DEEP RESEARCH · JUSUNG ENGINEERING

Jusung Engineering: The Next-Gen Solar Equipment Opportunity Opened by AI Power Demand

A review of perovskite tandem, ALD/CVD equipment, III-V compound semiconductors, corporate split, and the 2025-2035 market opportunity.

0. Bottom line first

My core read is that Jusung Engineering is not a solar-cell maker, but an equipment enabler that can make high-efficiency solar manufacturable. AI data-center power demand forces higher generation per unit area, and perovskite tandem plus ALD-based deposition equipment become the key to solving that bottleneck.

Official fact: The source says conventional crystalline-silicon solar cells are approaching the Shockley-Queisser limit of about 29.4%, creating technology saturation, while perovskite-silicon tandem cells are emerging as the next-generation alternative. Jusung Engineering is presented as a company applying ALD technology accumulated in semiconductor and display equipment to solar manufacturing.

Interpretation: The investment point is not module shipment volume. It is whether Jusung can solve mass-production bottlenecks such as large-area uniformity, durability, encapsulation, and damage-free deposition with equipment. In other words, the case is the equipment premium when solar shifts from price competition to efficiency competition.

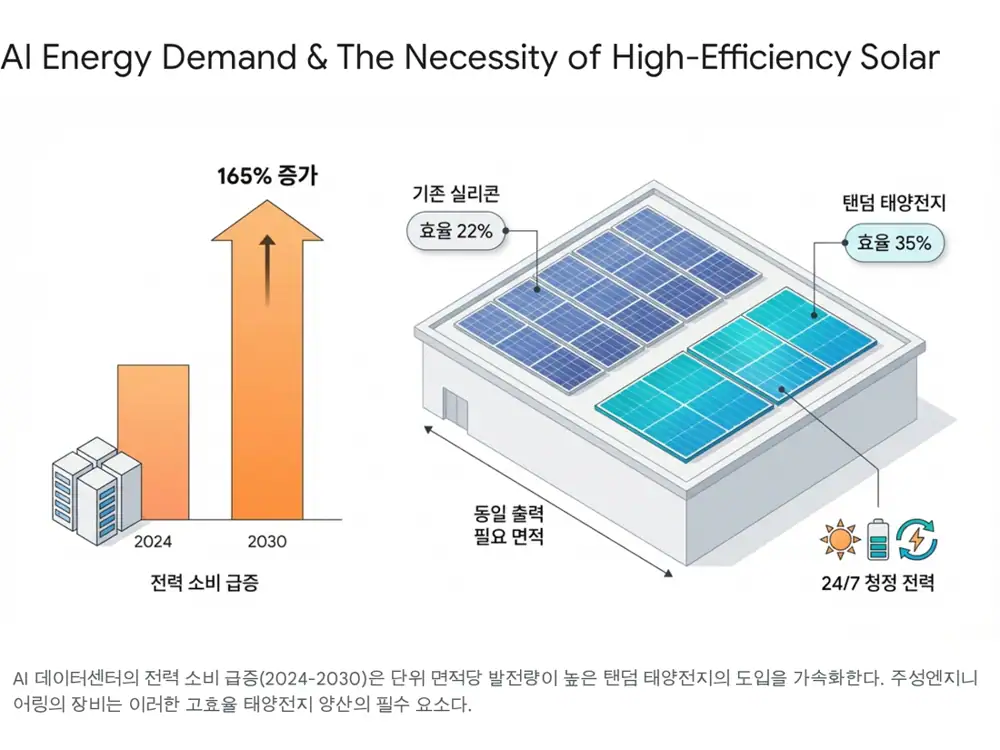

1. AI data centers accelerate solar-efficiency competition

The source frames the 2025 energy market as facing dual pressure from net-zero requirements and power demand from AI and data centers. Renewable energy, especially solar, is becoming essential infrastructure rather than an optional alternative.

