI IR deck: PDF

- PV Tech — OCI Vietnam wafer: pv-tech.org

- PV Magazine — 2.7GW factory operations: pv-magazine.com