DEEP RESEARCH · LG Energy Solution

LGES Acquires 100% of NextStar for KRW ~140,000 — Settling MVG Penalties via Equity

Take-or-Pay / MVG penalty settled in kind, gain on bargain purchase, North America ESS pivot

0. Bottom line first

On Feb 6, 2026, LGES acquired Stellantis’ 49% stake in NextStar Energy (Canada) for USD 100 (~KRW 140,000). This is not an M&A valuation event but a ‘settlement in kind’ of Stellantis’ Take-or-Pay / MVG (minimum volume guarantee) penalty. Outcome: ① LGES books a gain on bargain purchase > KRW 1 trillion, ② full control of a ~KRW 5T factory, ③ rapid pivot to North American ESS, ④ 100% capture of Canadian / Ontario incentives.

1. EV chasm and JV structural risk

The 2H25 EV demand pause hit OEM electrification hard — rates, charging gaps, and price resistance combined. JV factories that looked great in boom times turned into fixed-cost / volume-commitment risk for OEMs in the slump. Stellantis pulling out of NextStar is the clearest example yet.

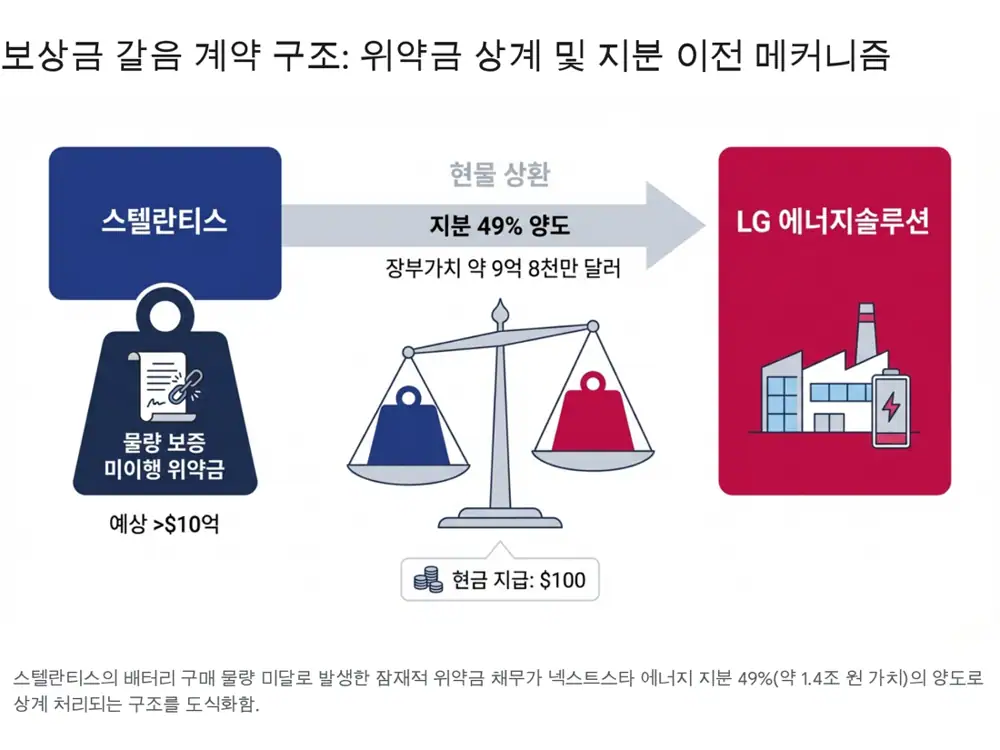

2. The deal mechanics — why USD 100?

2.1 Settlement, not M&A pricing

NextStar is producing modules with cell lines being commissioned — a near-finished asset worth trillions of won. The USD 100 price is not a fair-value purchase but the carrying mechanism of Stellantis’ contract-breach penalty. Stellantis missed the Take-or-Pay battery purchase commitments and settled the penalty by giving up its already-invested equity (~USD 980M, KRW ~1.42T) instead of paying cash.

2.2 Take-or-Pay / MVG mechanics

- MVG: Stellantis was contractually obliged to buy a high share (e.g., 80–90%) of 45+GWh/yr capacity.

- Penalty: Failure to order in 2025 triggered fixed-cost and lost-margin penalties measured in hundreds of billions to trillions of won.

