DEEP RESEARCH · CURIOSIS

Curiosis: Where Lab Automation Meets Korea’s Synthetic Biology Strategy

A small-cap biotech equipment report centered on optical moving, hypercasting, and biofoundry policy demand.

0. Bottom line first

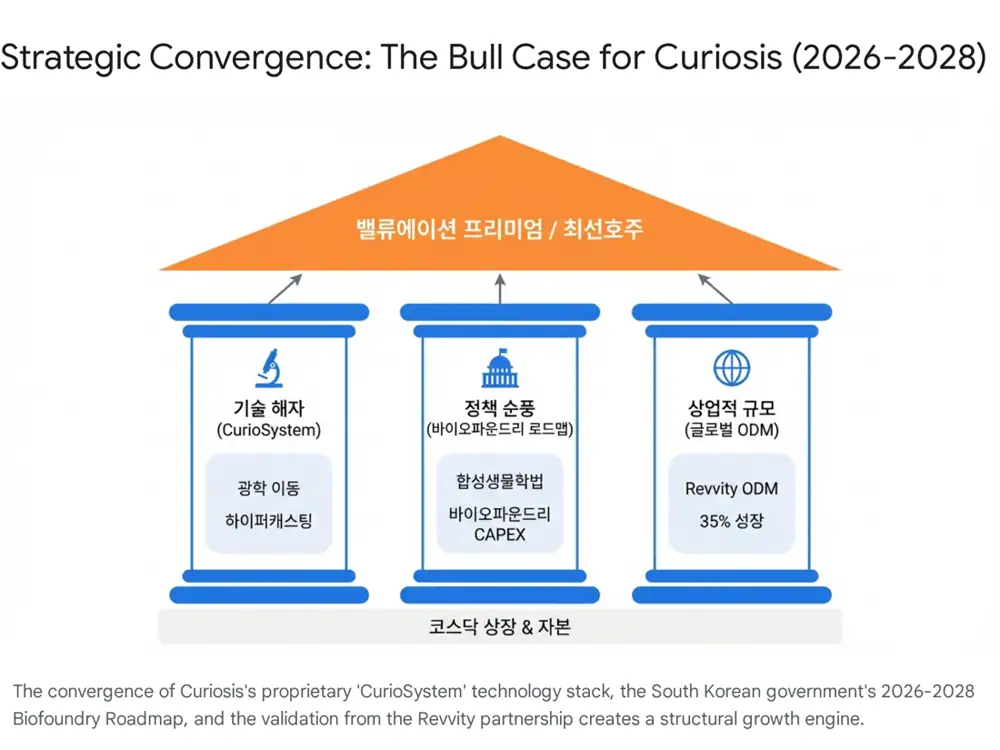

My read is that Curiosis is not just a biotech equipment maker. It sits at the intersection of differentiated engineering, national biofoundry policy, and global ODM validation. The source frames 2026-2028 as the start of a J-curve and names Curiosis as a Top Pick among Korean small-cap biotech names.

Official fact: According to the source, Curiosis listed on KOSDAQ through a technology-special listing in November 2025. 2025 revenue was about KRW 7.3 billion, up 34.8% YoY, while operating loss widened to KRW 7.5 billion due to recurring R&D expenses for ODM new-product development.

Interpretation: The loss is a near-term burden, but it can be reinterpreted as upfront investment if the Revvity ODM contract and Pohang Techno Park system contract convert into revenue.

1. Company and capital structure

Curiosis was founded on January 22, 2015 as a company combining biology and mechanical engineering. It has headquarters in Gangnam, Seoul and manufacturing/R&D facilities in Yongin, and the source describes its CurioSystem™ as an internally controlled stack of core parts and software.

CEO Ho-young Yoon studied mechanical engineering at Hanyang University and Seoul National University, later working as a Harvard researcher. The source interprets this microfluidics and biomedical-engineering background as the company’s “engineering-first” DNA.

| Item | Source detail | Why it matters |

|---|---|---|

| Largest shareholder | CEO Ho-young Yoon about 14.79% | Stable control when combined with Jisan at 8.79% and management-related stakes |

| Institutional holders | STIC Innovation Fund 6.59%, Kiwoom-Shinhan Innovation No. 2 4.92%, Shinhan-Timefolio Bio Growth Fund 4.61% | Institutional validation of the technology-company scale-up case |

| IPO | Listed on November 13, 2025; IPO price KRW 22,000; 1.2 million shares issued; about KRW 26.4 billion raised | Capital for Yongin capacity expansion and global orders |

| Capacity | KRW 100 billion by October 2025 and KRW 200 billion by Q2 2027 | Preparedness for biofoundry equipment demand and Revvity ODM volume |

2. Technology moat and product portfolio

Official fact: The source describes CurioSystem™ as a proprietary platform vertically integrating optics, mechanical design, electrical control, and software.

Observe cells without shaking the sample

Conventional plate moving can create vibration and shear stress. Curiosis fixes the cell stage and moves the optical lens module on the X-Y axes, aiming to bring physical vibration close to zero.