Official fact: Citing Goldman Sachs, BloombergNEF, and others, the source says global data-center power demand is expected to rise about 165% by 2030 versus 2023. It also mentions an aggressive view that U.S. data-center power consumption could reach 35GW to as much as 106GW by 2030.

Transmission grids face capacity and stability limits, so hyperscalers such as Amazon, Google, and Microsoft are adopting on-site generation near data centers. The source compares nuclear and SMR, which can take more than 10 years to build, with solar, which can be deployed within 18 months.

Interpretation: The bottleneck is land. Data-center sites have limited nearby space, so demand rises for high-efficiency modules that generate more power from the same area. That is where tandem solar cells become not just a new technology but a candidate solution for data-center power bottlenecks.

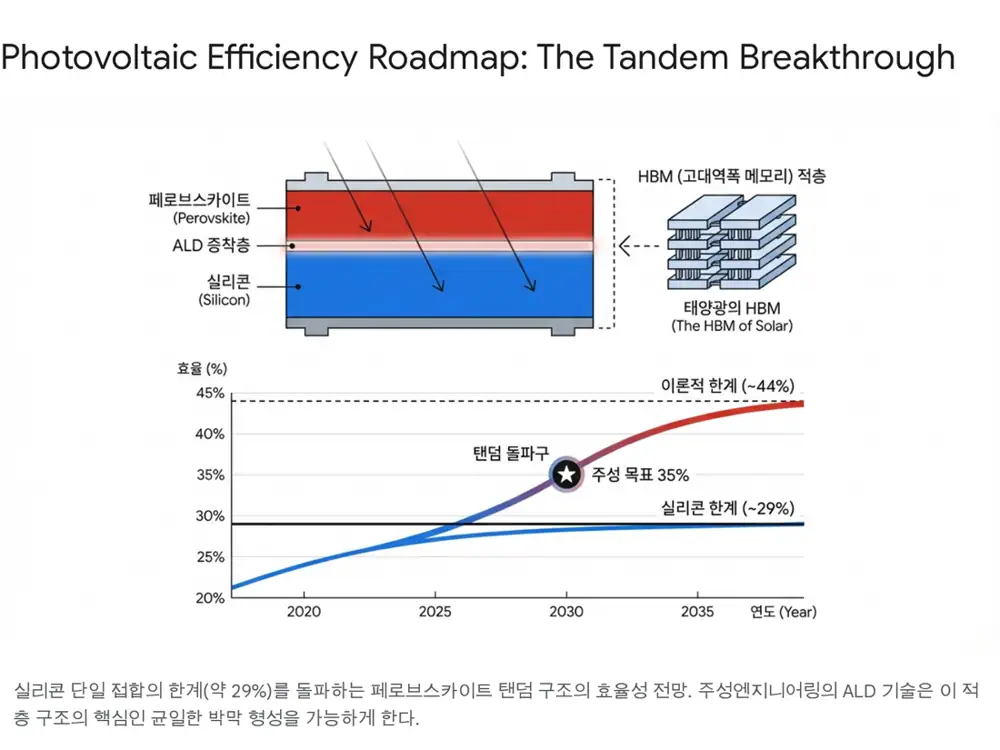

2. Tandem solar cells: the HBM of solar

The source compares tandem solar cells to HBM in semiconductors. Just as semiconductors vertically stack memory chips to overcome data-processing limits, solar stacks cells that absorb different wavelengths to break through efficiency limits.

Silicon or CIGS

Primarily absorbs red, long-wavelength light.

Perovskite

Absorbs blue, short-wavelength light and can tune absorption through bandgap control.

35%+ efficiency

The source says Jusung targets more than 35% generation efficiency by placing perovskite on HJT silicon cells.

Official fact: The source says conventional silicon modules remain in the low-20% efficiency range, while perovskite tandem modules have a theoretical efficiency limit of 44% and may reach 30-35% or more in early commercialization. That implies more than 1.5x power generation for the same area.

