DEEP RESEARCH · E-Mart (139480.KS)

E-Mart — from asset-heavy to alliance-led; unpacking the 0.2× P/B paradox

A four-piece combo: CJ Logistics ‘Star Delivery’ + Alibaba JV ‘Grand Opus’ + Traders warehouse club + value-up

0. Bottom line first

E-Mart is leaving the ‘slow retail dinosaur’ persona behind and turning into an agile hybrid platform. Four levers: ① ‘Star Delivery’ via CJ Logistics — rocket-speed without rocket-Capex — bringing G-Market’s SLA in line with Coupang; ② ‘Grand Opus Holdings’, the Shinsegae–Alibaba JV that executes a ‘sleeping with the enemy’ strategy; ③ Traders (2030 sales target KRW 10T) capturing the single-household and ageing-population tailwinds; ④ a real value-up programme — 20% of OP returned to shareholders, 50%+ of treasury shares cancelled. Today’s P/B of 0.16–0.2× is among the cheapest of any global retailer — even the consensus 2027 OP of KRW 660–760B (vs management’s KRW 1T) leaves ample re-rating room.

1. Intro — a retail paradigm shift

The past decade was ‘mobile-first + dawn delivery’ (Coupang-dominated). The next five years will be ‘cross-border commerce + super-ageing society’. E-Mart’s P/B of 0.16–0.2× reflects the ‘growth-less old-economy retailer’ frame — but actions visible from 2H25 onwards are starting to break it.

2. The business and its moat

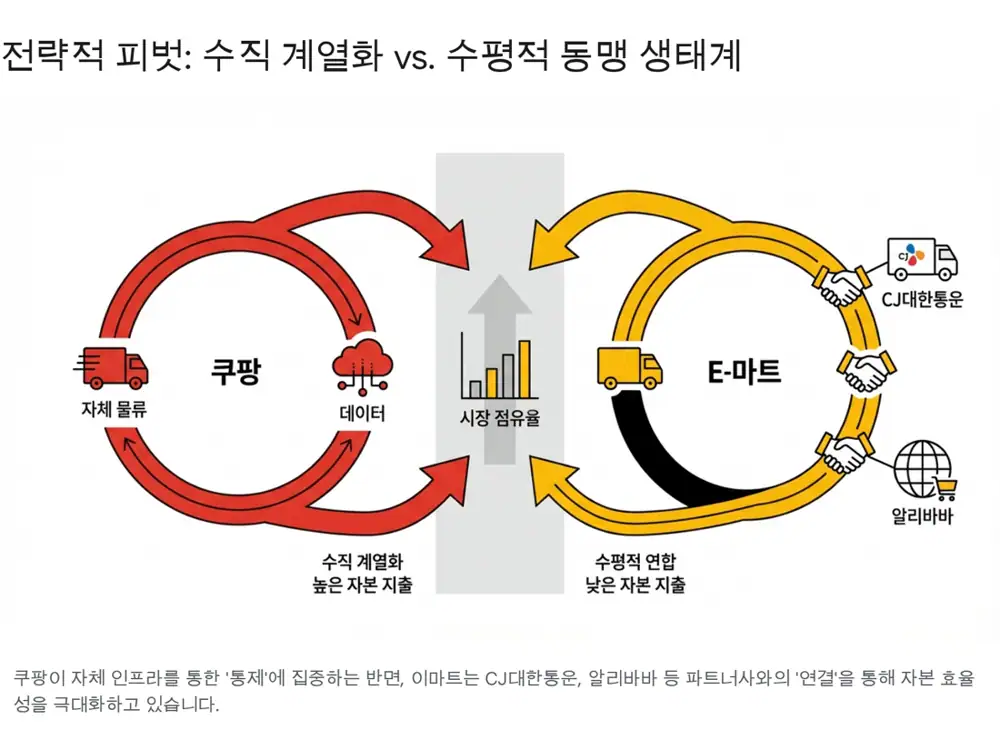

2.1 ‘Capex-less rocket delivery’ — Star Delivery

SSG.COM previously copied Coupang and built its own NE.O fulfilment centres — high fixed costs. From 2H24, the alliance with CJ Logistics changed everything. G-Market’s Star Delivery runs on CJ’s O-NE service to provide next-day, 7-day-a-week delivery — Coupang-grade SLA without the Capex. Sellers using Star Delivery saw average revenue rise +160% in one year. The contrast with Coupang’s self-built fulfilment is stark. Chosun Biz — Sunday delivery, Dealsite — CJ Logistics handling Star Delivery

2.2 Integrated sourcing & buying power

E-Mart, Traders, E-Mart Everyday and convenience stores buy as one — a buying-power weapon nobody else has. Grocery hinges on waste and cold-chain control; E-Mart turns its nationwide stores into urban fulfilment nodes (PP centres) for inventory turn and freshness. Coupang’s ‘Rocket Fresh’ structurally lacks this offline footprint.