Precision plus manufacturability

The aluminum die-casting based process targets micrometer-level precision, while the chassis acts as a heat sink inside a 37°C, 95%+ humidity incubator.

Reducing cell loss

Cellpuri replaces centrifugation with a filterless microfluidic-chip approach that separates cells by size and targets higher cell viability and rare-cell workflows.

| Product | Source description | Business meaning |

|---|---|---|

| Celloger Mini/Nano/Pro/Stack/M26 | Real-time cell observation inside incubators; the 2026 flagship M26 targets high-throughput screening through Revvity collaboration | Core revenue base and pharmaceutical demand fit |

| Cellpuri | Damage-minimizing separation and concentration for cell and gene therapy workflows | Equipment plus disposable-chip consumables |

| CPX | Automated colony picker for synthetic biology and the target of the Revvity ODM contract | China-market supply and global-standard validation |

| MSP | Digital pathology scanner converting glass slides into digital images | Long-term option tied to AI diagnostics and hospital digitization |

3. Policy demand and catalysts

The strongest external variable in the source is Korea’s biotech policy roadmap. The Synthetic Biology Core Technology Promotion Act, promulgated on April 22, 2025, defines synthetic biology as a national strategic technology and elevates biofoundry construction into a legal policy task.

Official fact: The source says Korea plans to invest KRW 126.3 billion from 2025 to 2029 in public biofoundries, with 2026-2028 as the heavy equipment-ordering phase.

Interpretation: The KRW 2.08 billion antibody-drug discovery automation-system contract with Pohang Techno Park in December 2025 is an early example of policy demand converting into an order.

| Catalyst | Fact or number | My read |

|---|---|---|

| Revvity ODM | ODM contract with Revvity Biomed Shanghai announced January 23, 2026; 3-year MOQ; base contract about KRW 2.18 billion | The source reads this as a baseline equal to 46% of 2024 revenue |

| Pohang Techno Park | KRW 2.08 billion supply contract in December 2025 | Potential reference site for public biofoundry demand |

| Biosecure Act context | US-China biotech rivalry and lower China dependency | A possible channel for Korea-built equipment sold into China as “Powered by Curiosis” |

4. Financial outlook and risks

| Item | Source figure | Checkpoint |

|---|---|---|

| 2025 revenue | About KRW 7.3 billion, +34.8% YoY | Evidence of product penetration |

| 2025 operating profit | KRW -7.5 billion | Whether ODM R&D spending is recovered |

| 2026 revenue scenario | The source presents KRW 15 billion+ and more than 100% YoY growth as possible | Revvity purchase orders and B2G revenue recognition |

| Break-even | Quarterly profitability as early as H2 2026, or by 2027 in the source scenario | Operating leverage and R&D stabilization |

- Overhang: venture-capital stakes, including STIC Innovation Fund, are estimated at roughly 6-10%, and lock-up releases can create selling pressure.

- Cash burn: 2025 losses consumed cash. Although the IPO raised KRW 26.4 billion, failure to turn profitable by H1 2026 could raise additional financing concerns.

- Key monitoring items: Revvity PO size, additional public tenders, and whether quarterly profitability appears in H2 2026.

5. Final read

The source’s conclusion is that Curiosis combines technology, policy, and capital/business execution. Optical moving and hypercasting are the technology moat; the 2026-2028 biofoundry buildout is the policy demand; IPO funding and Revvity are the commercial bridge.

Interpretation: I read this less as a generic “good equipment company” story and more as a checklist for a company whose public-infrastructure and global-ODM opportunities must now prove themselves in numbers. The first real test year is 2026.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224175600249

- 합성생물학 육성법 공포 안내 - 법무법인 세종: https://www.shinkim.com/kor/media/newsletter/2808?page=13&code=&keyword=

- 합성생물학 기술개발 및 국제협력 현황 - 대한민국 정책브리핑: https://www.korea.kr/common/docViewer.do?fileId=197651442&tblKey=GMN

- 스틱벤처스 '이노베이션펀드' 관련 기사 - 뉴스톱: https://www.newstopkorea.com/news/articleView.html?idxno=42698

- 큐리오시스 - 유진투자증권: https://www.eugenefn.com/common/files/amail/20251027_B_jongsun.park_2467.pdf

- 라이브 셀 이미징 시장 보고서 - Mordor Intelligence: https://www.mordorintelligence.kr/industry-reports/live-cell-imaging-market

- 큐리오시스 레비티 ODM 협업 기사 - MEDI:GATE NEWS: https://www.medigatenews.com/news/1716217143

- 세계 최초 합성생물학 육성법 - 법무법인 화우: https://www.hwawoo.com/newsletter/2025_04_07/250407_k_t.pdf

- 바이오파운드리 인프라 구축사업 예타 통과 자료: https://www.motir.go.kr/attach/down/095a2dda9c864e1d90d751f7668a1117/3ce78ecf646ac7913d049a301befb3d7