3. Value-chain bottlenecks and Jusung's role

The commercialization bottlenecks for perovskite tandem cells are large-area uniformity and durability. Small lab cells can achieve high efficiency, but commercial-scale modules face efficiency drops and structural degradation from moisture and oxygen.

| Value-chain stage | Key issue | Jusung Engineering's role |

|---|---|---|

| Materials | Chinese companies dominate raw-material supply chains and pricing is volatile. Research continues on different chemical compositions. | Rather than producing materials directly, Jusung focuses on equipment compatibility for stable precursor handling and thin-film technology that minimizes expensive material use. |

| Equipment | Nanometer-scale perovskite and ETL/HTL layers must be deposited uniformly over large areas without damage. Solution processing has limits in large-area uniformity. | Semiconductor-proven ALD enables atomic-level thickness control and coverage. Spatial ALD improves process speed and manufacturability. |

| Cell/module | Oxford PV, Hanwha Qcells, and others are competing to commercialize; preventing moisture-driven degradation is a final gate. | ALD-based ultrathin encapsulation layers block moisture and oxygen and support solutions targeting more than 20 years of perovskite lifetime. |

Interpretation: Jusung is better understood as a platform-equipment company than a materials company. The source treats damage-free deposition, which forms electrodes and protective layers without damaging the underlying perovskite, as a key moat.

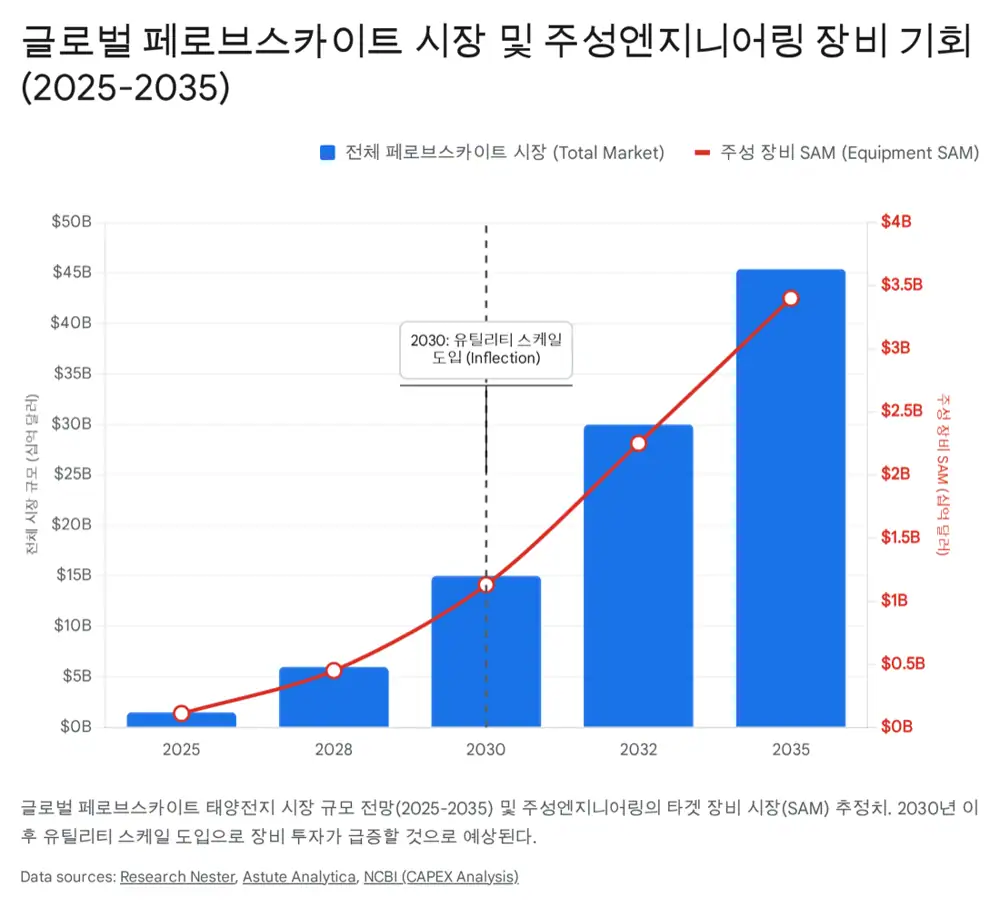

4. 2025-2035 market opportunity: SAM matters more than TAM

| Market | Source figure | Interpretation |

|---|---|---|

| Perovskite solar cells in 2025 | About USD 342M to USD 1.94B | Early commercialization through pilot lines, BIPV, and small electronics |