2.3 ‘Sleeping with the enemy’ — Grand Opus Holdings

The 2025 50-50 JV between Shinsegae and Alibaba — Grand Opus Holdings — brings G-Market and AliExpress Korea under one roof. Financial News — 50:50 JV

- E-Mart gets Alibaba’s global sourcing for non-food price competitiveness.

- Alibaba gets Korean trust and logistics.

- G-Market’s 50M+ member DB × Alibaba’s AI targeting — a powerful synergy on paper.

However, the KFTC made physical separation of Korean consumer data a condition of merger approval — limiting near-term personalisation synergy. Shin & Kim newsletter, KED Global — data-sharing ban, Seoul Economic Daily — conditional approval

3. End-market — restructuring of Korean retail (2026–2030)

3.1 The ‘zero-growth’ era and M.I.N.D

Korean retail real growth is converging to ~0% from 2026. Shinsegae’s industry think-tank prescribes M.I.N.D.

- M (Multi-channel): grocery leadership across on/offline — offline fresh strength pushed into online.

- I (Inbound): ~20M annual foreign tourists as new consumers — make Starfield/E-Mart tourist hubs.

- N (Next-gen tech): AI/robotics to offset wage inflation — checkout-free, AI inventory.

- D (Dwell-time): longer dwell = more sales — ‘Starfield Market’ etc. Shinsegae newsroom — 2026 outlook

3.2 Demographic shift

- Single-person households: 36% in 2025 → ~40% by 2030. Chosun English — single households 36.1%

- Population aged 65+ exceeds 10M → super-ageing society.

- Polarisation: near-store small baskets (CVS/SSM) and warehouse-club bulk buys.

- Traders is the prime beneficiary — quarterly revenue surpassed KRW 1T; targets KRW 10T sales / 50 stores by 2030. NBN — 3Q OP KRW 151.4B (+35.5%), ETNews — 2030 KRW 10T

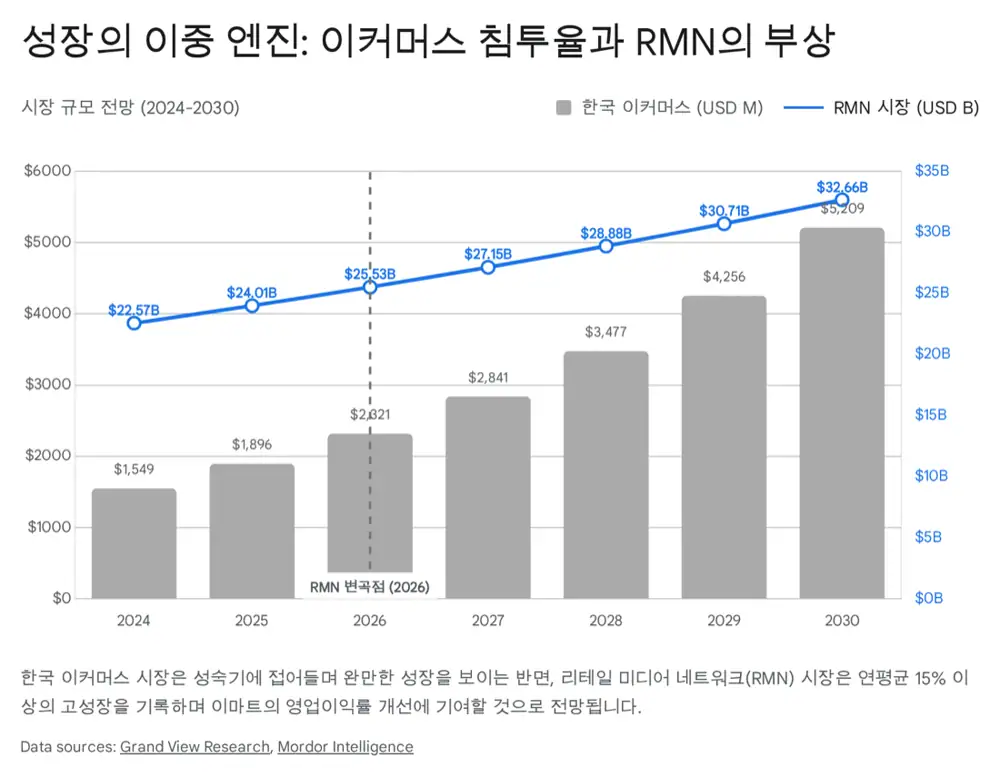

3.3 RMN — retail’s new profit engine

Retail media networks (RMN), validated by Amazon and Walmart, are entering bloom in Korea — 15%+ CAGR expected from 2026. E-Mart’s integrated on/offline customer data supports sophisticated targeting and structurally lifts OPM — analysts see hundreds of billions of KRW in additional OP. Mordor Intelligence — RMN, Fugo.ai — 2026 RMN trends, Insight Korea — E-Mart RMN

4. Impact analysis — Q · P · C

4.1 Q (volume)

- Offline: Starfield Market refurb → dwell-time and basket size up; inbound-tourism boost.

