DEEP RESEARCH · YAS

YAS: From OLED Deposition Equipment to Perovskite Tandem Tools

A research note on large-area vacuum deposition, technical moat, and 2026-2035 re-rating potential

0. Bottom line first

My core view is that YAS should not be reduced to an OLED equipment cycle stock. It is one of the few companies with production-level experience in large-area vacuum deposition. If LG Display capex returns and perovskite tandem cells adopt dry deposition, the sub-1x PBR discount could narrow.

Linear source

The LNS that forms uniform films on Gen-8-plus substrates is the main moat.

OLED + solar

LGD OLED upgrades and tandem-cell investment by players such as Hanwha Qcells are the key triggers.

Discount case

Low PBR versus Sunic System and a debt ratio in the 3% range support the re-rating thesis.

1. Corporate identity: a deposition-physics equipment company

Official fact: The source says YAS has a record of commercializing OLED deposition equipment for Gen-8 class and larger substrates, including 2200mm x 2500mm panels.

Interpretation: The value lies less in equipment assembly and more in controlling uniformity over very large areas. That capability also matters for solar panels and other large substrates.

2. Why vacuum deposition matters for perovskite tandem cells

Early perovskite work focused on wet processes such as spin coating and slot-die coating. In silicon-perovskite tandem cells, however, preserving the textured silicon bottom cell and avoiding solvent damage to electrodes or passivation layers become critical.

Official fact: The source presents the theoretical efficiency limit of single-junction silicon solar cells as 29% and frames tandem structures as the commercialization route beyond that ceiling.

Interpretation: YAS’s vacuum thermal evaporation is a solvent-free dry process that can support conformal coating. The more the tandem standard moves toward full deposition or hybrid deposition-wet process flows, the more valuable YAS’s option becomes.

Solution process

Lower initial CAPEX and speed, but texture uniformity and solvent damage are risks.

Vacuum deposition

Solvent-free conformal coating is attractive for tandem mass production.

3. Business structure: LGD dependency plus a solar option

- YAS has been highly tied to LG Display’s OLED capex cycle, which created earnings volatility.

- If LG Display resumes P10/P9 upgrades, IT OLED preparation, or efficiency capex, deposition sources and transfer systems can become immediate revenue drivers.

- Adoption by Chinese panel makers such as CSOT in the Gen-8.6 cycle could reduce LGD dependency.

- The key solar trigger is whether Hanwha Qcells places pilot or mass-production tandem-cell tool orders in 2026-2027.

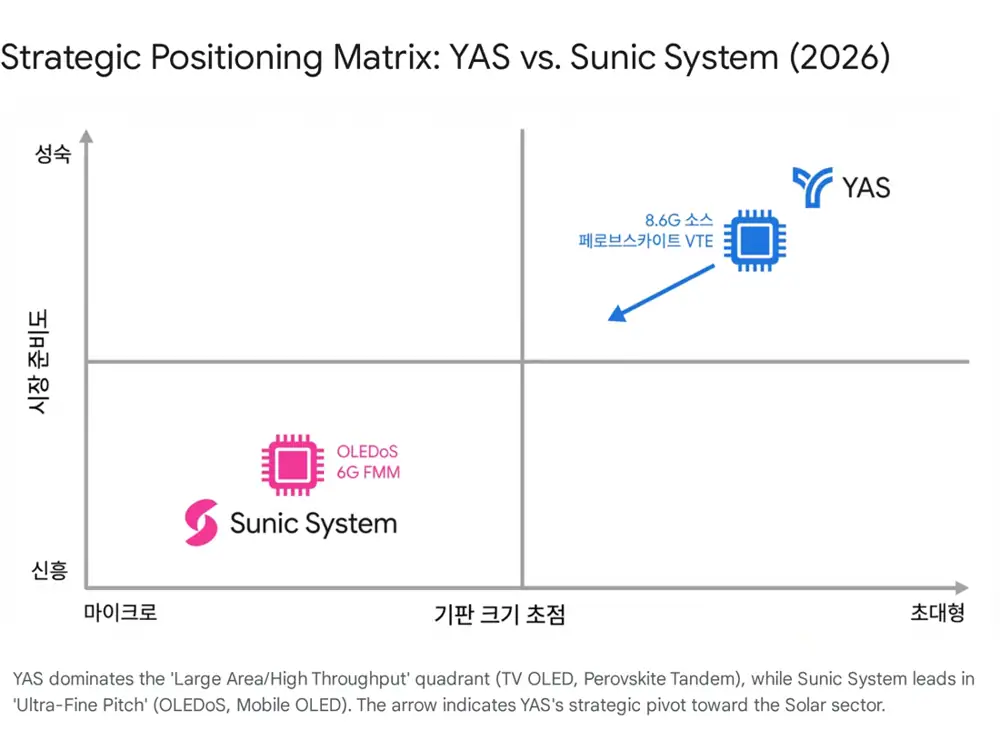

4. Valuation versus Sunic System

| Metric | YAS | Sunic System | Note |

|---|---|---|---|

| Market cap | Around KRW 130bn | KRW 450bn-500bn | Sunic is about 3-4x larger |

| PBR | 0.9-1.0x | 4.0-5.0x | YAS trades near liquidation value |

| Forward PER | 10-15x assuming normalized earnings | 30-40x | Sunic reflects a growth premium |

| Financial stability | Debt ratio in the 3% range | Around 100% | YAS has the stronger balance sheet |

Interpretation: If YAS wins perovskite tool orders and is reclassified as a solar-equipment name, the source argues that a PBR re-rating toward 2-3x becomes possible.

5. Three things to watch

- Formal LGD investment in Gen-8.6 or large OLED upgrades.

- Hanwha Qcells tandem-line equipment orders and whether YAS appears on the vendor list.

- Whether perovskite mass-production standards settle on hybrid or full-deposition processes rather than all-wet processes.

In short, YAS looks less like a glamorous growth story and more like a deep-value equipment name with large solar upside from a low valuation base.

Sources

- Naver original post

- YAS corporate profile

- YAS quarterly filing, KRX

- The Elec on LG Display capex

- Etoday LG Display conference call

- MDPI review on large-area perovskite preparation

- Large-area perovskite fabrication using slit coating

- Etoday on YAS and Hanwha perovskite deposition patent

- Qcells tandem-cell efficiency release

- DataM Intelligence perovskite solar cells market

- Simply Wall St YAS analysis