| Perovskite solar cells in 2035 | At least USD 24.1B to as much as USD 66.5B | Potential CAGR of 28-69% |

| Regional mix | Asia-Pacific 33-56% | Chinese expansion and Korean technology-led investment concentrate equipment demand |

| Global ALD equipment in 2025 | About USD 3.2B-3.6B | Total ALD market including semiconductors |

| Global ALD equipment in 2035 | USD 9.7B-10.7B, about KRW 13T-14T | CAGR 11.5-12.9% |

| Jusung solar ALD/CVD SAM | USD 1.5B-2.5B per year, about KRW 2T-3.3T | Could reach 15-20% of the overall ALD market by 2030-2035 |

Interpretation: Investors should focus on the deposition-equipment SAM where Jusung can actually generate revenue, not the total module-market TAM. The source states that CAPEX is about 15-20% of solar-cell manufacturing cost and that thin-film deposition becomes more important as cells move higher in efficiency.

5. Competitive edge: ALD/CVD and III-V compound semiconductors

Official fact: The source says Jusung Engineering pioneered the application of semiconductor ALD technology to solar and that spatial ALD improves the slow deposition speed of conventional ALD, making mass production possible. This helps raise yield and equipment uptime, reducing LCOE.

Another axis is III-V compound semiconductors such as InGaP and GaAs. The source says this technology targets ultra-high efficiency above 47%. Traditionally, it required processes above 1000°C and expensive substrates, limiting use to aerospace, but Jusung claims to have developed technology to deposit these materials on ordinary glass substrates below 400°C and lower production cost to 1/30 of the previous level.

Atomic-level control

High-precision deposition that provides full coverage even on rough silicon surfaces.

Spatial ALD

Instead of time-cycling precursor injection and purge, the substrate passes through spatially separated zones to raise deposition speed.

Premium high-efficiency markets

Could expand into EV roofs, BIPV, UAM, and other high-value energy markets.

Interpretation: Chinese equipment companies are strong in turnkey lines and lower-cost general processes, but North American and European manufacturers may prefer non-Chinese high-performance tools amid U.S.-China supply-chain reshuffling. The source calls this a geopolitical premium for Jusung and positions its tools as high-end solutions competing on yield and efficiency ROI rather than price alone.

6. Corporate split, earnings outlook, and risks

Official fact: In May 2024, Jusung Engineering announced a governance restructuring that would split the semiconductor business through a human split and separate solar/display businesses through a physical split. The source interprets this as a strategic decision to have the solar-equipment business valued separately from semiconductor-cycle volatility.

| Outlook item | Source content |

|---|---|

| Solar business unit | Could be separated as tentative Jusung SD or Jusung Lux, enabling independent financing and aggressive R&D |

| Valuation expectation | Market hopes for global solar-equipment peer valuation of 20-30x PER |

| 2024 revenue | Expected around KRW 400B range |

| 2025 revenue | Expected to exceed KRW 500B with solar and non-memory semiconductor equipment contribution |

| 2026 revenue | Expected above KRW 600B |

| Operating margin | Expected to remain in the 30% range as high-margin ALD equipment mix expands |

| ROE | Expected to rise from 19.2% in 2024 to 23.7% in 2026 |

Risk factors

- Perovskite durability: If moisture and thermal-stability problems remain unresolved, large orders may be delayed. Outdoor durability data for more than 20 years is critical.

- Chinese catch-up: Chinese equipment companies are improving quickly. Jusung needs to maintain a 35-47% efficiency technology gap to defend against price competition.

