DEEP RESEARCH · SAJO DONG-A ONE

Sajo Dong-A One: Governance Reshaping and Grain Value-Chain Revaluation

A report on Sajo CPK's market purchases, K-ramen export spillover, and wheat-cost stabilization

0. Bottom line first

I see Sajo Dong-A One's 2026 watchpoint as triple momentum across governance, fundamentals, and macro. Sajo CPK's market purchases signal strategic revaluation inside the group, K-ramen exports lift flour volume, and lower wheat prices improve margin spreads.

1. Governance: what Sajo CPK's emergence means

Official fact: According to the large shareholding report disclosed after market close on February 6, 2026, Sajo Dong-A One's largest shareholder Sajo Seafood and related parties increased their stake from 63.56% to 64.85%, up 1.29 percentage points.

The source focuses on the buyer. The buyer was not an existing listed affiliate but unlisted Sajo CPK. Sajo CPK was formerly Ingredion Korea, the Korean subsidiary of global starch and sweetener company Ingredion. Sajo Group acquired it in February 2024 and changed the company name.

| Company | Source detail | Connection to Sajo Dong-A One |

|---|---|---|

| Sajo CPK | Manufactures and sells food ingredients such as starch, syrup, and sugars | Another basic food-processing material axis alongside flour |

| Foodist | Sajo CPK acquired a 68.16% stake in September 2024 | Food-material distribution and institutional catering channel |

| Sajo Dong-A One | Handles flour milling and feed | Upstream position in the group's food value chain |

Interpretation: Sajo CPK has become close to an intermediate holding company with both manufacturing and distribution. Its market purchases of Sajo Dong-A One shares read less like simple bargain hunting and more like a group-level strategic move to connect flour and starch/sweeteners through procurement and sales-channel synergies.

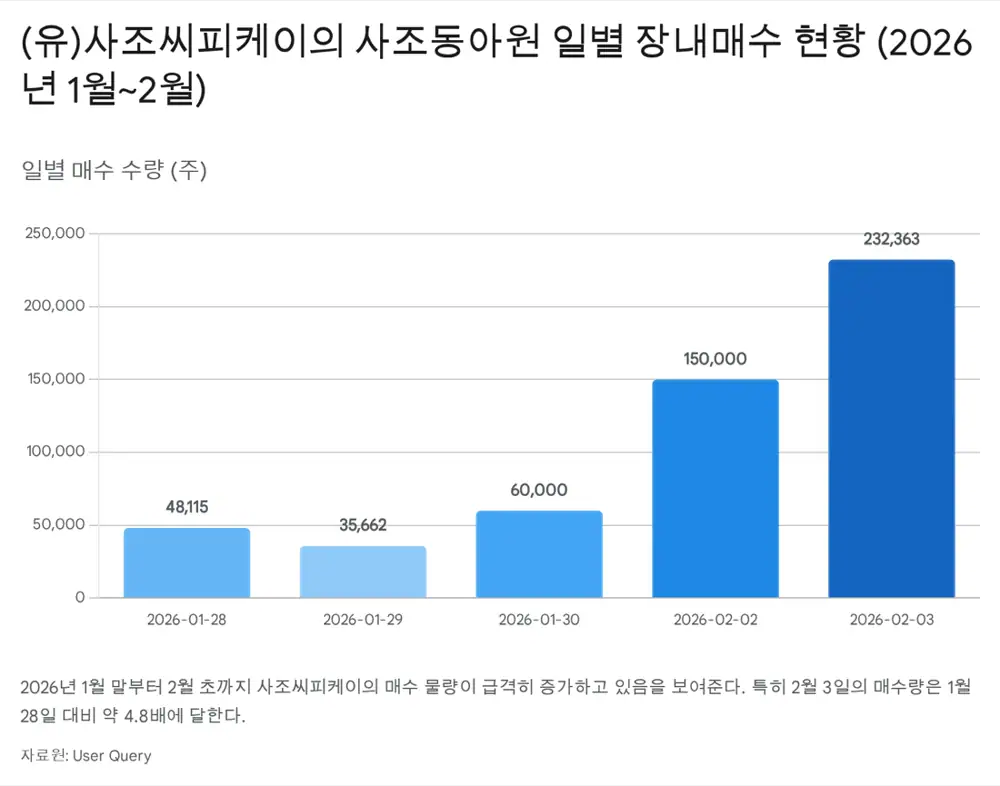

2. Supply-demand: accelerating purchase intensity

The transaction details show Sajo CPK's purchase intensity increasing from late January to early February 2026. Daily purchases rose from 48,115 shares on January 28 to 232,363 shares on February 3.

| Date | Shares purchased | Read |

|---|---|---|

| 2026-01-28 | 48,115 shares | Start of the buying phase |

| 2026-01-29 | 35,662 shares | Early accumulation |

| 2026-01-30 | 60,000 shares | Purchase size increased |

| 2026-02-02 | 150,000 shares | Shift toward aggressive accumulation |

| 2026-02-03 | 232,363 shares | About 4.8x January 28 volume |

Interpretation: Since the largest shareholder and related parties already own more than 60%, hostile M&A defense is not the main explanation. The weight is on resolving undervaluation and improving group governance efficiency. The source connects this with the owner family and affiliates steadily buying listed-affiliate shares since 2021.