- Why equity: Sunk-cost equity is cheaper for Stellantis than cash; LGES prefers a productive asset over cash compensation.

2.3 Gain on bargain purchase

Under K-IFRS, when consideration is materially below fair value of net assets in a business combination, the difference is recognized as profit. With Stellantis having invested ~USD 980M (~KRW 1.42T) for an effective USD 100 acquisition, the accounting gain should exceed KRW 1T — boosting LGES’ 1Q or 2Q 2026 consolidated net income.

3. Stellantis crisis — EUR 22.2B impairment

| Item | EUR | Description |

|---|---|---|

| Product plan reset | 14.7B | Cancellation of EV projects mismatched with demand; platform write-offs |

| EV supply-chain reset | 2.1B | Includes NextStar stake-sale loss; battery sourcing change |

| Other operating costs | 5.4B | Recalls, warranty provisions, NA inventory clean-up, etc. |

| Total | 22.2B | Non-cash charges booked in 2H25 |

CEO Antonio Filosa admitted Stellantis “overestimated the electrification transition pace” and announced a “business reset.” H2-25 net loss expected ~EUR 19–21B; 2026 dividend suspended; ~EUR 5B bond issuance — a full-blown cash-securing push. Markets Insider, Finviz, MarketWatch via Morningstar.

4. LGES strategic pivot — ESS

4.1 From stranded asset to opportunity

While the EV market is in a lull, the ESS market is booming on AI datacenter buildout and renewable grid stabilization. LGES will rapidly convert NextStar into an ESS-only or mixed facility — modules started shipping in Nov 2025, and 100% control accelerates decisions. The focus is cost-competitive LFP-based ESS cells and modules.

4.2 Trade-policy tailwind

- US: Per USTR Section 301, tariffs on Chinese lithium-ion batteries (including non-EV) rise from 7.5% → 25% in 2026. Acculon Energy, InfoLink

- Canada: Mirrors the US; combined with Trump-era ‘critical minerals trade bloc’ design, North American production becomes more valuable.

- Edge: LGES is the only non-China player with truly large-scale ESS cell production in North America (Michigan-Holland-Lansing + Windsor — the ‘North America triangle’).