- Post-split execution: The solar business needs concrete overseas orders, especially in Europe and North America, to sustain re-rating.

7. Final view

Interpretation: My conclusion is that Jusung Engineering is a distinctive equipment company transplanting semiconductor technology into solar. AI data-center power demand is pulling high-efficiency solar demand forward, and Jusung's ALD tools could become essential if that demand converts into mass production.

The key, however, is not expectation but orders and durability data. The strongest re-rating requires evidence that the post-split solar business can secure concrete overseas orders in Europe and North America and that its process equipment can solve the 20-year-plus durability problem for perovskite tandem cells.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224175926105

- Goldman Sachs: https://www.goldmansachs.com/insights/articles/ai-to-drive-165-increase-in-data-center-power-demand-by-2030

- Utility Dive: https://www.utilitydive.com/news/us-data-center-power-demand-could-reach-106-gw-by-2035-bloombergnef/806972/

- WRI: https://www.wri.org/insights/us-data-centers-electricity-demand

- IEA Energy and AI PDF: https://iea.blob.core.windows.net/assets/b8a83930-5c77-4da7-b795-270ab6a6c272/EnergyandAI.pdf

- Perovskite PDF: https://drive.google.com/open?id=1gcOfc77AKoX8yVcBf5Q4k2s-xLy_EcFM

- Department of Energy: https://www.energy.gov/eere/solar/multijunction-iii-v-photovoltaics-research

- Jusung Engineering Solar Cell: https://jusung.com/eng/document/solar

- The Korea Times: https://www.koreatimes.co.kr/business/tech-science/20230511/interview-oled-displays-another-axis-in-s-korea-us-alliance

- NREL PDF: https://docs.nrel.gov/docs/fy23osti/80941.pdf

- Asia Economy: https://cm.asiae.co.kr/article/2024060508440800545

- Research Nester: https://www.researchnester.com/reports/perovskite-solar-cell-market/6346

- Astute Analytica: https://www.astuteanalytica.com/industry-report/perovskite-solar-cells-market

- GlobeNewswire: https://www.globenewswire.com/news-release/2026/01/14/3219084/0/en/Perovskite-Solar-Cells-Market-Projected-to-Reach-US-24-19-Billion-by-2035-Supported-by-Scaling-of-Manufacturing-Capacity-Says-Astute-Analytica.html

- Market Research Future: https://www.marketresearchfuture.com/reports/atomic-layer-deposition-equipment-market-24147

- Research Nester ALD: https://www.researchnester.com/reports/atomic-layer-deposition-market/1519

- Precedence Research: https://www.precedenceresearch.com/atomic-layer-deposition-market

- EurekAlert: https://www.eurekalert.org/news-releases/1087234

- PMC: https://pmc.ncbi.nlm.nih.gov/articles/PMC12000492/

- Investing.com: https://www.investing.com/equities/jusung-engineering-co-ltd

- LEAD Intelligent: https://www.leadintelligent.com/en/lead-rolls-out-end-to-end-perovskite-equipment-to-accelerate-solar-breakthroughs/

- THE INVESTOR: https://www.theinvestor.co.kr/article/3408773

- Businesskorea: https://www.businesskorea.co.kr/news/articleView.html?idxno=216376

- Mirae Asset Securities: https://securities.miraeasset.com/newir/view/pc/en/investor/researchReportsView.jsp?messageId=2323949

- Mirae Asset PDF: https://securities.miraeasset.com/bbs/download/2127971.pdf?attachmentId=2127971

- Bloter: https://www.bloter.net/news/articleView.html?idxno=615805

- MDPI Nanomaterials: https://www.mdpi.com/2079-4991/15/21/1674

- TaiyangNews: https://taiyangnews.info/technology/spatial-ald-for-perovskite-solar-cell-manufacturing

- OAE Publishing: https://www.oaepublish.com/articles/energymater.2023.150

- NREL Research Hub: https://research-hub.nrel.gov/en/publications/six-junction-iii-v-solar-cells-with-471-conversion-efficiency-und/