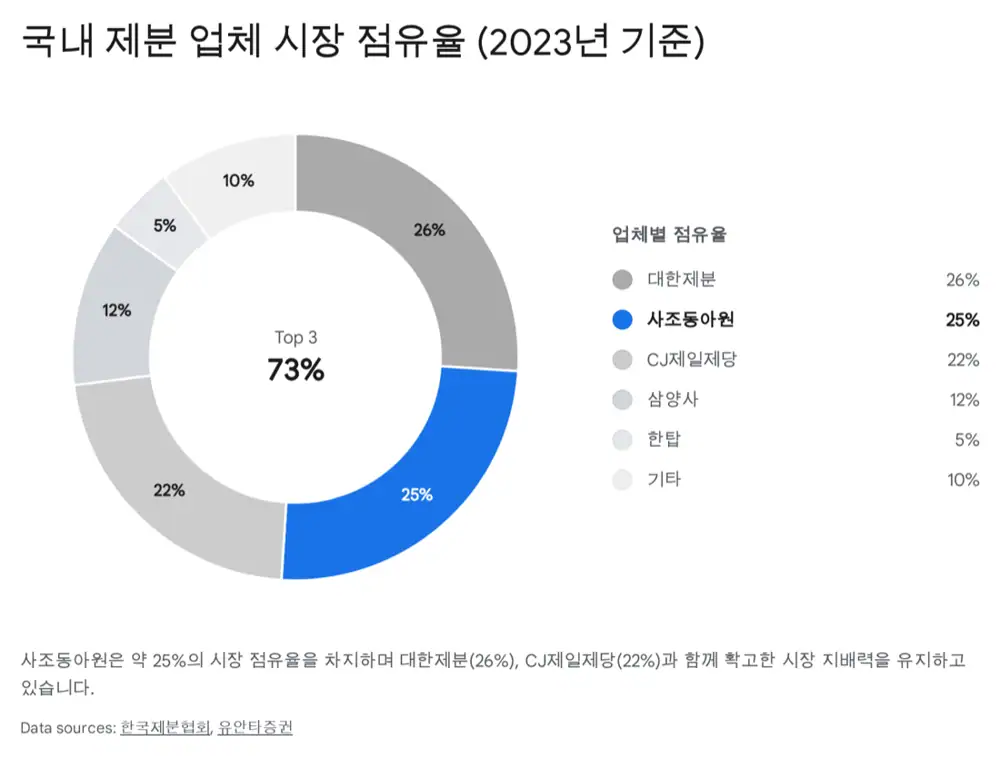

3. Industry: K-ramen exports change flour milling

Sajo Dong-A One's flour business has traditionally been viewed as a mature domestic industry. But since 2024, rapid growth in K-ramen exports has created direct spillover for domestic flour millers that supply wheat flour, the main ingredient in ramen.

| Item | Source number | Meaning |

|---|---|---|

| 2024 Sajo Dong-A One flour sales volume | About 640,000 tons, YoY +8% | Faster growth than competitors |

| Daehan Flour Mills volume growth | About +1.5% | Evidence of Sajo Dong-A One outperformance |

| 2025 additional supply estimate | About 7,500 tons | Customer capacity expansion begins to matter |

| 2026 additional supply estimate | About 30,000 tons | Volume growth becomes more visible |

| Revenue uplift effect | KRW 50.0 billion to as much as KRW 200.0 billion annually | Operating leverage is possible due to the fixed-cost structure of milling |

Interpretation: Even for export ramen, most flour is sourced from domestic millers because quality control and blending know-how are tied to domestic production. When volume rises and plant utilization improves, fixed costs are spread over more output, so operating profit can grow faster than revenue.