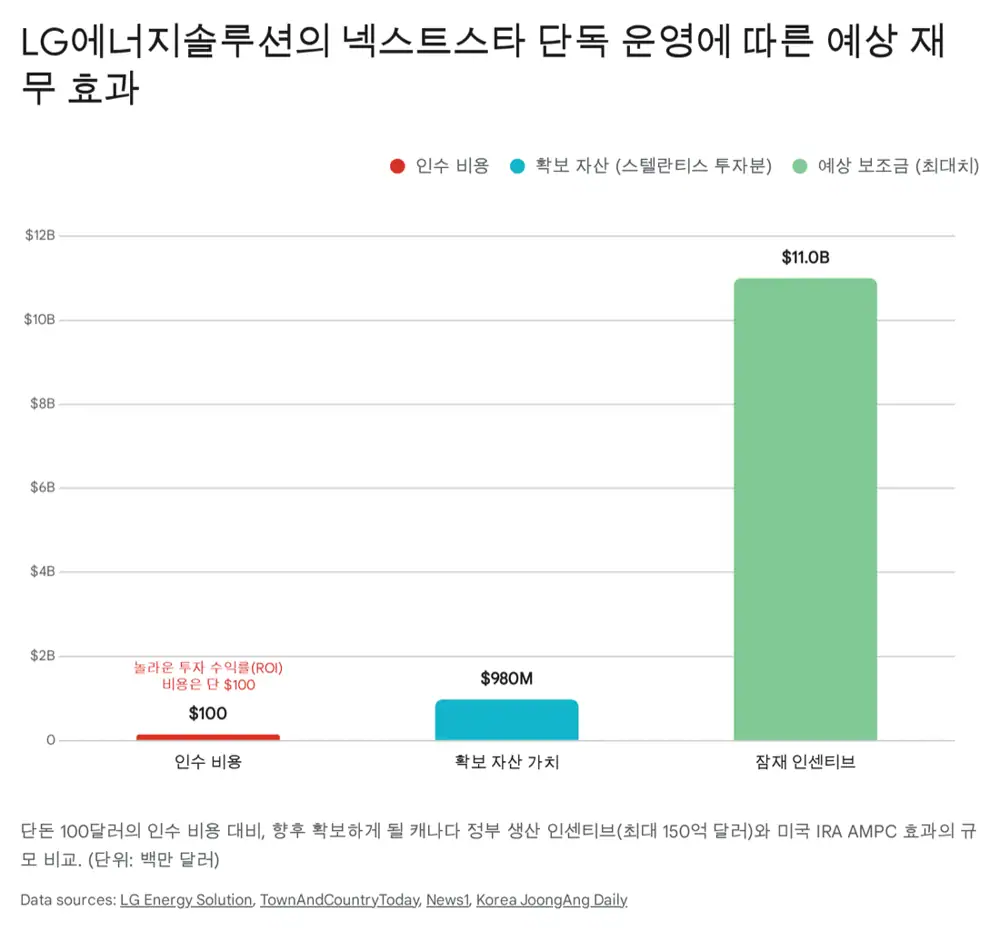

4.3 Subsidy capture

Performance-based incentives promised by Canada federal and Ontario provincial governments total up to CAD 15B (~KRW 15T), indexed to the US IRA AMPC (USD 35/kWh for cells, USD 10/kWh for modules). The benefits were previously split 51:49 with Stellantis — now LGES collects all of it. Spending USD 100 to secure trillions in future subsidies is an extraordinary ROI moment.

5. Canadian government policy and Korea-Canada defense link

5.1 The Canadian view — jobs first

For Ottawa, who owns the factory matters less than whether it runs and employs Canadians. By Sep 2025, ~CAD 530M in support had been paid out. Conditions: operations through 2032, 2,500 jobs. LGES committed to the existing 1,300 jobs and to ramp up to the target. CBC — government support

5.2 The ‘invisible hand’ of CPSP

Canada is pursuing a ~KRW 60T submarine program (CPSP) for 12 boats. Hanwha Ocean competes against Germany’s TKMS — and Canada’s Industrial and Technological Benefits (ITB) policy is a critical scoring factor. When Stellantis walked away, the fact that a Korean company (LGES) stepped in to preserve jobs strengthens ‘Team Korea’ credibility — a potential halo for Hanwha Ocean. Chosun — Korea consortium vs Germany, FOE, Hanwha press, Canadian Defence Review.

6. Conclusions and outlook

Bargain-purchase gain

Material accounting gain likely lands in LGES H1-26 results.

Capturing NA

Chinese imports squeezed; LGES’ triangle accelerates market-share gains.

Economic alliance

Batteries-submarines-energy ties — possible CPSP halo for Hanwha Ocean.

The transaction blends two strategies: asset capture via penalty offset and portfolio reshaping for shifting trade conditions — a textbook case of crisis-into-opportunity execution.

Sources

- Naver blog source: m.blog.naver.com/.../224175171279

- LGES press release: news.lgensol.com

- Town and Country Today — $100 sale: townandcountrytoday.com

- BNN Bloomberg: bnnbloomberg.ca

- Finviz — $26B charge: finviz.com

- Seoul Shinmun — KRW 140K purchase: seoul.co.kr

- Korea JoongAng Daily — wholly-owned subsidiary: koreajoongangdaily.joins.com

- Chosun English — independent operation: chosun.com

- Joseilbo — disclosure pick: m.joseilbo.com

- News1 — $100 magic: news1.kr

- Business Korea — $100 acquisition: businesskorea.co.kr

- LGES 2024 audit report: PDF

- Korea Times — JV full control: koreatimes.co.kr

- Stellantis business reset: markets.businessinsider.com

- MarketWatch via Morningstar — $26B hit: morningstar.com

- Stellantis press release: stellantis.com

- The EV Report: theevreport.com

- ESG Today — $100 sale: esgtoday.com

- Acculon — Tariff Tangle: acculonenergy.com

- InfoLink — Section 301: infolink-group.com

- CBC — federal support $530M: cbc.ca

- Chosun English — Canada submarine race: chosun.com

- Focus on Economy — Hanwha Ocean industrial proposal: foeconomy.co.kr

- Hanwha press release: hanwha.com

- Canadian Defence Review: canadiandefencereview.com