DEEP RESEARCH · LONGi Green Energy

LONGi Green Energy Analysis: Perovskite Tandem Roadmap and Next-Generation Solar Leadership

A review of 34.85% tandem efficiency, the HPBC/Maxwell ecosystem, and the 2026-2035 commercialization path.

0. Bottom line first

I see LONGi less as a simple module manufacturer and more as a bet on the post-silicon efficiency standard. The source’s core question is whether 34.85% NREL-certified efficiency can justify long-term rerating despite oversupply and margin pressure.

34.85%

The source presents this as the NREL-certified world-record efficiency for a two-terminal perovskite/silicon tandem cell as of April 2025.

BC and tandem dual strategy

LONGi uses HPBC/BC modules for today’s premium market and prepares them as bottom cells for future tandem products.

Durability and trade barriers

Twenty-five-year-plus lifetime validation and geopolitical rules such as UFLPA, the OBBB Act, and CBAM are the key risks.

1. Investment thesis: efficiency beyond the S-Q limit

Official fact: The source states that in April 2025 LONGi achieved 34.85% conversion efficiency in a two-terminal perovskite-silicon tandem cell and received NREL certification. This is more than five percentage points above the 29.4% theoretical limit cited for silicon solar cells.

Conventional single-junction silicon cells have an approximately 1.12eV bandgap, so high-energy photons are lost as heat and lower-energy photons pass through. The source’s starting point is that commercial TOPCon and HJT are saturating around 26% efficiency.

2. Efficiency records and technical innovation

| Company/institute | Technology | Efficiency | Date | Note |

|---|---|---|---|---|

| LONGi | Perovskite/Si Tandem 2T | 34.85% | 2025.04 | NREL certified, world record |

| LONGi | Perovskite/Si Tandem 2T | 33.9% | 2023.11 | Prior world record; source says it first exceeded a 33.7% S-Q limit |

| LONGi | Flexible Tandem | 33.4% | 2025.11 | Flexible-substrate world record, published in Nature |

| LONGi | Commercial Wafer M6 | 30.1% | 2024.06 | First 30% breakthrough at commercial 260cm² size |

| JinkoSolar | N-type TOPCon Tandem | 33.24% | 2024 | TOPCon bottom-cell architecture |

| Hanwha Qcells | Perovskite/Si Tandem | 29.3% | 2023 | Pilot-line validation focus |

| Oxford PV | Perovskite/Si Tandem | 28.6% | 2023 | Commercial M4 module basis |

Official fact: The source describes interface engineering as LONGi’s core innovation. The asymmetric carbazole-based self-assembled monolayer HTL201 adheres more densely to textured silicon surfaces and optimizes energy-level alignment.

- Asymmetric SAM: described as reducing non-radiative recombination and helping push open-circuit voltage close to 2.0V.

- Bilayer passivation: a LiF ultrathin layer plus diammonium diiodide molecules aims to improve electron extraction and heal surface defects.

- HPBC bottom cell: the back-contact structure reduces front-electrode shading and helps tandem current matching.

Interpretation: The 34.85% result is not just something achieved by buying better equipment. It reflects materials, interfaces, voltage-loss control, and bottom-cell design working together, which is where the lead over followers can come from.