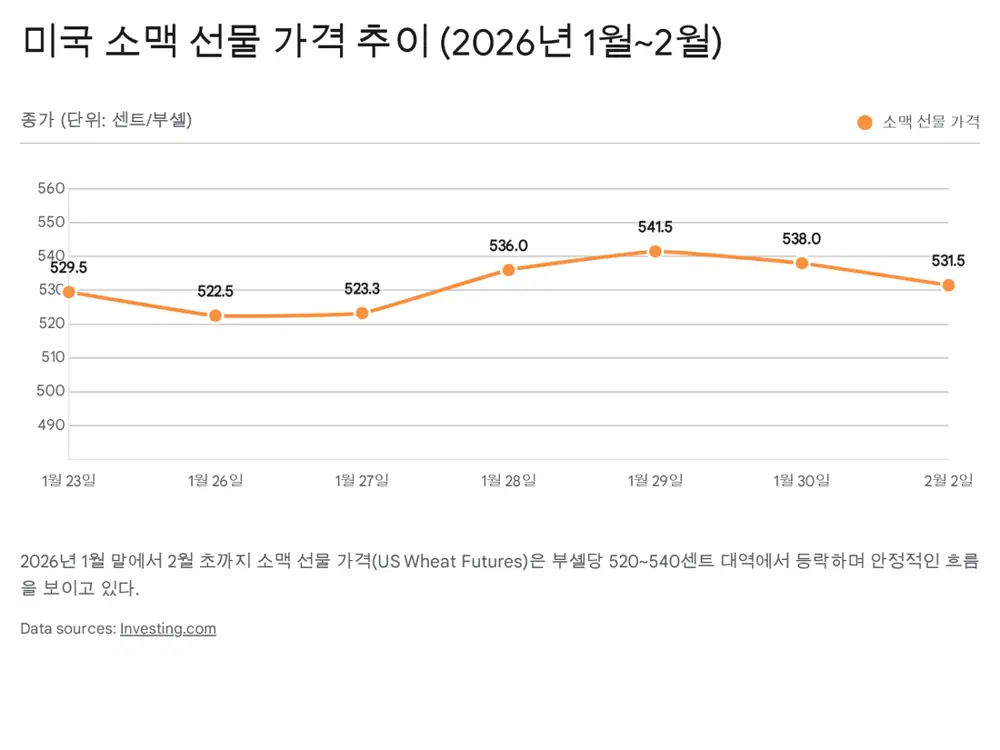

4. Macro: wheat prices and FX

Official fact: In late January to early February 2026, CBOT wheat futures moved in the 520-540 cents per bushel range. This is less than half the level above 1,200 cents per bushel seen during the 2022 Russia-Ukraine war period.

| Variable | Source number/detail | Profitability effect |

|---|---|---|

| CBOT wheat, 2026-01-28 | 536.00 cents | Lower raw-material burden |

| CBOT wheat, 2026-02-02 | 531.50 cents | Continued stabilization |

| Raw wheat input lag | 3-6 months | Low-priced wheat bought in 2H25 affects 1H26 cost |

| 2026 average FX outlook | KRW/USD around 1,390 | Still high, but gradual stabilization is mentioned |

| FX range | Mid-1,300s to low-1,400s | Lower grain prices and stable logistics can offset cost pressure |

The source expects corn and wheat production for the 2025-2026 season to remain healthy and the global supply chain to stay relatively loose into 2026. Because milling has a lag between raw wheat import and processed-product sales, spreads improve if low-cost wheat flows into production while product selling prices fall less.

5. Earnings and valuation

Official fact: Sajo Dong-A One's cumulative 3Q25 revenue was about KRW 513.3 billion and operating profit was KRW 33.1 billion. Annualizing this gives estimated annual revenue of about KRW 680.0 billion and operating profit of about KRW 44.0 billion.

| Item | Source number | Meaning |

|---|---|---|

| 3Q cumulative OPM | About 6.4% | Above the typical milling-industry average of 3-4% |

| Market cap | About KRW 155.8 billion at KRW 1,104 per share | Viewed as low relative to asset value and earnings power |

| Conservative net-income estimate | About KRW 25.0 billion | After deducting interest and other costs from 2025E operating profit of KRW 44.0 billion |

| P/E | About 6.2x | Low versus food-sector 10-12x and ramen-export names above 15x |

| Equity | About KRW 500.0 billion | About 0.3x P/B |

Interpretation: The source sees 0.3x P/B as the sort of level that appears when the market questions a company's ability to continue. But Sajo Dong-A One remains profitable and has growth momentum, so the source views this as irrational overselling.

Group synergy also matters. Through acquisitions such as Foodist and Ingredion Korea, now Sajo CPK, Sajo Group increased group revenue from the KRW 4 trillion range in 2023 to the KRW 6 trillion range in 2024. Sajo Dong-A One sits upstream in that value chain and can absorb demand growth from Foodist's distribution channel and processed-food affiliates such as Sajo Daerim and Sajo Oyang as captive demand.

6. Checklist

- Whether Sajo CPK continues buying additional Sajo Dong-A One shares

- Whether K-ramen exports and customer capacity expansions deliver the expected 7,500 tons in 2025 and 30,000 tons in 2026 additional supply

- Whether CBOT wheat stabilizes around the 520-540 cent range

- Whether 1Q26 earnings confirm the benefit of low-cost wheat input

- Whether earnings growth can support normalization toward 10x P/E and 0.8-1.0x P/B

In conclusion, the source argues that Sajo Dong-A One has enough potential to move out of extreme undervaluation at 0.3x P/B and return toward normal valuation. The key checks are continued stake increases and 1Q26 earnings.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224174285386