- Reverse direct purchase: 2024 USD 294M (+26%) — E-Mart taps Korean exports via the G-Market / Ali alliance. Business Korea — reverse-direct purchase near $3B

- Online: Alibaba JV rebounds G-Market traffic — AliExpress low-price items pull Coupang-lapsed customers back.

4.2 P (price / margin)

- Move toward ‘profitable revenue’. Integrated sourcing defends margin while staying price-competitive.

- Higher PB share — No Brand / Peacock margins.

- Traders paid membership → loyalty + ticket size.

- RMN — separate high-margin line, lifts blended OPM.

4.3 C (cost)

- Logistics: 3PL transition turns fixed costs into variable costs.

- Workforce: voluntary retirement + store-level efficiencies reduce wage share.

- Real-estate monetisation: Gayang, Seongsu etc. sale/redevelopment — proceeds pay down debt.

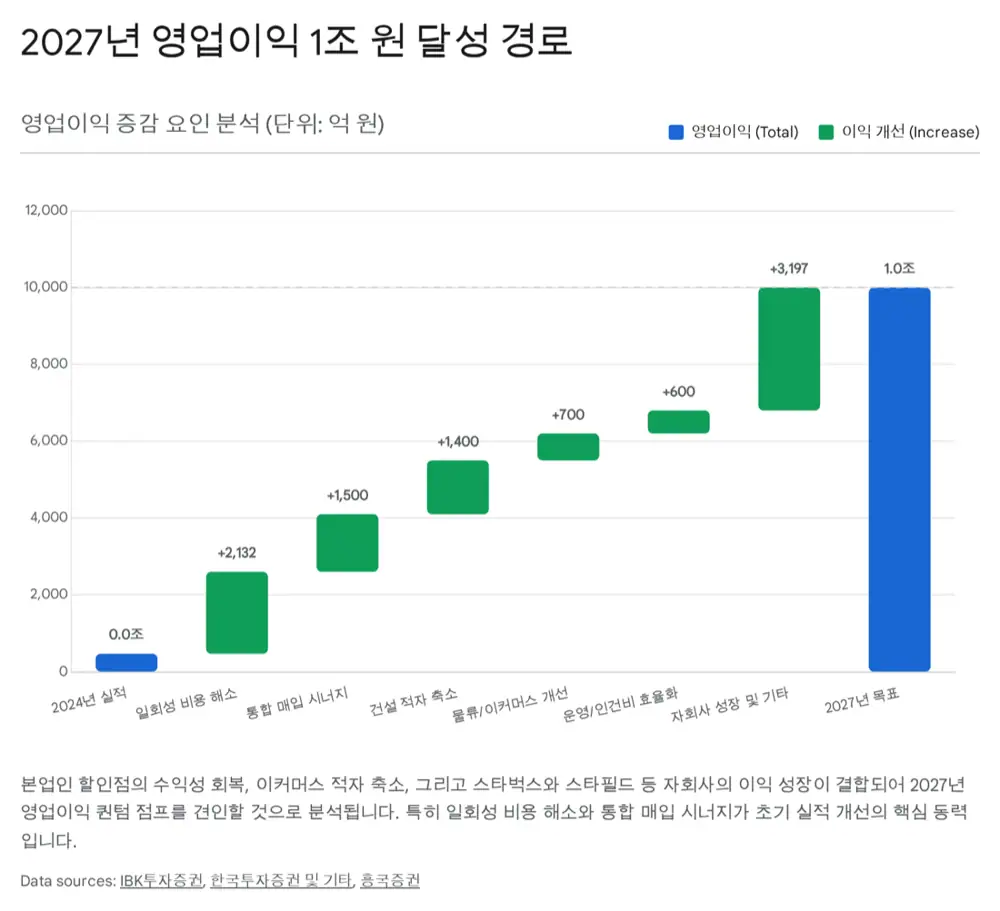

4.4 Reality check on the 2027 guidance

| Bucket | Expected OP |

|---|---|

| Core (Discount + Traders) recovery | KRW 400–500B |

| E-commerce loss narrowing (BEP) | ~+KRW 100B+ |

| Starbucks, Shinsegae Property etc. | KRW 400B+ |

| Shinsegae Construction loss resolution | +α |

| Company guide (2027) | KRW 1T |

| Sell-side consensus | KRW 660–760B |

From 2024 OP of ~KRW 47.1B, consensus alone implies 14–16× growth. IBK Securities — TP 83k → 95k, Heungkuk — 2027 KRW 1T target, EBN — 4Q OP to beat consensus, Hankyung — 52-week high, Hana Sec BUY

5. Balance sheet & capital allocation

5.1 Liquidity

In Jan 2026 E-Mart issued KRW 400B in corporate bonds — markets still trust the credit. Debt ratio of 157.4% (2024) is elevated, but Traders / Starbucks cash flows are solid. Capex diet steadily improves net debt.