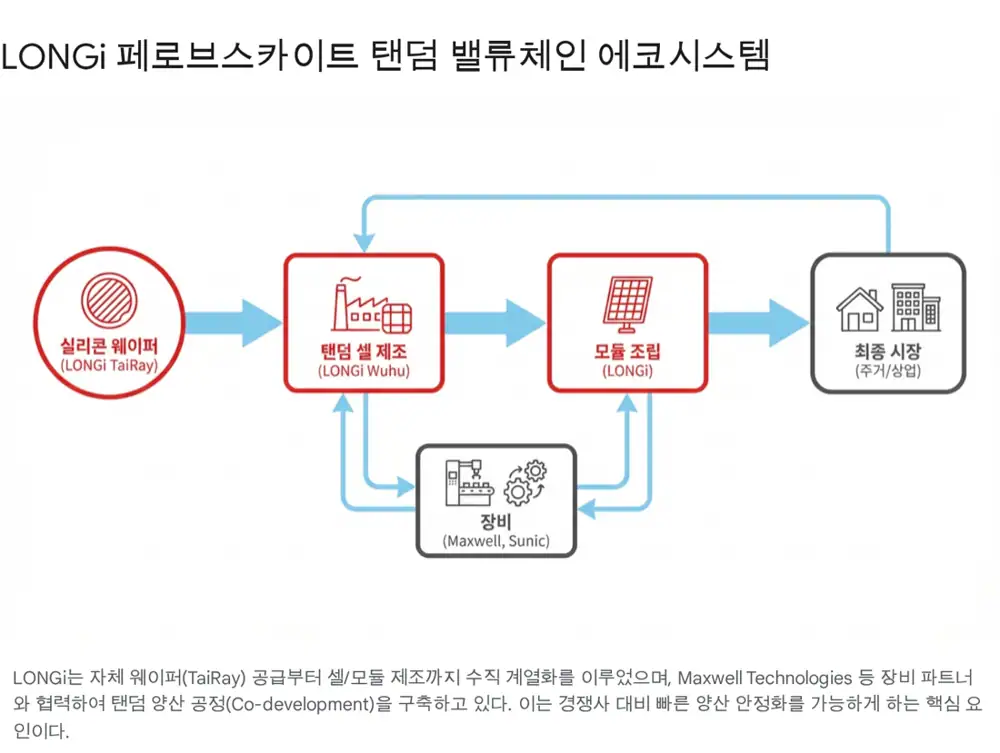

3. Lab-to-Fab: value chain and industrialization

The source says the hardest and most expensive step is turning lab records into factory products. LONGi is trying to cross that valley of death by linking wafers, cells/modules, and equipment partners.

| Stage | Source highlight |

|---|---|

| Upstream | TaiRay wafers for thermal stability, oxygen control, and reduced crystal defects |

| Materials | Perovskite precursors and TCO combine internal R&D with external sourcing, including organic-material cooperation with Chinese chemical companies |

| Midstream | Wuhu, Anhui production base with pilot lines for GW-scale manufacturing and large-area coating optimization |

| Large-area process | M6/M10 commercial sizes require slot-die coating or vacuum deposition; June 2024 M6 30.1% suggests a manufacturable recipe |

| Equipment | Co-development with Maxwell Technologies for PVD, ALD, and large-area inkjet printing |

| Pilot | Maxwell is described as completing large-area deposition prototypes by late 2024 and supplying 100MW pilot-line equipment in 2025 |

Interpretation: LONGi’s edge is not only cell efficiency, but simultaneous control of wafer, coating, deposition, and equipment ecosystems that determine yield. The possible use of OLED deposition know-how from companies such as Sunic System fits this frame.

4. Market size and LONGi revenue potential

Official fact: The source cites a 30-70% CAGR range for the perovskite solar-cell market. Its aggressive 2035 scenario is about $66.58 billion, roughly KRW 90 trillion, while its conservative scenario is about $24.19 billion, roughly KRW 32 trillion.

| Technology | 2025 | 2027 | 2030 | 2035 | Note |

|---|---|---|---|---|---|

| TOPCon | 50% | 65% | 60% | 40% | Current standard |

| PERC | 40% | 20% | 5% | <1% | Phase-out |

| HJT | 9% | 12% | 20% | 25% | High-efficiency niche |

| Tandem | <1% | 3% | 15% | 35% | Rapid-growth forecast |

| Market feature | R&D/pilot | Premium launch | Manufacturing competition | Standard replacement | Source forecast |

- Penetration: the source expects about 2-5% of the total solar market by 2030 and potentially 15-30% by 2035.

- Initial markets: European and U.S. residential rooftops plus C&I markets where installation area is constrained.