5.2 Value-up programme

- By 2027, 20% of annual OP returned to shareholders.

- Minimum DPS raised from KRW 2,000 → 2,500 (+25%).

- Cancel 50%+ of treasury shares (~560k shares, ~2% of total) — directly improves EPS / ROE.

- DealSite TV — dividend raise + treasury cancel, NewsWatch — 50%+ cancel, News1 — value-up plan, Magazine Hankyung

6. Valuation & conclusion

6.1 The 0.2× P/B paradox — Walmart benchmark

0.16–0.2× is among the most depressed of any global retailer. Walmart spent 2015–2020 in a low-multiple zone while building omnichannel; the multiple lifted sharply once on/offline synergies kicked in around 2018. TSI Network — Walmart e-commerce +25%, Simply Wall St — Walmart 2025

6.2 SOTP — the ‘zero core value’ trap

- SCK Company (Starbucks Korea) stake: ~KRW 2–3T in value. TIKR — Starbucks 2026 outlook

- Traders + E-Mart: annual EBITDA KRW 1.5T+.

- Real estate: book value alone in the trillions — already above the current market cap (~KRW 2T+).

Today’s price implicitly values E-Mart’s core operations at zero or negative — clear oversold territory.

6.3 Risks

- KFTC data separation: halves the personalisation synergy of the Alibaba JV.

- Coupang defence: membership boosts and logistics investment continue — online share recovery won’t be smooth. Alpha Biz — Coupang vs C-commerce, PESTEL — Emart landscape, DataInsights — Korea e-commerce 2026–2034

6.4 Final view — bet on ‘M.I.N.D’

Own grocery

Use the offline footprint to defend fresh-food leadership.

Non-food = alliances

Use Alibaba/CJ alliances to compete cost-efficiently.

Visible value-up

20% payout + 50%+ treasury cancellation.

The next 3–5 years decide whether E-Mart becomes ‘Korea’s Walmart.’ KRW 1T 2027 OP is an aspiration; even structural cost cuts plus subsidiary contribution already justify base-up. View: BUY. A long-horizon position to watch the restructuring of Korean retail.

Sources

- Naver blog source: m.blog.naver.com/.../224174135313

- DealSite TV — dividend raise + treasury cancel: news.dealsitetv.com

- Chosun Biz — G-Market Sunday delivery: biz.chosun.com

- Dealsite — CJ Logistics handling Star Delivery: dealsite.co.kr

- IBK Securities — TP 83k → 95k: biz.chosun.com

- Financial News — Shinsegae-Alibaba 50:50 JV: fnnews.com

- Shin & Kim newsletter — KFTC first data-integration remedy: shinkim.com

- KED Global — data-sharing ban: kedglobal.com

- Seoul Economic Daily — conditional approval: m.sedaily.com

- Shinsegae newsroom — 2026 retail prism M.I.N.D: shinsegaegroupnewsroom.com

- Chosun English — single-person households 36.1%: chosun.com

- NBN — Traders 3Q OP KRW 151.4B: nbnews.kr

- ETNews — Traders KRW 10T by 2030: etnews.com

- Mordor Intelligence — RMN: mordorintelligence.com

- Fugo.ai — 2026 RMN trends: fugo.ai

- Insight Korea — E-Mart RMN: insightkorea.co.kr

- Business Korea — reverse-direct purchase near $3B: businesskorea.co.kr

- EBN — 4Q OP to beat consensus: ebn.co.kr

- Business Post — Heungkuk 2027 KRW 1T target: businesspost.co.kr

- NewsWatch — 50%+ treasury cancel: newswatch.kr

- PESTEL — Emart competitive landscape: pestel-analysis.com

- Hankyung — 52-week high, Hana Sec BUY: hankyung.com

- DataInsights — Korea e-commerce 2026–2034: datainsightsmarket.com

- Magazine Hankyung — value-up announcement: magazine.hankyung.com

- News1 — value-up plan: news1.kr

- TSI Network — Walmart e-commerce +25%: tsinetwork.ca

- Simply Wall St — Walmart 2025: simplywall.st

- TIKR — Starbucks 2026 outlook: tikr.com

- Alpha Biz — Coupang vs C-commerce: alphabiz.co.kr