- Module value: more than 20% higher generation from the same area supports premium pricing where BOS costs are high.

- 2030 model: 50GW global tandem demand, 25% LONGi share, and $0.20/W ASP imply about $2.5 billion, or KRW 3.4 trillion, of revenue.

- 2035 model: with 100GW+ demand and maintained share, revenue is presented at $5-8 billion and more than 20% of LONGi’s total revenue.

5. Competition, financial impact, and catalysts

Reliability and U.S. channel

Jincheon 40MW pilot line, mass production targeted by end-2026. Efficiency is in the 29.3-30% range, but U.S. residential distribution is strong.

TOPCon extension

33.24% tandem using an N-type TOPCon bottom cell. The strategy is a gradual transition using existing TOPCon lines.

Commercialization lead

The Brandenburg, Germany plant is closer to commercialization, but scale is limited versus large manufacturers like LONGi.

Official fact: The source puts LONGi’s annual wafer capacity at more than 100GW. It also states that 2024 R&D investment exceeded RMB 5 billion, about KRW 950 billion, or roughly 6% of revenue.

| Item | Source checkpoint |

|---|---|

| Economic moat | SAM materials, interface control, dual-junction design, and 100GW+ wafer scale |

| Margin outlook | Potential return to 15-20% high-margin structure after tandem commercialization from 2027 |

| Near-term catalysts | 2025-2026 successful 100MW+ pilot-line operation and first commercial prototype |

| Mid-term catalysts | 2027-2028 IEC/TÜV long-term reliability tests and GW-scale production investment announcements |

Interpretation: The source concludes with a long-term Strong Buy view, but I would translate that into a technology milestone checklist. Efficiency, lifetime, large-area scaling, and reliability certification all need to pass before 34.85% turns into enterprise value.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224176189009

- Source 2: https://drive.google.com/open?id=1blsYYP2hzahpUaSamBnWt2CbrpWiauE459Iz7NT_kxg

- Source 3: https://www.fluxim.com/research-blogs/perovskite-silicon-tandem-pv-record-updates

- Source 4: https://www.longi.com/en/news/2024-snec-silicon-perovskite-tandem-solar-cells-new-world-efficiency/

- Source 5: https://www.longi.com/en/news/longi-2024-annual-report/

- Source 6: https://www.longi.com/en/news/breakthroughs-in-hibc-and-flexible-silicon-based-tandem-solar-cells-nature/

- Source 7: https://www.pv-tech.org/industry-updates/maxwell-unveils-perovskite-hjt-tandem-cell-manufacturing-solution-at-snec2025/

- Source 8: https://www.perovskite-info.com/maxwell-secures-full-line-order-perovskiteshj-tandem-cell-solution

- Source 9: https://static.longi.com/LON_Gi_Interim_Report_2025_94f8752606.pdf

- Source 10: https://www.pv-tech.org/industry-updates/longi-included-in-2026-bloomberg-green-watchlist-for-leading-esg-project/

- Source 11: https://www.longi.com/en/news/is-m6-wafer-silicon-perovskite-tandem-cells-new-efficiency-record/

- Source 12: https://www.longi.com/en/news/nature-and-science-research-of-tandem-solar-cell/

- Source 13: https://www.longi.com/en/news/2023-longi-facing-new-industrial-cycle/

- Source 14: https://cordis.europa.eu/project/id/101084251

- Source 15: https://www.longi.com/en/news/silicon-perovskite-tandem-solar-cells-new-world-efficiency/

- Source 16: https://www.researchnester.com/reports/perovskite-solar-cell-market/6346

- Source 17: https://www.astuteanalytica.com/industry-report/perovskite-solar-cells-market

- Source 18: https://www.cervicornconsulting.com/tandem-solar-cell-market

- Source 19: https://static.longi.com/LON_Gi_annual_report_2024_0026f3477f.pdf

- Source 20: https://simplywall.st/stocks/cn/semiconductors/shse-601012/longi-green-energy-technology-shares/future